Publications & Thought Leadership

The Art and Science of Communication – How the Wealth Management Industry Can Adapt and Improve

Jul 22, 2021

The Hubbis Digital Dialogue of July 8 took an in-depth look at the art and science of communicating with private clients in today’s world. The ability to communicate effectively must be first and foremost on the list of must-haves, and it is not simply the right digital tools, but understanding when to speak up and being able to tackle complex subjects and potentially awkward topics with sensitivity. And communication is not only about the multiple channels of delivery; it is about empowering the RMs and advisors and providing carefully curated advice and information that is truly relevant and suitable, with the banks and other incumbents leveraging client behaviour, data, analytics, AI, machine learning, and a host of client-friendly digital media, which are all so vital for client engagement and loyalty.

Panellists

- Anna Sacha, Senior Consultant, Comarch

- Sharon Chan, Head of Wealth Segment, DBS Bank

- Mark Wightman, Asia-Pacific Wealth & Asset Management Consulting Leader, EY

- Lawrence Yin, Regional Sales Director, InvestCloud

Opening the discussion, an expert observed that nowadays, everybody believes that communication cannot properly exist without technology, with even very simple forms of communication, such as video conferencing, chatting, emailing, calls, all are made possible by technology. Delivery of more sophisticated communication in the wealth industry, for example, investment insights, investment updates, investment ideas, and advice; in fact, all types of engagement with clients can be delivered digitally rather than personally, they remarked. This is all especially vital at these times of the pandemic, which has currently largely closed the door on face-to-face personal interactions between clients and their wealth managers, especially for those outside national borders.

Today’s ‘diverse’ communication

“If you ask me how technology can make communication better, I will say that it, first of all, brings diversity,” this expert observed. “Diversity, meaning it gives you different outlets, different gateways, where you can push the information, push the communication you want to run through to your clients. Here, I mean, for example, customer portals, mobile applications, chatbots, pitch bots, different interfaces that you can use for the communication with the customers.”

This diversity also extends to the information that is transferring to customers, which should already be refined and filtered by the financial institution and the wealth managers for the clients, and therefore more relevant and thereby helping to make the clients more engaged with the offerings.

Expert Opinion - Anna Sacha, Senior Consultant, Comarch: “Technology can improve communication. Technology brings diversity in terms of number of gateways which can be used for communication with customers. To name a few: web portals, mobile application, chatbots, video rooms. It also enables automated and targeted communication by generating and sharing investment content and portfolio updates at scale with little or no human intervention.”

Amidst a plethora of information, less is more

Another expert observed that “less is more” today, as clients are flooded with so much information. But they agreed that the successful wealth manager should be able to filter what really matters to the client and deliver it to them in a very timely manner, in a form that is simple to understand, and with the elimination of lots of financial or other jargon that used to pervade the wealth industry in a ‘blinding by science’ type mentality.

Indeed, this expert observed that whereas in the past, there was a tendency to use complex words and ideas to communicate, that is no longer considered ‘cool’. “We see increasingly across the entire wealth spectrum that everybody prefers things delivered more bite-size and more easily understood,” she explained. “It has become about how we can put the message across efficiently and through the channels that actually can reach the clients, that engage them so that it is really effective for them.”

She advised that instead of sending a 100-page report covering the entire span of the CRO ideas and recommendations, that can be broken down into bite-sized delivery of relevant ideas, personalised messages, having filtered out what really matters to the clients. “News and information are everywhere,” she said, “but insights are essential.”

Expert Opinion - Mark Wightman, Asia-Pacific Wealth & Asset Management Consulting Leader, EY: “Wealth managers need to understand what their clients consider as hygiene functionality and focus on differentiated experiences. We must use data better to provide a relevant insightful timely wealth service to clients. Clients will be willing to pay more for an integrated and overall better experience.”

‘Bite-sizing’ communication

Another guest agreed and observed that the proliferation of information these days can often get in the way of effective communication between the advisory community and the clients.

“When you want to communicate with clients, you really need to communicate what is relevant, and the great thing is to be able to do that in a bite-sized manner and on a timely basis,” he reported. “I think what happened with the pandemic, I think, has taught us a lesson on the importance of sort of digital tools to enable RMs to be able to do that in a very curated and highly personalised way. Regarding the trend towards what we call conversational banking, we are part of the drive to help our clients empower RMs to have more conversations and more meaningful conversations with their clients.”

The quest for personalisation and hyper-personalisation

And the digital revolution is clearly helping deliver personalisation and more targeted communication at a greater scale. “Personalisation is super important now,” a panel member stated, “and with the use of new technologies such as machine learning and artificial intelligence, we can reach out to the customer segments with a higher personalisation level than ever before. Looking ahead with a longer-term perspective, I believe that basically all of the information that we currently convey to customers in a personal way, in a personal manner, all that information can be actually moved effectively to the digital channel, and this should be already happening.”

He said providers could start with sharing investment recommendations prepared by RMs and push them to the customer channels; they can talk about market updates, investment insights, different types of information, all delivered through the digital channels. “And you can see what kind of adoption rate you actually experience relating to the information delivered,” he added. “It is important to be monitoring and adapting all the time to the trends that emerge.”

A guest mined down into what the difference might be between personalisation and hyper-personalisation. Personalisation is about reaching out to people of a similar type of profile and based on that type of persona, delivering ideas that appear to fit what they would be interested in, they explained. But hyper-personalisation then zooms in on specific details about the individual, a greater understanding of what makes them tick, what catches their attention and would make them read certain reports and messages, and therefore how to connect to them more effectively. That's hyper-personalisation.”

Expert Opinion - Anna Sacha, Senior Consultant, Comarch: “Are the banks and other incumbents investing wisely in boosting their channels and protocols surrounding communication? Yes, short-term, these investments have focused on switching from personal to virtual interactions - which already pays off in terms of cost savings and the value delivered to customers.”

Is your communication truly relevant?

“One word that really strikes in this discussion on communication in the wealth industry is relevance,” a guest told delegates. “In short, we know there is just too much information, and that people receive it constantly from every quarter, but to be of value, it has to be relevant, it has to be meaningful for the client.”

To be relevant, he said the bankers and advisors must first understand the clients, their personas, their individual journeys and so forth. And as to delivery, clients appear to like the hybrid relationship, in other words, part digital delivery and part personal delivery.

A guest pointed to ESG, which nowadays appears in some form or another in virtually every wealth management discussion. He referred to a survey his firm had conducted that showed how important sustainability is to clients in the region these days, but that also highlighted how wealth providers are not necessarily doing a very good job of delivering on those goals. “That is one example of where data and information from the providers are lacking, where they are not fulfilling the needs for those particular client goals.” In short, be relevant and engaged.

Automation, scale and democratising wealth management in Asia

Technology clearly enables greater automation, an expert commented. “Technology brings automation to communication, so if you want to communicate your customers at scale if you offer wealth management services to a wider spectrum of customers, technology is definitely here to support that,” she said. “For example, generating notifications to your customers, generating portfolio updates, investment insights, investment reports, these all can be easily automated and pushed to the customer channel with basically no human intervention nowadays.”

This is all about the democratisation of the wealth management offering that is taking place, said one guest. He said there is very evidently a greater role today for technology across the different wealth segments, with communication tailored to those segments.

A panellist explained that the democratisation of wealth management across lower segments of wealth was core to the wealth management industry’s future proposition. Whereas certain products and advice had only been available to the very wealthy clients, there is an increasingly broad offering being delivered gradually across the mass affluent market as well, with these customers having greater accessibility, enabled by technology as well as the provider’s strategy implementation.

Expanding the offering, broadening the client base

Another factor is the democratisation of a wider range of investment opportunities across lower categories of wealth. For example, a guest reported how private banks are looking at how they can offer their mass affluent customers alternative assets that hitherto have been targeted only at the HNW and above segments. He said education around financial literacy, more technology, greater digitisation, greater agility; all these will be drivers to help these banks offer a better range of products and ideas across the various categories of wealth in the region.

“It comes back to the bite-size offering,” another guest remarked. “Wealth management and getting started on the investment journey do not have to be daunting for customers. You do not now need a million dollars before you can even start; you can start small. It is not about just serving the top small percentage of the population but really making wealth management accessible to everyone. For us, it is about helping people on these journeys, regardless of what levels of wealth they already represent.”

Expert Opinion - Anna Sacha, Senior Consultant, Comarch: “What we should aim for within the enhanced communication is a hybrid approach that blends personal, high-touch approach with digital capabilities that the technology brings. Let’s empower RMs to make their interactions with customers more efficient, timely and relevant.”

The ‘Hybrid’ model

Another guest placed the discussion in a more commercial context, pondering how the wealth industry can provide the necessary insights efficiently to as many as possible and at the right cost levels. “Given the high level of personalisation that’s required nowadays, it's very hard to do this on a one-to-one basis,” she reported. “So, it comes down to how at the centralised level, we can do this efficiently across various channels, making sure that messaging is consistent yet personalised. The successful wealth managers should focus on and leverage that.”

Technology is here also to support the personal approach, but it is not here to replace RMs and to keep them away from the customers, another expert observed. “Let's not forget about empowering RMs within the communication they deliver to their clients,” they said. “It's not only about delivering everything fully online, in the customer channel, it's also about empowering RM in the whole discussion about communication.”

A fellow guest agreed and commented on the drive to help RMs and advisors be more personalised in their approach to clients and more efficient in their day-to-day activities and productivity. “The delivery today is perhaps 50% centrally driven and 50% relationship manager driven,” they said, “and what I mean by that is it is humanly impossible to deliver 24/7, so there needs to be a reliance on centralised operations to reach out to customers.

Leveraging RM communication with digital tools and the right approach

Meanwhile, the effective and efficient RM will be supported by the necessary tools to empower them to achieve their goals.”

An expert expanded on this, explaining that such tools might include CRM – customer relationship management - systems, where they can record and remember engagements with clients and details. These details might, for example, include birthdays of family members, perhaps the purchase of a new car or house, and so forth, thereby helping the RMs deliver a more intimate, personal level of communication. But these details do not need to be in the RMs’ heads; it can be all stored and filtered through a centralised CRM system, so that information in there can be extracted or prompted in a timely manner.

Another panel member also observed that clients connect with the banks across a variety of touchpoints. There needs to be cohesiveness, but not repetition, across the organisation, she explained. So that perhaps when a client contacts the call centre, the person taking the call can immediately understand the more personal context for the call with the help of technology, and the RM can then follow up in greater detail and greater personalisation.

Cohesive communications and understandable messaging

“The cohesiveness across channels and different touchpoints must be there,” they elaborated. “And that means the RMs also need to share information; it is not like in the former times of private banking when the RMs kept all the really personal information on clients to themselves, in the proverbial little black book, so to speak, like state secrets. But now, the reality is different; the truth is that it is incredibly difficult today for RMs to really handle portfolios of clients and handle so much data and so much information; they need to be much more efficient and really make use of the tools that are available, leveraging the centralised team functions so that half of their jobs can be done for them.”

But the experts agreed added that the other 50%, the half of the relationship that is definitely face-to-face, or remotely face-to-face these days, is still incredibly valuable to the clients. “The human touch remains vital, so the combination approach allows for RMs to amplify from the personalised to the hyper-personalised, which is really appreciated by these clients, regardless of what levels of wealth they represent,” a panellist remarked.

Hybrid moves to the next level

A guest offered his views on the hybrid approach, commenting that the banks are actually now taking customer service and or client communication to the next level. “For example, we are working with a number of firms at the moment to help transform their more traditional type of client-facing reports, the pdf or other documents, perhaps after an investment proposal conversation, and evolve those into more digital documents whereby the RMs can easily add a very personalised touch into those digital documents and co-create with the client,” he explained.

He said this does not add more burden to the RM, as all the key elements are there anyway as required by the compliance and administrative departments of the banks, but the RM can easily add a personalised message, for example, to that report, because if they’ve just spent two hours with a client talking about their financial future. In this way, they can deliver more personalised content that really links the ideas and proposals to those individuals.

Conversational banking

A panellist explained that amongst clients his firm works with across the wealth management field, there had been an accelerating drive towards what is known as ‘conversational banking’. “There's been a lot of focus amongst clients being able to provide voice communication through WhatsApp, WeChat and so forth,” he explained. “There are levels to those conversations. Initially, it is simply having secure conversations with RMs and advisors. Secondly, can information and details be exchanged securely and thirdly, can the clients then transact safely and simply? So, with the remote work practices nowadays, we see this drive to conversational and then transactional banking.”

As to segmentation, another guest commented that the providers need to understand what their different clients expect. He said many of the millennials, and particularly those in North Asia and China, have a greater propensity to go digital-first, so we have to be cognisant of how the particular clients think in terms of communication. We need to allow clients the ability to converse with their bankers and wealth management firms in the ways that they prefer, and some might be highly digital, some might be more traditional and personal.”

To achieve this, he explains, there is the need to provide more bite-sized research, additional bite-sized information and sharper insights to the RMs, and therefore the clients, in a very timely manner. “Those efforts open up greater opportunity to have these relevant and timely conversations with the clients, and thereby really build trust with them, and the ‘stickiness’ the wealth industry hopes for. That ultimately means your clients do more business with you and more of that with your bank or firm. And if this is all implemented correctly, some of these solutions can actually make RMs more efficient, for example so they don't have to log into multiple platforms to communicate with the clients, and other advances, therefore saving time and money as well.”

High-touch and co-creation, albeit from afar

An expert explained that the RMs could, for example, add elements such as relevant research, rich media such as a voice memo or a video, and as these are then shared with the client digitally, the client can then comment, ask questions, raise suggestions, so there is a genuine two-way flow. “This is the co-creation experience between the RM and the client, elevating the delivery of information and follow-up documents to a far more engaging and relevant client experience,” he explained. “That is just one example of how we can sort of use technology these days to empower RMs to bring that whole client communication to a new level.”

He observed that traditionally, the private banking industry had placed all of its reliance on RMs to provide the ‘high-touch’ experience to private clients, and because of the pandemic and its dramatic impact on meetings and travel, the RMs are under increasing pressure to handle the clients remotely.

“Tools that genuinely empower RMs when it comes to client communication have therefore become far more essential and valuable,” a guest observed. “As a result, I think we are heading in a direction where advice and investment insights are delivered in a more relevant, more tailored, more engaging, and more timely way. We actually see this as a tremendous opportunity for the wealth industry to really enhance this client communication experience, leveraging technology to do this in a much more curated and personalised fashion and delivering personalisation at scale.”

He pointed also to the use of what he termed ‘explainable AI’. “If, for example, we can take a bank's research and break that down into bite-sized snippets, and match that with their clients, aided perhaps by CRM and other client history and information, and then deliver those bite-sized insights and ideas to clients in a very timely fashion, conveying clearly why they are so relevant to them, then we open the doors to a lot more conversations for the RMs to have with clients, and of course, considerably more engaging conversations that are more likely form a business perspective to bear fruit, thereby making more win-win situations for the banks, the RMs and most importantly for the clients themselves.”

Secure communications

A panel member zoomed in on data, and the challenges around exchanging data efficiently and securely with clients. “Many private clients are actually multi-jurisdictional,” he commented, “perhaps with homes in Singapore, the UK, Hong Kong and so forth. We then have to think about regulations around data and privacy. We have to think also about what data clients are comfortable sharing.”

And although he said the term hyper-personalisation is perhaps very overused these days, the banks must do better at assembling data on their customers, including ultimately how they want to be communicated with, in order to deliver the relevant, insightful, value-added timely and valuable information, ideas and advice.

The Hubbis Post-Event Survey

Hubbis: In brief, what are the vital elements for the wealth management industry to maintain and boost client relationships during these times of pandemic and remote working?

- To be right up to date and have timely communication with clients.

- Timely response and market insights with the quality that provides a real edge.

- To maintain regular communication with clients and to be sensitive to their changing needs.

- Delivery of personalised and relevant advice.

- Voice contact is essential, not just emails and messages.

- Zoom calls are not welcomes by clients, unless they specifically request those.

- Regular updates on trends and market news.

- Keeping up to date with the client’s situation, both investments, family and business.

- Being a good listener for clients is vital.

- Client communication should be driven by the ‘less is more’ principle.

- Invest in digital technology to make RMs more efficient and also to be able to deliver a hyper-personalised offering.

- To promote a central operations driven client engagement and 50:50 with driven by the RMs.

- Very important in these times is always to keep in touch and not only talk about investments but care and welfare.

- Ongoing training is important to enhance communication skills.

- Those banks and firms who take in trainees and build their skills internally have a better and

- more wholesome approach compared to those who buy out teams to expand.

- In my opinion, the wealth management industry is not doing enough to equip the RMs with the soft skills necessary. The industry needs to really focus on boosting soft skills.

- We need to be careful. It takes two to tango. Some clients are very private and don’t want to share everything with their RMs, but those who manage to get their clients to open up have a far better chance of sustaining a good business relationship.

- Technology has to help RMs free up time away from compliance and admin, which is all too often making them bogged down.

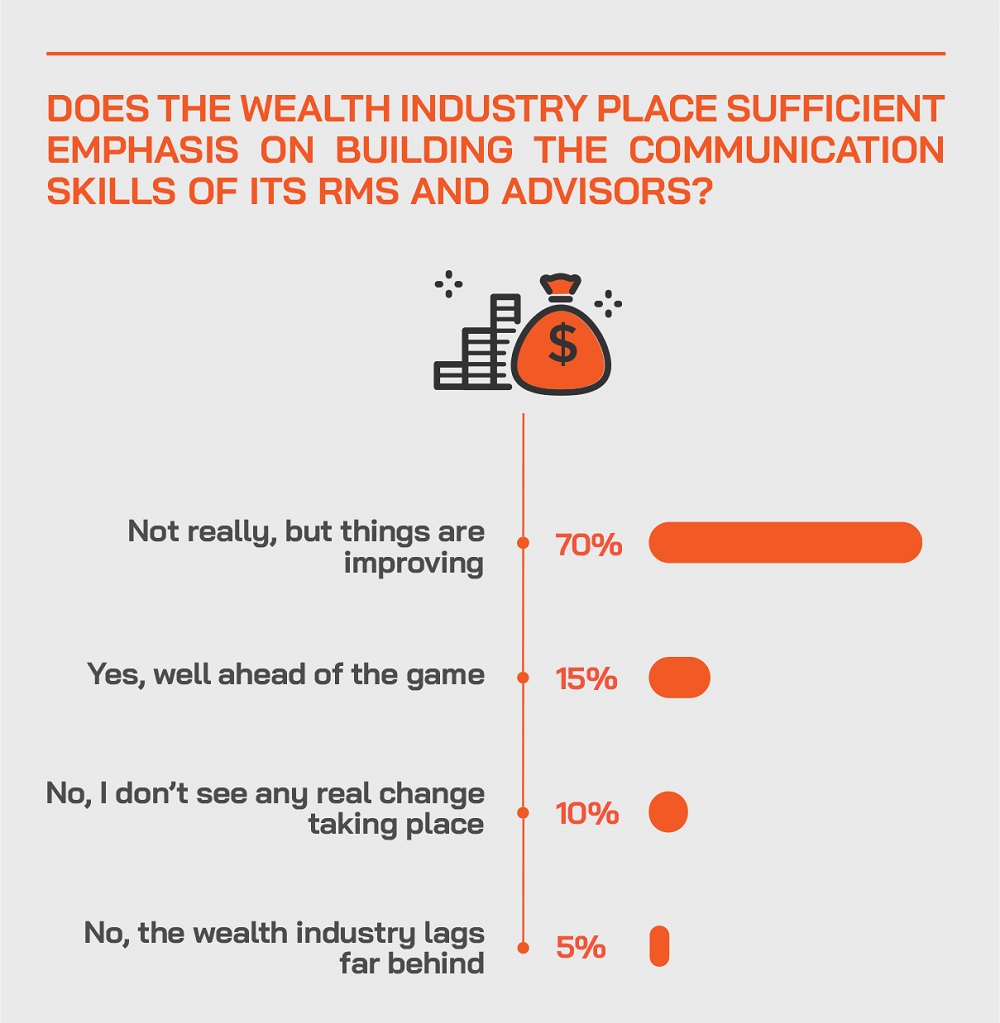

Hubbis: What key ‘soft’ skills of communication are required of the RMs and advisors?

- Listening

- Empathy

- Consistency

- Timely response

- Timing the delivery of information and ideas

- The art of listening – this is a skill that can be learnt but rarely taught

- Ability in times of crisis to provide good advice and say the right things

- Listen, understand and only then offer advice

- Patience

- The ability to communicate trustworthiness

- Skills in delivering complex information, ideas and structures succinctly

- Constant radar on client needs, goals and aspirations

- Ability to persuade when there is genuine conviction

- EQ as much as IQ

- Interpersonal skills, the communication of genuine interest and ‘care’

- Modest and humble communication of expertise and knowledge

- Patience, empathy, and understanding

- Privacy and integrity

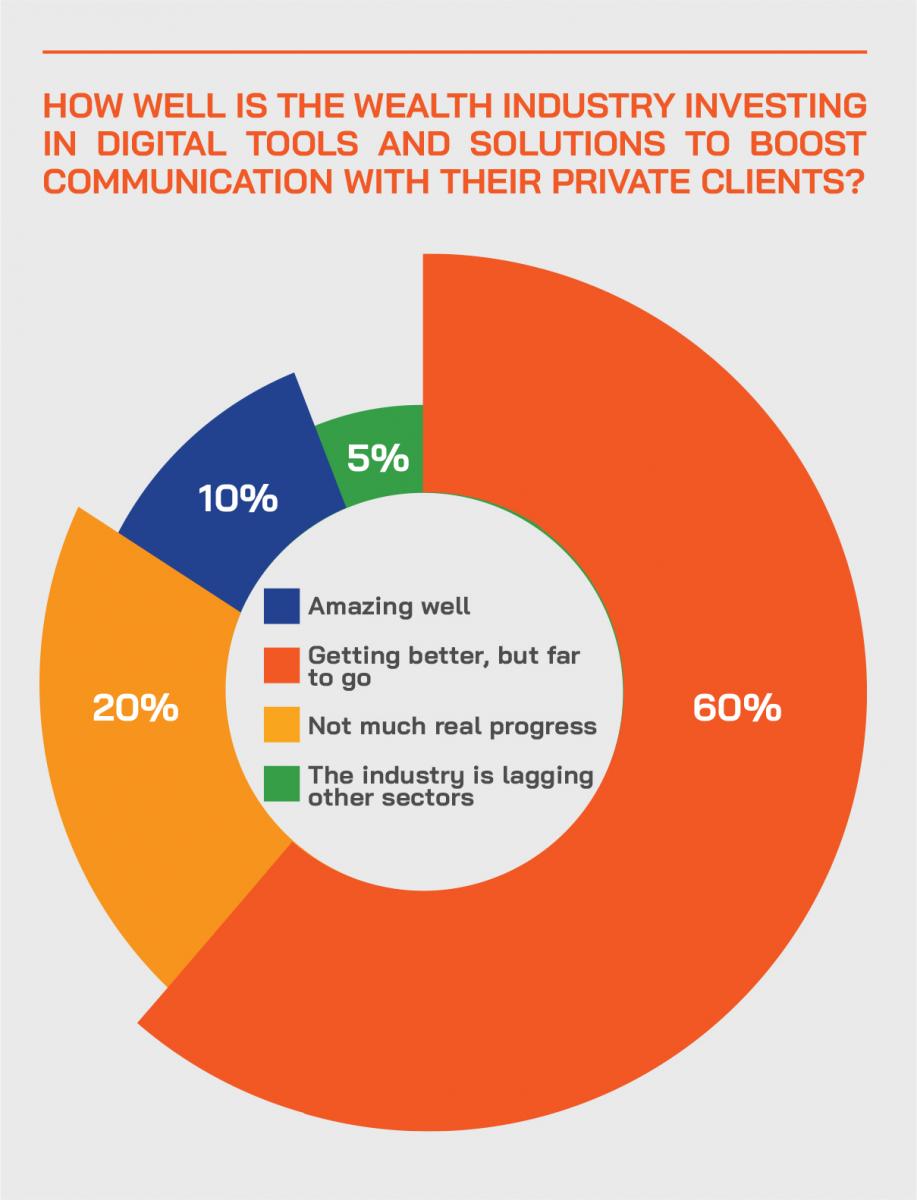

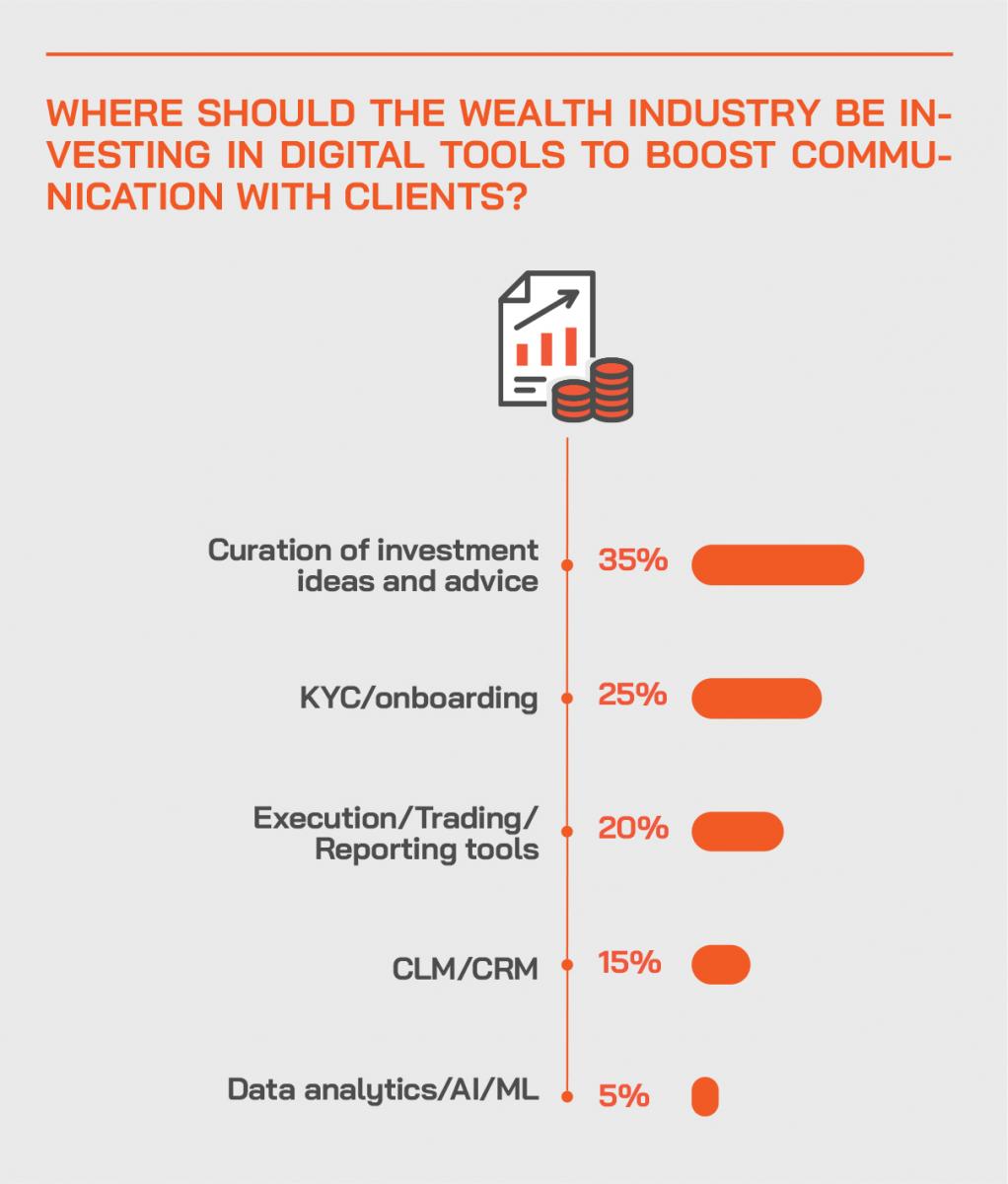

In which areas should the wealth industry invest in digital tools to help boost client connectivity and enhance communication?

- Constant performance updates

- Robo-advisory

- CRM

- Easy access to research

- Video calls and webinar.

- Timely advice

- Video conferencing, virtual event tools

- AI

- Enhanced trading systems

- Asset and Portfolio management

- Across the board

- Enhancing and empowering the RMs

- Client Lifecycle Management

- Data Analytics

- Online Onboarding and KYC

- Curation of investment ideas

- Ease of use and access

- Expert views and insights on a timely basis, ease of delivery, simplicity of communication

- Online transactions, everything at the fingertips

- Secure email convenience

- More AI access

- Improve usage of digital technologies such as data analytics, AI and so forth

- Better and timely advice, through automation and friendly CRM systems

- Communication with clients using their preferred apps

- Digital onboarding and AI

- The rollout of the hybrid advice model, which is going to be future of wealth management

Adopting the right strategies, making good decisions

A panel member also tackled the thorny issue of how wealth managers actually go about their digitisation. “People are doubling down on Asia because they see this is where the growth will be,” he comments. “But at the same time, they have to look at costs and that is certainly the case for the digitisation journey. In theory at least, greater automation should de-risk the businesses and drive those efficiencies, but it is very important to always look at this thrust through the lens of the cost and the value to be extracted.”

He commented that there are three key elements to the development of effective solutions – the needs and expectations of the clients, the needs of the business and RMs to help deliver efficiently and effectively on those clients ‘wants’, and a robust perspective on what is happening amongst competitors in the wealth industry. “Clearly, if we are working with the ‘C’ suite decision-makers, they need to really understand these three key elements in order to formulate strategy,” he stated.

And he advised that there needs to be greater consistency in how the banks approach clients across the different segments of wealth. He said that often when clients move within banks from mass affluent to HNW status, they so often effectively have to onboard again; it is almost like opening an account with another bank entirely.

Keeping it all as simple as possible

He advised that the banks must therefore aim to make that all simpler, and while there is so much excitement in Asia and so much hiring taking place, bank clients must take a long, hard look at the model they want to roll out, the service model they want to offer and how they will really boost their advisors and RMs.

And then, throughout each organisation, he said they need to build and demonstrate a real consistency of experience and services as customers move through the wealth continuum. Clearly, the wealthier the clients become, the more sophisticated the services, products and advice they will be offered. And as advice becomes more important to the clients, as a broader portfolio approach is taken to their investments, it is vital that goals and objectives and risks are aligned properly with tailored, relevant ideas and recommendations. Technology, he said, can help wealth management organisations achieve those aims as long as the right approaches and the right strategies are put in place at the outset.

The discussion closed with a comment from an expert who reiterated the importance of aligning the commercial models and strategic business goals, and in striving to achieve that, technology can certainly help but it is an enabler that helps the wealth industry achieve these goals in a more holistic manner. And ultimately, the panel agreed, it all comes down to the right messages and the right content and the right modes and delivery of communication.