Strategy & Practice Management

Wealth Management in Asia - Where does our Industry Go from Here?

May 19, 2020

Hubbis assembled five eminent Asian wealth management experts to tackle the first of the new Hubbis Digital Dialogues Series on May 14, casting their experienced eyes over the impact of Covid-19 on the wealth management industry, and reviewing some of the implications for the foreseeable future while the world struggles with the pandemic. If there was one overriding conclusion from the discussion, it was that the direction of the wealth industry remains largely the same, but the trends will have accelerated and the need for significant change become even more compelling and time-sensitive. Our panel of experts comprised two private bank CEOs, the head of business development at a Singapore-based EAM, the Asia Pacific head of a major online execution and custody platform, and the ex-Asia head of a global private bank who now runs his own fintech communications platform. Together they represented more than 125 years of combined wealth management expertise, of which the majority of those years have been spent in the Asia Pacific region. The discussion was moderated by the Hubbis founder & CEO, Michael Stanhope.

The Big Picture – Where are We Now?

Six Signs (to the Future)

- The trends remain, the pace of change is accelerating

- Technology and digitisation are pre-requisites for being competitive

- Business continuity planning is vital

- The personal touch will prevail but in lockdown leverage all media

- Big brands and the independents will be the winners, and new entrants will multiply

- The wealth industry is very likely to see more consolidation

To open proceedings, we first asked the experts to give their assessment of the current environment. The first comment was that fundamentally not much is changing, but the changes that were already happening are now accelerating quite significantly. Digitisation has been a core focus for the wealth management (WM) community for several years, and now effective, smart digital solutions and client interface are even more in the spotlight. “You must deliver digital solutions in order to be able to compete,” said one expert.

The second major change is the proliferation of the home office, which an expert argued will result in many banks and firms later reducing office space, even after the pandemic (hopefully) abates.

Another guest noted how his bank’s legal and compliance functions had, in fact, functioned reasonably well in Singapore since the lockdown, as most of the processes and many of the documents are managed digitally, with any physical documents also handled by a skeleton staff representing about one-third of the overall team at the office.

One panel member opened his commentary by stating that he refuses to believe this situation will persist. “This is not the future and not the future of wealth management,” he said. “I am on Zoom or other digital interface all day, but let’s be honest, nothing replaces the personal interaction with the client or a business partner. Moreover, we cannot do much more than maintain existing relationships; it is incredibly difficult to build new relationships. And hiring new people is very tough, as one simply does not get the right degree of insight to them as people and as potential colleagues from a video call. On the point of working from home, there are however, some advantages, especially in time management. Overall, I would generally summarise that the negatives outweigh the positives.”

He added that Singapore has been remarkably proactive and effective at supporting businesses and people with financial measures, grants and subsidies. “We did not need to let anyone go from the bank,” he remarked, “and we are even attempting to attract talent in some areas through all of this,” he reported.

Talking about his firm’s digital, global custody and execution platform, an expert noted that the crisis had put the company’s technology and business continuity protocols through extreme duress, but that the systems and processes had stood up very well to the test. “Everything has functioned very smoothly,” he reported, “so this brings to focus the great importance of businesses having business robust continuity plans in place.”

It appears that the global brand-name private banks will battle it out for HNW and UHNW clients with the independent asset managers and MFOs, as 65% of respondents see these providers as the winners in the future. Meanwhile, the market expects considerably more competition from new entrants in the form of fintechs, Big Tech and other disrupters.

There is a very widespread expectation of continuing modest or perhaps significant consolidation in the wealth management industry in Asia in the coming years.

Building Value-Added and Diversifying Revenues

The discussion shifted to the need for wealth management businesses to build their value-added proposition and thereby protect and build their revenue streams.

The panel conceded that nobody could predict the future course of the virus and the exact implications. “We do not know how regular or big the waves of the virus will be and where,” he warned, “so we have to work closely with clients to manage the risks and rebalancing portfolios, that is a key area where we can add value in the months ahead. And actually, clients have a bit more time as they are locked up at home mostly, with many of their future-focused concerns front of mind, including estate planning, succession planning and so forth. In short, this is a good time to talk with clients about markets and about their lives, their hopes, expectations, and to help guide them through this crisis.”

“Yes, I completely agree,” said another expert. “This is the time to really build up that holistic relationship, to really try to reach out and understand the clients, their families, and then to leverage our professional relationships to bring all types of expertise to bear for them, whether lawyers, trust experts, fiduciary people, accountants, immigration experts or others. We must bring our whole network and knowledge to the table for these clients. This is certainly not the time to be pushing product to them.”

Six Signs (to the Future)

- The client must be front of mind in all wealth management activity

- Providers must broaden their proposition far beyond investments, deep into wealth and estate planning

- The RM will remain incredibly important for HNW and UHNW clients

- But to be trusted advisers they must offer value-added advice, insights and solutions

- DPM and advisory will see a post-Covid-19 surge

- The vital importance of professionalism and consistency cannot be overstated

Audience Comment - The value of independence

“From a family office perspective, our business is countercyclical to the markets. Generally, in times of stress, the probability of signing up prospects is higher. Due to the conflict of interest that exists in the private banking industry, generally client portfolios under the supervision of independent advisors tend to perform much better. The current situation has reinforced this view with clients experiencing this first-hand. This will keep the business robust and on a sustainable growth path. More and more clients are realising the importance of independent advice.”

“Clients have had to get used more to the distant connection to their banks, via various media and digital communications,” another panellist commented. “They are now forced to handle their relationships and their transactions, so unless the banks and advisers offer them genuine value-added, they can simply opt for the discount brokerage approach. Finding ways to maintain and build relationships with the clients and offer true value is therefore even more essential right now. Again, this trend was in play before this crisis, but is even more acute now.”

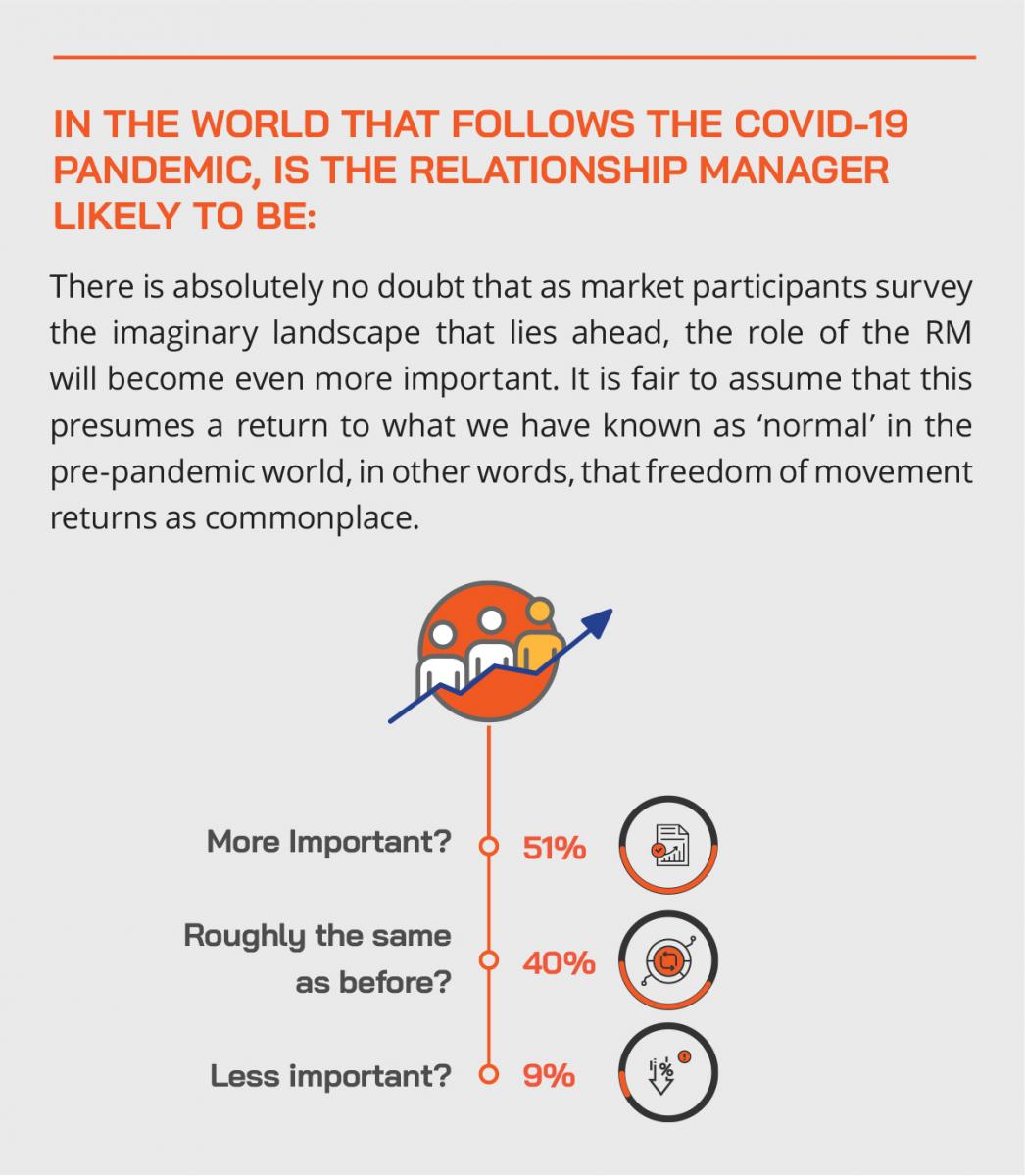

There is absolutely no doubt that as market participants survey the imaginary landscape that lies ahead, the role of the RM will become even more important. It is fair to assume that this presumes a return to what we have known as ‘normal’ in the pre-pandemic world, in other words, that freedom of movement returns as commonplace.

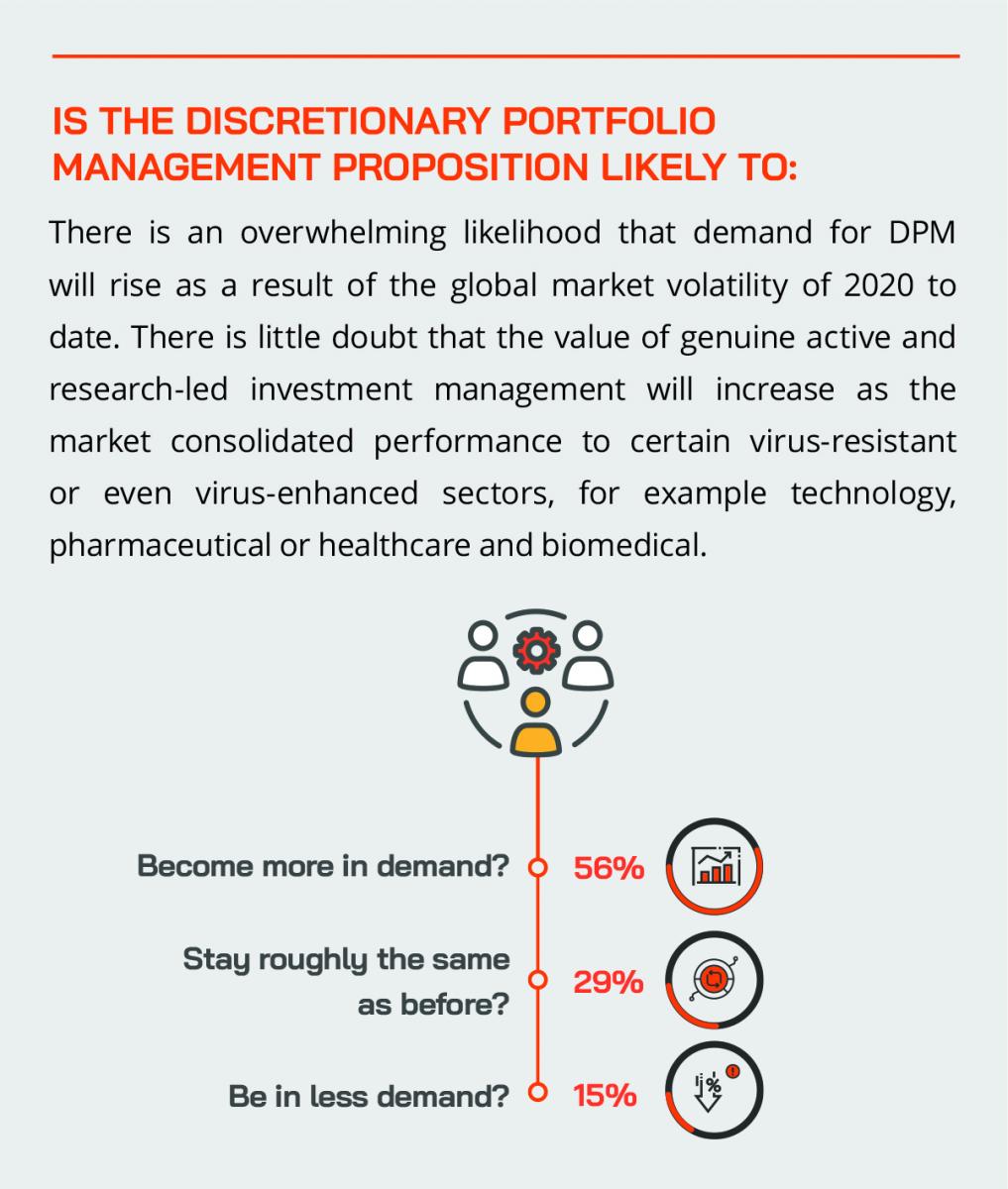

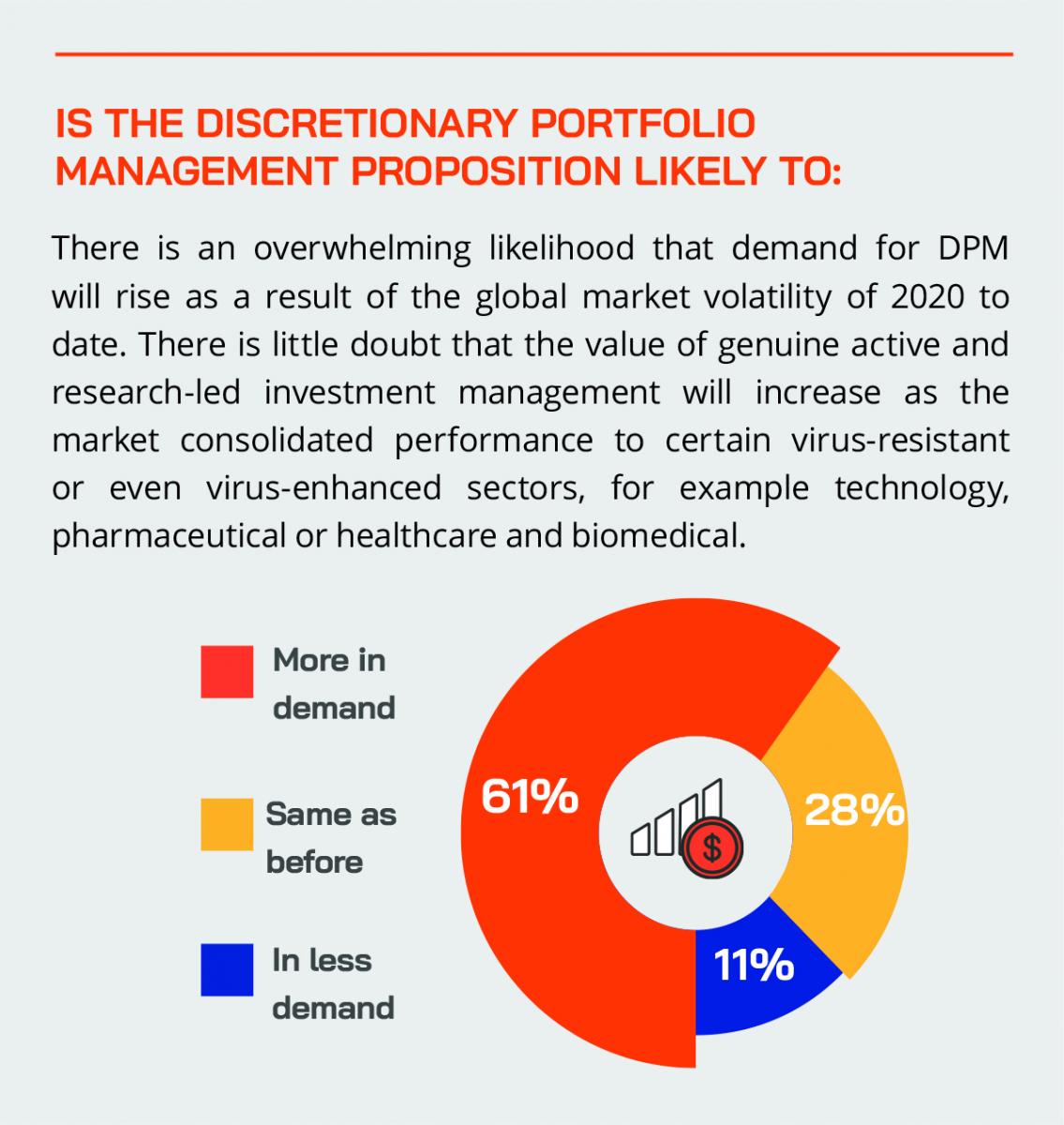

There is an overwhelming likelihood that demand for DPM will rise as a result of the global market volatility of 2020 to date. There is little doubt that the value of genuine active and research-led investment management will increase as the market consolidated performance to certain virus-resistant or even virus-enhanced sectors, for example technology, pharmaceutical or healthcare and biomedical.

There is an overwhelming likelihood that demand for the advisory proposition as a result of the global market performance during 2020 to date. Many Asian HNW and UHNW clients prefer not to relinquish full control of their portfolios, hence the advisory proposition whereby they can continue to make the final investment decisions, but based on research and advisory-led, fee-paying services, is likely to expand significantly in the foreseeable future.

One private bank CEO stated that his bank’s income has remained relatively robust as the bank charges fees as a percentage of average assets under management of the preceding quarter. “We are conservative,” he said, “and we have kept our clients and portfolios to strategic asset allocation, we have not fallen into the trap of becoming too tactical even throughout the crisis. We think clients have to realise that sometimes it is even worth paying money while they are not doing anything, that is also value-added, as it is at times better not to rush in or out as the only people who really make money then are the banks and brokers.”

Private banks have in reality made a lot of revenue as volumes have been high through the crisis as clients were de-risking and recalibrating their portfolios, or even as leveraged clients sold in order to pare losses and meet margin calls, but looking ahead, the winners will need to learn to add value, while others who continue to focus on transaction-driven revenues are likely to lag behind.

He added that looking back over several decades and including the 1987 crash, the 1997 Asian financial crisis and the global crash of 2008, people tend to have short memories. “However,” he said, “the reality is that clients also learn, and they are generally considerably more sophisticated than they were 10 or 20 years ago. That is actually positive for us, as clients appreciate our approach to investments and portfolios, they appreciate that it is not possible to time the market that well, so they are willing to take the longer view. In fact, we have not seen any knee-jerk reactions really.”

He also commented that some crises – this one included – reinforce the bank’s business model, as clients understand more readily that they need a trusted adviser and are more willing in some ways to pay up for that. “These same people pay for tax advice, for medical advice, so they should also pay for high-quality financial advice, so I would not be surprised if COVID-19 might speed up the shift towards a more fee-based approach for our industry.”

One guest picked up on this point, noting that private banking is not only about investing, as there are several ways to make revenues, including leading, the trust business, advice on life insurance policies, deposits, FX, and during the pandemic.

“Trusts are especially important right now,” he commented, “as many private banking clients are older, and many own SMEs, which will require additional lending, so there are two key avenues for revenue potential. Meanwhile, life insurance is even more in the spotlight, offering another good reason to talk to your clients. Additionally, active investing and DPM should flourish in this situation, so that opens doors to client discussions.”

He also advised providers to consider the RM remuneration packages to ensure that they are productive for the bank but also for the clients. “Cost-income ratios are too high and must come down, especially as revenues ahead will be under pressure. This is something the industry cannot defer any longer. Moreover, to be honest, digital is here to stay, so how many RMs do you need in a digital world where talent is available at the click of a button, and cheap and fast; speed is very important in this environment.”

Audience Comment - HNWs & UHNWs will continue to want help

“Wealth managers will, in my view, never become irrelevant for HNW and UHNW clients as it is inelastic spending for them. Being in a unique position where I serve clients yet am a client myself due to family wealth, I can definitely see an increased reliance on our relationship manager during these times for investment ideas and market outlook. We have found that HNW and UHNW individuals tend to be undeterred and unaffected by certain spending they consider necessities. That said, the industry may see a bumpy road ahead post-Covid-19 where a reduction in service fees may be more appealing to clients for a short period of time. However, there will certainly be an equilibrium in the long run where everything resumes normal, and it will be business as usual. It seems to be a matter of which financial institutions manage to survive these difficult times.”

An expert cautioned against the onset of zero commissions, noting that any business must make revenues, so those discount online providers end up making their money by relatively high interest charges on margin and other leveraged accounts. “The danger is that with such compressed fees and commissions, quality advice is unsustainable form a cost-revenue perspective,” he warned.

Looking ahead, however, he expressed some concerns that for the HNW and UHNW client community, the personal touch is crucial. “Clearly everyone is having to think about how they can replace the human interaction during this time,” he commented. “Many firms had been moving towards a hybrid human plus robo-advisory model, but now they need to consider how to move clients to become active clients without a face-to-face connection. This means there is a lot of thought required on the business development front.”

A different perspective came from another guest, who maintained that this situation could be addressed by a more agile approach. “We are increasingly digital people, all of us, anyway and including many of the so-called older generation,” he observed. “We can see that technology stocks have performed well through this debacle, meaning that digital solutions are ever more important; it is simply that this crisis is accelerating things.”

Quite simply, he continued, the industry needs to fully adopt the mindset to shift to digital, perhaps moving business models as completely digital as possible. “I believe high-quality interaction with clients can be achieved through digital means,” he claimed, enthusiastically. “This is like a Kodak moment, and for the wealth management sector I believe all aspects can be handled digitally, from client onboarding right the way through to conducting meetings with clients on a more regular and more efficient basis.”

Audience Comment - Broaden your horizons

“By looking at value added services such as philanthropy, bespoke private equity investments, succession planning and integration of e-related initiatives into service platform and investment suites. Also, wealth managers should look outside the traditional bank custodians for their smaller clients and explore good platforms that cater to these clients. There are several web-based platforms such as IG markets that they can collaborate with.”

Another panel member concurred with an earlier view that the current situation presents a remarkable challenge to the credibility of client relationships and the skills of the relationship manager. “And we must recognise that this is also a major test of senior management and how they are helping their RMs and other teams function through all of this, how they are motivating them, how they are maintain lines of communication, how they are supporting them digitally, psychologically, as well as from a business perspective.”

He added that clearly cross-border client relationship management would be the most difficult to resume properly once lockdown abates across various countries, as people will find travel more problematic. This, of course, represents a key issue for Singapore and Hong Kong as regional and indeed global wealth management and financial centres.

“Accordingly,” he commented, “I believe that strategic partnerships between international firms and local firms in surrounding Asian countries will become even more strategically important. For independent firms practitioners like ourselves who are operating out of Hong Kong and Singapore, we see it as critical to have those deep local relationships and partnerships around the region, so we can combine their skills on the ground with our own more international, specialist skillsets. We see this situation as accelerating that trend.”

Another widely supported view was that the future wealth management winners must constantly be, unerringly client-centric, while those firms that are product-centric will be losers, unless of course, they are product manufacturers, for example, fund managers.

Sustaining Relevance, Building Connectivity, Growing Revenues

In our post-event Survey, we asked our delegates how best wealth managers could sustain their relevance and their businesses in the future? We have summarised their many replies here in the form of the recurring words and phrases, to provide a guide for what the industry should be focusing on. In no particular order, we found that they emphasised:

- A more holistic approach to the client and families

- Client-centricity

- The greater need for value-added advice and services

- A deeper understanding of clients and markets

- Focus on advice-based fee models

- Emphasis solutions over product sales

- Adhere to and communicate transparency

- Constant engagement with clients

- Stay relevant and up to date

- Deliver tangible value

- Leverage digital technologies and solutions

- Be continually adaptable and flexible

- Expand the range of services and dialogue

- Upgrade skills

- Education and training

- Integrate and automate via technology

- Assess and rebalance portfolios constantly

Technology, Communications & the Clients

The panel then explored the role of technology in wealth management, as well as its potential to boost communication during the lockdown, also extrapolating how these enforced changes might endure post-virus.

“We are all becoming more comfortable with technology, video calls, using more apps and so forth,” one expert remarked. “The more you get used to it, the more comfortable you feel with this type of conversation. Ok, this will never be as natural and pleasant as face-to-face physical meetings, but I think you can get very close if you do it often enough and become more polished at it.”

A fellow panellist concurred but said he would certainly be back out having as many meetings as possible once the pandemic fully abates. “Meanwhile,” he reported, “this is also a great time to step back and strategise about activity and plans for more normalised conditions. To achieve that we are, of course using whatever communication media we have at our disposal, whether chat apps, email, VDO calls, and telephone.

Six Signs (to the Future)

- The broadly positive experience means some degree of remote communication to clients will survive post-lockdown

- The market participants want more technology investment and more focused on the client and boosting revenue generation

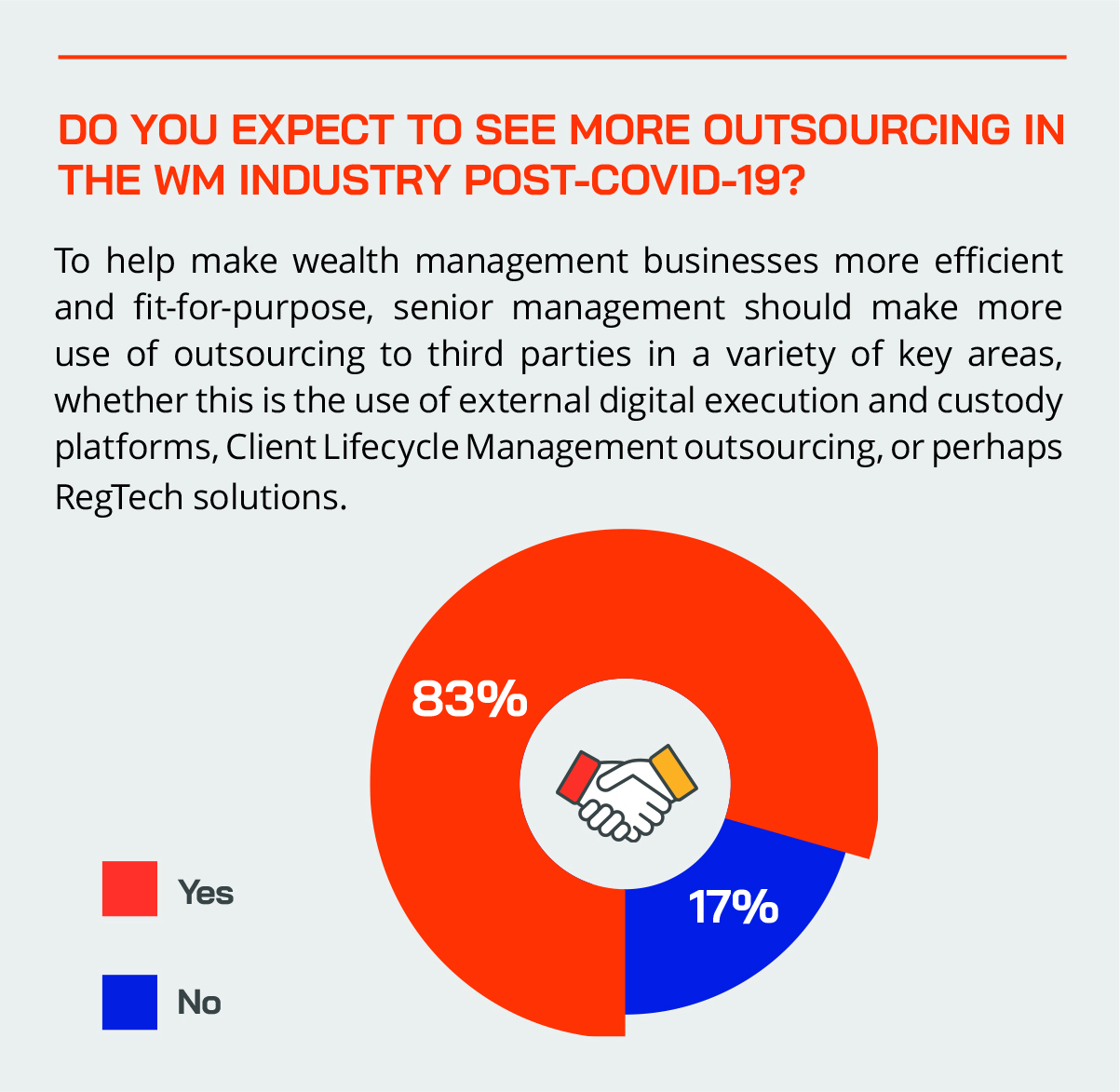

- Technology and digitisation is both complex and expensive, so more outsourcing will help boost success and control costs

- Technology should also be applied to operational processes to make firms more efficient and the client USX better

- Robo-advisory will increase but should be focused more on mass affluent, while in the HNW and above space should be tailored to enhance the RM

- Leverage capabilities by a broad-based, sophisticated approach to digital solutions

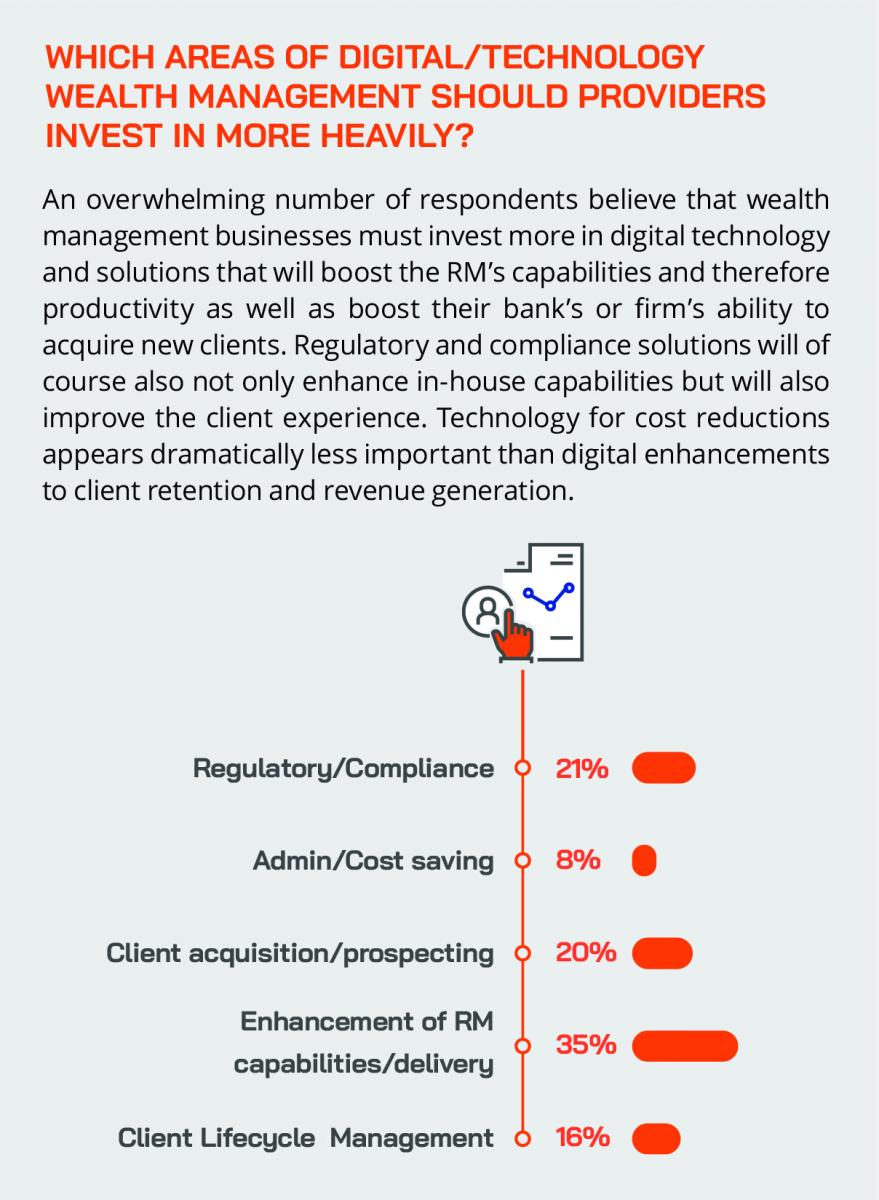

An overwhelming number of respondents believe that wealth management businesses must invest more in digital technology and solutions that will boost the RM’s capabilities and therefore productivity as well as boost their bank’s or firm’s ability to acquire new clients. Regulatory and compliance solutions will of course also not only enhance in-house capabilities but will also improve the client experience. Technology for cost reductions appears dramatically less important than digital enhancements to client retention and revenue generation.

To help make wealth management businesses more efficient and fit-for-purpose, senior management should make more use of outsourcing to third parties in a variety of key areas, whether this is the use of external digital execution and custody platforms, Client Lifecycle Management outsourcing, or perhaps RegTech solutions.

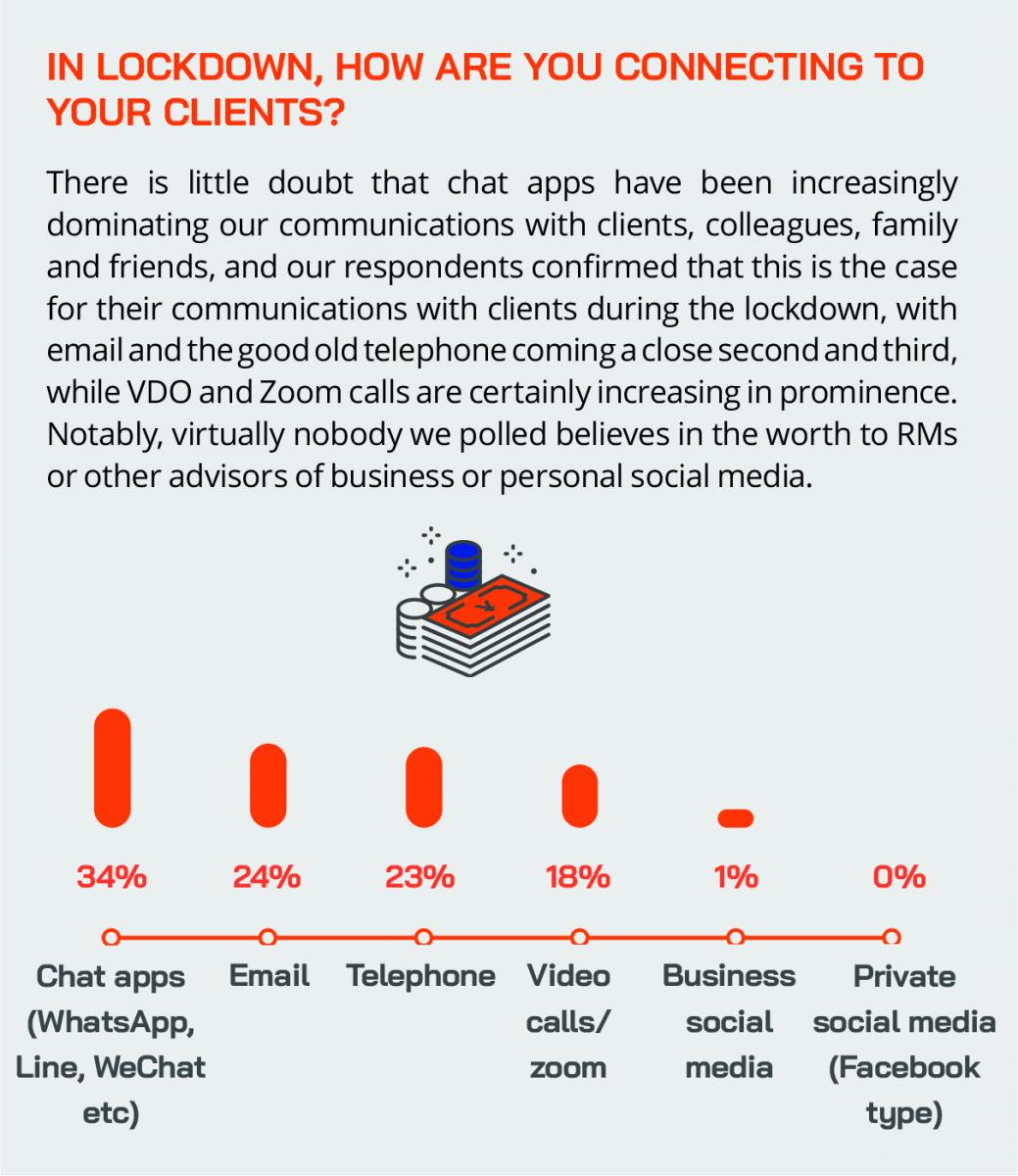

There is little doubt that chat apps have been increasingly dominating our communications with clients, colleagues, family and friends, and our respondents confirmed that this is the case for their communications with clients during the lockdown, with email and the good old telephone coming a close second and third, while VDO and Zoom calls are certainly increasing in prominence. Notably, virtually nobody we polled believes in the worth to RMs or other advisors of business or personal social media.

“Geography is history,” another expert stated. Technology allows us to be present anywhere. “We can even send clients a bottle of whisky and a nice cigar and set up a time to share it with them on a video call. But joking apart, we have seen for several decades more of the major global banks and investment banks investing more and more in tech and buying up solutions providers or disruptors, and that will continue. Remember Morgan Stanley after the GFC, they bought Smith Barney from Citi, then more recently bought E-Trade, so on and so forth.”

He also argued enthusiastically that banks and firms should consider acquiring new clients in the digital world, via social media, business social media and other media. “People must become more familiar with these resources,” he advised. “My entire business is based on client acquisition using LinkedIn, Facebook and other resources, and they work. You can be exactly where your clients are, much quicker, much more often, you can be in multiple locations at any one time. You need an open mind and smart digital skills and the ability to hone your digital marketing.”

Audience Comment - Leveraging digitisation

“In an ever-challenging and competitive landscape, the new tomorrow is to embrace and fully leverage digital capabilities to successfully compete. To address the enemy - increased costs and declining revenues - now is a good time to strengthen the frontline, to develop and improve transparency in mandates involving discretionary, advisory and execution-only for clients and to improve operational efficiency. With declining revenue, technology could be the future to reduce operating costs, bringing savings that can be passed on as lower advisory or product fees to clients.”

Technology can be used in both operational processes to make firms more efficient, but also in a variety of ways to make the team members, especially the RMs, much more efficient, and of course for the delivery of the end-product and for execution.

“Nevertheless,” one expert commented, “my own view is robo-advisory cannot replace the value of really communicating face-to-face with clients and then coming up with effective wealth planning and the means and solutions to achieve the clients’ goals.”

However, he firmly believes that technology can really help in freeing up the RMs and other advisers to become more effective, to make more productive use of their time and their clients’ time.

“I believe 80% of their time should be creative and productive, but as we know, it has been more like 20% as they are swamped with basic compliance and other admin. In short, there are many digital solutions that offer huge upside, but you must know what you are trying to achieve, and where within your organisation to best apply investment and focus.”

Audience Comment - Making the best of the situation

“I have been sending information and updates and follow-up with calls to my clients and prospects. Clients have more time to read and digest information and also time to evaluate their respective position in their lives, and many are taking more time to speak and respond when contacted and I have been able to access many meaningful insights to other parts of their lives which they had not previously disclosed to me. The client/RM relationship has been taken to another level as we both are not rushing through discussions. Prospects value that we care for them personally instead of just their portfolio and appreciate it.”

Another expert advised WM firms to consider instead outsourcing more of their current operations to third-party providers, for example, fintechs or others that can provide the solutions and infrastructure necessary, which is especially vital for the independent firms. This can significantly reduce cost-income ratios, especially for the smaller and medium-sized firms, whereas the major global banks and brands can spread such investments and overhead over a far, far bigger client base and also across the mass affluent client base.

And a panellist also advised far more use of third party freelance and other resources, to boost resources at sensible costs and to expand capabilities and upgrade skills and capabilities.”

Audience Comment - Keep in constant touch

“Given the current situation, clients tend to be sensitive in face-to-face meetings. However, clients are highly appreciative of more frequent attention and contact either by video or audio. Clients themselves have more time to listen and speak to wealth manager resulting in many sales being concluded and business being completed.”

“Be prepared for crises,” advised another expert, “and from this crisis, learn where exactly you can even further improve your business continuity and delivery and value. Leverage your capabilities as well, so, for example, we are also working closely with a lot of aggregators on consolidation and reporting software. We are also investing additional resources into our API systems because many of our clients now want that extension. So, whilst ensuring that our core business is still working efficiently and effectively, it has allowed us to look at other aspects that we think may come sooner than we had earlier planned for. My own view is the world has not changed forever, but we need to ensure that we progress positively as we hope for some form of normality in the near future.”

The final word

The final word of the first Hubbis Digital Dialogue discussion went to a panellist who, in reply to a question from the audience, argued that the old days of transaction-driven private banking are over, and the more agile players, the EAMs, IAMs and family offices, can provide a more rounded overall solution and charge clients appropriately for that application of a more holistic perspective and greater value-added. This polarisation will occur,” he said, “although for the short-term the road ahead will certainly be bumpy for all concerned. Seeing through the chaos, I believe transparency, honesty, client-centricity, all these values will prevail, especially for those who use resources wisely, who form the right partnerships, and who are agile.”

Latest Thought Leadership

Publications & Thought Leadership

Investment Products & Solutions - Are we at the Dawn of a New Investment Paradigm?

Latest Articles