Publications & Thought Leadership

Investment Products & Solutions - Are we at the Dawn of a New Investment Paradigm?

May 26, 2020

Whatever new dawn is ahead for the world economy, for businesses, for investors and even for the social and family lives we have long cherished, the world has undeniably changed, and in ways not seen in our lifetimes. The chaos wrought on economies, businesses, individual liberties and of course on the financial markets has been dramatic and shocking to all. What then is the next phase for Asia’s wealthy investors as the world struggles to escape the straitjacket of lockdowns, economic malaise, and financial market volatility? The second Hubbis Digital Dialogue, on May 21, focused the minds and experience of four seasoned private bankers and investment experts on the implications for HNW and UHNW investor clients in Asia, set of course against the backcloth of the events of 2020 to date, from the worst of the global markets rout in February/March, to the relative stability by May 21, as hope dawns and markets tentatively claw back some of the losses, and as some sectors, such as Big Tech, power ahead. Our panel of experts cogitated on how the wealth management community – the providers and the clients – might respond. We did not delve too deeply into asset allocation or other theories; instead, we tried to keep our collective eyes firmly set on the key implications, such as for self-directed investment versus discretionary portfolio management and advisory mandates, for the elevation of risk management in the post-coronavirus world, the implications for derivatives and structured products, for leverage and its dangers, and framing the entire discussion against the responsibilities that wealth management intermediaries have to their clients.

Moderator

Michael Stanhope

Founder & Chief Executive Officer

Hubbis

Speakers

Johan Jooste

Managing Director

The Global CIO Office

Andrew Hendry

Head of Distribution – Asia Pacific

Aberdeen Standard Investments

Bryan Henning

Consultant

Arjan de Boer

Deputy Chief Executive, Head of MIS, Asia Markets, Investments & Structuring, Asia

Indosuez Wealth Management

Advice for the post-pandemic world

Take 6: Six Pointers to the Road Ahead

- Lessons from crises are seldom learned and/or soon forgotten

- Risk must be better measured against return

- Asset allocation models must adapt to the new world

- Leverage must be more cautiously applied

- The WM industry has an opportunity to elevate the investment dialogue

- The WM industry must prove its worth by the curation of relevant ideas for the new world ahead

The discussion began with the moderator focusing the experts’ minds on whether this crisis is likely to change the collective wealth management community’s approach to advising clients.

“Sadly,” an expert began, “we do not see lessons of past crises having been learnt and remembered, so we have seen the same old mistakes, time and again. There has been insufficient focus on risk appetites and risk exposure, while we have seen too much leverage, often applied in the wrong segments. All this means that we need to rethink asset allocation, reconsider how we communicate and engage with clients, and grasp the opportunity that arose more than a decade ago in the global crisis, in short build a better wealth management industry ahead.”

A fellow panellist highlighted the difference this time from the time of the Lehman Brothers debacle and all that ensued.

“This time, everything went down across the board, equities, fixed income, all assets, while volatility soared, all in just days,” he reported. “And the severity and speed meant it was incredibly difficult to react and with leverage added in, of course, investors were often hit very hard.”

“From my own viewpoint, as a former banker and now investor,” he continued, “I now find my conversations with private banks and others frustrating, as the dialogue has not been about portfolio re-construction in light of these events, in the new normal times ahead, but I hear only about jumping on specific trades. I see and hear a lot of similar thinking, but little value-added insight.”

He argued that this Covid-19 crisis has wrought a fundamental change in all aspects of our lives, and that investing is going to be fundamentally different. “We need to focus on how to derive true alpha, whilst the concept of beta is potentially dangerous going forward,” he commented. “We really need to differentiate between who is going to survive in the new world and who will struggle or fail. We need to see beyond QE-enhanced credit – the central banks have been artificially propping up all types of credit and therefore fixed-income funds, for example - and consider the creditworthiness of the corporations and even countries ahead.”

Comment: Run to cash is the adage in times of severe market or economic or geopolitical stress, and this is certainly a key finding in this situation. Similarly, it appears that the wealth management community is already seeing a shift towards managed investments, although as the panel highlighted in the main discussion, this trend can reverse quickly, especially in Asia, if indices suddenly recover further, leading investors to rapidly forget the market traumas and return to some of their former investing misdemeanours.

In short, he concluded, RMs and wealth management leaders need to be having more discussions that delve into the real meat of how HNWIs and ultra-wealthy investors should invest, not using the old thinking, but seeing a new reality in the markets and assets classes. “I, for one, do not see any V-shaped recovery,” he remarked, “and I am sure we must try to understand what will be the new normal for economies, markets and portfolios.”

Another speaker noted that investors had found chunks of their holdings unexpectedly and remarkably illiquid during the worst of the market sell-offs; they therefore often had to sell better quality paper, meaning that they now needed to again improve the overall quality of their holdings.

Comment: A similar story appears in relation to fixed income holdings, although as debt is generally less volatile historically, it appears our market experts believe a reasonably significant portion of the wealth clients in Asia will continue to apply leverage in the foreseeable future. That view might, of course, change if there is a dramatic fall-off in credit quality as the clouds clear in the post-pandemic world. And in any case, our industry discussions indicate at this stage that investors will be more generally cautious than they have been for some years.

A panellist then remarked how the fallout in FMPs – fixed maturity products – in the fixed income markets, allied to leverage, had resulted in many unexpected margin calls. “The lessons from that situation,” he explained, “are that some of the private banks had not chosen the paper wisely; there had been far too much focus on the magical 4% to 6% target yield, but now there needs to be greater conservatism, acknowledging that there is always a significant risk in the constant search for a ‘magic’ number in terms of yield.” Better, in short, to focus on a more modest yield and a higher-grade portfolio of credit, and therefore significantly lower risk.

Another panellist concurred, adding that what he had seen in the worst of the market fallout was margin calls requiring either the addition of more cash collateral or more realistically investors selling better quality assets to stave off their lenders’ demands. “The problem we often saw is the compounding effect of margin calls and excess leverage, but then as assets bounce and recover, those investors that had suffered the worst are not able to participate, hence the double negative. Badly constructed portfolios, poorly thought-out loan packages and the result is real toxicity in unexpected market crises.”

He added that the dangers of excessive focus on return mean investors often lose sight of risk. “In the more clement market conditions,” he explained, “it is almost impossible to persuade a client to build in greater portfolio resilience, as investors baulk at paying up for downside protection, but the reality is that those defences need to be in there in good and bad conditions. We need to be bold in getting these messages out, even if they are difficult conversations.”

He extrapolated further, noting that it is also very difficult to remediate portfolios in the aftermath, even if there is wreckage out there to be picked up cheap. “Again, those sorts of conversations are very tough, as it is an incredibly easy error to look only at the recovery, the spike after the crash and just ignore why we went down in the first place. The errors made are common investment errors, not simply Covid-19 derived, so we must learn, and we must get this message out, loud and clear.”

A fellow panellist agreed, adding that the communication of risk and risk management by the RM community has historically been poor, and remains thus today. “I would like to see risk exemplified in models that show me different outcomes under different scenarios, and with different asset allocation models,” he reported. “Framing the conversations in this way should be a natural for private banks with their resources.”

Audience Views

Hubbis asked the audience for their comments to specific questions immediately after the discussion. We have selected a few such comments to highlight here.

“The views from some panel members echo the sentiment of some of my clients. Some of them were very wary about the recent rally in the stock markets, as it appears there is a big disconnect between the real-world economy and the stock markets. Others are opportunistic to take advantage of cheap buys for short term trades.”

“The situation will require more portfolio rebalancing and conservativism around investment decisions, for now. Once the pandemic has stabilised, or people are getting used to dealing with it after many months, clients will likely see their confidence increase and rebuild their investment portfolios.”

“Between now and year-end, the virus will still have a major impact on the mentality of our clients. I think they will choose to hold cash instead of entering any major investment decisions until conditions become somewhat more predictable. The more jittery clients may undergo some panic selling when they over-analyse the charts and data, but as highlighted by the panellists, it would seem patience is the key.”

“Most clients will take on a more conservative stance keeping ample liquidity, so will look to park money in liquid funds which become increasingly attractive in light of the extremely low interest rates. Some portion of the income and yield play will come from the emerging market bond segment. Overall, a cautious approach with some hedging will dominate the landscape, while investors keep their powder dry for opportunistic investments into sectors which will prove to be resilient in the post-Covid-19 world.”

“Clients will be confused with the uncertainty and will require a lot of information on the risk exposures for various asset classes and will likely seek more active management and constant updates from their advisors. Though the focus now should be back on long-term goals, with the world so jittery, with the uncertainty surrounding what the new normal is and how long this pandemic will last, and the after-effects and the undercurrents, most clients will require constant feeding of information, and a formulation of their portfolio being adapted into the new normal environment.”

“From a product creator’s perspective,” said another expert, redirecting the discussion, “there was considerable disparity in how the peer group of asset managers reacted in the early days from late January, as well as considerable differences in the reaction of distributors, meaning the private banks, wealth managers, IFAs, insurance and others across Asia-Pacific. There was certainly a need to keep communication lines open, due to the pace of events at the time and the escalation of fear. For us as asset managers in normalised times, it is more of a weekly cycle, whereas we needed to rapidly switch to very concise, very short, daily briefings because of so much panic. We know there are no perfect answers, but clients need viewpoints.”

He reported that a core message at the time of the worst anxiety amongst investors was that such crises do happen, and they happen again and again, and therefore it is vital to be financially fit for the future. But it was also essential during those very difficult times to help investors and distributors and others in the investment world to articulate a delicate sequencing of introducing some calm, helping the financial advisors and bankers with the incredible volume of queries, and then starting to be more productive in terms of recovery ideas.

The case for external control

Take 6: Six Pointers to the Road Ahead

- There appears to be a current indication that alpha will return, and beta be less relevant

- This is an ideal time for providers to prove the value of DPM and advisory

- The industry firmly believes more Asian clients will embrace DPM

- But there are risks that improved market conditions will cloud the message

- Asian HNW and UHNW investors will remain cautious about passing control over to the wealth manager

- The advisory proposition is, some argue, more likely to gain greater sway than DPM

“We did, of course, learn that managed portfolios and managed solutions were of greater interest to clients after the Lehman crisis,” said one specialist on the panel, “and I do hope and believe this will be even more the case now.”

After the global financial crisis, he reported, discretionary in Asia went from a roughly 2% penetration to about 10%; although that is nothing today compared to Europe or North America yet, it is a remarkable growth. “This crisis will, we believe, therefore trigger the second wave of growth for discretionary and advisory,” he reported. “Realistically, it is so much better to have other people manage these investments. Do you really want to stay up all night in Asia watching US markets? We need to emphasise our capabilities and help clients reposition and encourage them to let us hold the reins so they can sleep easier at night.”

An expert noted remarked that as this is the second fairly recent crisis event effectively driving the growth of DPM and advisory after the global crisis of 2008-2009, there is little doubt that risk management and a less emotional, more dispassionate approach investing should grow robustly, at least in theory anyway.

“However,” he warned, “market activity and trading levels have again begun to return in recent weeks, and it is clearly easy for clients to return to their previous behaviour. As professionals, we need to step back and remind our clients of the need to focus on long-term investing and a more elevated approach to risk management.”

He noted that while there were opportunities selectively to pick up assets at attractive price points - after all in only a few weeks the S&P 500 fell 35% then bounced more than 25% - RMs were often putting out fires for clients, with little time to focus on bigger picture ideas and managing portfolios.

Audience Views

Hubbis asked the audience for their comments to specific questions immediately after the discussion. We have selected a few such relevant comments to highlight here.

“Although a shift towards DPM can be long term structural trend, I personally do not envisage this pandemic making significant changes, as this is a short-term shock to the market, and long-term investors’ philosophy will not easily be changed. However, this can also be seen as a testing period for the DPM portfolios to demonstrate resilience and quality investing protocols in order to gain client confidence in how we manage the portfolio and risks professionally.”

“I am conflicted on this issue, as it seems to be highly dependent on the client mindset. On the one hand, I believe the significant shift will be for clients who are willing to opt for the hands-off approach, and who might be concerned with making the wrong decisions should any of these pandemics or other crisis occur in the future. On the other hand, I agree with a panellist who said he doubts that private banks can effectively manage/control assets on the client’s behalf.”

“I think Asian clients are not so ready to pay yearly fees for the fund managers to manage their account completely. Moreover, DPM portfolio performances were also down when the market corrected. There might be a 5% to 10% increase in penetration in DPM, but I do not see a significant increase.”

“I am not sure that there will be a significant shift towards DPM, but I definitely see a shift towards an independent advisory model, on a semi-discretionary basis; this approach has proven to be relatively more resilient in protecting client portfolios amidst the market volatility, due to no inherent conflicts of interest or aggressive product pushing by banks irrespective of client risk assessments.”

“Clients will appreciate more discussions and adherence around strategic portfolio allocation. More will be willing to pay for independent and good quality advise wherein each client portfolio is managed in accordance with his/her risk profile and requirements. A large number of our clients have been shaken up by the experience of their family members and friends who have lost a substantial portion of their wealth with the private banks in the current market meltdown. They have expressed their appreciation to us [and independent firm] for helping them protect their capital.”

“This major bounce somewhat clouded the more existential question on the role of the RM,” he observed, “thereby allowing them to sort of sweep the bigger picture questions under the rug. However, looking ahead, we will need to think more rigorously about portfolio resilience, DPM, and the professionalisation of the overall approach to HNW and UHNW investing.”

He said he does, however, continue to worry that RMs will keep taking the easier route of letting the clients drive the conversations, typically around yield, leveraged yield, and often ignoring the underlying risk.

“We need to elevate the dialogues to levels more often seen in private wealth management in Europe,” he observed. “The family offices and the ultra-high-net-worth, they have professionals who really focus on these conversations, which kind of forces the issue. But for the typical HNWIs, it remains more transactional, and RMs are not often enough elevating the discussions. I hope this time around might be the catalyst for real change.” Nevertheless, the panel did not appear to be especially confident that this will transpire as quickly as many would like to see.

Another specialist added that RM availability throughout such crises is extremely important in keeping lines of engagement open. “My advice to them is to keep having those conversations all the time,” he said, “and to keep trying to be as confident as you can about what you know, as well as trying to also be as humble about what you are not so familiar with or certain about. And as to fees and approaches, I certainly believe we need to drive clients further towards fee-based solutions such as DPM and advisory rather than transaction-based.”

Another expert how incredibly exhausting the advisory approach to fund sales can be for the private banks and other distributors, as they struggle to arrive at greater recurring revenues. “We have been switching therefore to SMAs, providing those to banks which perhaps don’t have DPM capabilities. We have, for example, seen considerable progress in Australia, which is much more advanced in terms of the pressures switching to fee-based revenues, with SMAs coming in a lot more, and the result is far more resilience for them.”

According to Australian financial firm JB Were SMAs are financial products that are sold via a Product Disclosure Statement (PDS) and operate within a Managed Investment Scheme. However, SMAs are not pooled investment vehicles – the investor is the owner of the underlying securities. This direct ownership of the underlying securities, JB Were comments, is one of the characteristics that set SMAs apart from other popular retail investment products such as listed investment companies (LICs).

“I feel that bankers need to take this opportunity to confront the more existential question of whether they want a fee-based, recurring revenue business, with best-honed products and structures and protocols, or whether they simply want to go back to the old approach of selling products and trades. Accordingly, we are taking this perspective and, within this region, having more discussions about business model structures, for example focusing on SMAs.”

Investing amidst ongoing uncertainty

Take 6: Six Pointers to the Road Ahead

- Patience is needed – although markets have bounded vigorously from the lows, we might be in a period of false hope and expectation

- There are numerous uncertainties still out there, from Covid-19 to geopolitics

- Asset allocation models must be challenged and made fit for purpose for the environment ahead

- Portfolios must be more closely aligned to risk appetite and client objectives

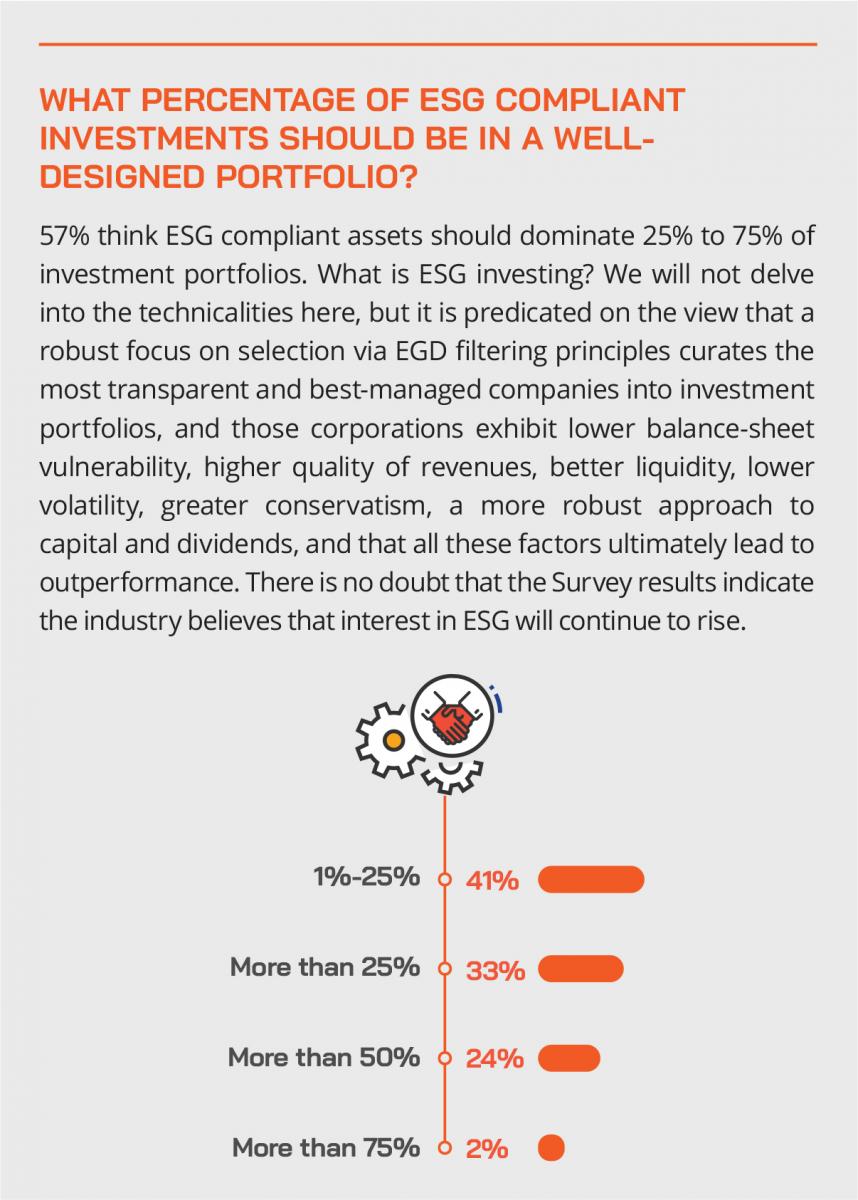

- ESG investing is valuable as a means of filtering out the highest quality corporations

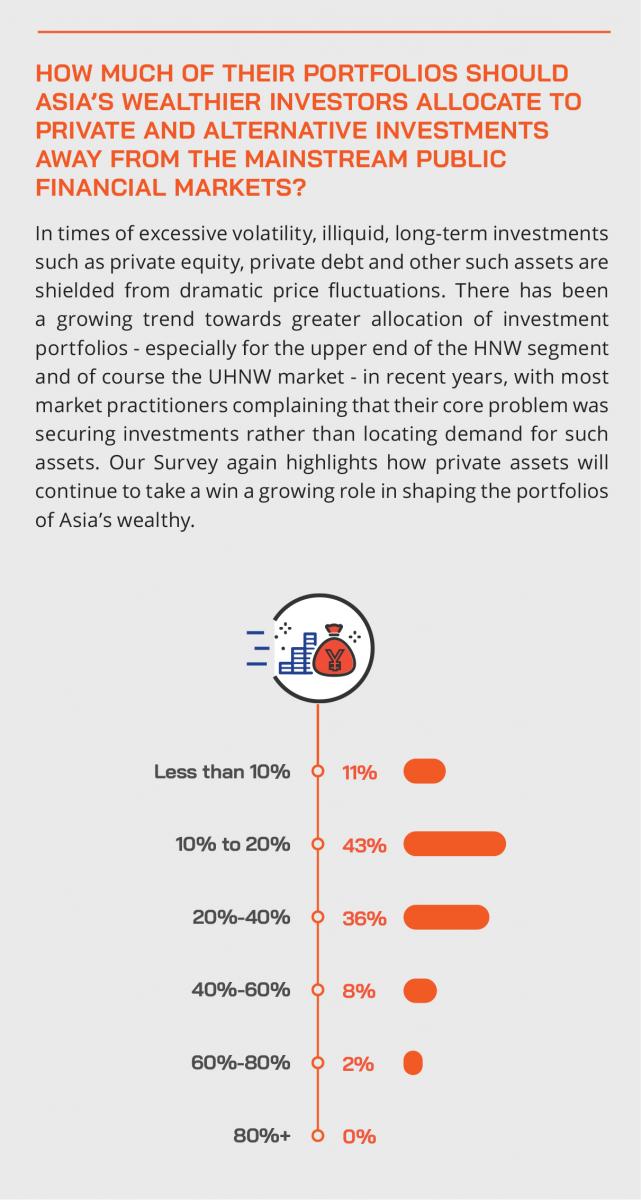

- Private assets protected from the volatility of public market pricing will gain greater sway

Constant communication between RMs and clients must be attained, as information and insights are even more vital in a market that will see increasingly divergent performance

One speaker launched into the view that the global economy will not recover as quickly as perhaps the markets anticipate, based on the recovery of asset prices in many key sectors in recent weeks.

“We are now in the phase I would characterise as a false bubble of hope,” he commented, “resulting in the markets powering forward with this belief that we are closer to a V-shaped recovery, but it is selective, so a large chunk of the S&P 500 recovery is five Big Tech stocks. However, I am not convinced, and remain very concerned about the short and medium-term course of the virus, about the impact of ending lockdowns, about US politics, about geopolitics, and of course about the economic situation globally and the gigantic central bank support.”

In light of these very evident and realistic concerns, he said he wants to see concepts for asset allocation that make sense for the new world and then see more detail on how such allocations will be fulfilled for investors from the product suite out there. “I have not had such discussions,” he stated. “I have heard plenty of good thematic ideas around robotics, enterprise software, the cloud, but actually I want more. In effect, he appeared to be calling for a different approach to the new world ahead, one that combines a more historical and philosophical appreciation of the past aligned with a far more realistic and pragmatic vision of wealth preservation and accumulation ahead. This means new world solutions for a new environment.

A banker agreed with this general viewpoint, adding that the bank had been stressing the importance of factors such as quality, liquidity, lower volatility, conservatism, capital preservation and transparency, especially focusing on ESG principles, as that strategy is proving to very often unveil the best-managed, most transparent companies and that, in turn, often translates to better asset price performance.

“Patience is essential,” came another voice. “Avoid the obvious errors, wait and find the right ideas for the medium- to long-term view. Don’t make mistakes that take a long time to rectify. You do not need to rebuild portfolios immediately, especially with so much uncertainty out there. Don’t chase trades, try to be more accepting of modest returns, build resilience into the portfolio. I also struggle to understand how the market can price in the V-shape recovery, so don’t push too hard, let much more dust settle first.”

Another expert concurred, reiterating that what he had seen in the worst of the market fallout was margin calls requiring either the addition of more cash collateral or more realistically investors selling better quality assets to stave off their lenders’ demands.

“The problem we often saw is the compounding effect of margin calls and excess leverage,” he commented, “but then as assets bounced and recovered somewhat, those investors that had suffered the worst are not able to participate, hence the double negative. Badly constructed portfolios, poorly thought-out loan packages and the result is real toxicity in unexpected market crises.”

Audience Views

Hubbis asked the audience for their comments to specific questions immediately after the discussion. We have selected a few such relevant comments to highlight here.

“We anticipate a better long-term alignment of portfolios with clients’ longer-term financial goals. We see reduced leverage except in a smaller speculative portion of their portfolios. We will help them seek to identify those industries and companies most likely to adapt to the 'new norm'.”

“We will see portfolio repositioning with a long-term, quality view and a core/satellite approach. We anticipate more diversified investments into next-generation/‘new normal’ stocks, more ESG, and the traditional fixed income core. Structured products and FX will play a role in the trading/satellite part of the portfolio.”

“Clients will adopt a ‘wait and see’ strategy as many of them felt that there would be a second wave of the coronavirus once markets and lockdowns start to reopen. There will be some opportunist clients who will trade shares for short-term gains, but the more conservative client will prefer to wait for better entry levels.”

“Clients, in general, have a very short memory. Markets have dropped in the last couple of months by 35% but have also regained 27% since the worst decline. They will remain cautious and conservative for the time being, perhaps till year-end, but once markets pick up again, they might forget about the situation they might have been in during the crisis and start investing wholesale again. Not all learn their lessons from the crisis.”

“As one panellist said, the shift could be towards thematic investments in new segments. Communication with clients may be less face-to-face for the foreseeable future, but we can all use more technology channels and devices. Fee revenue may experience compression, while performance fees may be more commonly accepted by clients.”

“The way to approach portfolios will most definitely change, while we as advisors are also grasping with the changes and new normal, during this time of fear. I believe that going forward will be more effort to obtain and disseminate information about the market and the impact on the assets class, as well as the calibre of the asset managers. We need constant updates from the fund managers on changes, or changes in management style and market outlook. This information should be constantly disseminated to investors, where it is applicable, and discussions more closely aligned with the interests of those investors. In a nutshell, more work needs to be done, but we must ensure we keep the relationships strong and keep the emotions at bay.”

A fellow panellist agreed that it is always very difficult to remediate portfolios in the aftermath of major market selloffs, even if there is wreckage out there to be picked up cheap. “Not only that,” he commented, “but we must try to elevate the conversations, make investors focus on the lessons, as it is an incredibly easy error to look only at the recovery, the spike after the crash and just ignore why we went down in the first place. The errors made are common investment errors, not simply Covid-19 derived, so we must learn, educate, get this message out.”

A banker added that the dangers of excessive focus on return mean investors too often lose sight of risk. “In the more clement market conditions,” he explained, “it is incredibly difficult to persuade a client to build in greater portfolio resilience, as investors baulk at paying up for downside protection. But as we have seen time and again, the reality is that those defences need to be in there in good and bad conditions, and certainly in case of Black Swan type events like this virus. We need to be really bold in getting these messages out, even if they are difficult conversations.”

Keeping true to the values of wealth management

Picking up on this point, another expert commented that wealth management remains a very personal business, so steering discussions towards more personal relationship building, the family and so forth is also important.

“The style should be to combine a more personal approach from the RMs with experts offered to the clients who are more hands-on, fact-based, investment advisors, and they should be the ones driving investment decisions and portfolio construction. I personally think the days of having one contact point are over. We need to see RMs managing relationships, and investment advisors handling and managing the investment advice.”

“The reality,” said one speaker, “is that calling a client from home simply feels different from calling out of an office, or more importantly meeting clients. Bankers are very social animals, so this is not an easy period for them. They say 80% of all communications is nonverbal and at the moment we can only do it verbally, even though Zoom or other live calls do help somewhat. So, my advice in this situation is call clients as much as possible, but focus on the longer-term view, and on risk mitigation.”

The final word went to a guest who believes the industry must now embrace a new model of excellence and professionalism. “From the top management down,” he said, “we need to see greater confidence, more tools, more training, greater application, the right incentivisation, and the result in mind all the time of the client getting the right outcome. In Asia, the providers can find the balance between core and satellite to keep their annuity income going while also continuing some transactional, but we need to see that conducted in a more formalised, sustainable, robust and easily managed manner to ensure the providers are fully on top of all that.”

Latest Thought Leadership

Publications & Thought Leadership

Investment Products & Solutions - Are we at the Dawn of a New Investment Paradigm?

Latest Articles