Publications & Thought Leadership

The Evolution of DPM in Asia and Offering Tailored Portfolio Management at Scale

Jun 2, 2022

Hubbis assembled an erudite and influential panel of private bankers, IAM leaders, digital platform experts and asset managers on May 19 to discuss how they are adapting their business models to help produce more recurring and more predictable revenues, to promote active management of portfolios, and to swing away from the vicissitudes of product-driven selling and to more client-centric and also more stable businesses. There is indeed no doubt that one of the key missions for the private banks and independent wealth managers plying their trade in Asia has in recent years been to gradually shift their models from the historical norm of a more transactional-driven approach in the region to more of a DPM and advisory model. DPM has thus far been rather exclusive to the HNW and UHNW market, but that is changing. The latest digital technologies, a robust regulatory environment and access to private equity that will fund new wealth management ventures have all helped encourage the development of platforms that are scaling up tailored portfolio management offerings to Asia’s vast mass affluent market.

Panel Members

- Mitchell Lam, Vice President, CSOP Asset Management

- Vineta Salale, Portfolio Strategist, Focused Equity, GMO

- Regan Shum, Head of Insurance Brokerage, Hywin International

- Harmen Overdijk, Chief Investment Officer, Leo Wealth

- Gareth Nicholson, CIO and Head Discretionary Portfolio Management, Nomura

- Ritesh Ganeriwal, Head of Investment Advisory, Syfe

Setting the Scene

Many believe that the relatively slow adoption of DPM in Asia can now be fast-tracked as the markets, geopolitics, central bank policy and financial conditions are so very different from the incredibly benign environment since the Global Financial Crisis.

While on the one hand the rise of the digital platforms and the major improvements in digital delivery and execution might be seen to favour the self-directed investment model, the rising volatility and global financial and geopolitical uncertainties are actually tailwinds for the advisory and DPM propositions, and wealth management leaders in the region point to robust traction amongst their clients for this more professionally-led private client investment model.

Moreover, as the assets and/or control of Asia’s vast private wealth transitions to the second and third generations, there is evidence that these types of clients are more disposed to professionalising the management of their financial investments rather than maintaining the typical hands-on model preferred by the founder-patriarchs in the region.

Additionally, digitisation has opened the door to the democratisation of tailored portfolio management options for Asia’s vast mass affluent market, where literally scores of millions of clients are tentatively feeling their way into the world of financial investments.

Our panel of wealth management experts painted an eloquent picture of the rationale and objectives around enhancing the DPM offerings in the region and advised delegates on some of the lessons they have learned from their efforts to drive their DPM proposition forward. And they analysed how scale is being achieved in tailored portfolio management through the various dedicated portfolio management platforms building their brands and their mass affluent market clientele in the region.

To do so, these banks and the independent wealth community clearly need to reshape their models and also to leverage new technologies, AI, ML and of course build more talent. They need to improve their marketing and communication of DPM and advisory, to better explain why a fee-based, professionally run model is more in the clients’ interests. They will want to elucidate the role of DPM in facilitating the growing rationale for the core/satellite portfolio approach incorporating thematics and also different asset classes, including private (non-public) assets, and how this can help fast-track client’s adoption of ESG. And they will need to analyse how their remuneration and management models must adapt to an environment in which the RMs are helping drive DPM adoption, rather than the historical ‘product-pushing’ and ‘fees-for-transactions’ models.

Pressure points on the private client portfolio – policy, (geo)politics and the pandemic

A guest opened his commentary by observing that there are currently three main pressure points, namely policy, geopolitics and the pandemic. “Policy is driving a lot of fear in the market,” he observed. “Clients and investors had become too acclimatised to an environment in which the Fed apparently won't let the markets go down too long, and where volatility dampening has been the name of the game. But we think that the path now is different, and the Fed will be the type of aggressive Fed back in 1994, aiming to get inflation under control but also engineer a soft landing. However, back then, we saw some of the largest drawdowns in bonds and some of the largest drawdowns in funds in history. In short, 2022 looks pretty tough.”

Accordingly, he reported that their private clients are largely following his and the team’s advice. “We are now sitting on 21% cash and 10% in alternatives, which represents the most cautious approach for a long time,” he reported. “However, with inflation rampant, cash is not king, so we aim to be nimble, to try offset inflation, to protect but also to seize opportunities, for example, through structured products. In short, we need to be active, we cannot sit and wait; we need to assess volatility and the risks and take advantage if and where we can.”

With markets and portfolios under pressure, wealth protection is the first mission for private banking

“In this environment, it is all about managing volatility, managing the downside and taking a very institutional investment management approach, which is the heart of our DPM offering,” this same guest extrapolated. “DPM is increasingly relevant for all clients in at least a portion of their portfolios, and across the risk profiles they might have. Indeed, we are seeing more clients in this region wanting to have at least some of their money in portfolios that are professionally managed. That often frees them up to focus their own investments in areas in which they might be knowledgeable or highly confident.”

He said that this is a trend he expects to continue, especially as clients in Asia increasingly see the value of the active approach. “Private clients want to achieve capital preservation first and foremost in this environment,” he said. “They see our value in helping to actively manage their downside, especially in environments where volatility is so high and while policy continues to so significantly drive markets. The overall environment is actually rather conducive to DPM.”

An expert added that a core appeal of DPM is the consistency of approach. “Over time, we are confident that DPM produces better, consistent, lower volatility returns,” he stated. “In the very good years, DPM may not outperform, because there is a bit more of a cost associated. But in times of greater uncertainty and more volatility, more clients come into the fold, perhaps starting with 20% of their assets and then building confidence and loyalty over time. The current environment globally is supportive of and encouraging for this type of transition towards DPM.”

DPM mandates are certainly not one-size-fits-all – they can be accurately tailored and tweaked to individual risk appetites

As to the formulation of portfolios, a banker explained that this naturally depends on the risk appetite of the client. However, in general terms, he said that a roughly one third apiece approach with fixed income, equities, and cash and alternatives was a basic approach around which the different risk approaches could evolve.

“This is a massive simplification for the purposes of this discussion,” he told delegates. “However, in short, we need to have a mixture of ETFs where we like the beta, we need single line securities based on underlying conviction, and at the same time, we need some thematics and the alternatives such as larger REITs, hedge funds and private equity. A robust DPM portfolio can contain all these elements, supported by our house view and then adjusted to clients’ risk appetites.”

He also remarked that passive strategies such as ETFs are very widely employed by active managers. “It is not an either-or approach, as some of the biggest investors in ETFs are actually active managers, using them as excellent vehicles for beta exposure at very low cost,” he reported.

A fellow panellist agreed that using [passive] ETFs does not mean passive investing. “Buying a single ETF is a passive investment, but we use ETFs actively in our DPM formation and allocations,” he reported. “We are active in our factor allocation. And ETFs are ideal for expressing those active choices in a very efficient way. They are also very transparent, as we know accurately what is in each ETF at any one time.”

More insights into how an increasingly diversified array of ETFs can help empower portfolios and DPM offerings

An expert agreed that the passive and the active approaches can align, they are not mutually exclusive. He explained that his firm’s ETFs are well diversified and listed both in Hong Kong and Singapore and targeted at the region’s wealth management community and investors. He explained their whole purpose is to increase the range of tools for discretionary managers to use and to offer more and more diversification, focused on the Asia region anything from the Hang Seng Tech Index, Chinese bonds or Asian REITs, and plenty more.

“We have a variety of broad-based indices ETFs, or smaller and niche indices,” he reported. “We have also rolled out our set of thematic ETFs and also a range of leverage and inverse products, the latter of which have been especially good for investors to play around with on the recent volatile environment. In short, our mission is to expand on this toolbox of ETFs for family offices, discretionary portfolio managers and retail clients, so they can easily plug and play our products into their portfolios, whether for the short-term basis, or with longer-term horizons.”

He said they believe that by investing into ETFs, clients have access to very simple, easy to use tools within the toolbox, helping them manage their time and resources and tailoring portfolios through careful selection of ETFs, and still allowing them to express other preferences for different assets and sectors, perhaps such as private markets. “Stay diversified, stay calm in these very volatile conditions,” he advised. “Investors can find greater diversity in ETFs and thematic ETFs than ever before, including around ESG, so these are ideal vehicles to consider for their portfolios.”

DPM can and should be constructed to take into account private client’s individual situations

Another guest offered his arguments for DPM. “We strongly believe that DPM offers significant advantages for clients,” he reported. “It helps clients stick to their strategy, it helps clients to be tax-efficient, it helps with the accurate rebalancing of portfolios. It's proven over time that having a more consistent approach is simply better for your returns longer term.”

He explained that the DPM activity should also reflect the client's personal situation, his or her tax position, as well as their plans and goals. “Almost all of our clients are international clients living in different countries, having businesses in different countries, and DPM can be tailored to their particular situations,” he reported. “Nobody is the same or takes the same approach. We have bigger clients who simply want a core approach and don't want to be talking or looking at their portfolio very often. We have smaller clients who want to be more involved. We need to cater to each one of them.”

He said DPM can encompass a wide range of portfolio options, so part of the process is helping clients to optimise their portfolio choices, starting from their core DPM portfolio, where they use a lot of ETFs to very individualised more single-named portfolios where they can build in certain tilts that clients might find interesting. “In this way,” he said, “we can complement their other positions, because people always have other assets, whether property or businesses, or perhaps private equity, so we aim to achieve balance and take those elements into account. We also need to look at the efficiency in terms of costs and how things might impact their tax positions. DPM can help in all these areas.”

The DPM market’s evolution is being helped by digitisation and other software advances

A panellist commented on the evolution of DPM in Asia since the GFC, remarking that the basics had not changed, but the technology around it had evolved. “Nowadays, we all have access to integrated portfolio management systems, and most of the custodian platforms, even the more traditional private banks, are becoming more digital and helping make it more efficient to implement portfolios across the board,” he reported. “The data is a lot more transparent with a lot more data providers, and that all helps to optimise portfolios in a way that maybe 10 to 15 years ago, only large pension funds could do. We can now do it for relatively small portfolios.”

The stars are better aligned for active portfolio management by asset management firms and through DPM mandates

A guest highlighted the value of DPM and also of actively managed funds within those mandates. “My view is this is one of the best times in recent history to be an active manager,” the told delegates. “Look at the performance this year – had you been passive, particularly in developed markets, you would be down double digits in terms of equities. That is a quite significant destruction of wealth. But as an active manager, we take a valuation lens, and as such, we have a clear focus on the upside or downside of stocks and what a company can produce over the long term, hence a solid price target. In these types of volatile and bearish markets. With such clear views on valuations, we can move in and out to achieve alpha.”

This same expert explained that in an environment of a falling tide in the markets, investors need to be smart and adopt interesting ideas and thematics, with especial focus on climate change, absolute return and commodities.

“This is a difficult market,” they observed. “There are growing recessionary fears. There are serious concerns about earnings disappointments, particularly in US tech, but I think tech more generally around the world. And rates are rising, so all this means that some of the easy, typical ways to position portfolios, for example by taking on more fixed income, are very tough. And central banks around the world are tightening. Investors have to be very astute and selective, to build in hedging potential in the portfolios while retaining some upside. Shifting from growth to value, focusing selectively on absolute return, on resource equities and on themes around climate change all offer potential.”

DPM at scale – how the mass affluent market can be served digital DPM and the smart curation of ETFs

A guest told delegates how their platform aimed to democratise access to portfolio management digitally to an under-served mass affluent market.

“They are typically pushed a lot of products through bankers who have fundamental misalignments in terms of how these products are supposed to be marketed and how the advice should be delivered,” he said. “Our fundamental value proposition is that we espouse a long-term passive investment strategy. And we want investors to remain committed and invested through their investment journeys, because when you're trying to solve for your long-term goals, which are 10 years, 20 years down the line, in our opinion, there is no point trying to time the market or trying to second guess the market.”

He advised that the best way is to position to be super-efficient and low cost. “We use ETFs as building blocks to our portfolio construction. Actually, if you look back at data, 85% to 90% of active managers end up underperforming the benchmark,” he cautioned.

He explained that clients can also express themselves and take views on the market as and when necessary. “However, we believe clients need to understand that the bulk of their money should be in more passively oriented strategies, so we recommend those for long-term oriented portfolios to help clients navigate through these ups and downs of the market, but without reacting to those waves.”

To achieve this effectively, he reported that these clients need to choose their risk profile correctly. “So, we focus heavily on making sure that we educate our clients to first understand what their risk appetite is, before selecting particular portfolios we offer,” he explained. “And then when they want to express themselves if they want to hedge against inflation, there are satellite strategies such as thematic portfolios, and other ways to custom build on top. To achieve the scale, everything is delivered via technology.”

He added that while their offering is aimed at the mass affluent market, they had drawn a lot of interest from the HNW market as well, due to the simplicity of the offering and the ease of access. He explained that the reason for this is also because the technology allied to the regulatory environment mean they are able to offer the same types of institutional risk management approaches and frameworks as offered by the big banks, pension funds and others. And all at low cost. Moreover, investors’ portfolios are rebalanced automatically, dividends are reinvested, there are no entry fee, or exit fees. People can see what they are buying into and have flexibility. All this is made possible by the technology we apply.”

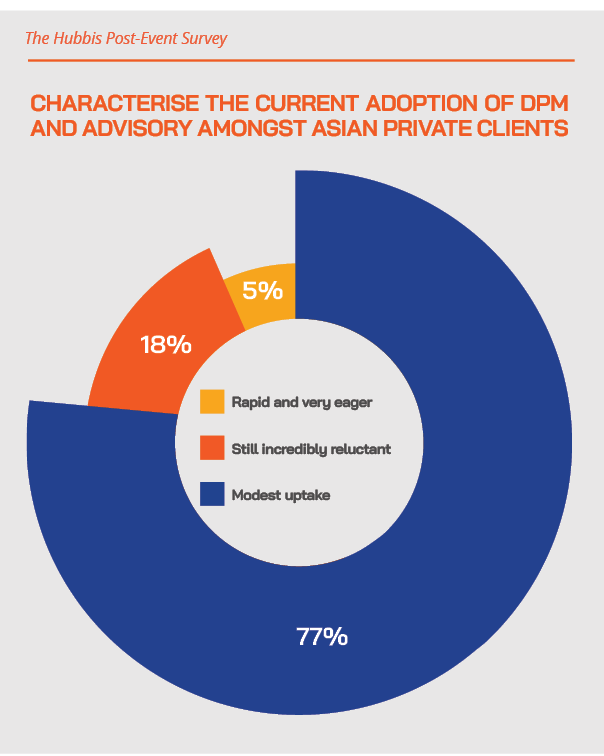

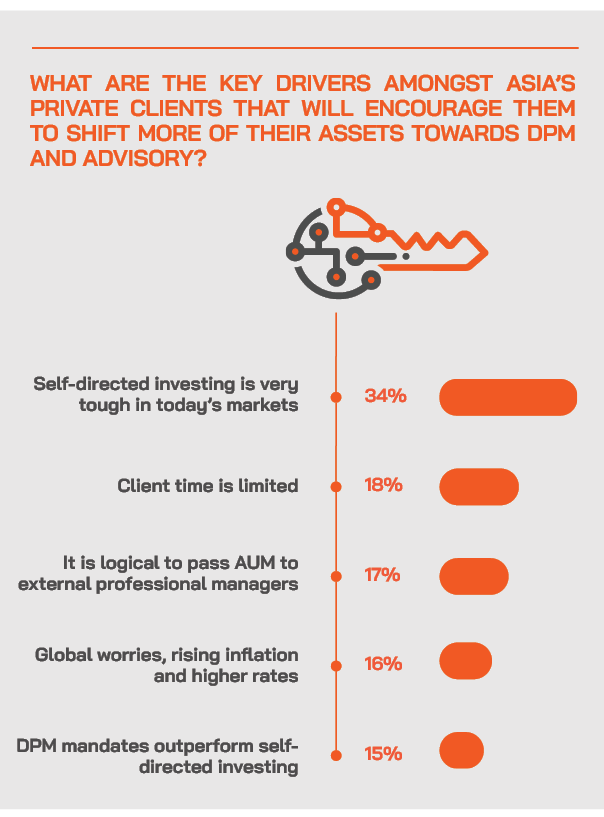

The reality remains that adoption of DPM amongst Asia’s private clients is improving, but more progress is needed

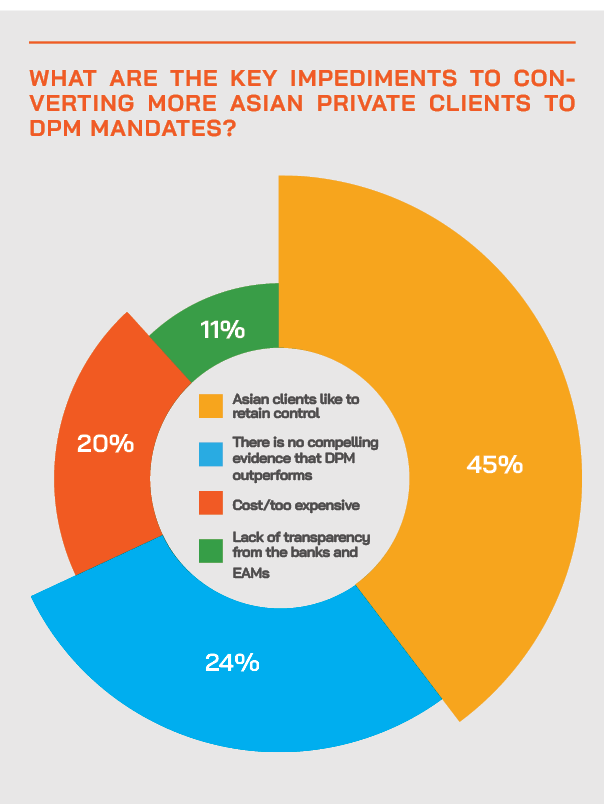

Despite all these positives for the adoption of more DPM mandates in Asia, progress remains slower than proponents had anticipated. “Actually, I have managed DPM portfolios since 2001 in Asia, and the progress has been much slower in Asia than in Europe, where perhaps one-third of all AUM is in DPM, but here it remains much lower,” one banker reported.

He said there are several reasons. The inclination towards more of an advisory business model that some of the banks have chosen still appeals to clients in this region. Large swathes of Asia are emerging economies and emerging markets where GDP growth is such that clients can rapidly expand the size and profitability of their own private businesses, allowing them to generate a lot of personal wealth at real pace. And many clients still prefer their own self-directed approach, although that is likely to change amidst these difficult market conditions.

“Things are changing,” he observed, “as we are shifting from a low interest rate environment anymore, and we are in an inflationary world. Of course, there will be economic growth, but it will be more difficult, and having a manager to help you at least be consistent in implementing your views is very valuable. I certainly believe this will continue to become a more professional market, with the type of evolution as we have seen in the US market, for example.”

A guest remarked that DPM allocation does not prevent clients from managing their own money as well. An ideal combination, he indicated, is often DPM alongside advisory/self-directed. “Quite often, when the clients play their own portfolios, they tend to take much more risk in a less consistent way, so they tend to do well in up markets and a lot less well in down markets. Then they realise after a couple of years they could just as well put it in DPM. And as to costs, clients might think DPM is expensive as there are fees attached, but we also know that these clients are paying a lout out in trailer or other fees in their self-directed investing, and perhaps taking greater risks and achieving less in performance at the same time.”

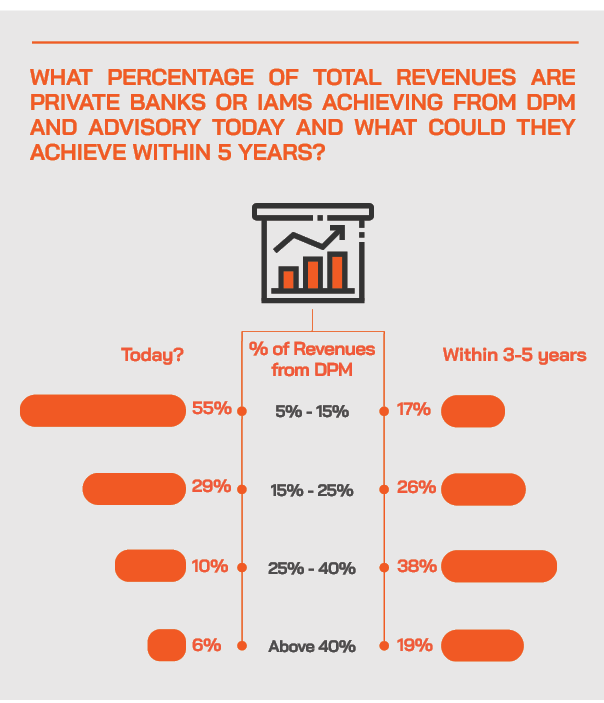

Another expert who specialises in Hong Kong and China, agreed adding that growth is coming, albeit from a low base. He estimated in the past five years, the penetration rate had increased from roughly 5% to around 10%.

“That is good growth, but it's not there yet to compare with the rest of the world,” he commented. “I feel the mentality is changing a little bit, nevertheless. Before people did not pay much attention to DPM, as returns they were making were so easy, especially for the onshore mainland customer. But we have seen some of the easy returns, for example fixed income for real estate developers, turn very difficult, the same is true for the SOEs in China. So, clients there understand increasingly that nothing is risk-free, and nothing is too big to fail. Moreover, they see that the concentration risk of home bias can be devastating. So, we see DPM growing in importance and in acceptance.”