Publications & Thought Leadership

Asian Private Clients and their Investment Opportunities and Challenges for 2021

Jan 27, 2021

Does anyone know the direction of travel for the world’s economies, for equities, fixed income, real estate, commodities, currencies or alternative assets of many different types? The answer, in reality, is ‘no’, but therein lies both the opportunity and the challenge. The chaos wrought on economies, businesses, government finances, individual liberties and of course, in the financial markets has been dramatic and shocking to all. What then is the next phase for Asia’s wealthy investors as the world struggles to escape the straitjacket of lockdowns and economic malaise, of rising unemployment and burgeoning state debt, and as they re-calibrate their investment portfolios in the face of all these events? The Hubbis Digital Dialogue of January 21 brought together a panel of private bank and wealth management experts to give their perspectives on where to find value and return without excess risk. The debate was naturally forward focused on the implications for the world of investments for the immediate future in 2021, set of course against the potential economic and investment landscape of the years beyond. The experts targeted their insights at what they consider to be the right choices for investors in the region to be making in 2021, helping them to assemble portfolios that find the right balance between the universe of mainstream public and also private and alternative assets, as well as the implications for active versus passive, and for self-management versus handing the responsibility off to discretionary managers or taking the half-way house of advisory mandates. A truly fascinating and insightful discussion played out.

The opening comments went to a banker who observed that while there is much uncertainty, their view is to stay with the idea that there is stronger and stronger likelihood of reflation boom by the second part of the year, which therefore demands more exposure to highly cyclical assets, and of course, equities, but within equities, probably more small and mid-caps, with a particular focus on IT and semiconductors, North Asia, and China technology. “That is the main focus of our advisory currently,” he reported, “and in light of this and other factors, we remain bearish on the dollar, particularly relative to emerging currencies and the Yuan.”

Rotating within equities

Another expert said their firm recommends clients to overweight equities but to rotate within equities, away from the early beneficiaries of the pandemic and towards the beneficiaries of a reopening of society and life as we knew it. Geographically, he advised that also means rotating to the emerging markets, particularly Asia ex-Japan, especially North Asia. And as the US dollar has an inverse relationship with US inflationary expectations, the dollar should weaken, playing well for emerging markets, and Asia ex-Japan.

“Nevertheless,” he commented, “we've had the longest bull market in history, followed by the shortest bear market in history, and all of that in the middle of the worst pandemic in 100 years, so it seems a strange time to be overweight in equities, but it is also unfortunately a necessary time to be in equities. The structural decline in interest rates all over the world caused by the pandemic has more than offset a temporary loss of corporate earnings. So, that's the whole logic of the discount rate and net present valuations prevailing today.”

He added that corporate earnings had not fallen anywhere near as much as during the Global Financial Crisis, largely because of the scale of government handouts. “Financial repression is here, and fear of inflation, and the two of them are forcing people out of cash and into stocks,” he remarked. “And there is a lot of cash out there, in fact I saw data that US commercial bank deposits grew by 23% over the past year. In short, you must be in equities, you must take risk assets. We like EM, and in the developed markets we like financials, the energy sector, and the oil majors, which I think are extremely cheap and are geared towards a reopening of economies.”

Expert Opinion - Say Boon Lim, Senior Advisor, Premia Partners: “We continue to overweight equities. The structural decline of interest rates caused by the pandemic has more than offset the temporary decline in corporate earnings. That’s the logic of discount rates and net present valuation. Also, financial repression is forcing people from cash to stocks. It is perfectly rational to be in stocks if you fear financial repression, particularly if that financial repression could lead to inflation down the line. Note that US inflationary expectations, as measured by the US 10-year breakeven inflation rate has been rising relentlessly since March of last year. And the US Dollar Index DXY has been declining in negative correlation to that. That forces perfectly rational people into stocks, even when they are aware that equities valuations are above historical averages. And within equities, our preference is Emerging Markets and Asia ex-Japan. For Developed Market equities, we had been recommending rotation trades out of ‘Work From Home/StayHome’ stocks – that is information technology, communication services, online retailers, and content streaming – into stocks that would benefit from a reopening of economies on the end of the pandemic. That rotation also works geographically, away from the US to laggard Emerging Market and Asia ex-Japan markets.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific - Chief Executive Officer, Hong Kong, Lombard Odier: “We do not believe that more fiscal stimulus, in particular in the US, should lead to tighter monetary policies. This should only happen if temporary, cyclical reflation evolves into long-term, structural inflation. If investors confuse the latter with the former, and if central banks’ guidance is not proactive enough, then volatility will strike again.”

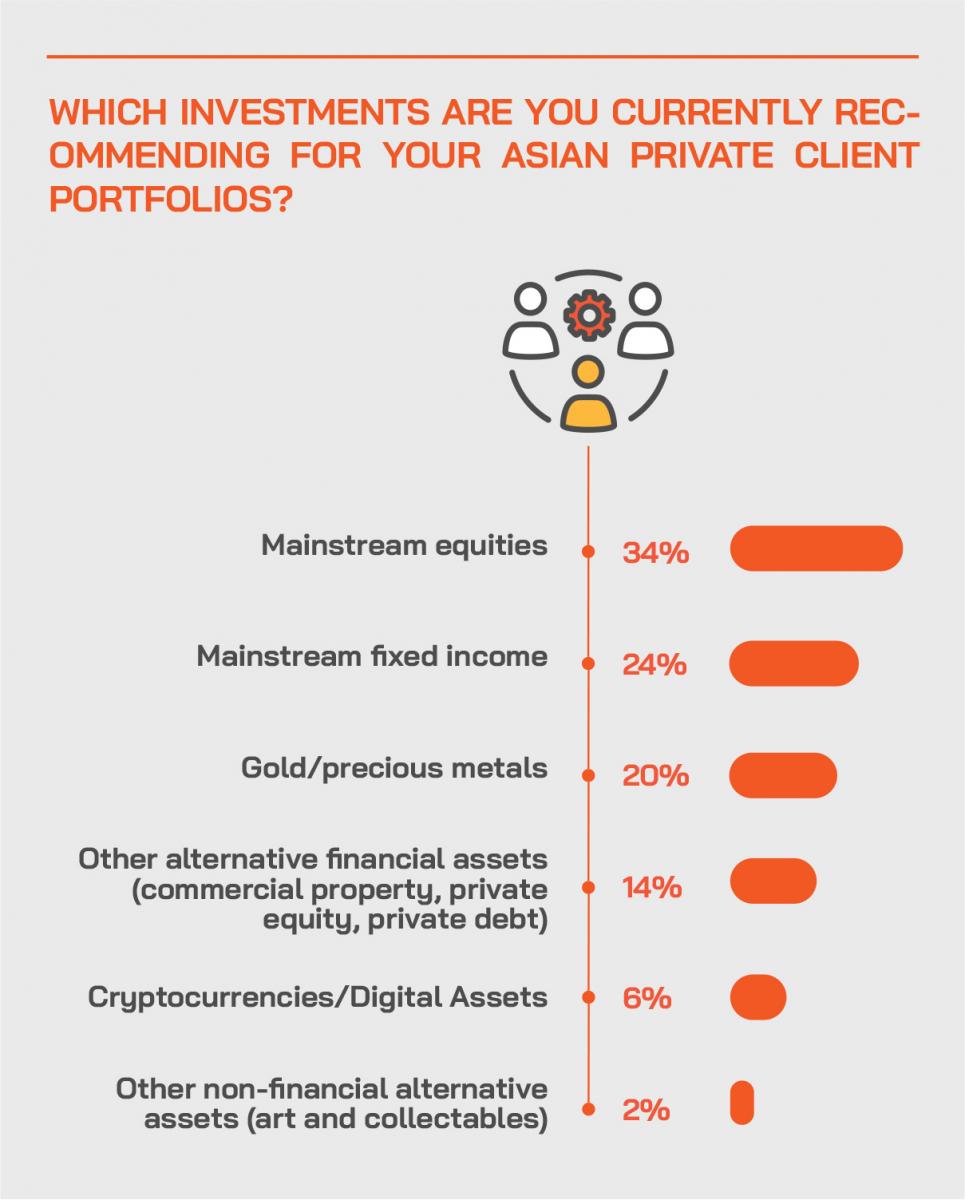

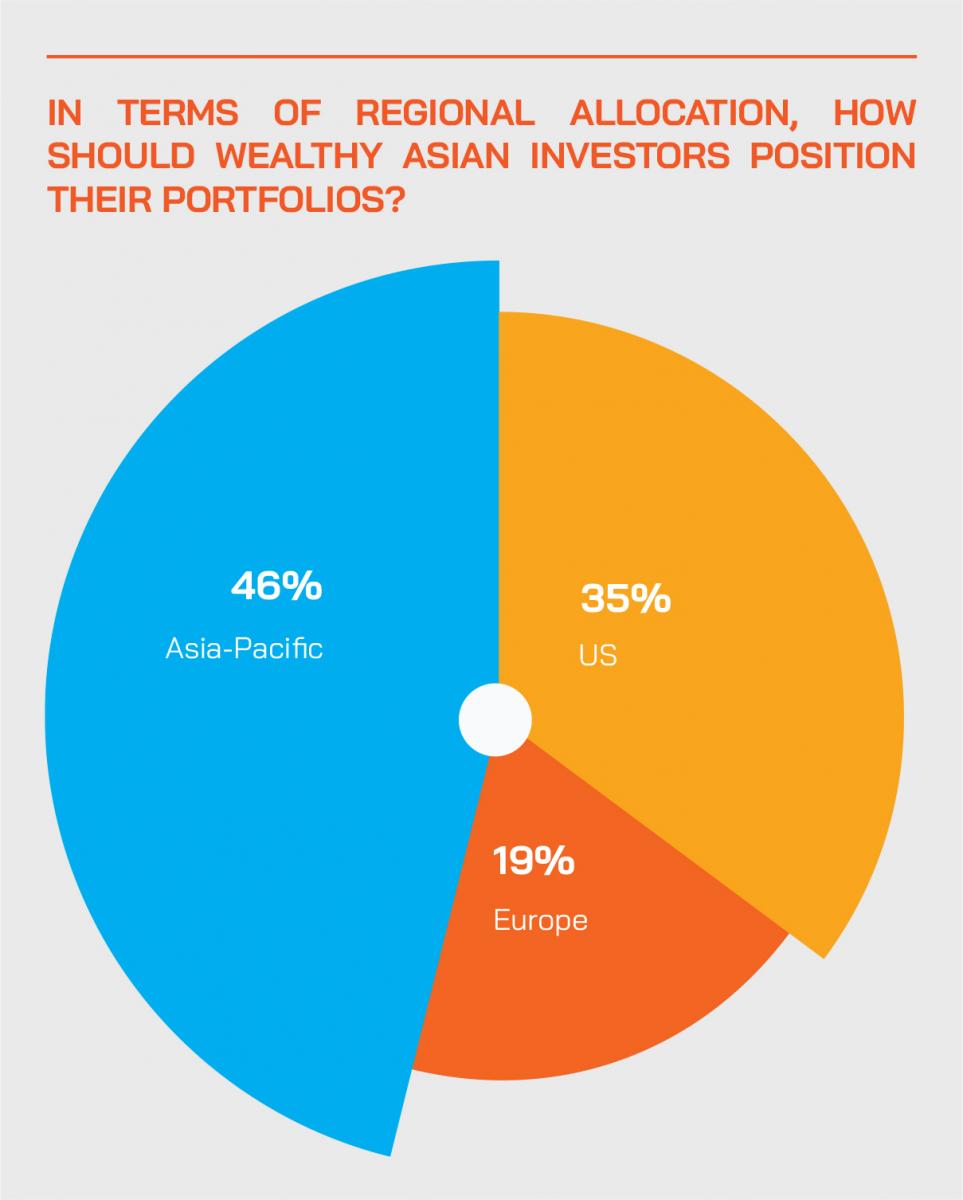

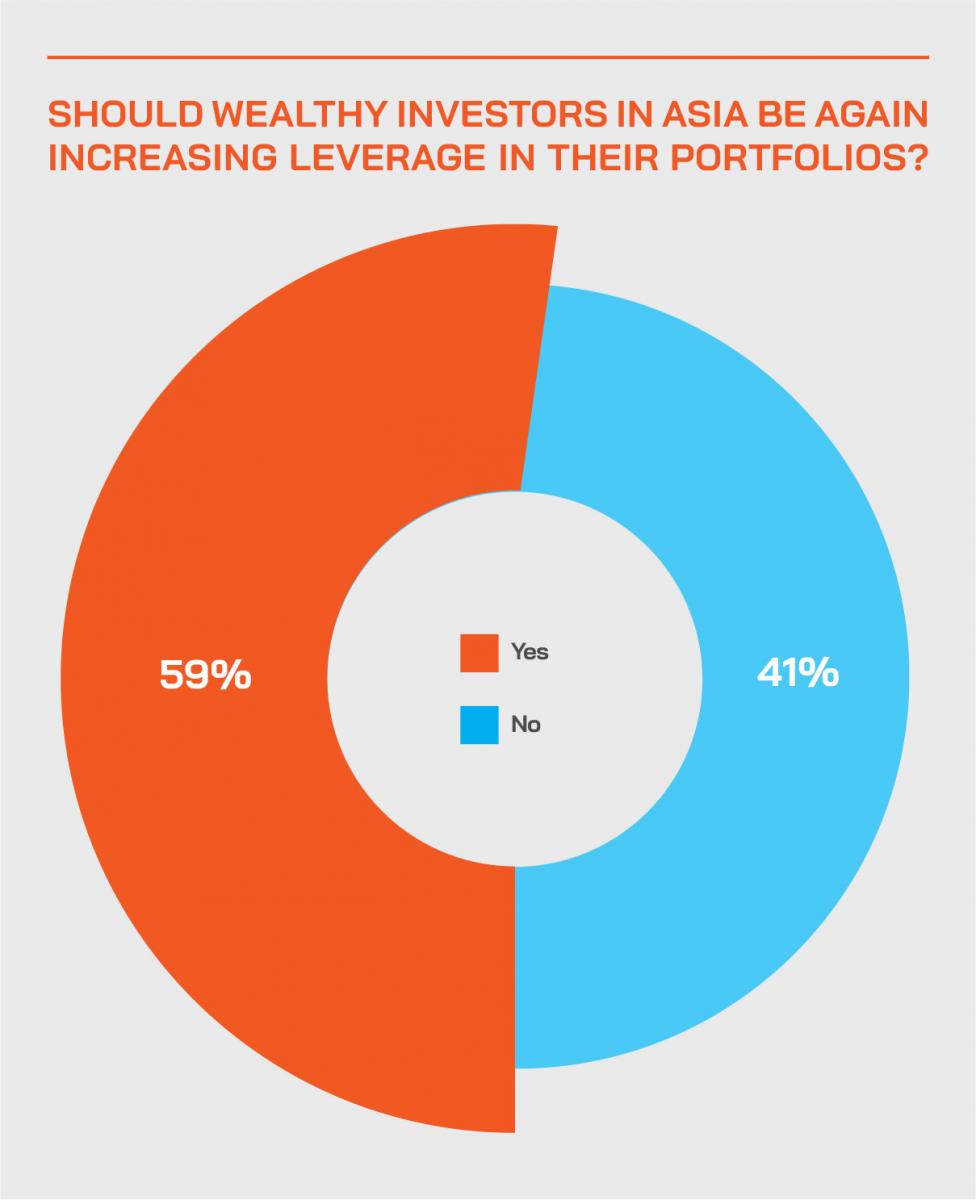

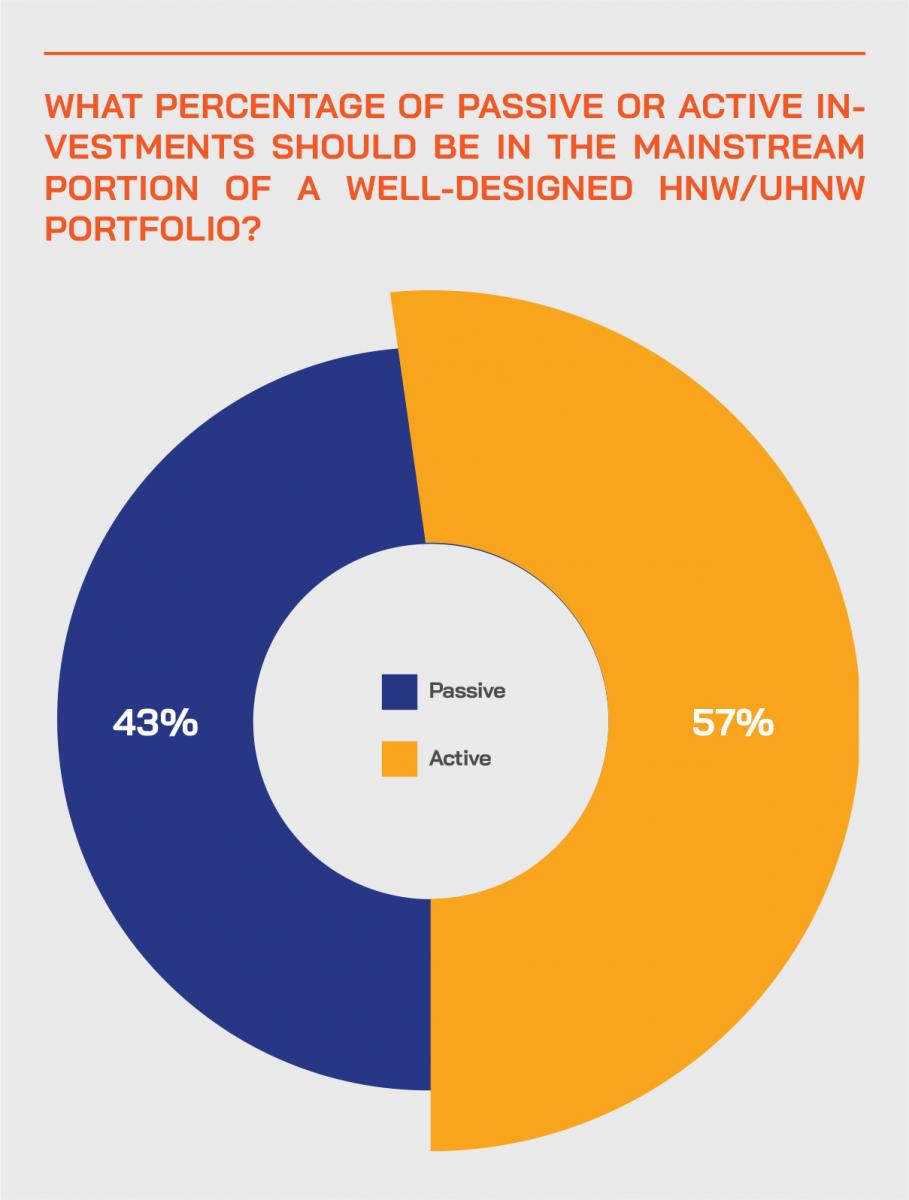

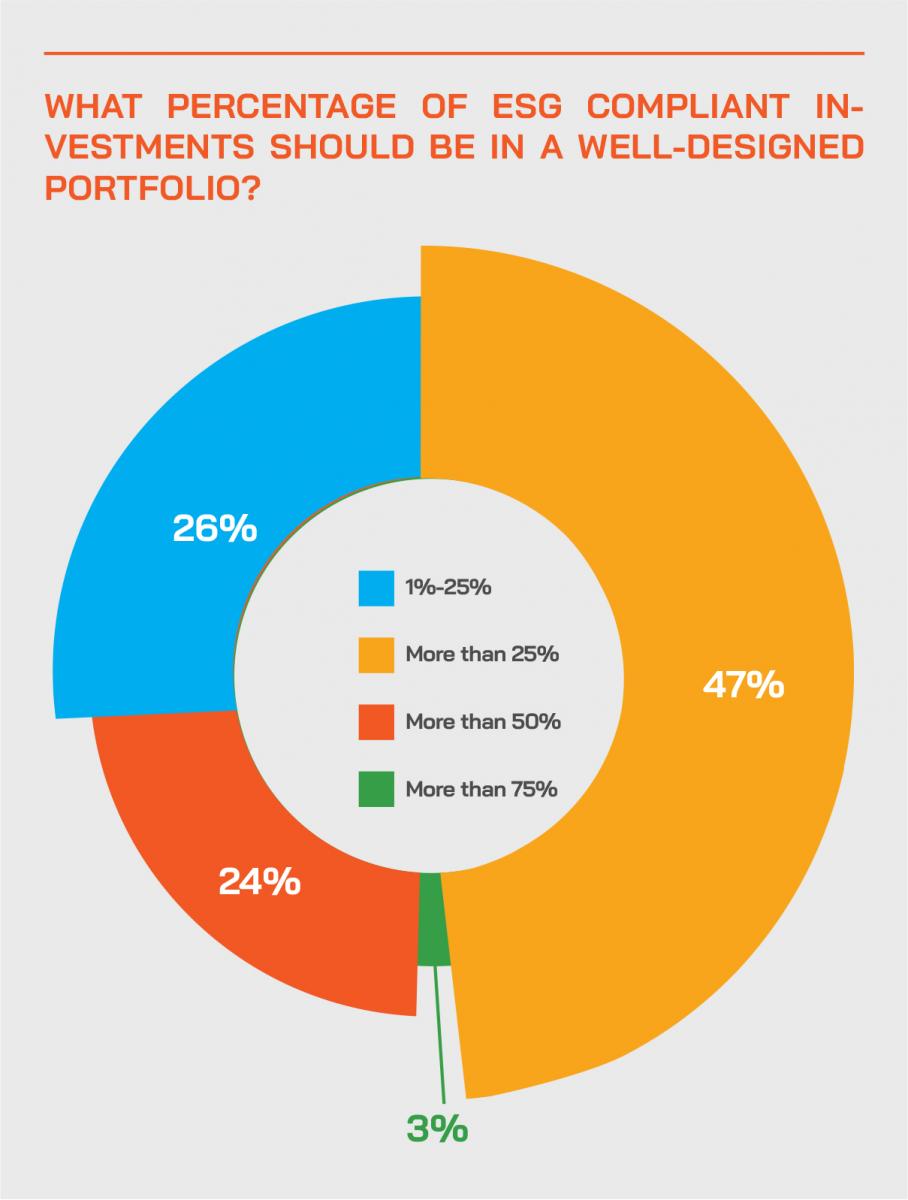

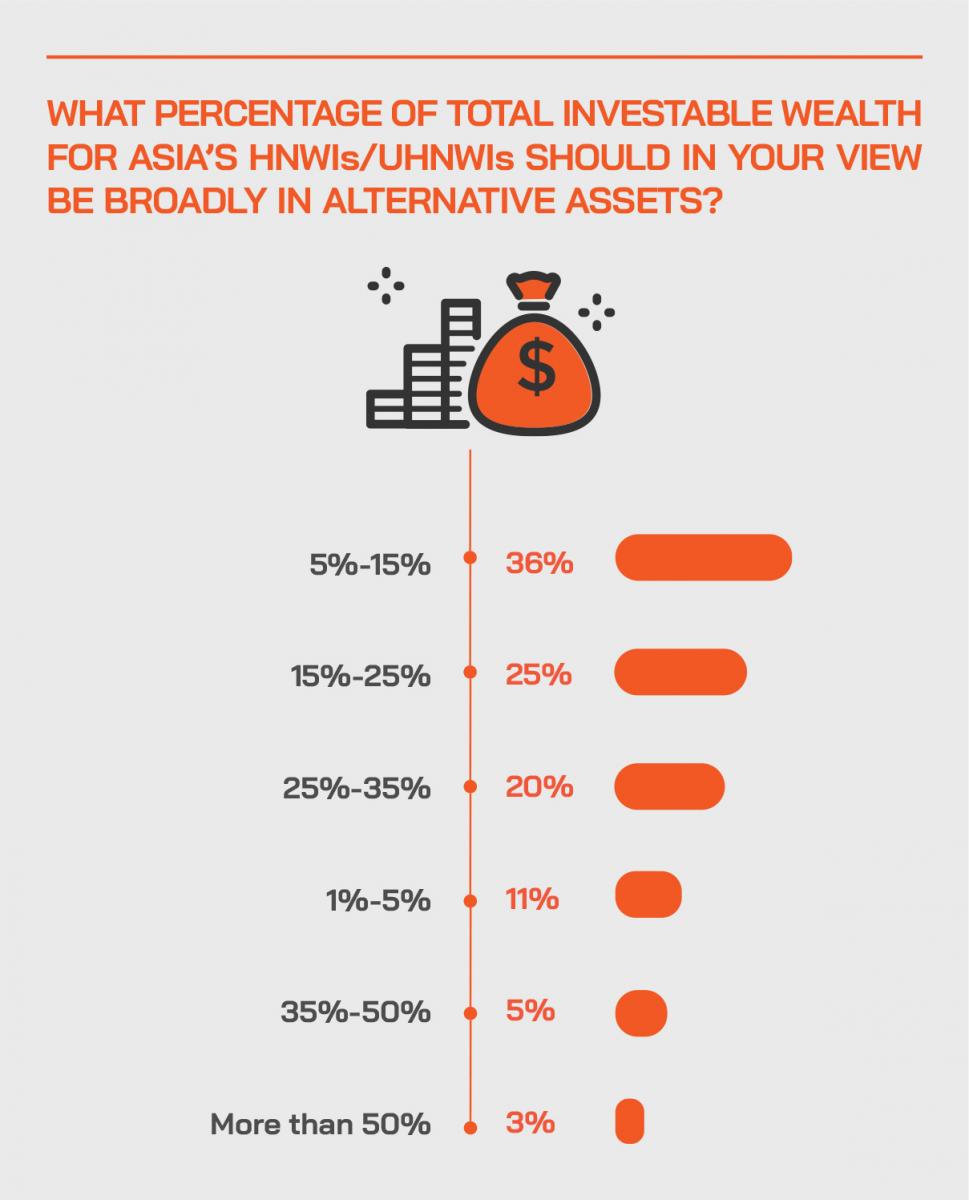

The Hubbis Post-event Survey

Searching for yield and safety

Another view came from a guest who said that while they like stocks, many of their institutional investors are still very hungry for yield, for defensiveness, “Right now,” they explained, “we are talking to our clients around three concepts - the need for income, yet yields are so low, then the need for protection yet duration looks even more risky these days than not, and the need to actually meet other obligations, whether it’d be regulatory or solvency that keeps them firmly very much in the fixed income side of things. Inflation risk is a major concern that most institutional investors are facing, because they need to match or outperform inflation. Fixed income today is where there's a lot more difficult that for equities in terms of the risk-reward trade off.”

The Hubbis Post-event Survey

Immediately after the event, Hubbis asked the delegates for their views on the evolution of portfolios for their Asian private clients. We have set out a selected representation of their views below.

Hubbis: Briefly, how are you positioning Asian HNW and UHNW portfolios for the year ahead, and why?

Delegates views:

- More ESG-oriented investments will have a larger weighting due to their potential in delivering growth.

- To be fully invested as Biden is in the White House now.

- Diversification of portfolios, due to uncertain markets.

- A stronger focus on climate change, and also ESG as there are signs of traction in Asia.

- In emerging markets and currency plays.

- To be better equipped with the right market information and strategies and good advice, as there is a volatile year ahead.

- We see 40% in cash, 20% property, 20% equities, 10% subordinated bonds and 10% precious metals. Why? Because of disconnections between stock markets and the real economy, huge national debts from stimulus packages and easy monetary policy, extremely low US rates and the increased potential for inflation.

- Overweight equities (particularly small cap with focus on technology, consumer technology, healthcare and ‘green’ plus large cap technology and healthcare), and in fixed income to focus on convertibles and Gulf states sovereign and sovereign-linked.

- Long ETFs in emerging Asia markets as these are the driving engine for the next few years.

- Overweight in equities, mostly in Asia ex Japan and selectively in the US.

- US equities and bond funds plus a long view on ESG.

- Underweight investment grade credit and overweight equities and commodities.

- The portfolios will be more aggressive with focus on equities in the US and greater China. China and US markets expected to have quick recovery and growth.

- Will position Asian HNW/UHNW portfolios to purchase equities mainly for capital appreciation and heavily skewed towards growth stocks in the market.

- Positioning for growth with a strong weighting to equities markets.

- Continued exposure to ETFs with an increased exposure to Alternatives for clients that can stomach the risk/reward and time profile.

- In view of Covid19 and new US President we need position the portfolio more on Asian, and somewhat downsize China.

- Half in equities and half in bonds because of uncertainty of Covid-19.

- China equities – the economy there will recover much faster than other developed countries.

- Equities 80% Bonds 20%.

- From a Family Office perspective, we believe the opportunity is good, but risk needs to be monitor closely. Equities in Hong Kong and China, Euro Dollars and Gold are my preferences.

- We have clients with different risk profiles, so it varies but in general we would highlight equities and to a lesser extent bonds for the next two quarters.

- Due to the uncertainty and volatility of the market, we will focus on liquidity as a priority.

- We like hedge funds - specifically multi strategy and global macro.

- Clients will seek to have professional manage their portfolio as opposed to making their own decisions in this environment.

- We are recommending 40% bonds, 50% equities, 10% gold.

- The fixed income markets as they are one of the best places to go for income from a return on liquidity perspective, with emerging market debt in focus. REITs are good as the property sector went through a difficult time in 2020 and returns might be quite good because of the recovery.

- Diversification and balance in the portfolio is still the way to go. A portfolio should benefit when the market is half full and yet be relatively well protected when the market is feeling half empty. In terms of country allocation, 30% in US, 25% in Europe and 45% Asia where the China growth story remains intact, and Asian countries where the pandemic has been well managed. In terms of products, structure of the portfolio should be according to the risk appetite and target returns, but we recommend a main focus on financials, energy, green energy, ESG, healthcare and biotechnology, the new economy in technology combined with dividend earning stocks for the yield. US dollar Emerging Market bonds and Alternative Credits, as well as PE and VC appeal.

- I think Asian HNW and UHNW portfolios for the year should likely position more in Asia, especially China which has in recent years seen high demand like online retailing and social media platforms.

- The focus will be overweight on equity/index ETF, structured products, while underweight on Treasuries and fixed income.

- Overweight APAC equities and Asian high yield, China equities and EM equities and Fixed Income. In equities, overweight Small and Mid-caps, and also diversifying into cyclicals and the energy sector. Currency wise, diversify into EUR and GBP.

- Head to risk off, suggest investing more into gold and a G7 currencies basket as the equity and bond market prices are too high with too much risk. Cash on hand and wait for the market collapse to pick up some quality assets later on.

- A very challenging year ahead. With a new US President, markets are somewhat bullish. Unfortunately, Covid-19 persists and with continued lock down measures,

- businesses are going to get hurt even more this year. Clients are quite happy to continue to remain heavily in cash. Tactical pays are preferred, rather than going in blind, as we believe we are still in unchartered waters.

- China, global technology, small cap and ESG. Why? There is less pressure on the Chinese government, rates remain low at least until 2023 and the vaccine programmes will take longer time to fight back against this pandemic.

- We are still overweight on equities but cautious of the increasing fiscal policies' effect on impending inflation. Try to look to defensive fixed income if possible.

Hubbis: What is your view on inflation and currencies?

Delegates Views:

- Cryptocurrencies are certainly something to pay close attention to vis-a-vis traditional fiat currencies. Some sort of inflation is likely despite contractions in the real economy.

- Inflation rising slowly.

- US dollar weakening on the continuation of low inflation.

- Inflation is closer than before, and US dollar depreciation can be seen as a quick solution to ballooning debt.

- I believe inflation will remain low due to the current economic climate.

- Inflation should be benign. The dollar will weaken.

- There is higher inflation pressure, better to go short the dollar and long the Chinese Yuan.

- We expect low inflation in 2021, and the US dollar to maintain at current levels throughout this year.

- We expect the dollar to be weak but not too optimistic on the Yen either.

- Inflation is coming, the USD will continue to weaken.

- Inflation will keep going up due to gradual economic recovery from Covid-19. For currencies, CNY will keep going strong and USD will weaken.

- USD will continue to devalue. We suggest going long CNY, CAD, AUD and short JPY and CHF. Inflation to stay relatively low.

- Inflation will be kept low by governments trying to save the economies.

- Inflation should be moderate this year and we will continue to accumulate gold against US dollar weakness.

- We believe de-globalisation may trigger regional inflation and the depreciation of USD will also favour commodities.

- There will be inflation and the ensuing appreciation of Asian and EM currencies.

- No inflation so far in sight and the dollar will consolidate with other currencies.

- Inflation won't be an issue in the near term.

- Don't think there will be inflationary pressure in 2021, and the dollar will be firmer under Yellen's guidance.

- Inflation is the second-most ‘popular’ view for ‘tail-risk’ for markets as we head into 2021. As currency moves can be a major risk, use the hedging instruments available.

- Inflation in general will be moderated by the pandemic and unemployment. We remain bearish on the dollar.

- I don't expect the USD to weaken a whole lot due to resurging coronavirus cases and the persistent pandemic, which in turn in my opinion should continue to keep the USD fairly supported although on the downtrend in the short to medium term. I do not also expect inflationary pressures to pick up in the near/medium term as central banks remain accommodative and supportive.

- Inflation and money printing are more of a concern, so the USD must depreciate finally. The CHF is more stable, the JPY will be in its role of risk-off currency and AUD and NZD bonds will be also good positions in a portfolio this year.

- The US dollar will be forced to remain weak. With rising global unemployment, inflation will surely move upwards. The SGD will still me a safe currency for most of my clients.

- We agree with panellists that the US dollar will continue to weaken and agree that inflation might lead to permanent stagflation.

Beware the consensus

Another banker pointed to private equity, remarking that there is great consensus currently. “In my 22 years of banking, this is the most consensus I have seen, with the view of dollar down and equities up. However, in the past, so often when there's significant consensus, something bad happens. Looking at the ongoing fiscal and monetary stimulus, we think there are still reasonable valuations vis-à-vis EPS growth, again, seeing a weaker US Dollar outlook, which is good for Asia. GDP growth, and better US-China relations will probably also lead to somewhat higher risk appetite.”

He concluded that with this backdrop, the bank is positive on equity markets, but somewhat more careful on US equities. “Because of the dollar,” he added, “we're bullish on commodity-related currencies, such as the Norwegian Krone, Australian Dollar, Canadian Dollar. We tend to now shy away from the Japanese Yen and the Swiss Franc, because as normalisation gradually takes place, they will somewhat lose their safe haven status.”

Mind the gap

A guest highlighted that 2020 was surprisingly positive given the bifurcation between the real economy and capital markets, and that their discretionary portfolios performed surprisingly well. He agreed with the view that the level of similar thinking currently was disquieting potentially. And that on the fixed income side, the firm still sticks to its view of going down further the capital structure.

“In fixed income,” he reported, “we're quite overweighted in subordinated debt, and preferred shares in the US. We're now looking at adding pipelines and utilities on top of that, at least for the income generation side, because the equity is there, and so long as inflation and expectations of inflation are well anchored on the low side, that growth story is there, but whether it is fully compensated risk is a big question.”

Expert Opinion - Arnulfo de Pala, Chief Investment Officer, TriLake Partners: “Regarding investor sentiment, there’s currently an uncomfortable consensus on risky assets. In particular, the widespread acceptance of TINA – There Is No Alternative – has driven money into equities especially in the last quarter. It’s practically an article of faith today that central bankers (and now national treasurers) will keep supporting asset values with financial repression and fiscal support. The last time the State Street Confidence Index was this high was January 2018 and we all know what happened at the end of that month.”

The focus shifted to China, its potential and ways to access that market selectively, with the panel agreeing that the combination of China’s apparent ability to control the pandemic, the ability to keep its domestic economic and export industries alive, and the liberalisation and therefore opening of its financial markets internally and externally were providing powerful reasons to upgrade exposures in equities and in debt.

Expert Opinion - David Lai, Partner & Co-Chief Investment Officer, Premia Partners: “After seeing a strong GDP growth of 6.5% in the last quarter, the China recovery will carry forward the current strong momentum with the consensus growth rate of over 8% this year. The overall equity market should be positive with the support of rebounding earnings, which would increase substantially comparing to the low base. The unattractive low yield environment in the fixed income market will channel fund flows into equities steadily. Increasing the proportion of equity in asset allocation is essential for investors in near future as the low interest rate phenomenon will stay and the expected return of bonds is not sufficient to justify the embedded risks. Within the market, 2021 marks the beginning of the 14th China five-year plan, on which the details will be unfolded in the next few months. Investor sentiment will gradually come back to the sustainable themes such as cloud computing, 5G network, artificial intelligence, electric vehicle, new energy, e-commerce, and biotech.”

ETFs aplenty

Another expert concurred, adding that aside from both broader and smarter/selective access to China, another trend is growing demand for what he termed ‘industrial’ ETFs, focused on certain themes and specific markets and segments.

“We had of course been using an increasing number of ETF strategies before,” he explained, “but this trend has accelerated a lot over the last few months, with strong demand amongst clients for these specialised ETFs. They have also over the past year produced some excellent performance for our clients.”

An expert then pointed to the strong performance of some thematic smart beta ETFs they have promoted, based on the right selectivity at the right time to capture growth trends and opportunity, for example Premia’s China New Economy and its Premia Asia Innovative Technology. “And on the other end of the spectrum,” he added, “we can see mean reversion playing out, as people seek out the value opportunities available, such as the Premia ASEAN Titans ETF and our Vietnam, both of which will look promising on the rapid rebound in economic recovery and weaker USD trend. Remember that so far, Southeast Asia has been left behind because a lot of things have been shutting down, tourism, hospitality, all these kinds of things. But if the vaccination is going to be successful this year, I think a lot of appeal will come back to the ASEAN and specifically also the Vietnam markets.”

Focusing further on ETFs, a panel member commented how their bank was directing more and more discretionary mandate money through the evolving world of ETF to express and capture certain themes and views, but for regulatory reasons in Hong Kong generally avoids direct sales of ETFs to clients themselves.

Expert Opinion - David Lai, Partner & Co-Chief Investment Officer, Premia Partners: “As to investment tools for China, the new economy space is clearly benefiting from policy support and showing a clear roadmap in medium-to-long term. Premia China New Economy ETF (3173) would be a useful vehicle that taps the opportunities in information technology, healthcare, and consumer discretionary. And if investors continue to like riding on the overall tech cycle, then they may pay attention to Premia Asia Innovative Technology ETF (3181) which invests in a basket of top 50 innovative firms across China, Japan, Korea, Taiwan, and Singapore. For those who believe the vaccine will help bring back mean reversion in the equity market, then the laggards like Premia ASEAN Titans ETF (2810) and Premia MSCI Vietnam ETF (2804) will look promising on the rapid rebound in economic recovery and weaker USD trend.

A guest remarked that while their firm had been predominantly focused on active strategies, there are certain countries and sectors where given enough positive macroeconomic indicators, there is sense in considering the ETF route, mentioning countries such as Indonesia, the Philippines and Vietnam. “The idiosyncratic risks in these countries are far greater than in developed markets,” he explained, “so we tend to go to active managers with a great track record in these countries, but we are considering ETF access to certain countries and sectors within those countries. In fact, we have always gone in and out of Korea through the ETF route.”

Call the professionals

Shifting the discussion towards the investment approach that private clients are adopting, an expert commented that after the volatility of 2020, there had been a trend for clients to be more and more willing to go into so-called managed solutions, including funds, fund of funds, advisory mandates, discretionary mandates, structured products, and fixed maturity products for fixed income, which remain very popular. “In general, we have noted a lot of positivity, and this continuing marked trend towards more delegated solutions.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific - Chief Executive Officer, Hong Kong, Lombard Odier: “Renewed fiscal stimulus plans adopted to buffer the negative impact of current lockdowns on first quarter activity should fuel pent-up demand when economies re-open fully. There is an increasing possibility of a reflationary boom in the second part of 2021. Markets’ expectations will resume with this perspective as the progress of the vaccination campaigns will become more explicit.”

Expert Opinion - Say Boon Lim, Senior Advisor, Premia Partners: “We will get sharp rebounds in economies around the world, even without rapid reopening of societies. Even with continued social distancing for most of the year, we should still get around 3% GDP growth in the US; 4% in the Euro area, 2% in Japan, and around 8% for China. With gradual roll out of vaccines, we should see business confidence rise, and there could be some upside surprise to those numbers from inventory restocking. The biggest opportunities are in commodities, which should benefit from reflation, and even better from inflation. Crude oil has seen a lot of supply restraint and supply destruction and its price is still significantly below the pre-pandemic peak. Industrial metals have already gone up a lot, but we could see it go higher yet, to the levels reached in the surge from 2009 to 2011.”

(Some of) the dangers ahead

There are of course plenty of dangers ahead as well, and the panel discussed just some of those. Amongst those dangers, one guest commented that the pandemic is far from beaten back, indeed getting worse in many countries and regions, and the tail-risks from mutations and worse forms of Covid-19 are significant. Meanwhile, he commented that the more mundane economic risk is the risk of reflation - generally a good thing - but with the danger of turning into inflation, or worse, stagflation.

With yields on prime debt where they are, and expected to remain so historically low, he said he likes dividends and combined with lower valuations. “That directs us towards financials, energy, selected Asia ex Japan markets, and China,” he said.

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific - Chief Executive Officer, Hong Kong, Lombard Odier: “Can reflationary trades lead to a sustainable rotation from growth to deep valued assets? We do not think so. Beyond the strong cyclical catch-up that should be experienced later in the year, the structural conditions for higher growth and higher inflation regimes in the long run are just not there.”

Another guest reiterated the dangers of inflation. “We are in a situation where all governments will have to spend in order to support their economies, but rising unemployment will potentially breed a lot of negative sentiment,” she said.

A panel member refined that view, noting that there is a risk of confusing legitimate cyclical inflation that should emerge, especially in the second part of this year, with a more permanent structural reflation or inflation path.

Cyclical or structural inflation?

“If all the legitimate cyclical reflation should show up in the coming months, and that might be pretty strong actually, there is a risk that investors suddenly are bit surprised, that they would interpret it as a new path for growth and for future and permanent inflation. And then it will lead to new renewed expectation that there will be policy normalisation, so on and so forth, then we will see a lot more volatility, as in 2018. That is why it is vital we have right proactive guidance from central banks, so we understand with the new monetary policy regime [in the US] there's no reason for them to react to what is only cyclical inflation, not permanent structural inflation.”

He added that as investors see a boom of money going onto the market supported by public policy, there is the risk they confuse cyclical reflation both in growth and in prices with a more permanent new regime of growth and inflation. “That, in our view,” he cautioned, “would be a mistake.”

Expert Opinion - Say Boon Lim, Senior Advisor, Premia Partners: “Historically, pandemics have tended to be followed by deflation and wars have tended to be followed by inflation. The logic is that wars destroy productive capacity, while pandemics destroy demand. But we have some important differences with this pandemic: 1) It has a war-like quality about it through the extreme monetary expansion which is what you typically see happening in wars when governments print money to finance the war effort. 2) Productive capacity has also been affected through the disruption of the global supply chain in a manner not seen in previous pandemics. 3) There is also a distributive element in the pandemic relief measures around the world. It tends to benefit lower income groups more, and they have a greater propensity to consume than higher income groups. And that will in turn contribute to higher inflation.”

A fellow panellist agreed, noting that there is also plenty of room for policy mistakes. “Given the disconnect that we have [in valuations and reality] I think the risk grows higher, but so long as the authorities and monetary authorities have their finger on it, then it's fine, we are breathing a little easier. But remember that nothing is holding them to their policies, it's a pronouncement for now, but it's not a guarantee.”

Cryptos – approach with caution

The discussion shifted to cryptocurrencies, with an expert observing that their firm does not view them as currencies, and for a variety of reasons arguing that this is the kind of asset for sensible investors to avoid. “We don't deny that there is room for these prices to continue to increase this year, because the global excess liquidity will not go down markedly, but the discrepancy between price and fundamentals is so huge, bigger really than for any other asset classes. Accordingly, we do not recommend our client to go into crypto assets.”

A fellow panellist agreed, cautioning that there is no rational basis for their valuations. “We do not advise our clients to buy them, we do not offer them to clients,” he stated.”

Expert Opinion - Arnulfo de Pala, Chief Investment Officer, TriLake Partners: “No doubt people have made money and we may very well be using (regulated or not) digital currencies someday. Nevertheless, as money managers, we deploy our clients’ money into investment and not speculation. Can the asset generate cash flow, if not today, then in the future? These assets should be able to return your investment – yes, it may take years – without having to sell it to “the bigger sucker.” For example, raw land might be speculation for, say, a dentist, but it is an investment for a property developer, a farmer, a parking lot operator, someone who can turn it into a productive asset. The dentist is just speculating that he could sell it at a higher price to someone else. Nowadays, many government bonds of developed markets don’t generate positive cash flow either. But at the very least, Swiss francs, Japanese yen, gold have been traditional stores of value. I can’t say the same about Bitcoin.”

Breaking through resistance

Turning back to the equity indices and the new US administration, a guest said he expected the S&P 500 to break through the 3800 resistance level, which will have knock on effects for other markets. “But as we know,” he added, “there is no such thing as a free lunch, so the flip side is inflation and the continued weakening of the US Dollar, and those will at some point choke off the equities bull market. I don't think it's going to happen in 2021, but it might well be a problem for 2022.”

And another expert remarked that the gargantuan debt across the US and so much of the developed world is a problem that will have to be addressed at some time. “The problem with fiscal stimulus,” he warned, “is that it's easy to hand out, but incredibly difficult to wind back.”

“Yes,” came another voice, “at some point, you're right, somebody has to pay the piper and over the past 20 years no developed economy has been able to outgrow the debt. You can kick the can down the road but how far down the road you can keep doing that?” And with that he raised the spectre of higher taxes in the future.

ESG rules

A guest highlighted the rapidly expanding institutional and private client demand in Asia for investments that are ESG-centric but warned that people need to conduct their research properly and steer clear of widespread greenwashing. With the right approach and research, the whole ESG phenomenon is both highly laudable, they commented, and good for investment returns and for the companies and boards that practice ESG properly.

Another expert agreed, adding that in Asia, the more professional the clients are, so institutions, family offices and others, the greater the focus on ESG. “As more institutional money globally flows into high ESG credential securities then in itself, you have demand and supply issues that create an outperformance for ESG.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific - Chief Executive Officer, Hong Kong, Lombard Odier: “In the tug of war between the pandemic’s reacceleration and the rollout of the vaccines, the rapid spread of new, more contagious variants of the virus and the chaotic start of the vaccination programs have raised the perception that the pandemic was leading the race. However, this perception should change within the next few weeks.”

The discussion closed with the experts reiterating some of their earlier views and recommendations, set against the backdrop of the broad discussion that had taken place. As one guest said for a final comment: “There is great optimism out there, and immense liquidity, we now have to hope that the vaccines can truly turn the tide against this virus. We must all hope and believe they will.”