Asia’s Private Clients and the Return of Hedge Funds in an Uncertain World

Jun 11, 2023

In the Hubbis Digital Dialogue of May 11, a panel of experts drilled down into the role of hedge funds in the wealth management community in Asia, aiming to identify the key characteristics of these hedge funds and to debate why they should suit certain investors and also what liquid alternatives/hedge funds are out there and performing well.

The Panel:

- Rada Tuntasood, Director of Hedge Fund Advisory, Bank of Singapore

- David Elms, Head of Diversified Alternatives, Janus Henderson Investors

- George Boubouras, Executive Director and Head of Research, K2 Asset Management

- Harmen Overdijk, Chief Investment Officer, Leo Wealth

These are some of the questions the experts addressed:

- Given more difficult and challenging markets - what hedge fund strategies will deliver the best performance today?

- Are ‘true alternatives’ now increasingly relevant? And why?

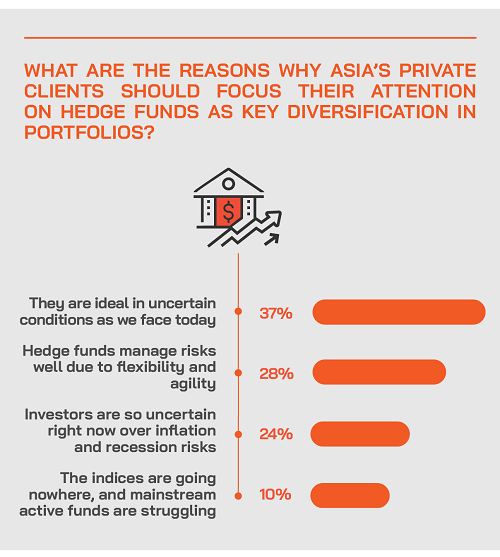

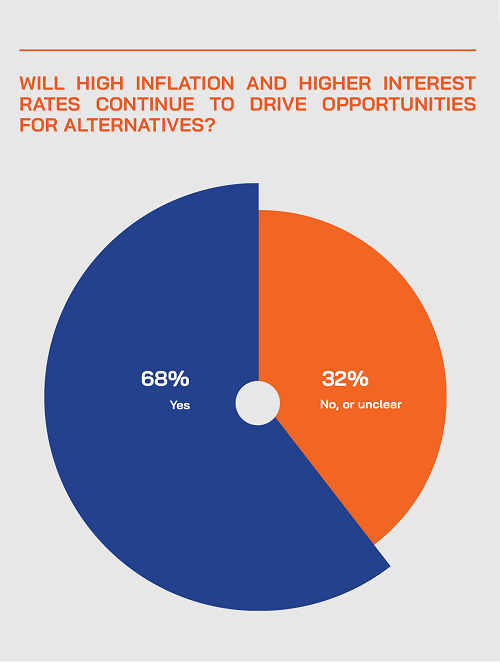

- Will high inflation and interest rates continue to drive opportunities for alternatives?

- Hedge funds do not always perform well – take 2020 for example – so how can investors make sure they are in the right funds with appropriate risk management protocols?

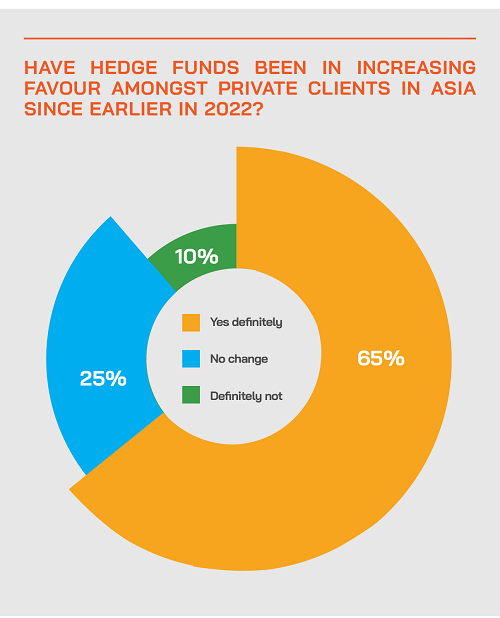

- Are hedge funds already in greater or increasing favour amongst private clients in Asia, and why or why not?

- What are the downsides of buying hedge funds?

- Where should private clients in Asia source their advice and expertise to determine which strategies and managers to invest in?

- What is coming next in the world of hedge funds?

Setting the Scene

Liquid alternatives in the form of hedge funds have been a key theme amongst the private banks and more broadly the institutional investor community since the main global markets turned downwards in early 2022 and since so many people lost money.

In a falling market, one of the few ways private clients could make money, or at least to preserve capital, was to diversify for downside protection through hedge funds that are investing in liquid, diversified alternatives representing non-correlated returns.

There is both considerable logic and opportunity in this type of approach, as hedge funds have played a crucial role in providing liquidity for mispriced assets, particularly when large volumes are traded in thin markets thereby reducing market volatility.

Hedge funds enjoyed an encouraging Q4 in 2022 and continued that performance in Q1 of this year. Their performance came on the back of investors trying to navigate unprecedented uncertainty associated with the ongoing military conflict in Ukraine, continuing rises in interest rates, and more bad news on inflation. Liquid alternatives in the form of hedge funds covering all types of markets, assets and geographies are therefore increasingly interesting routes for private clients.

They can perhaps most ideally suit those private clients with risk aversion – perhaps who have been left scarred by the events of 2022, and who want to draft in more protections to their portfolios but also with some good upside.

And there is plenty of choice - combined, the top 100 US hedge funds managed USD2.75 trillion in assets as of 2021 with nearly USD1 trillion managed by the top 10 US hedge funds alone, and in that period, multi-strategy, long/short, and credit were the most common strategies employed. And those vast numbers do not of course include all sorts of hedge funds across many global markets, with a broad array of approaches and strategies.

The panellists debated the merits of hedge funds in an uncertain world, discussed whether Asia’s private clients should be allocations to hedge funds and if so, how much of their portfolios, and analysed how the wealth industry should be approaching the dialogue with their private clients.

Key Insights & Observations

The tide is rising for hedge funds as part of core alternative investment allocations for private clients

2022 was for most major markets (except the UK and notably some of the key emerging markets) somewhat of a disaster for conventional investments, with equities and bonds down significantly. Hedge funds have achieved a long-term stable return profile over several decades, albeit with a few hiccups along the way, an expert reported. HFs, he said, should produce strong risk-adjusted returns, and be genuinely alternative, meaning little correlation or high beta to conventional assets. “If your hedge fund just goes up and down along with the main markets, there is little point,” he added.

He said that private equity, property, and private debt are classified as alternatives, but often behave like levered versions of their public market equivalents. “Private equity is essentially levered public equity,” he explained. “In the short run, it doesn’t move, so it behaves like a stable investment, but in the long run valuation [related to the main public markets] is what drives it. Hedge funds are back for all these reasons - strong risk-adjusted returns, performance not driven by the other [main] assets that investors own in their portfolios.”

For the private banking industry, hedge funds serve a key role today in protecting client wealth

Another expert observed that for client wealth protection the risk-adjusted returns offered by hedge funds historically augur well for an increased allocation to the broader client portfolios, bringing low correlation, and lower volatility, and thereby helping to buffer the downside, or the negative impact on the entire portfolio. “This is definitely a year for the return of hedge funds,” they said, “and we are seeing more clients now wanting them in the portfolios.”

They added that multi-strategy funds with sound managers are sensible to obtain access to a group of HFs, and that their RMs and advisors are now working hard to remind clients of the importance of diversification and finding sources of alternative returns. And that means alternative types of strategies or asset classes that they would not get from the traditional asset classes they would be investing into, hence the need for hedge funds with lower volatility and less correlation.

Another guest acknowledged that hedge funds are quite complex investment vehicles, in which you might have less liquidity, and noted that some clients still have a bitter taste of hedge funds based on what happened in the global financial crisis, even though he said HFs, in fact, did quite well relatively during the GFC years.

A guest observed how HFs are very important as part of pretty much every endowment and pension fund, or sovereign fund in the world. “With interest rates and inflation much higher now, and the risk-free [bond] rates now far higher, people need to be comfortable that the rigour about their strategic asset allocation, and the way they adopt a tactical dynamic tilt, with hedge funds and variations of hedge funds critical [for those purposes].”

He explained that they are Australia's first hedge fund, but linked with many global hedge funds, as well as a fund of funds that are more active on the shorts in this higher risk-free rate environment.

High inflation and elevated interest rates are fertile ground for hedge funds

Inflation is a major driver for the dramatic changes seen in global asset markets, a guest reported. While 2023 is already a much better year than 2022, inflation is still rife and higher interest rates look set for the foreseeable future, while major economies are weakening, hence the environment for HFs is considerably more favourable.

Historically, a guest reported, hedge funds do particularly well, especially on a relative basis, in a period with high and falling inflation, and while that is also a period when equity markets tend to deliver positive returns, it makes sense to buy into hedge funds, as they tend to deliver at least the same or actually the research shows even higher returns in these types of periods, but with lower volatility and lower correlation. “

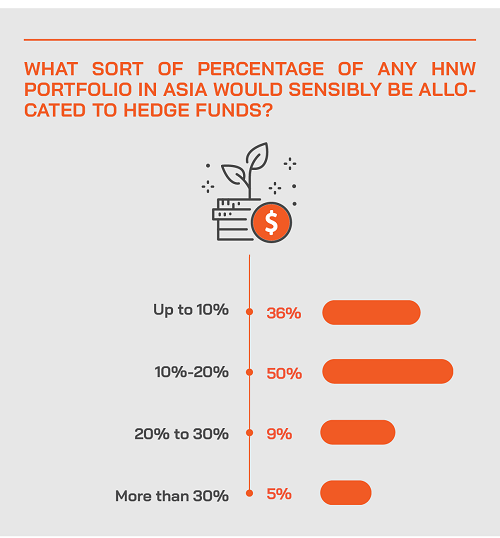

This means it makes sense from a portfolio diversification standpoint,” he added. “Accordingly, we are telling clients they should consider having 10% to 15% of their portfolio allocated to hedge funds as a broad group, including macro, long-short equity, a bit of CTA and relative value. We favour those at the moment.”

Another guest agreed, noting that low rates and downward trending rates are in the past now, and that means persistently high risk-free rates provide tailwinds for HFs. “Let's take a reasonable historical alpha expectation for a hedge fund, let’s add it to today's risk-free rate and that's the total return you should expect from a hedge fund, and then let’s compare it with the alternatives along the risk spectrum, such as equities and fixed income.” The conclusion, he said, is that actually, regardless of the inflationary outlook, higher interest rates are good for hedge funds as an asset class.”

Clients like to have the reassurance that they are taking the right steps

A guest said that it is easy for professionals like themselves to advocate HF virtues, but clients need more context and nuance. They said a client might spot a bank or corporate bond from an issuer they know that they like that could be yielding 6% or 7% and be wary of buying hedge funds instead, as there are more unknowns. And as advisors, they need to keep in regular dialogue with clients as markets and conditions change all the time. “It can be a difficult time to make these big decisions about hedge funds, and around advantages such as lower volatility, low correlation, diversification and so forth, so we need regular education and dialogue, often before we even get into CTAs or relative value or multi-strategy funds,” they reported.

There are challenges around manager selection and dud diligence to make sure the best funds are promoted to clients

A guest reiterated the view that multi-strategy funds are often the best route for private clients as normally only the very sophisticated and larger clients can go directly into certain hedge funds. “The challenge,” he said, “is then around manager selection in this space. Most private banks have hedge fund research teams, and we tend to work with independent research houses, and we use an independent hedge fund consultant for our manager selection, as we do with our macro research.

A panellist agreed, adding that it is important to have an independent review of the people overseeing the strategy, of the cost base on that strategy, and of course the performance. “Transparency and objectivity are essential,” he stated.

Another expert said that as advisors they also need to make sure they are completely on top of the managers and do due diligence around the funds, to ensure the optimal offerings for clients. Additionally, they must monitor the risk profiles of the funds, and also advise clients of the liquidity environment, as hedge funds are somewhat less liquid than a typical stock or ETF. “Clients who go into hedge funds probably don’t need daily liquidity, but they will want monthly or quarterly liquidity,” he explained.

The reality is that the jury is out on the G7 economies and the broader outlook for global metrics and amidst such uncertainty, hedge funds often shine brighter

Some members on the panel appeared to agree that although inflation and rates are much higher, the major economies are not yet tippling into recession, nor likely to do so. As one expert observed, aggregate earnings in the Western world are actually quite resilient versus expectations a year or so ago. “There is a resilience in the weekly data flow year to date, and there is resilience in aggregate corporate earnings, for example, those delivered so far in North America,” he told delegates.

But he said that everyone is preparing for more difficulty amidst the tight credit conditions, hence they see more managers globally much more active in shorts on key global corporate names, nervous about the future, including mid- and regional US banks for obvious reasons. “Managers are looking for a slowdown, but a shallow, not a deep recession in the US and Europe. The big corporates are actually well prepared for some sort of events, and more breakage along the way, more volatility along the way, but then we get out of it.”

He added that the muti-strategy funds will help protect clients through this type of cycle with an overweight to that strategy for the next two to three years.

Another somewhat less optimistic view came from a guest who said he has a feeling that the balloon has been punctured, that recession is inevitable and will come to us faster than we expect. He argued that the spending in the US has been largely pent-up from pandemic times, meaning the unused stock of money being spent, as opposed to the economy being in great shape, and not with income translating to higher consumption.

“With higher interest rates, credit breakage is coming, and generally these sorts of disruptions are good for investors that are not directionally biased but are looking for opportunities,” he explained. “When breakages occur, for example with the Credit Suisse AT1s and shifting pricing then in the higher-yielding US bank debt, these are opportunities that the hedge funds can pick up.”

He concluded that while he is not committed to a strong view on the economy either way, as they are not a directional investor, whichever way things go – and predictions are never easy – there will be plenty more of those relative value opportunities.

“I believe that well-managed multi-strategy funds are very well placed to harvest those sorts of opportunities,” he said. Market-neutral funds, he said, are run in the middle, aiming to remain neutral, and largely agnostic, return-wise, as to whether mainstream equities or bonds are up or down.