Publications & Thought Leadership

Wealth Management Leaders in Asia – Seizing the Opportunities and Overcoming the Challenges

Jul 1, 2021

If anyone knows what will happen next with the pandemic and to the world around us, or perhaps when ‘normal’ life might resume, then please raise your hand! Private bank heads and the founders and leaders of boutique independent wealth management firms in Asia have, like many around the world, been on a roller-coaster ride right from the onset of the global Covid-19 pandemic. Although 2020 turned out to be a remarkably impressive and generally very profitable year for the banks and other wealth management businesses, the pandemic-induced hiatus has given wealth management leaders both the time and the need to pause and to reflect on their strategic vision and plans for the years ahead, in terms of their organisational structures, their reach, their markets, their staffing, their expertise and training, and of course, their technologies, as the need for digitisation became turbo-charged by the necessities of remote working and remote relationship management and client acquisition. On June 17, Hubbis assembled a high-quality panel of private bank, wealth management and digital solutions leaders to offer their insights on the evolution of the industry and of their businesses since the pandemic, and most importantly, to focus on the foreseeable future and to explain how they are positioning their businesses for continuing growth and success.

The Panel:

Kees Stoute, Chief Executive Officer, North Asia, EFG Bank

Nick Xiao, Chief Executive Officer, Hywin International

Christine Ciriani, CEO - International Private Banking & Wealth Division, InvestCloud

Vincent Magnenat, Chief Executive Officer, Asia, Lombard Odier

Karen Tan, Head of Private Banking, Asia, VP Bank

The Big Picture

We all know what a good year 2020 was for the private banks and wealth management players in general, and a leading banker confirmed that 2021 continues in the same trend. He remarked that there is a heightened need amongst clients for good advice, for guidance through these periods of market volatility, and he remarked that there is no doubt that the close engagement with clients at this time is incredibly important.

He reported that the feedback that they received from our clients is that they want a mixture of digital and personal engagement. “Accordingly, that remains a key challenge for the foreseeable future, as we do not know when in the coming months or maybe years countries will reopen, and clearly some will reopen earlier, some later,” he commented.

Seeing and seizing the key market trends

As to the opportunities and trends in the Asian wealth markets, this banker observed that those are plentiful, including the rising appetite for more thematic investments, a far greater focus on sustainability, impact and ESG metrics in investments of all types, as well as extensive and ongoing investment in digitisation across the industry. He reported that these are all areas that are close to the bank’s core values and beliefs.

He also referred to a study of UHNW clients last year, which demonstrated without any doubt that sustainability is one of the major priorities for existing uber-wealthy clients and even more for the next generations of those very wealthy families.

“The drive to sustainability in investments and all our endeavours is most probably the biggest opportunity that we'll see in the foreseeable future,” he stated, adding that the same drive towards sustainability and ESG increasingly permeates all categories of wealth, especially amongst the nextgens.

Sustainability allied with a holistic approach

This same banker commented on the value of the holistic approach to the clients and to the advice proffered by the bank. “The first step is to really work to understand the clients,” he said. “We are all of us going through a period where we have had more time to reflect on the future, for entrepreneurs to think more about their family businesses, their family governance, their estate and succession planning. Bankers can help them with these considerations and then also help them define the best approach to their investments and portfolios. But it is all preceded by arriving at a very good understanding of the clients, their families, their objectives and only them offering them advice and solutions.”

Expert Opinion – Karen Tan, Head of Private Banking, Asia, VP Bank: “VP Bank will continue developing into a comprehensive wealth management service provider for intermediaries and HNWIs, looking at existing business fields, internationality, building excellent networks and with a strong focus on the topic of sustainability.”

Another banker reported that Asia is a key priority for the group, which has its HQ in Europe. They referred to the great opportunities in the HNW and UHNW segments, noting that Asia is the only region in the world where new client money is growing at a double-digit pace.

Agility and the importance of personalisation

They remarked that agility and adaptability are of paramount importance and that their offerings must be personalised and tailored, creating a bespoke proposition across investments, banking, wealth planning, asset management, estate and legacy planning and more besides. As to expansion in Asia, they reported that the bank’s growth in the region is supported by the hiring and appointment of experts that understand regional requirements and risk management, adding that new, different and even better talent is vital to the bank’s proposition going forward.

Expert Opinion – Christine Ciriani, CEO, Private Banking & Wealth Division, InvestCloud: “We have seen an incredible amount of movement of talent in recent times. There is clearly a talent war out there. And as that takes place, we are also seeing banks actually ask for the digital tools to be shown as part of their recruitment process because RMs know their value in helping them be more efficient, more collaborative with clients, and of course, ultimately more productive.”

Building the connections for the future

This same expert remarked on the great opportunity to cater to nextgen HNW and UHNW clients, especially in the face of the huge intergenerational wealth transfer to the next generations, and hence the need for education in estate, succession and legacy planning. Singapore, they reported, was a particularly good hub for capturing such clients, being such a major and rapidly growing family office centre for Asia, and indeed globally.

One key appeal for many of such clients is the expansion of the bank’s ESG-driven and sustainable investment approach. They explained how many of the younger generations, many of whom are home because their colleges overseas are not open or because they are taking time out during the pandemic, had been enthusiastically joining in the bank’s portfolio reviews of family assets along with their parents, and thereby opening more doors to the bank building better relationships across the generations of their clients.

Expert Opinion – Karen Tan, Head of Private Banking, Asia, VP Bank: “By integrating sustainability criteria into all our business processes, we aim to deliver a positive impact on society and the environment and actively contribute to the sustainable development of the finance industry. We have built our own VP Bank Sustainability Score (VPSS) system, which goes beyond standard ESG norms. We ensure that financial investments are aligned with our own corporate and ESG standards.”

Assuaging client fears and taking the conservative approach

Another banker told delegates that the current environment remains replete with both opportunities and challenges. “Investors have understandable concerns still over possible rising inflation, high equity market valuations, some credit concerns, the ongoing impact of the virus, and so forth, all of which might lead to them adjusting their portfolios and perhaps deleveraging,” he observed. “This is where we work hard to make clients feel comfortable, which of course is not always easy in the markets like this, and it will certainly be easier when we can again travel and meet them in person, which will continue to be the more effective approach for our business of private banking to the wealthy and UHNW community.”

Incredible growth in Greater China

He reported that despite the calamities of early 2020 onwards, private wealth from his viewpoint had continued to grow significantly, especially within Asia. “And despite the negativity about Hong Kong, I would cite a recent report from Boston Consulting Group, in which they predict by 2023, Hong Kong will be the biggest offshore booking centre in the world. In short, the opportunities in this part of the world remain very significant, and if the pandemic can be brought under control, the outlook is very exciting.”

Expert Opinion - Nick Xiao, Chief Executive Officer, Hywin International: “China will never be easy, but with private wealth increasing at some 15% a year, it is immensely alluring if you can get the right formula.”

A panellist noted that of the estimated 492 billion new billionaires Forbes media had tracked as having been ‘created’ in 2020, 40% of those had been created in China.

Spotting the new trends and new drivers for growth

“This indicates very clearly the simply massive wealth creation in the region, especially in China,” she observed. “If you look at the overall trends, not only do we see rapid wealth creation, but you are also seeing new entrepreneurs who are looking for different ways of investing their assets as well, with more direct investments, more direct participation. And at the same time, as all this new wealth being minted, there is a huge wealth transition taking place in the region to the next generations. And you also see this open ecosystem evolving as well, opening up possibilities for using digital in different ways to accelerate evolution across those areas.”

Expert Opinion – Christine Ciriani, CEO, Private Banking & Wealth Division, InvestCloud: “Asia is a really key market for us, and in the APAC region today we have six offices including Hong Kong, Singapore, Tokyo and Australia, and almost 500 people in the region, with 32 live implementations. With this sort of scale and reach, we have a great insight into the trends in the market, many of which have become more acute and that are developing more rapidly in recent times.”

This same expert noted that alongside this significant shift in wealth, there would also be a significant shift in clients moving their money across wealth managers, perhaps to the tune of 30% of the AUM, she indicated. This means that the banks and other firms must be especially proactive in working to retain their clients and to build their relationships with the nextgens, so many of whom are inheriting or to inherit or indeed to make more of Asia’s truly vast private wealth.

Building the USP and Expanding Revenues

Responding to the question of how to differentiate from competitors, a senior banker told delegates that the value proposition of the organisation is key. “We know we cannot be the best at everything,” he commented, “so we need to focus on what we can do best. For us in this region, we decided to go the route of our six strategic alliances, to create a strong ecosystem and to leverage each other’s strengths and advantages.”

These partnerships provide the bank with additional reach and both parties with additional expertise and access to a wider array of products and solutions, also tailored to the different regulatory environments, all of which are at different stages of development.

He also explained that it is not the product that makes the differentiation, so much as the quality of advice and the asset allocation expertise that should surround that product suite. “Deep expertise on the products and on defining the right approach to portfolio construction is a key differentiation,” he stated.

Close encounters with Asia’s UHNW elite

He referred back to his earlier remark about the UHNW client survey the bank and its partnerships had conducted with their own and their partners’ clients across the region in 2020, remarking that the process of personal interviews – most of those by video calls directly into the homes of those families and many of them lasting far longer than the allotted 30 minutes and often involving multiple generations of the clients who participated – had given unprecedented insights into the hopes and expectations of those clients and the children and grandchildren who will end up controlling what in all cases of those surveyed is genuinely enormous wealth.

“As I mentioned before, the message around their rising commitment to the planet and to sustainability was remarkable throughout the UHNW study,” he reported. “It became extremely clear that they want to work with advisors and with companies that are invested into sustainability, and they want to see their banks, insurers, their asset managers, or EAMs really walk the talk.”

Expert Opinion - Nick Xiao, Chief Executive Officer, Hywin International: “We as wealth managers should be even more curious, even more logically consistent, and spend even more time on refining our skills, and certainly exercise good judgement – we should be the stability in motion, the guardian of intellectual honesty.”

Taking the long view into the future

By way of background, after the interviews with more than 150 of Asia’s leading UHNW families and entrepreneurs, domiciled in Singapore, Hong Kong, Japan, Thailand, Philippines, Indonesia, and Taiwan, the bank had produced a White Paper detailing four key areas of note.

Those are: the accelerated rise of digital and how technology has redefined banking relationships; the delicate balance between returns versus risks and increasing need for advice; the growing conviction towards sustainability and the acknowledgement that this is certainly not merely a fad; as well as the importance of family services such as wealth and estate structuring and family legacy planning.

“The survey was very much forward-focused,” this banker reported. “We take a very long-term view of the market and of our clients.”

Patience is essential for the trusted advisor

And expanding on the theme of the right advice in terms of investments, he also explained that the wealth management providers as a rule also need to be patient, steering well clear of being associated with product pushing.

“There is wealth being accumulated all the time, and many clients are increasingly cashed up, perhaps parking chunks of this liquidity with banks such as us, and then waiting for the right opportunities to reinvest in real assets, real estate, direct private investments in companies, and so forth,” he said. “So, our advice is that we must be holistic and encompass this big picture approach so that we can help these clients achieve their objectives within the broader context of their goals and their values.”

Expert Opinion - Kees Stoute, CEO for North Asia at EFG Bank in Hong Kong: “It is vital to be highly self-critical when working out where one can truly add value as an institution. If you can only add value by reducing the price of your services, then you are diminishing yourself by commoditising your offering. If you have some major digital platform to support that, then possibly that is ok, but the boutique banks like EFG don’t have that type of platform, so we need to operate with clients that value what we offer and where we can work with them carefully through areas such as asset allocation, where we can connect to their next generations, and so forth.”

Solutions and service tailored to the clients

Another leading banker observed that all of their bank’s decisions are based on its expectations of how client needs, and their hopes and expectations, are themselves evolving, noting that their bank had identified several key developments.

“Positive impact investments and ESGs are certainly gaining traction, and we believe they will grow enormously,” she observed. “The industry has also entered an era of unprecedented transparency, which will be a vital issue - including access to investable solutions. Data analysis is another exciting development, and through it, investment recommendations will become more personalised. New asset classes are also increasingly becoming an alternative investment for our clients in the search for positive yield; indeed, this is an offering that we will develop with our new “Client Solutions” business area, as private market investments have also significantly increased over the past years.”

Keeping things personal in a WFH world

They also highlighted the very important shift of moving beyond advice to deepen relationships, explaining that clients had been growing increasingly fatigued with the number of online meetings and webinars, so the bank had been taking a different approach to keeping clients engaged and happy by layering in more of human touch. “We actually send them food and care packages, we meet them in person in Singapore when possible, and we converse on non-work-related stuff,” she reported. “Many of our clients are delighted to see us - including some clients who have remained in Singapore to enjoy the safety and convenience here in the new normal.”

Expert Opinion – Christine Ciriani, CEO, Private Banking & Wealth Division, InvestCloud: “If you lack the ability to aggregate data across wealth management services: advisory, discretionary, execution-only, third party funds, private equity investments, crypto investments, then you are not able to provide a holistic view either to the relationship manager or to the client. Without a solution that integrates easily and can aggregate data flexibly, then you become very limited in terms of how you share and how you really provide holistic advice.”

Empathy, patience and engagement

She elaborated on this, commenting that client engagement is all about empathy, with conversations being two-way. “We have always encouraged our advisors to be updated on the latest general trends, so they are able to engage in a wide range of conversation with our clients,” she said. “Not everything is about hard-selling. And when we are unable to meet our clients, we organise virtual events, including lifestyle themed ones. Relationships are established from the ground-up - where personalisation plays a critical role in today’s virtual climate.”

Very importantly, she said the bank’s Client Advisors must not limit themselves to serving up solely specific products; they must instead learn to expand the client relationship as much as possible and build the broadest portfolio with the clients and compete in as many areas as possible.

Seeing the bigger picture, keeping the clients involved

“Helping clients to diversify across a wide range of investments and capital markets to help them benefit from financial markets, offering unique proposition such as private equity, specialised real estate or investments in collectables; these are all vital missions for the Client Advisors and the bank and our clients,” she stated.

Expert Opinion - Kees Stoute, CEO for North Asia at EFG Bank in Hong Kong: “Many clients think they can do all this themselves, but in reality, they need experts who can help them reduce risk and take a more diversified and balanced approach to opportunity and risk. As professionals, we have the role of explaining our added value as institutions and as an industry, but in that, we actually fail too often. However, if we achieve that, we can be less concerned about competition, as we will be attracting and retaining the types of clients who really value what we offer.”

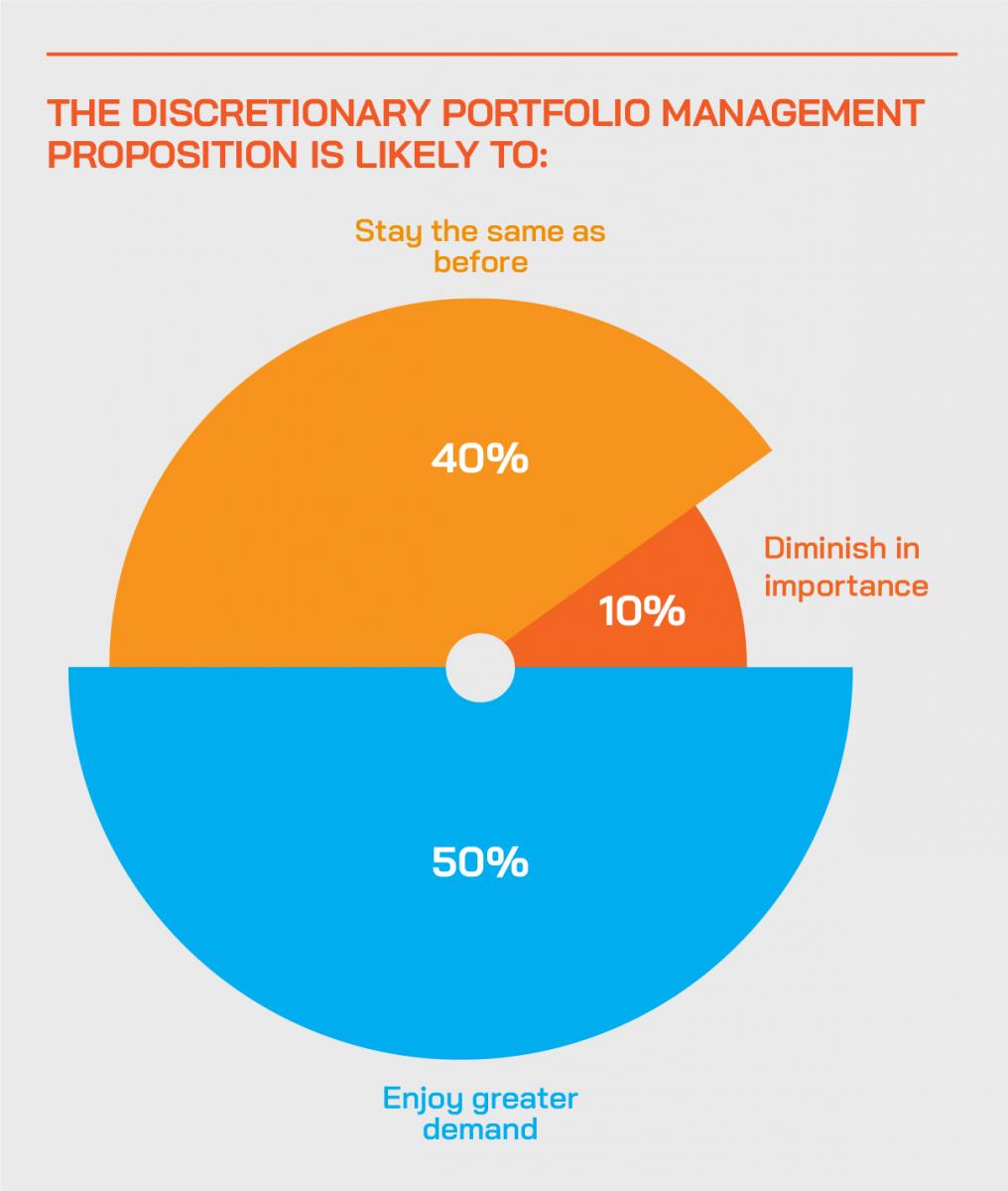

She also observed that while Discretionary Portfolio Management (DPM) is a positive step for clients, pure DPM can disengage the client from much of the investment decision-making process. “Clients want to be engaged and may prefer to be making at least some of the decisions themselves because it is their money,” she commented. “Moreover, relating to balanced portfolios, if the clients are up to speed with the markets, they will better understand what the DPM manager is trying to achieve. That is why we make sure we keep our DPM proposition as closely allied to the clients as possible and with the clients involved throughout.”

Better relationships = better business

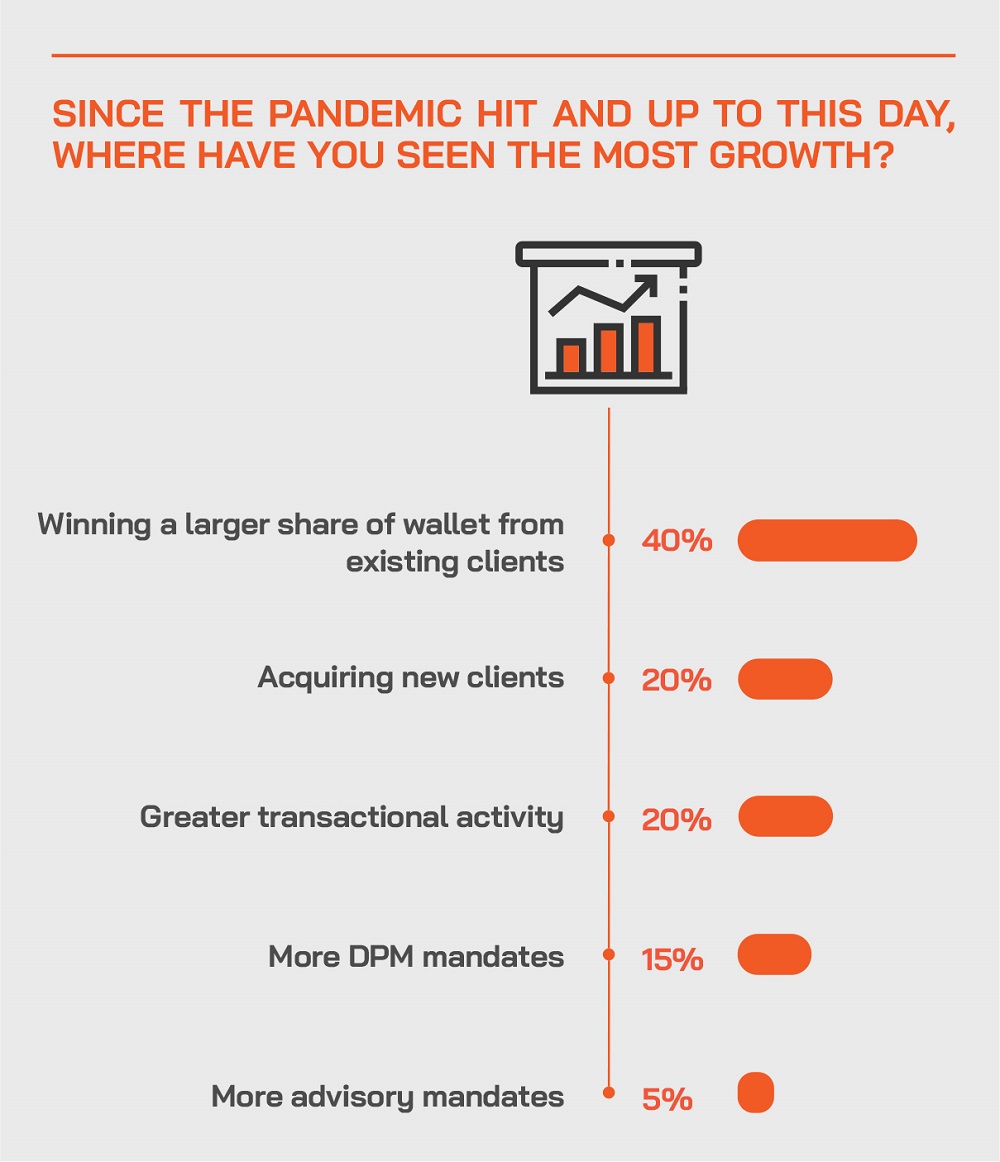

This banker also observed that the RM’s skills should be supported with the proficiency of the wealth manager’s broader array of products expertise as well as infrastructure and supplemented with specialist support. “By bringing to bear for the clients our full range of capabilities, we will then be able to retain them and build further client loyalty as well as greater share of wallet,” she said.

On this subject of client loyalty and retention and building connectivity with the next generations, they observed that Asia’s HNWIs are increasingly demanding a focus on socially responsible investing within their portfolios. “One aspect of investors assessing the culture of the bank or firm they work with is reaching an understanding of how their wealth manager and portfolio matches products and ideas with their social values,” she explained. “While HNWIs are increasingly demanding that the companies in which they invest have positive practices regarding ESG issues, they are still looking for a good return on their investment.”

Wealth management with a holistic vision

A banker commented that the value of being able to offer clients of all ages the benefit of the bank’s collective experience and expertise, offering a more holistic picture of what the market is really all about, and making sure investments are contextualised within a broader vision of their overall wealth management objectives, their wealth preservation goals, and even their legacy and succession planning.

Another leading banker gave his take on the concept of adding value and the bank’s USP. “It is vital to be highly self-critical when working out where one can truly add value as an institution,” he said. “If you can only add value by reducing the price of your services, then you are diminishing yourself by commoditising your offering. If you have some major digital platform to support that, then possibly that is ok, but the boutique banks like ours don’t have that type of platform, so we need to operate with clients that value what we offer and where we can work with them carefully through areas such as asset allocation, where we can connect to their next generations, and so forth.”

He extrapolated that this means the bank sees itself almost in a ‘missionary’ type role of communicating complex concepts and theories and highly professional advice to clients in order to elevate the proposition and the outcomes for those clients.

Expert Opinion - Nick Xiao, Chief Executive Officer, Hywin International: “As a high-growth MFO, we can pick and choose from the best available in the international markets to offer the best opportunities to our clients. It comes down to being utterly professional, giving it your best shot for clients. We are lucky actually in that the wealth management sector still has the margin for error and the chance for constant improvement, and, as our CEO said recently, we should actually embrace ambiguity and uncertainty and be prepared to be judged by our courage, robustness, resourcefulness and the logical consistency in analysing, addressing and providing solutions for clients in the context of a fluid global economy and a challenging global financial market.”

Delivering expertise where it is valued

“Many clients think they can do all this themselves, but in reality, they need experts who can help them reduce risk and take a more diversified and balanced approach to opportunity and risk,” this banker added. “As professionals, we have the role of explaining our added value as institutions and as an industry, but in that, we actually fail too often. However, if we achieve that, we can be less concerned about competition, as we will be attracting and retaining the types of clients who really value what we offer.”

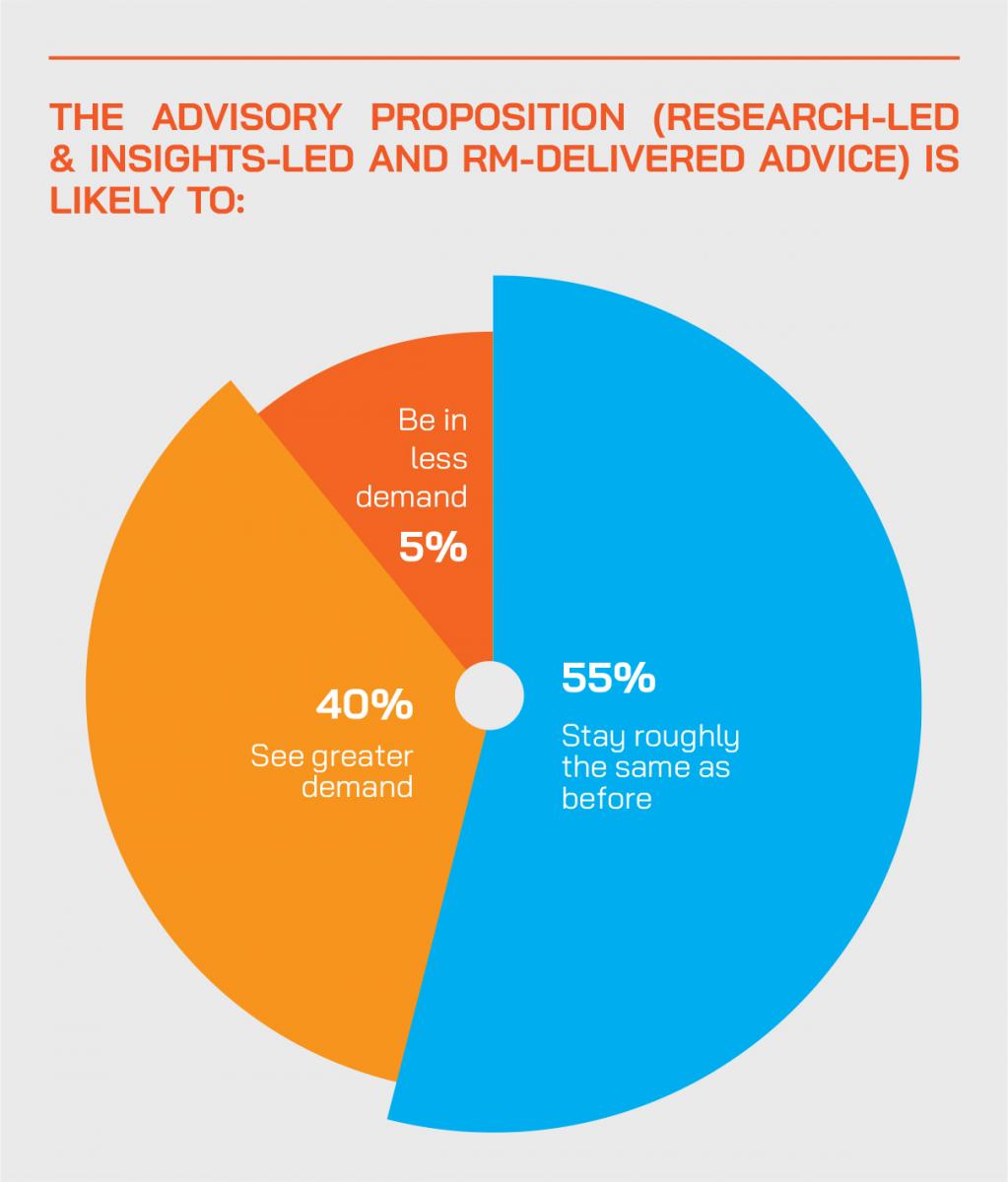

This also led him naturally to comment on the bank’s drive towards expanding its DPM mandates amongst clients. “We have been making good progress and focusing far more than in the past on communicating our DPM proposition, and that seems to be working out pretty well,” he reported.

In a changing world, stick to core values

This banker also commented that whatever the course of the pandemic, people in the industry, indeed worldwide, had become very used to remote connectivity. And talking to a screen is now embedded into our way of business and life. “Our bankers have become used to a whole new way of engaging with clients, but for our industry in the future, we also need, and actually hope for, more personal engagement with our clients to return, as I had mentioned earlier on in this discussion.”

His closing remark was that the world had really changed, and this will indeed have a lasting impact on how we all conduct business in the future, but also that there will hopefully also be some of the core elements of the wealth business that will one day return, although it will perhaps then be a more balanced approach between personal and remote connectivity.

Technology & Digitisation

This led neatly to the discussion on digitisation and new technologies, a theme that was, of course, deep within the veins of the entire body of the discussion.

As to market trends, a banker remarked on the absolute need for further digitisation across the industry. “These are threats as well as opportunities,” he remarked, “as failure to really grasp these properly could mean major road bumps for your business, even to the point of existential threats, because you need to act fast and decisively, or you will miss the boat.”

Embracing the FinTech revolution, he observed, is a must because of the remarkable array of digital solutions available, and he noted that automation could indeed eliminate many of the manual tasks and replace them with what should be 100% fool-proof processing and also checks.

“That is why you also see the regulators driving the financial industry towards FinTech solutions,” he observed. “For example, the Hong Kong regulator announced last week that they expect banks to embrace FinTech. Again, it is a great opportunity, but failing to grasp this is also a major risk.”

Expert Opinion – Christine Ciriani, CEO, Private Banking & Wealth Division, InvestCloud: “It is interesting that the client engagement devices, client portals if you wish, have actually been around for over a decade already, but now we are seeing increased demand for Client Portal version 2.0, a client portal that offers much more than just a window to their holdings. This client portal also offers clients the ability to collaborate and self-serve, increasing the service efficiency. The drive to remote collaboration is a permanent change after the last year or more that won't go away. This means clients want to be able to access information, documentation, research, personalised content through an empathic portal which is an extension of the bank’s brand and experience.”

Digital HNW and UHNW natives

Another panellist remarked that the younger generations not only value technology but that it is not a remote or distant experience for them, that they are very comfortable in the whole digital universe. While technology is central to their lives in all respects, she observed that these younger generations like to mine the information themselves.

“They like to use the tools to find their own information, conduct their own research by themselves, they want to research it, and they will often compare findings with friends,” she reported. “Nevertheless, some of them are humble enough to realise that it is often useful to listen to the parents and also their parents’ bankers and thereby see what experience and insights we have to add to them.”

Embracing digital innovation

She also offered considerable insights into how their bank intends to enhance the value proposition, products and service offering. A core area is digital innovation, which has been especially vital since the pandemic hit and had changed the way people in the industry operate and organise themselves.

“While digitisation has been ongoing for quite some years already, always been happening for private wealth management, the pandemic has further accelerated it,” she explained. “We are pleased to say we adapted quickly, and our advisors remain in close contact with their clients through multiple digital channels. It is vital to be at the forefront of digitalisation.”

Expert Opinion - Kees Stoute, CEO for North Asia at EFG Bank in Hong Kong: “Our CROs have become used to a whole new way of engaging with clients, but for our industry in the future, we also need, and actually hope for, more personal engagement with our clients to return. The world had really changed, and this will indeed have a lasting impact on how we all conduct business in the future, but also that there will hopefully also be some of the core elements of the wealth business that will one day return, although it will perhaps then be a more balanced approach between personal and remote communication.”

Upgrading IT and digital solutions

She explained the decision to embrace a new IT strategy is a key component of the implementation of their bank’s forward-looking multi-year strategy. “It sends a strong message that positions us as a driver of digitisation,” she commented. “This will reinforce the future role of IT and further professionalisation of our bank’s IT infrastructure and processes. By repositioning our IT, we are also responding to the rapid digital change that the financial industry is undergoing, relying on state-of-the-art technology in order to quickly respond to changes and seize market opportunities for our clients.”

And they highlighted key digital innovations such as cloud services and platform technology that offer many opportunities for the bank to compete in an extremely demanding and dynamic market. “In terms of client relations, we understand that private clients still prefer that personal touch and communication,” she explained. “As such, we will also continue to enhance the modes through which we stay connected with our clients, beyond the type of communication you can achieve only digitally.”

Open architecture with InvestCloud as partner

She took the opportunity to also comment on their new relationship with InvestCloud, announced only in early June this year. The bank has entered into an innovation partnership with InvestCloud with the aim of building the foundation for highly personalised wealth management services delivered via ecosystems and facilitated by a new ‘Open Wealth Service’ platform.

“Evolving client needs, digitalisation, ecosystems and progressive business models are accelerating the pace of change in the wealth management industry,” she explained. “To this end, we will significantly expand access to a wide array of innovative and customised financial solutions by taking a resolutely client-centric approach based on ecosystems and empowered by this Open Wealth Service platform. This is part of our Strategy 2026 to become an international Open Wealth Service provider for intermediaries and wealthy private clients, combining our in-house as well as third-party offerings to create bespoke financial solutions.”

Moreover, she added that these solutions would be offered to both the bank’s clients as well as HNW individuals served by financial intermediaries within the ecosystem, all delivered with open service architecture that includes all the bank’s locations. “With InvestCloud as an experienced partner at our side, we will be able to drive innovation and provide customised, bundled wealth solutions,” she reported.

Taking the best from Switzerland and Europe to Asia

Another banker said that Asia could rapidly absorb many of the proven innovations coming out of the more mature wealth markets. “We are bringing into Asia some of the successful implementations we have achieved in Switzerland, such as facilitating digitised onboarding, E-signatures, and other innovations to make the interaction between the bank and our clients much easier. Moreover, we have been boosting digital engagement with clients on a host of key topics, for example, emerging investment themes like disruptive healthcare, ESG, US infrastructure, and other interesting ideas, expanding the range of thematic ideas and delivering remotely via the bankers, and webinars and other tools, while being careful not to overload clients with information, webinars and so forth.”

A technology expert explained how the firm is well-positioned to capture the rising demand for wealth management products and services and the other emerging WM trends in the region through its five pillars of the digital private banking platform.

These pillars are: empower RMs with more efficient tools and front office operations; providing a tailored and premium service with AI insights; maximising brand entanglement with intuitive and simple design; delivering an innovative platform; and driving towards open banking.

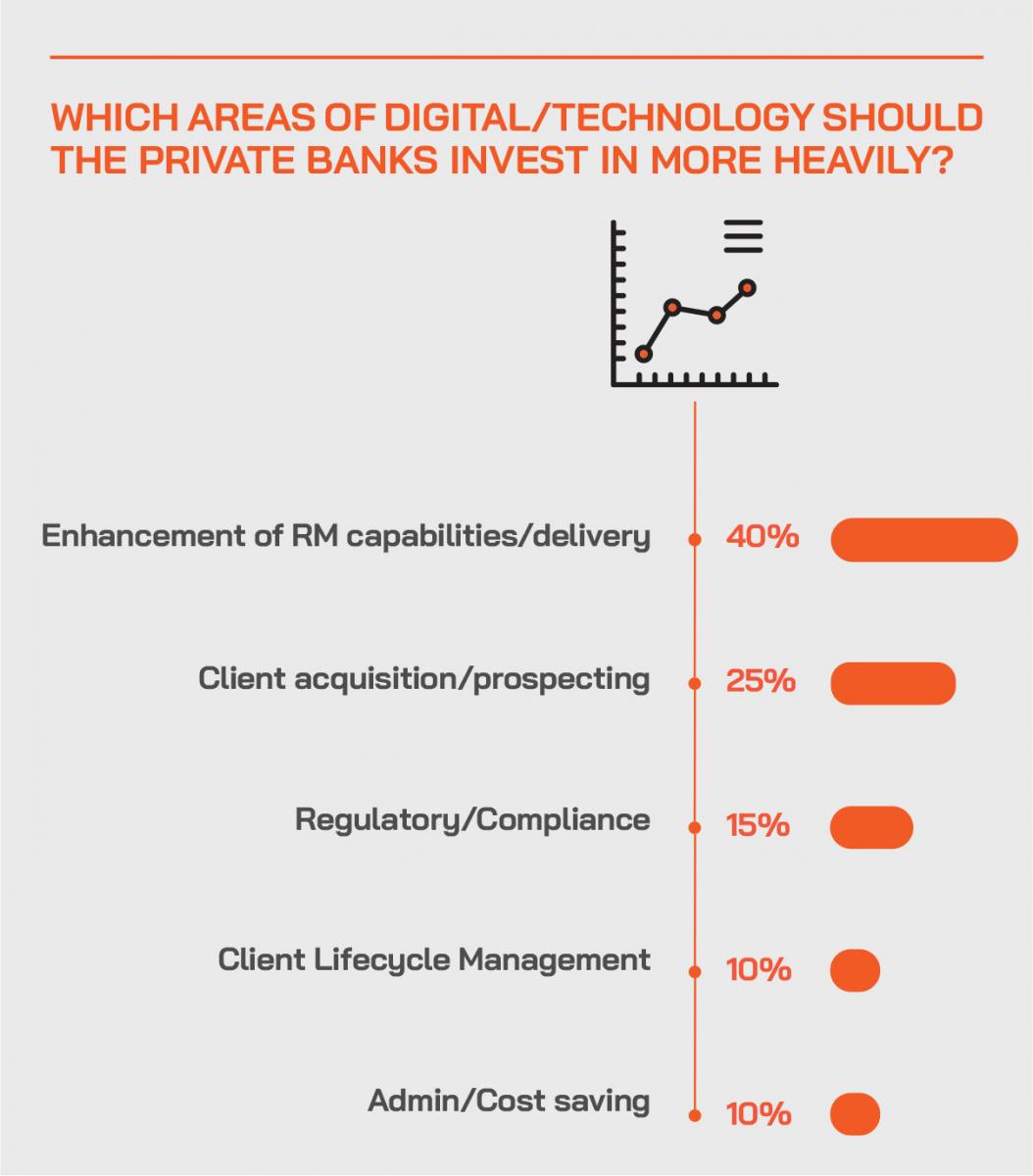

She elaborated on the first of these pillars, which centres around RM empowerment and simply making it easier for RMs to service clients. This also covers hunting for new AUM and all of the insights to support that process as well, and it includes cross-selling to existing clients, because winning new accounts since the pandemic hit has been particularly difficult.

Tailored AI-driven insights

The second pillar is using AI-driven insights to provide really valuable insights in terms of what she calls ‘nudges’ to clients, and to provide differentiation from standard recommendations, and to do all that at greater scale. “Because of fee compression, we are seeing RMs needing to actually service more clients,” she explained. “Accordingly, the ability to do that with a mainly personal, direct touch is very difficult. So, AI can be leveraged to actually help provide more insights and to deliver those to more clients more easily.”

Brand ‘entanglement’ and smart content

The third pillar, she elucidated, is around using digital channels for maximising what she calls brand ‘entanglement’. “Banks and other firms spend a lot of time and effort projecting their brand and what the brand can offer through the use of digital tools delivered in different areas of communication and collaboration,” she explained.

“And they are aiming to do that with an engagement which shows empathy to the clients,” she continued. “We know there are certain types of individuals who just want to trade on their phone or trade as much as possible. There are others who want information in terms of intelligent content, so this is about delivering that intelligent content through a digital channel to extend the brand and to build that community. We see that more and more as well, particularly in Asia.”

Innovation

She then explained that the last two pillars centre on delivering an innovative platform and open banking. “What we see, particularly in Asia, is a thrust towards transparency on fees and the value offered,” she explained. “This is for clients who want to know what they are actually gaining with the products and advice, and digital platforms are finding innovative ways to bring clients back to the bank and demonstrate that value. This may be more than just adjusting the advisory fee; it may be offering access to a community, it might be offering access to information, webinars, and to investment professionals that clients wouldn't have access to normally.”

Driving open banking

And then, there is the rollout of the open architecture and open banking concepts. She remarked that one of the leading banks represented on the panel had indeed entered a partnership announced in early June. The mission is to design a new platform for the bank to bundle its in-house as well as third-party offerings to create customised financial solutions and make those innovative products available not only to its own clients but also, for example, to wealthy individuals who have no direct relationship with this private bank and instead are served by financial intermediaries within the ecosystem.

This expert later also had the opportunity to also offer delegates a greater insight into the trend towards delivering intelligent content, which she had earlier said was in greater demand in Asia these days.

Taking the modular approach

They commented on how the ecosystem has evolved, noting that there had been a lot of innovation and technological evolution in the past five or so years. “If you look at banks historically as aiming to be a one-stop-shop, today we are talking about an open ecosystem, hyper-modularity, open API architecture, and the open ability to aggregate easily,” they observed, and warned that if banks or other providers lack that ability to be very modular and aggregate across advisory, discretionary, execution-only, third party funds, private equity investments, crypto investments as well, if you cannot offer that aggregation, and if you lack the capability to do all that in a modular manner, you become very limited in terms of how you share and how you really provide holistic advice.”

CLM and CRM

They added that another vital element for differentiation and success is the ability to serve clients across their lifecycle, explaining that it is increasingly vital to both understand the client and to understand their activity so that the RMs and advisors can obtain the information, insights and alerts that help them deliver advice, products, and solutions to those clients in a timely and relevant way.

Digital solutions, they observed, “offer the capability for holistic solutions aggregate for the RMs in line with the client view, and this is a core reason why we are seeing a lot of clients turn to us, because of this ability to actually service both hyper-modular solutions, but also to extend those across the lifecycle, leveraging CRM and CLM as well.”

Expert Opinion – Christine Ciriani, CEO, Private Banking & Wealth Division, InvestCloud: “Digital solutions offer the capability for RMs to manage a holistic view of client holdings which can also be shared with the client. This is a core reason why we are seeing a lot of clients turn to us, because of our ability to offer hyper-modular point solutions, but also to extend our solutions across the client lifecycle, leveraging CRM and CLM as well.”

Future-proofing your WM business

Another insight was that the incredibly active market in recruitment and a huge amount of movement of talent in Asia’s wealth markets is also resulting in a lot more interest in digital solutions, as the RMs are seeing this as a vital element of any bank or firm they might join, and a major deterrent if it is not available and essentially state of the art.

The discussion closed with the panel agreeing that there are numerous encouraging signs for the wealth industry in the region, and many drivers for growth, but only with the right strategies and a forward-thinking, client-centric approach will incumbents be able to capture those opportunities.