Wealth Management in Indonesia – Enormous Opportunities & Great Challenges

Sep 30, 2020

Indonesia’s huge population is growing fast, and so too is the country’s private wealth. Money has flowed back onshore following the government’s tax amnesty, and the regulators are keen to keep that onshore and boost the onshore proposition. A panel of experts ‘met’ for a virtual Digital Dialogue discussion on September 24 to give their views on the evolution of the wealth management industry and what needs to be done for it to develop more robustly. Greater regulatory creativity is needed, with the regulators working more closely with the private sector. There is a huge conservatism amongst those with money, with deposits the preferred option for more than 90% of the investible money, little surprise really given how badly the stock market was hit earlier this year and the fact that government bonds yield over 7%. But certainly, market education surrounding investment products must expand rapidly and all participants must spend both time and money to build their future clients across Indonesia’s vast span and its more than 13,000 islands. The same applies to the pensions and insurance market, where there are enormous funding and protection gaps throughout the entire population. There is a serious shortage of talent to cope with the wealth management industry’s growth, and the pandemic does not make it any easier to hire what talent does exist, but digital can help incumbent banks and other players boost their proposition across all facets of wealth management. A fascinating discussion evolved, with the six experts agreeing that the potential in a country with more than a USD1 trillion GDP and a fast-growing population making the challenges well worth tackling head-on.

Setting the Scene

A local expert opened the dialogue by remarking what a challenging year it is globally, but that Covid-19 should not obscure the wider-angle view that the local wealth market is still not yet punching its weight. “Every year we sit down and realise that for a market so promising like Indonesia, the growth in our industry is somewhat not meeting the high expectation base in our country. So, what has gone wrong?”, he pondered, rhetorically.

He answered this by referring to a study his firm had conducted that showed a 4% AUM penetration as a percentage of GDP, which is very low still compared to between 15% to 25% numbers in some of our neighbouring countries like Malaysia or Thailand. “We see the inflexion point that Indonesia needs to reach before our wealth management industry can take off is around a GDP per capita of USD5,000, while the country is roughly at USD4,100 now. The idea is very simple actually, people can only focus on their wealth and invest properly when they have already taken care of their basic needs. Of course, the Covid-19 situation is slowing things down, but we see a major acceleration of Indonesia’s wealth and asset management industry in five years or so.”

He reported that a leading indicator is the number of mutual fund investors, these figures growing four times, from around 450,000 in three years to almost 1.8 million by the end of 2019.

Expert Opinion - Antony Dirga, President Director, Trimegah Asset Management: “It is always lively to discuss about the challenges and opportunities in the Indonesian Wealth and Asset Management market, but one would notice that every year we sit down and realise that for a market so promising like Indonesia, the growth in our industry is still not meeting the high expectation being placed on Indonesia.”

“So what has gone wrong? To answer this, we need to understand where Indonesia is in the Wealth Management growth cycle. Referring to a study done by me and my team at Trimegah Asset, we found that Indonesia’s 4% AUM penetration, expressed as a % of GDP, is low compared to the 15-25% numbers that we have seen in some of our neighbours like Malaysia, Thailand and others. Based on our study of different countries’ wealth management growth cycle, the inflection point that Indonesia needs to reach before our Wealth Management industry can take off is a GDP per capita of USD5,000. The idea is very simple, people can only focus on their wealth and invest big time, when they have already taken care of their basic needs like food, clothing, housing, transportation, education, etc. We are now at USD4,100 per capita and I strongly believe that Indonesia’s wealth and asset management industry will accelerate 5-6 years from now, when we cross above USD5,000. A leading indicator to this is the number of mutual fund investor that has grown 4-fold from 444,945 to 1,774,493 by the end of 2019. This was just in the past 3 years. Sure, the AUM growth, driven by younger investor demographic, is far from matching the growth in the number of investors. However, in the next 5-6 years, as our GDP grow 5%+ and these younger investors get wealthier, we are about to enter an exciting growth phase that will finally fulfil our potential. The math just adds up.”

Another banker reported that they see the same type of growth path, and had been developing the digital wealth proposition for the HNW community of clients, and leveraging technology to expand in the mass affluent space, where he said moving to towards the mass affluent segment. “We take the hybrid approach,” he said, “combining automation and robo advisory with our personal advisors.”

Expert Opinion - Koh Keng Swee, Executive Director, Head of Investment Product and Advisory, DBS Bank: “We believe that the Indonesian wealth management industry is poised for greater growth. We now already have a robust suite of local bond and unit trusts offering. Complementing that is our increasing selection of overseas investment instruments such as offshore Shariah funds, which allow our clients to invest in the US, HK and China markets. Over the next few months, we plan to add exposure to India, as well as funds focusing on themes such as disruption and ESG.”

Expert Opinion - Abraham Ara, Head of Intermediary and Institutional Business, Eastspring Investments: “The Covid-19 Pandemic is an eye opener, it certainly educates us in different aspects. It may also provide new opportunities for Wealth Management business in Indonesia.”

Another banker explained that the pandemic had skewed investor focus more towards debt, as the government has been issuing so much paper to prop up finances for the country, while at the same time, the volatility had meant the stock market has been weak and volatile. “If you only have local products, mutual funds, unit trusts, your business probably has not been doing so well. So, we are focusing more on capturing the opportunities in fixed income, and at the same time tracking moves by the regulators towards opening up more mutual fund and unit trust activity to allow us to offer more offshore Shariah funds here. Actually, if you want to offer funds that allow the retail investors to invest overseas, in the US, in China, in Hong Kong, they have to be in Shariah format.”

Expert Opinion - Nico Fernando, Investment Product, Head, Maybank: “Inheritance planning services are only provided by few wealth managers in Indonesia, even though succession plans are critical, this service not only ensures the continuity of their existing client’s wealth, but also allows them to build a relationship with the next generation”

Expert Opinion - Abraham Ara, Head of Intermediary and Institutional Business, Eastspring Investments: “More and more clients look to their asset managers to consider Environment, Social, and Governance (ESG) issues when investing. Although ESG policy and compliance may not appear directly in companies’ financial statements, investors and asset owners will increasingly ask for evidence of their risk exposure as measured by various indicators, such as carbon footprint, overlap with ESG indices and evidence of engagement beyond proxy voting with companies on key issues.”

He explained that starting with just a few of such funds, and working with asset management providers, the bank was able to capture offshore opportunities, for example in the popular US tech sector.

Digital, meanwhile, he reported, was an essential initiative, and the bank had been expanding in this area, focusing on client-facing systems and access but also its digital platform to expand the produce range and accessibility for bonds, structured products, stocks, and funds/trusts.

“Digital is also for us about revamping the internal processes to help our teams, to keep them happy, and in that way seamless capabilities result in clients enjoying a great experience engaging with the RM,” he said. “It actually takes a lot of work and cost to come up with a straight-through system, and that's what we're doing actively over the last 12 months.”

Despite the turmoil in the markets, he reported that the bank had enjoyed a very good year to date, and expects a 25% uplift in the fully year, on top of 40% growth in 2019.

Another guest focused on the digital solutions, highlighting the interesting initiatives in the country on the banking side of financial services companies to develop their digital channels, their proposition, introduce robo-advisory, and make processes on employee side more efficient. ”We see a really bright future here,” he said.

Expert Opinion - Koh Keng Swee, Executive Director, Head of Investment Product and Advisory, DBS Bank: “Digitising wealth products and providing robust financial planning is DBS’s way of democratising wealth management, and taking it to a wider segment of Indonesian society. This aligns with the Indonesian Financial Services Authority (OJK)’s direction to accelerate the digitalisation of the financial sector. Also, to us in DBS, internal digitisation is as important as external digitisation. Our staff’s user experience is critical, as it directly impacts clients’ experience. Hence when designing all processes, we aim for a seamless experience for our RMs and ICs, whether it be for price discovery, trade placement or settlement.”

Expert Opinion - Nico Fernando, Investment Product, Head, Maybank: “The role of the wealth manager is and will remain important, despite the digital demands of High Net Worth Individuals, with digital platforms playing a complementary role in the client-wealth manager relationship.”

Expert Opinion - Abraham Ara, Head of Intermediary and Institutional Business, Eastspring Investments: “Digital channels will play important role in Wealth Management distribution in Indonesia. It provides new opportunities for clients with poor access to new ways of getting their financial planning done.”

Expert Opinion - Grzegorz Prosowicz, Consulting Director, Comarch: “Wealth management of tomorrow should orchestrate human relationship, self-service and power of data. That will free up the advisors for better engagement with customers, enable digital interaction and help leverage on data to increase conversion efficiency and enhance personalised experience.”

He explained that he sees the industry needing to focus on three main areas – enhancing the RM time efficiency throughout their role, including compliance headaches, leveraging data, and boosting the customer experience. “Additionally,” he said, “the banks must push hard with education of the client base.”

Another guest agreed with that last comment, observing that their research had focused on financial literacy, which he said must rise significantly. “And thankfully,” he reported, “we were well ahead on digital and robo before the pandemic struck, so 97% of our customers now use robo-RMs.”

A fellow panellist concurred that there was a robust move diving digital adoption, with providers such as insurance companies having greater acceptance amongst clients of conversations using digital technology. “I do think that although it is a challenging year, it is going to unleash some of the opportunities we have all been seeing in Indonesia.”

Audience Perspectives

Hubbis sent out a survey to delegates immediately after the discussion and we gleaned the following valuable insights.

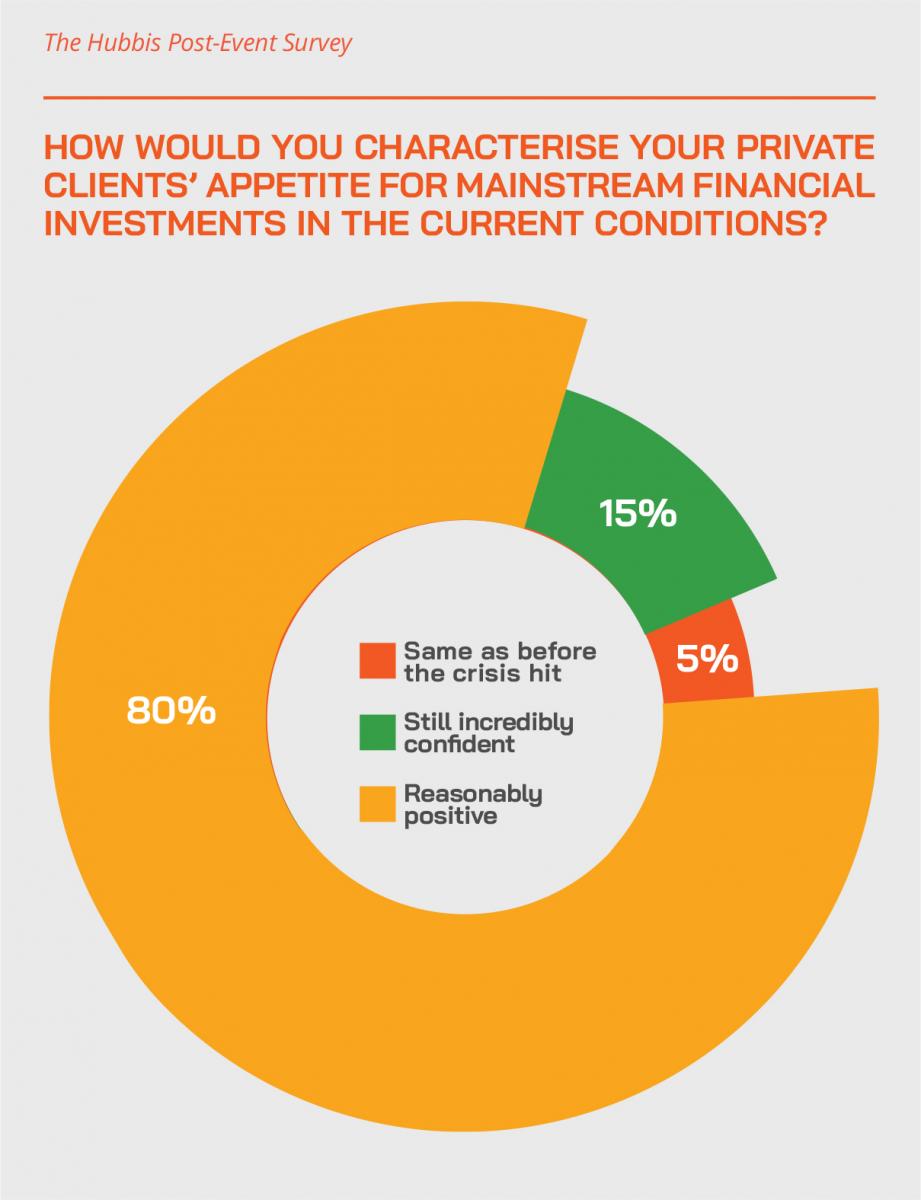

How would you characterise your private clients’ appetite for mainstream financial investments in the current conditions?

Still incredibly confident 0%

Reasonably positive 61%

Same as before the crisis 11%

Now rather cautious 28%

Steering away from new investments for this time 0%

Looking ahead, what percentage of your private clients’ investment portfolios will be in the following asset classes?

Mainstream fixed income 45%

Mainstream equities 30%

Private/Alternative debt and equity assets 14%

Gold/Precious metals 11%

Looking ahead over the next few years, what percentage of your private clients’ investment portfolios will be invested in offshore/international financial assets?

0%-20% 7%

20%-30% 14%

30%-50% 20%

More than 50% 31%

More than 75% 28%

How interested do you think Indonesian private clients are today in DPM and advisory mandates?

Rising interest 83%

No change 10%

Not very keen 7%

No interest whatsoever 0%

Are HNW and UHNW clients in Indonesia more likely to work with international, regional (e.g. Singaporean or Malaysian) local private banks/wealth managers or some of the new partnerships/JVs between international private banks and local institutions?

International PBs 48%

Local PBs/banks/WMs 28%

Regional PBs/banks/WMs 21%

Partnership/JVs PBs 3%

In general terms, how sophisticated and organised are Indonesian HNW and UHNW clients in their wealth and succession planning?

Incredibly advanced 6%

Improving/becoming more focused 73%

No visible change 9%

Still lacklustre interest 9%

No interest whatsoever 3%

How would you characterise the digital proposition offered by the local wealth industry for local private clients?

Incredibly sophisticated already 3%

Improving steadily 78%

No real change 13%

Not much progress at all 6%

A guest shifted the discussion further to products, noting that there is a significant rise in interest for sustainable investing, especially ESG-based. “We try to emphasise how we are not simply aiming for certain returns for our clients, we are aiming for a better future for all. That's what we're going to look forward to more in the rest of 2020 and 2021.”

Talking of segments, a banker argued that a multi-segment approach fits the bank’s Indonesian strategy very well, because Indonesia is such a huge country with varying levels of wealth.

“We also see that with the deregulation that we're seeing currently and also with the tax amnesty program that was launched some years ago, we see many of our customers bringing money back from overseas, and coupled with deregulations, so there are more options, more product choices for the clients,” he reported. “And as to engagement, for clients in the higher wealth segment, it would be more human, more RM led, whereas in the retail segment, it will be more digital led. This approach actually allows us to capture all opportunities, because when you put investments into building systems and products, it only makes good business sense for you to spread it out across a wider segment of clients.”

A fellow panellist said that in designing digital solutions, his firm focuses particularly on relevance to the clients, with the delivery and content of advice tailored to lower wealth segments or the upper end clientele, with lower categories needing more basic financial education and products, and the upper end more sophisticated products, a greater international focus and more input on market trends and outlooks.

Expert Opinion - Nico Fernando, Investment Product, Head, Maybank: “Indonesia's wealth management is expected to grow, even though Indonesia's wealthy market remains small. Less than one percent of adult population accounted for the wealthy population. The segment, however, held more than 95 percent of the total onshore liquid assets of Indonesia, with mass affluent alone owning more than half.”

Expert Opinion - Koh Keng Swee, Executive Director, Head of Investment Product and Advisory, DBS Bank: “With the integration of ANZ’s wealth business into DBS Indonesia in 2018, we have seen significant growth in our investment business. We have doubled our business revenue in just 2 years and continue to see immense opportunity in the fixed income as well as mutual fund space. Such opportunities will be availed to our clients in both the offline as well as online modes.”

On the question of whether DPM and advisory are winning through for clients, a banker reported that the behaviour of Indonesian clients is really no different from clients in the rest of Asia, in other words still very much transaction driven, trading oriented, and yield oriented of course, the latter specially as the government bonds could be as high as 7.5-8%.

“But having said that, actually, in Indonesia, we've been seeing increasing interest in a product called KPD, or PDNI, that allows the fund houses to manage your portfolio into overseas unit trusts, into stocks, into bonds,” he reported. “The majority of the funds that we see go into overseas mutual trusts, because like I mentioned earlier, if you want to sell an offshore unit trust, it has to be in Shariah format, which means that the universe of stocks that you can buy into is more limited compared to pure offshore unit trust. The minimum investment amount however is quite high, around USD500,000, so very clearly pitched to HNW customers.”

The panel then agreed that there needs to be a significant increase in the range of offshore products and life insurance solutions available. “There has to be a great emphasis on financial planning,” he observed, “so we beefed up our financial needs analysis, and the regulator is now allowing this conversation to happen online or over a call, over a video call, so we record it, and we feel more confident that the quality of the conversation can be reviewed, the quality of the conversation is pretty structured. And our people are able to get where we want them to get much faster, because technology tools are providing that bridge to have that consistent quality advice.”

An expert also commented that as Indonesia is a majority Muslim country, Shariah products and solutions must be honed to the market, both for investments and for insurance.

“We are a country of 17,000 islands, we have a 270 million population, so segmentation is crucial,” said another insurance expert. “At the lower wealth segment, we go direct, and in the middle [mass affluent] segment we have around 10,000 agents approaching clients, and we are focusing heavily on educating the agents and the customers, then we are also able to engage digitally and bring them onboard as clients remotely. Then we focus on customer engagement, for example bringing them on as health and wellness customers, with virtual meetings and virtual presentations and so forth, tailored to fit the clients’ timetables, including even the weekends. I see this as a growth opportunity for digital and education directed only towards the agent, but also towards the customers.”

“Yes,” said another expert, “wealth management is turning hybrid, and it is important to have this experience on both on the RM side and also customer side.”

The final word went to a banker who said that expanding awareness of wealth management and investments was the key to unlocking the country’s potential. “I'm not talking about it from just a money-making perspective,” he said, “as this is all about linking investments and solutions back to the goals in life, whether you're planning for retirement, whether you're planning for education or whatever. Financial institutions can play a major role here.”

Discussion Perspectives

Based on the discussion, and on the feedback from delegates after the event, we have summarised some interesting insights, as follows:

- Indonesia follows broader ASEAN trends.

- Asia-wide there is a rush to boost the onshore wealth management proposition. And this is being done across all segments, from retail to mass affluent to HNWIs and the ultra-wealthy.

- Education and communication are vital

- The wealth management industry and regulators must do more to boost client education, and to do so, communication is essential. It must be a two-way, collaborative process for private banking in particular.

- Elevating the offerings.

- Looking at the reality of fee compression globally, to combat the commoditisation of fees, a greater emphasis on expert advice and high-end portfolio management will help boost fees. High levels of service, and a better client interface and regular dialogues all help.

- Be client-centric rather than product or producer centric.

- There is a major trend towards boosting the product offerings, but banks and other wealth management firms must remember to be client-centric and to boost the expertise and quality of the relationship managers.

- Understand the client as deeply as possible.

- It is vital to promote higher education amongst the clients, but the industry must also focus on obtaining a deeper sense of the client needs and then tailoring the financial product to help them achieve their goals.

- Being proactive.

- Wealth advisors need to understand their clients as well as possible, in order to offer proper advice on protection of the client wealth, not just from relationship problems, but also in the event of lawsuits relating to their businesses, or other factors. Plan early, and plan well was the advice from one expert.

- Leverage your capabilities.

- Wealth management firms should work closely with external experts, such as trust experts, lawyers or accountants, to boost their and the client’s proposition.

- Repatriation of money must not be reversed.

- The government’s tax amnesty has resulted in an enormous repatriation of wealth, but the mission for the onshore wealth industry now is to keep that money at home, especially in light of the country’s growing infrastructure spending and current account deficit.

- Diversity of products must improve.

- To achieve this, the industry needs more products to attract money into financial investments, although high government bond rates and equity market weakness are hindrances currently.

- Regulators must encourage the industry.

- Growth at home should be faster in terms of the product suite and expertise on offer. However, the regulator could be more proactive, especially improving segmentation between offerings for HNWIs and the mass market to permit the speedier release of new financial solutions to the top echelons of wealth and then down over time to the mass affluent and then retail markets.

- Some commendable progress, for example insurance.

- There are clear pockets of progress, for example, insurance companies in Indonesia are at least now able to invest offshore as to 20% of their assets, they can also launch unit-linked products that invest 100% offshore and distribute that to retail clients as long as it doesn’t breach that 20% cap. Within the mutual fund industry, Sharia funds are able to invest 100% in offshore assets, although that liberalisation has not yet flowed to the conventional fund segment.

- And progress is happening.

- There is a growing number of SID numbers, representing the single investor IDs required in order to permit an individual to buy and trade financial instruments, such as stocks, bonds, or buying mutual funds. The SID data is, therefore, a leading indicator of coming growth.

- When USD5,000 GDP per capita arrives, the wealth industry will take off.

- A banker at the discussion highlighting how once USD5,000 is reach per capita, likely by 2022 all being well, the wealth industry will accelerate.

- Corporate bonds – liberalisation gradually taking place.

- A guest pointed to the regulator’s move earlier this year on corporate bonds, allowing banks to distribute them, while previously it was only the securities firms.

- Look across the region, and learn.

- Indonesia can work more closely with ASEAN counterparts to learn more of the development of a robust wealth management market, especially with eyes on the generations who will be holding the wealth in the next five to 30 years.

- Addressing the generational disconnect.

- There is all too often a major ‘disconnect’ between the founder or parent generations and the second and third generations. Wealth management experts must be aware of these gaps and address them as openly as possible.

- Structures for preservation first.

- Wealthy clients too often look at structures for tax mitigation, rather than wealth protection and preservation. Paying a fair amount of tax will not erase wealth, but not having the right structures in place and the right family organisation and governance and constitutions will potentially wipe out family wealth.

- Multi-generational buy-in required.

- People are living longer, and it is essential to organise succession planning for the family assets and businesses well in advance of the 11th hour. Effective estate planning requires buy-in from all the key family members across the generations.

- The differences are significant.

- The second and third generations might be tending to be less ostentatious about their wealth. Private bankers need to understand what drive these generations and therefore adapt their products, services and approaches to suit those.

- Governance protocols and family constitutions strongly advised.

- Without an appropriate family structure and governance, there is less likelihood of preserving wealth from generation to generation.

- Insurance offers part of the solution.

- Insurance structures can often be well employed as part of smart succession planning, but they are instruments, not the solution in itself. Liquidity in the event of someone’s death is vital, but this should be part of a sensibly organised and executed plan.

- Insurance offers huge growth potential.

- While some markets in the region, Thailand for example, are seeing a slower take-up of life insurance and associated solutions, Indonesia’s growth path is assured for the foreseeable future, so life and other insurers are keenly encouraging the regulators to open up the market, while at the same time boosting their product and distribution capabilities.

- Digital enhancement of the agency forces.

- Digital technologies are being employed to help insurers boost their distribution capabilities, as well as the skills of their agents and the clients' experiences.

- Self-regulation vital.

- The insurance and general wealth management markets should also self-regulate more effectively, rather than simply relying on new rules and guidance from the authorities. Better offerings, better transparency result in more customers and greater satisfaction, then, in turn, more business.

- The drive for personalisation.

- The wealth management customer wants everything to be much faster, and they want more personalised and seamless communication.

- Regulatory requirements.

- The proliferation of regulations means a vast amount of internal and external rules for banks and other providers, so smart RegTech solutions are the only way, realistically, to manage the scale and complexity of these issues.

- The art of being ‘Appy.

- In countries such as Indonesia with its huge and growing population, low wealth management penetration and rapidly rising private wealth, at least until the pandemic hit, the smart use of apps for all generations, especially the younger ones, will put incumbent banks and financial institutions in the optimal position to leverage their business models.

- Enhance what you offer.

- Banks are thinking not about digital disruption, but digital enhancement of the wealth management firm’s relationship with the customers, staying true to their business models, dramatically improving the client experience.

- Seeking scale through transparency.

- Banks in Indonesia have the scale, so the use of technology to help achieve a better customer experience and facilitate greater transparency should be keenly pursued.

Conclusion

This was a fascinating and lively discussion that in just one hour of focused discussion captured the key trends, challenges and opportunities ahead in Indonesia. It is fair to say the industry is still not yet punching its weight, but the belief is that once momentum gathers, it will snowball. And that is precisely why so many of the key wealth management industry incumbents locally, regionally and internationally are prepared to focus so much time, energy and money on this market.