The Vital Future of the Relationship Manager in Asian Wealth Management

Jul 15, 2020

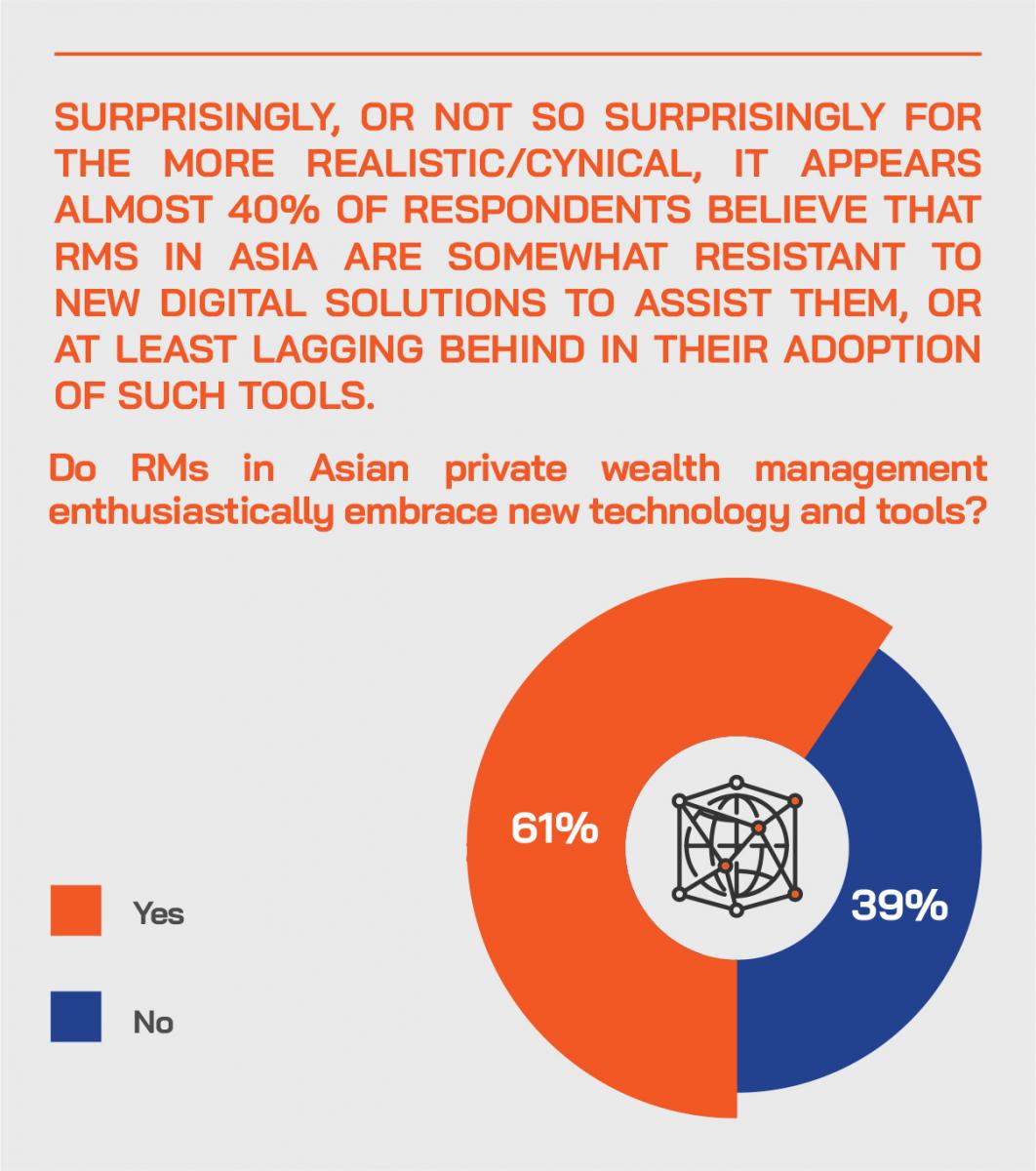

On July 9, Hubbis, in collaboration with sponsor Wealth Dynamix, held its latest Digital Dialogue, focusing on the role of the relationship manager (RM) and empowering them with new processes, protocols and technologies. The premise for this discussion was that, in more normalised times, the RM would continue to be central to the delivery of the enhanced capabilities and solutions in the Asian wealth management industry, particularly for the robust HNW and UHNW segments. While Asia’s economic growth and private wealth creation have been truly remarkable for the past two to three decades, the wealth management market has in some respects lagged behind its counterparts, for example, the far more mature markets of Europe. Boosting the capabilities of the RM is a crucial element in upgrading capabilities and productivity for the private banks and the independent wealth management sector, as they fight increasingly tough and smart to retain and boost their share of the buoyant HNW and UHNW markets.

There are many ways in which the RM can be re-invented in the decade ahead, and many steps are already being undertaken to achieve precisely that. The lively discussion analysed why the RM’s day has thus far been excessively hampered by needing to constantly perform non-productive administrative and compliance tasks. The panellists looked at what tools and technologies the RM can be provided with to make them more efficient, more productive, and most importantly more client-centric, they discussed what the RM’s workstation should look like and what it should comprise, and how the top management of the banks and WM firms must adapt to the mission to empower the RM. Moreover, the panellists analysed how the RMs themselves must evolve in order to improve outcomes for their clients and to enhance their share of client wallet, as well as their professional satisfaction and career longevity. The discussion painted a clear and comprehensive picture of how, in the decade ahead, the RM can be enhanced and empowered to the betterment of themselves, their clients, and of the banks and firms they represent.

Overview from Wealth Dynamix: Empowering the RM

Dominic Gamble, Head of Asia at Wealth Dynamix in Singapore, opened the panel discussion with his own on-the-record introduction and overview.

“To open this discussion, for which we at Wealth Dynamix are proud to be the exclusive sponsor, I would like to quickly give you my overview of the key topics and considerations. To put these in context, I want first to refer to a research report we recently published with Hubbis, titled ‘Empowering the RM – Their Role in the Future of Wealth Management’, in which following our extensive surveys of senior wealth management professionals across Asia we gathered some tremendous insights on the challenges the RM face and the future of their role in the decade ahead.

Hopefully, when you have time at home during the Covid-19 hiatus, you will be able to read through the fascinating insights that we had gleaned from what I think is probably the largest survey on RMs in Asia that certainly I am aware of; in fact, we had about 175 very senior wealth managers contribute to this comprehensive report, which you can download from the Hubbis website.

Why did we conduct this research and work on this report with Hubbis? Well, I think we are all pretty used to some of the rather negative headlines in the media everyday about how our industry is in crisis and widespread disruption, and perhaps some of the interesting headlines around the degree of digital transformation that is happening in the industry, not just in Asia but globally. Accordingly, we were particularly interested in how that is impacting Wealth Dynamix or not the RM, and I personally have a vested interest in exploring this topic because I was actually a private banker for about 10 years of my career, starting off in the early 2000s.

I have reflected back on those years, and now look at the role of today and of the future. The art and science of being an RM hasn’t actually changed much, but their day job itoday, as you all know so well, is driven now by so much regulatory compliance tasks, taking the attention of the RM away from their clients.

I will highlight a few pointers from the report. Most of the respondents believe that the Asian market for wealth accumulation is going to outperform other regions of the world in the decade ahead, and 87% think that the wealth management business in Asia is going to grow over the coming decade, as well. However, interestingly only a third of those who responded believe that the industry is actually on the right path to seize these opportunities, with most of them thinking that there is considerable room for improvement.

And we saw some salient points arising around the RM’s role. The good news and I think we are all in agreement on this, it is a much discussed topic, the RM will continue to be very central in the wealth management industry especially in the UHNW segment, with 62% believing the RM is an overwhelmingly important element, and similarly in the HNW segment, where those we surveyed firmly believe that the RM will be crucial, although in this segment perhaps also helped significantly by more digital tools and delivery.

Respondents also made a very interesting point around client centricity, commenting that this factor is the single element that will drive WM institutions to win and keep the most competitive positions in the industry.

Moreover, a quite unique insight that came out was that 84% of respondents said RMs are currently reactive to situations, with only 10% reporting that they are actually proactively servicing clients day in, day out; that really is a fascinating and quite damning statistic.

To develop that a bit more, client relationships and client service are overwhelmingly the areas where respondents thought RMs must concentrate their efforts. In terms of the digital delivery elements, more efficient administration, even compliance solutions, these really didn’t rank at all compared to the need to understand the client and their families far better than they have to date.

The research found that 73%, a huge majority, said that client lifecycle technology solutions will allow these institutions to deliver a more personalised service, and from my viewpoint, this personalised approach is really the future of wealth management. As we enter an era of more and more competition, including new competitors coming from left field, it is the ability of these wealth management institutions in the future to deliver a personalised service, beyond the homogenisation that we have seen so much of over the last 5 to 10 years, that is going to really ensure that institutions remain competitive and thrive well into the future.

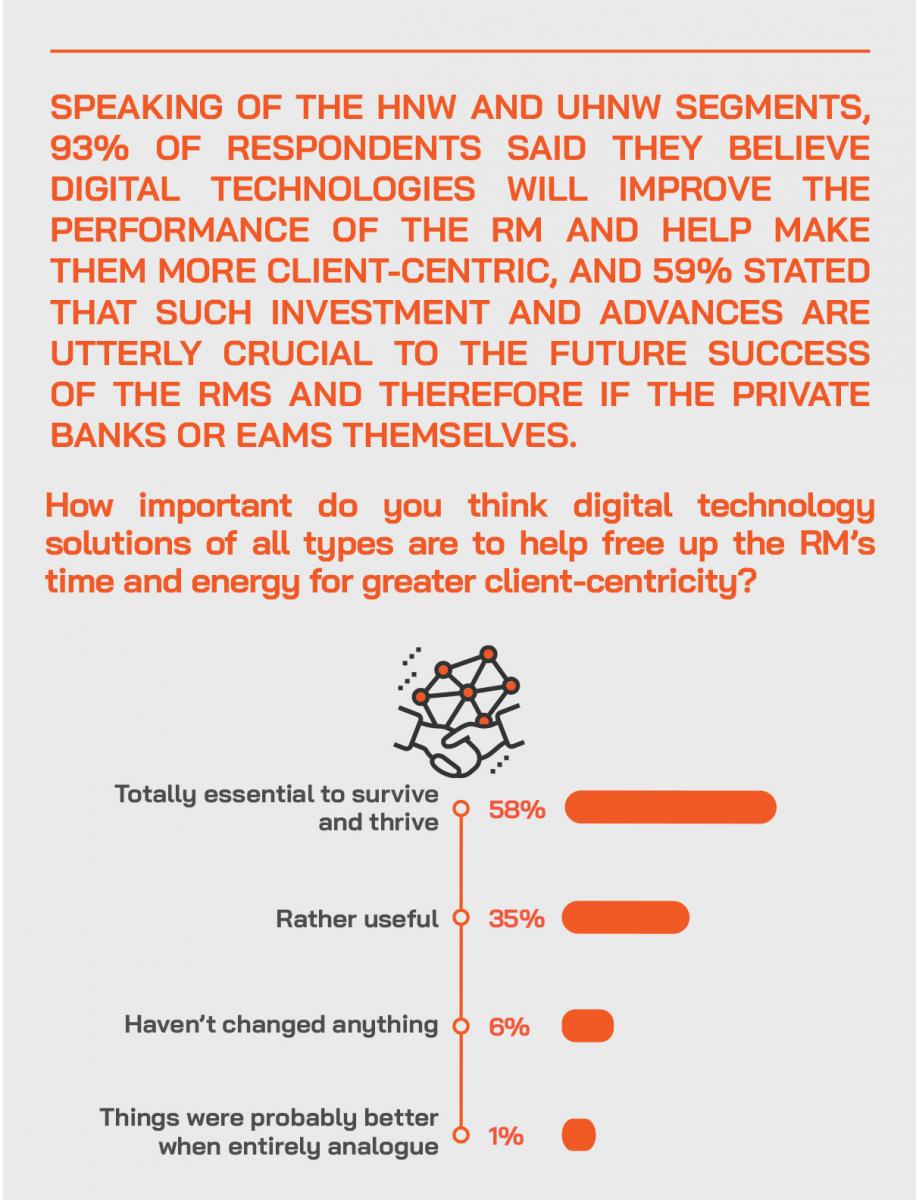

We also found that a resounding 96% believe that technology is the tool that is so essential to free up an RM’s time and energy for greater client centricity.

So, when I put this all together, I reflect at just how forgotten RMs have been in the race to digital transformation thus far.

There has been so much investment in the areas such as AML, KYC, regulatory and compliance technology, core banking systems of course, portfolio management systems, perhaps front-end client tools as well, while the RM is left stranded with a very antiquated toolbox. But with the right tool, they can be helped greatly in prospecting and building their pipeline, nurturing clients to the onboarding stage, helped greatly in that onboarding, which is today largely fraught with inefficiencies and paper flying backwards and forwards internally and to clients. And as a result, the RMs can focus their attention on their advisory and true wealth management components which are really the core drivers of a RM’s dedication to client centricity.

And we should remember that it is not all about helping an RM to provide quality advice or sales. It is very much about helping the RM to be efficient in the more painful areas of relationship management; those might be service requests, executing changes of address, transfer requests, and so forth.

It is essential I believe, and some of you will have heard me say this before in my talks, that private bankers tend in the current era to have far too many systems purportedly supporting the client lifecycle management protocol. In fact, I am regularly told by RMs at a large private bank in Singapore that they have as many as 18 different systems to help them with their day jobs. That is simply not a tenable situation and it will impede the RMs role, let alone the institutions goal in fostering a profitable business.

What we need, therefore, is high-quality service touchpoints throughout the entire RM journey. In fact, the research we conducted with Hubbis for the report highlighted that a huge proportion of the respondents - 86% actually – determined that the right technology solutions will drive more revenue, with many benefits accruing, including enhanced AUM, greater client retention, improved ability to attract and retain RMs, greater job satisfaction, and of course better client outcomes. I could go on at considerable length on this fascinating subject, but I will now hand back to the panel to discuss these matters at detail and from their viewpoints, bring their great experience to bear.”

The Development of the RM in Asia: A Work in Progress

With that, the floor was opened to the other experts to debate the evolution of the RM to date and how they might evolve in the decade ahead.

“To me,” a fellow panellist began, “the key to me is the relationship, even more so perhaps at this time. They must keep close to their clients and be more proactive, as Dominic commented, rather than being reactive. What we are seeing in the marketplace is that it is playing into the hands of some of the smaller players, some of the EAMs and family offices out there who are a bit more agile that have really built sustainable client relationships.”

Expert Viewpoint – Karen Tan, Head of Private Banking, Asia, VP Bank: “Relationship Managers will remain valuable players in wealth management in Asia. The goal of relationship managers is to work closely with clients as their trusted client advisors, managing risk exposures by matching investments based on clients’ needs and objectives. As a reliable sparring partner, who understands their clients to help them achieve their life goals in the long term, beyond simply focusing on achieving revenues for themselves or firm.”

Another expert concurred, noting that RMs tell him regularly that they are impeded from a lot of their capabilities due to the persistent need to manage compliance issues and to handle operational matters. “But there is no doubt there are technology solutions that can significantly improve this situation,” he commented. “And the pandemic has forced the speed of digital connectivity and solutions, with banks shifting urgently to new tools to solve the immediate and future challenges. Technology can allow the RMs to keep close to their clients through this pandemic, and that is certainly an essential element for them at this time.”

The panel agreed that RMs spend too much time on administrative tasks, not enough time on learning, too much time hunting for information, too little time mining data on their clients and thinking holistically about the products and solutions that will result in optimised outcomes for those clients. “They need tools that will help turn them into trusted advisers who win an ever-larger share of client wallet,” said one guest.

The panel also concurred that there had been a huge and growing investment in technology, including regulatory software, to help the middle- and back-offices at the banks and other wealth management firms become more automated and efficient in recent years. “But meanwhile,” said an expert, “the RM has been left with an array of legacy systems and processes. The RMs need to be in the driving seat, with smarter, data-driven insights into client behaviour and sentiment, and technology that boosts productivity. Only then will they be able to deliver faster, more efficient and responsive client servicing.”

Indeed, in the Hubbis/Wealth Dynamix report that Gamble had earlier referred to in his introduction, the majority of respondents said they believe the RM will remain central to the upper echelons of the wealth market, but 84% said RMs remain reactive, and just 10% said they are sufficiently proactive.

And in that same report, it was clear from the many replies received than that RMs clearly need new technologies and a fresh management outlook to help them up their game. To achieve this, 86% of replies in that survey had indicated a more process-driven/disciplined/structured Client Lifecycle Management (CLM) system would boost revenues, while 85% had said this would increase talent acquisition and retention, 89% said this would help increase new clients, and 87% said client retention would be improved. And some two-thirds roughly had said costs would be reduced as well.

Expert Viewpoint – Dominic Gamble, Head of APAC, Wealth Dynamix: “The RM has not been tooled sufficiently over the last few years - RMs are a critical lever to driving AUM and revenue growth, but they have been passed over by the digital transformation in many cases. That’s about to change, and Covid-19 has accelerated that thinking. Firms must move fast to understand the technology wins that RMs would cheer, drive a culture of technology adoption inside of the business and clearly highlight the positive role that technology can play alongside RMs in order to meet business goals. Without that evolution, the role of the RM and mere survival of the institution will be at risk over the next decade.”

Post-Event Perspectives from the audience on whether the RM will remain core to the UHNW and HNW wealth segments in the decade ahead.

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on whether the RM will remain a central to the wealth management proposition for the UHNW and HNW clients in the decade ahead. We have edited their replies to provide the following insights from the wealth management community.

In your view, in the HNW and UHNW segments, do you think the RMs will remain central to those relationships in the decade ahead. Why? Or why not?

- Certainly. The RMs will continue to be a direct means of reaching someone at the bank to assist in handling their accounts; it seems unreasonable to ask HNW and UHNW clients to call the general hotline every time.

- Definitely, and it will be slanted towards the UHNWIs, because that’s where most of the revenue is for the bank.

- They will remain central if they are keep abreast with the market, continue to build relationships with clients and the next generations of clients, and be client-centric and not solely revenue or transaction-focused.

- Yes. Whether HNW or UHNW, they are people and when it comes to investing, people matter more than technology. Relationships will still drive the business.

- In the UHNW segment in particular, yes, as it will still be easier for an UHNW individual to work with an RM to manage and plan their vast wealth.

- Yes, but maybe more for the UHNW segment. What is key is not client acquisition, but client retention.

- Yes. Robo-advisory will never be able to replace the human interactions and soft skills.

- No. HNW and UHWN segments have become very sophisticated, so these segments will require different subject matter specialists to assist them, rather than generalists.

- Yes, without human intervention it will be almost impossible to get attention of HNW and UHNW clients, so in my view RMs will remain central in the decade ahead, but with the enhancement of technology.

- Yes. Because even if the entire bank operates digitally, UHNW and HNW clients will still need/prefer to have human interaction. RMs will move up the value chain and spend less time on more mundane matters, and focus on more value added advisory from a fresh perspective on matters like tax and legacy planning, advising and executing capital market deals, fund raising and so forth.

- Yes, unlike in the mass market segments, the HNW and UHNW clients need customisation in view of size of assets to be managed.

- Somewhat hard to say, but the new generation of wealthy clients might have more interest in algorithm trading, which decreases the need for the RM in the future.

- Yes, but there will need to be a skill-shift away from market commentary to the ability to assist and advise clients in their personal strategic/financial planning.

- Yes, an RM is the conductor of the family’s affairs and therefore essential to the performance of all the players in the long term. They pull everything together, and also provide that emotional intelligence to help within the understanding of the family.

- No, I think RMs will not remain central to those relationship because AI can take over the function in the future.

- Yes, but only if they have strong communication skills and deep relationships because machines, algorithms & digital cannot at this time manage emotions, or understand family values & ethics.

- Yes, because those with money want the human validation aspects of a relationship, most of them don’t want to or don’t have the time to look after their money to the extent that is needed, nor do they have the skills or tools.

Expert Viewpoint – Dominic Gamble, Head of APAC, Wealth Dynamix: “The RM in private banking is still relevant over the coming decade. The question is how the technology works alongside the RM to supplement and augment their day job. Automating administrative and compliance tasks as much as possible and providing suggestions to help RMs intelligently develop and personalise client relationships is key. The statistic from the Hubbis/Wealth Dynamix report highlighting that RMs are overwhelmingly reactive rather than proactive, speaks volumes to the pressures and challenges that RMs face.”

Asia’s Wealth Management Market: Helping the RMs Seize a World of Opportunity

One of the expert panellists stepped back from the detail to survey the market in Asia, remarking that the region has been enjoying the greatest wealth creation on the planet across all segments, from retail to the UHNWIs. “This,” he said, “means that many of the banks and other leading firms have been concerned about having enough well-trained RMs, particularly in the mass-affluent space. Training can certainly bridge some of these gaps, but training must centre on all the angles, from the regulatory and compliance angles through making better use of the tools, the data, and bringing it all together.”

He added that some of the banks are increasingly thinking for some segments that they might be able to supplement their 40-plus RMs with 20 years of experience, with well-trained younger bankers with perhaps five years of experience and outstanding tools and automation. “This could, for example, help them comply with regulations, cross border issues and so forth, as the tools offer automation, they understand the next best action, they can actually listen to the conversation and convert voice to text, and links through to next best actions. These kinds of tools are actually starting to become available. So, training and tech go hand in hand.”

Post-Event Perspectives from the audience on what the banks or EAMs can do to help the RM

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on what they consider the private banks, or EAMs can do to improve the success and client-centricity of the RMs in Asia. We have edited their replies to provide the following insights from the wealth management community.

How best do you think the banks and other wealth management firms can help and support their RMs?

- Better top management vision.

- The organisation’s management needs to put themselves in the shoes of the RM and help them.

- Effective software implementation and tools, rather than multiple programmes.

- Fewer systems for the RMs to handle.

- Proper IT training to smoothly integrate technology into daily business activities.

- More training to help with regulatory and compliance requirements.

- Assuming the digital and virtual aspects are lacking, simply ensuring that RMs have every resource required to go above and beyond in keeping their HNW and UHNW clients happy.

- A robust platform that the RM can leverage.

- Coming from the US, at times, I find myself astonished at how far behind the 'state of the art' the regional wealth management companies and private banks are here. It appears that they are still deeply entrenched in a transactional mindset, even though they may say something different. It seems that there is a real need to focus on the building block basics of truly helping clients manage their wealth. Technology is a key tool and ‘enabler’. If we provide good technology capabilities and position those properly, the RMs will embrace them as an integral part of the development and ongoing enhancement process.

- Better and more streamlined processes and compliance to free up time to attend to income-producing activities.

- The technology deployment can efficiently improve the investment transaction and avoid the long duration of the order confirmation. For the clients, they can attain real-time portfolio status and discuss with RM and IC to meet future wealth plan.

- Be prepared to spend on digitalising the business model. These should be seen as critical tools for RMs. The intangible benefits like improved morale, more time for soft skills and portfolio advisory training, more time with clients and prospects. Ultimately, the business can scale up better, leading to improved return on investment per RM.

- By empowering RMs by giving them time and space so that they can build a long term relationship with the clients rather than a transactional relationship, by bringing in digital tools for research & product updates, and having a robust platform for all types of financial transactions.

- By webinar conference and providing updated market information.

- Not too important. RMs in Asia are glorified customer service representatives. Contrary to having RMs connecting and complimenting technology, they should transition to a contingency role in the event that technology fails.

- Streamlining and digitalisation of antiquated processes and paperwork, and on the front-end clients able to trade or conduct simple transactions online, as some would like to, as well as digital enhancements for gathering client-centric data for better risk management and monitoring of positions and trades.

- A powerful platform which can assist on RM and assistant to do the valuation or calculations to determine whether that investment product is suitable to the customer, fits the portfolio and meets all the regulatory requirements.

- By having a smart system that holistically covers all aspects of the life cycle for client management.

- Establish and e-trade platform to meet the clients’ expectations and a real-time online communication app approved by the authorities.

- RMs have historically had to use antiquated systems and/or too many systems, which has impacted on the time available for engaging with the client. A focus on bringing the RM systems up to date and allowing them better use of data would be a significant help.

Expert Viewpoint – Dominic Gamble, Head of APAC, Wealth Dynamix: “Data is much talked about in the industry but still not widely used to provide crucial business insights and client service personalisation. Addressing the question of data - how to collect it, then how to use it in a meaningful way - is critical for institutions to address, however difficult that is, so that steps can be taken with the right technology solutions to intelligently digest, crunch and provide tangible actions points to the users.”

Expert Viewpoint – Karen Tan, Head of Private Banking, Asia, VP Bank: “Addressing the issue of client centricity, this is part of our business philosophy, and we take great strides in equipping our advisers and talent with the right strategies and technologies, to sustain and cultivate great results with our clients.”

“Technology is not always the magic potion,” a panellist opined. “Training needs to be considered carefully for maximum adoption.” Another expert added that the combination of training plus hands-on experience learning from experienced colleagues is the ideal. “I think smart management teams can combine formal training with shared experiences and best practices,” he commented.

“I agree,” came another voice, “and would add that it is up to the RMs to engage with all the suite of tools at their disposal. The RMs must themselves be welcoming of exploring new ideas, of increasing their knowledge, they must not have a fixed or closed mindset; they need to keep growing. That then helps the banks themselves to change and grow. In short, the RM needs to be a leader of innovation and change.”

A fellow panellist concurred, adding that today’s RMs are no longer the RMs of 10 to 15 years ago, who simply handled the relationship and then leveraged an army of specialists to handle the specifics with the clients. “The RM today needs to be armed with product knowledge, but also a broad general knowledge so that they can talk across many topics with their clients,” they said. “They need to be on top of events and offer their clients viewpoints and strategies on a very timely basis.”

Post-Event Perspectives from the audience on the training and professional development of RMs

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on the role of training and professional development for the RM community in Asia. We have edited their replies to provide the following insights from the wealth management community.

How important is training and professional development for RMs in Asia? How does this connect and complement technology?

- Training and professional development are very important to RMs in Asia to keep them abreast in happening in the fast-changing market environment.

- Very important as it serves us a tool to upgrade the skills of the RM as well as to serve as

- information to help the RM in the course of their work.

- Training and professional development are crucial to prepare and equip RMs to face the increasingly competitive environment especially in keeping up with the younger generations taking over family wealth.

- Very important. Asia’s wealth is being handed over to the next generations which prefer using technology.

- A much-neglected area if compared with the insurance industry where training is regular and constant for products, as well as leadership training. RMs need more than just product training. There should be soft skills training that help RMs to be an effective salesperson and effective adviser to clients. Technology is a critical component especially if we are serious to attract talent into this industry, and to attract 2nd/3rd gen wealth owners to stick with us instead of have their assets flow out to other competitors.

- Clients are becoming more sophisticated. RMs must be capable enough to handle their concerns & objectives. Effective human interaction will make technology less intimidating to clients.

- Training and professional development is of utmost importance. I see the quality of RMs has gone down with the passage of time because of attrition amongst the talented RMs. So, training can act as a tool for RM retention, as well as better client experience.

- It is extremely important so that we are competent enough to continue to provide advisory services to clients. As we are all facing the current pandemic, it is only through technology that we can continue to connect effectively.

- RMs already undertake a lot of training, but there is always a place for learning and professional development which also they should undertake themselves. They should also be trained on the technology available to them so that they can make better use of the data available to them.

- Very important, because some RMs might not want to embrace new technology. Further training & professional development might encourage RMs to take further steps to enhance their skills and keep themselves up to date on the current conditions.

- In our highly regulated industry, RMs must constantly be looking at upskilling through training and professional development. Technology processes are constantly evolving as well and to better serve their clients RMs must ensure they keep abreast of these changes.

Leveraging Smart Technology to Empower the RMs

A panel member commented that despite the RM evidently being core to the HNW and UHNW proposition in the years ahead, the RM is still not often the beneficiary of investment in the latest and best technologies. “Arguably,” he said, “the RM is still one of the poorest-tooled employees within the institution, and yet they are the frontline soldiers. I think it is a relatively quick win to give them the new tools that are data-supported, enabling them to better understand the clients and then offer far more personalised service and far more efficient and targeted delivery. Digital tools will augment and supplement the relationship at all wealth levels.”

Another expert warned that the RMs, especially in the private banks, are spending too much time selling and not enough understanding their clients. They commented that the RMs need to truly leverage a deeper understanding and then proffer a more holistic vision of their wealth solutions, including succession and estate planning.

Another guest advised delegate to look carefully at some of the leaders in digital transformation, for example, DBS Group. He warned that a McKinsey study had highlighted how 70% of digital transformations fail, so tech should be incorporated into the model on a strategic basis, but step by step. “And the culture needs to be embraced from the top and throughout the organisation,” he advised, “and from top to bottom across all areas of the firm.”

A question came from the audience as to what banks and other firms can do to enhance the RM’s creativity and productivity. “The growth mindset of individuals in the firm are less favoured in very large organisations,” came one expert’s reply, “largely because there are policies and procedures and when ideas are offered, top management does not always take those on. In smaller institutions, we believe the RM should be more of a wealth manager than transactional, able to speak sensibly with clients about fine wine investment as much as succession and estate planning. They should be competent over a wide range of different areas, so naturally training is vital to this. We aim to deliver ideas into realities from both side, top management through the firm, and the RMs coming up with their own visions and own ideas, and that will help propel the bank forward.”

Another panellist commented that he is seeing more wealth management providers take the high-level CIO type perspective, aligning much of their investment with that. “When you think about the growth mindset for the RMs, empowering them with the right views, and also the right data and information and then delivering that to them through the dashboards and making all the information and ideas easy and digestible for the RMs is essential,” he observed. “They can learn and update themselves on the go, for example with 5-minute or 10-minute podcasts, news, PDFs, and so forth. In short, it is up to the RMs to engage with all this, but access to information and data is one important element in the overall equation.”

“Technology doesn’t just free up their time by automating tasks,” said another panellist. “It helps them transition from a role that’s very reactive, to being proactive. Having the ability to see data in context means they have more meaningful conversations with clients, thus creating a better client experience.”

“Communication has indeed been vital through the dark times in the markets in March especially,” said another guest. “If clients couldn’t get hold of their RM that would be a major black mark in that relationship going forward. And then being and staying relevant to those clients is essential, offering views on the likely scenarios, reposition the portfolios, having the conversations, being accessible and visible. There is no doubt that Covid-19 is putting stress on the whole industry, but through these difficult months, we have seen that we can shift to a virtual world successfully. As to the future, it will be absolutely critical for our future to further enhance digitalisation, and to make far better use of data. These are going to be fundamental differentiation and success elements in the post-Covid landscape.”

Another expert added that there are also relevant tools to help the RMs help the clients, for example with recommendations on their portfolios, relevant insights to the markets and then delivering with the appropriate and best technologies. We need to see more of the omnichannel and multichannel solutions.” He added that auditable conversations are also valuable for compliance purposes, or exchange of instructions with the clients through apps that can record those activities. “All of this improves the customer experience and ensures that there are proper procedures for the compliance teams and regulators as well,” he commented.

This same expert noted also that clients do not move as readily with RMs if they jump ship as they used to some years ago, largely because of the complexity and annoyance of KYC, onboarding and so forth. “Equally,” he said, “there is more relationship being formed with the wider teams within the banks, so there is broader support and more reasons for the clients to stay.”

A fellow panel member added that their firm was investing heavily in a new portfolio overview and curation tool, which is designed to significantly boost the RM’s engagement with and relevance to the clients.

A guest added that data on the clients themselves should be as much of the overall picture as external data on markets and opportunities. “The role of technology in soaking up client data from those clients directly and from multiple sources is increasingly important in the ultimate delivery of a more personalised service,” he commented. “The institutions have to differentiate, and I think the best way to differentiate is in the way that they provide solutions and services to clients. All the apps and tools are now more hygiene factor than a few years ago, so the next stage of differentiation is similar to that we see in Big Tech and retail, namely providing personalised solutions that really rely on client data.”

“Accordingly,” he continued, “you have got to have a level of sophistication internally in how you are capturing that data through your systems and keeping that data securely, then extracting that into useful functions and useful cases for the RMs. We are often drowning under data but how you then extract that in a meaningful way which complements the RMs day job rather than setting them thousands of tasks is really the icing on the cake; it is absolutely critical to the adoption and success of that sort of innovation.”

A guest agreed, adding that right from the start it is vital to coordinate data, rather than collecting and analysing it in silos. “It is about the whole ecosystem,” he said, “so consistency of data is fundamental, right from the very first meeting and then how data flows all the way through. And then you need to link that through to your dashboard and statements, with alerts and notifications. We talked about relevant advice, but that’s often to marry the house view and linked to the alerts and notifications to the clients, so it is important to get that architecture right, end to end. It sounds very simple, but data is absolutely critical, and it all has to come together to achieve that holistic client experience.”

Another expert added that for any technology to be adopted, it has to be adopted organically by the RMs themselves. “This means that we must, from the top management downwards, consider at the outset what the RM wants to help improve their capabilities and the client experience. And I also believe that the banks need one big core system that evolves itself instead of having a lot of different ones.”

A banker explained that their bank implements technology on a global basis and a lot of time had been spent and significant investment made in improving the lifecycle management and the workflows for the RMs as well as to improve the processes and generally simplify processes. They explained the bank had just launched a new online onboarding system for clients to help the RMs by reducing the paperwork they need to do. “So far it has been embraced very readily, as it is clearly designed to make life better for everyone internally and of course for the clients,” they noted.

Expert Viewpoint – Karen Tan, Head of Private Banking, Asia, VP Bank: “The ideal business model is one of a trusted, committed relationship with clients. This includes an inherent understanding of their value proposition, and an open dialogue with the clients on moving forward. A trusted environment, where clients are guided safely and securely to their objectives.”

The final comments focused on what the pandemic might have done to change the course of the evolution of the RM’s empowerment. “I think it has done wonders to promote the need for the RMs to have better technology internally,” came a reply. “Although how well only they will know within the four walls of each of the banks and firms, the wealth management industry has somewhat weathered the Covid crisis, helped by having some key people actually at the offices. But the further need for providing the client with digital touchpoints I think is absolutely concrete now in people’s minds. From our perspective, conversations on CLM are proliferating as more and more customers are waking up to the need to have an orchestrated and digital client lifecycle management system. Bringing it all together and orchestrate the RM’s technology needs are absolutely imperative.”

“In summary for me,” he said on closing the discussion, “RMs are definitely here to stay, and they need to be given better technology tools, there needs to be more culture inside of institutions focused on digital transformation to really foster that adoption and bring the RMs to the table. I do not believe the RM can succeed that well over the next five to 10 years without these solutions, so the question really is how each institution starts taking the right steps to invest, to decide that cost is valid ahead of revenues in order to bring all this together into a cohesive technology strategy.”

Conclusion

What this pandemic has not done is in any way to alter the trajectory in which the wealth management industry in Asia has been travelling. But what it has done is to turn on the floodlights to show in immense clarity the need for solutions and also the type of solutions that can be achieved, and also how, without it, the wealth management leaders, the RMs and even the clients would still be working somewhat in the dark.

By leveraging technology to create operational efficiencies and enrich client experience, the RMs and the firms they represent will benefit from longer client relationships, and the quality RMs will stay longer at their banks and other advisory firms. The result will be more energised and motivated teams and happier clients who are receiving better and more individually tailored perspectives on their wealth, and then optimised advice, products and solutions.