Publications & Thought Leadership

The Quest for Income and Yield for Asia’s HNW and UHNW Investors

Jun 16, 2021

So much of the world’s highest quality sovereign and quasi-sovereign fixed income was submerged in negative yield territory for most of 2020 while the ongoing global pandemic wrought devastation on many of the economic, fiscal, credit and equity market assumptions that analysts and investors had previously held. But as 2020 turned into 2021, new hopes for a resumption of some kind of normality rose as the vaccines gradually won regulatory approval and as the mass vaccination programmes began to roll out worldwide, prompting a migration of investment back towards cyclical and value stocks. Meanwhile, the US election, followed by the USD1.9 trillion Biden-encouraged Federal Reserve QE programme, and of course with the positive news around the effectiveness of the vaccines, have all combined to drive US Treasury yields significantly higher. Having reached an all-time low of 0.52% overnight during August 2020 and having ended 2020 well below 1%, the yield was hovering around 1.5% by June 10. And at the same time, as prospects for a resumption of economic growth around the world improve and the rotation to cyclical and value stocks both continue, there is at the same time greater hope for a recovery in dividends for the traditionally strong cash-generating corporations around the world. But what damage could inflation wreak on financial markets and portfolios? The US Federal Reserve remains confident inflation should remain under control, despite recent headline numbers suggesting otherwise, and despite leading analysts and institutional investors becoming increasingly apprehensive. So how do wealthy private investors play all these factors as they search for income and yield in their portfolios? The panel of experts at our Hubbis Digital Dialogue of June 10 sought to offer their insights, set against the backdrop of what is a somewhat more optimistic but still highly uncertain world.

Panel Members

- Darren Wills, APAC Head of Fixed Income iShares and Institutional Index, BlackRock

- Nivedita Sunil, Portfolio Manager, Asia & EM Fixed Income, Lombard Odier Investment Managers

- David Storm, Chief Investment Officer - British Isles & Asia, RBC Wealth Management

- Alex Yang, Vice President, Institutional Solutions, Samsung Asset Management

- Aman Dhingra, Managing Director - Head of Advisory, UBP

Some of the Questions addressed:

- What is happening to interest rates and fixed income yields globally, why and what is the outlook?

- What is happening to equities, corporate profitability and dividends, and what is the outlook?

- What is the likelihood of continuing QE around the developed world?

- What allocations to fixed income do panel members recommend in this environment? And what allocations to value/dividend stocks rather than low/no income growth stocks?

- Where should Asia’s private clients turn to seek predictable, low-risk income?

- What role should leverage play in Asia’s HNW and UHNW fixed income portfolios in the current environment?

- What about the prospects for yield and income from structured products and other more esoteric investment structures?

- What is the trade-off between short-term and longer-dated paper in the fixed income markets?

- Are ETFs or active funds the right way to play fixed income and dividend stocks, and why? And what about REITs? Can they offer both safe income and gains as well?

- Do the private markets offer better opportunities to earn yield and income, or are the public markets more prolific, and why?

- What opportunities for yield and income are there within Asia itself, for example, in the vast and rapidly opening Chinese fixed income market, or amongst the historically strong dividend-yielding corporations in the region?

Everything is relative

“With the yield at 1.5% on the 10-year US Treasury bond, yield is very tough to find these days,” said one guest opening the discussion. But he said that 1.5% was not so bad in the context of central banks pumping liquidity to support economies and while his firm expects rates to drift somewhat higher, the rise will be only modest. He said his firm has many conversations with clients about rates, and most people think late 2023 at the earliest for the Fed to raise rates, and for the ECB more like 2025. “So, expectations for yields are still low and much lower than they used to be.”

Accordingly, he reported that for his firm, fixed income allocations are definitely lower at the moment and in particular, in rates. “We tend to be more allocated to spread product, and in equities we've been adding infrastructure equity income as a bit of a defensive play. We don’t want to be overweight value, or growth, so we've really been looking at adding stable dividend-paying stocks to portfolios to add yield and to cut duration.”

Rates won’t race ahead

The roughly 1.5% yield on 10-year paper, although lower than the 1.7% yield breached in March this year, is some three times higher than in mid-2020, when the yield approached just 50 basis points.

“So, where are we headed from here?” pondered another guest. “There is a chance the yield could approach 2%, with a risk of a slight overshoot beyond that, but that is where we see rates side tapering off. So, to get more return, you need to assume more credit risk, or you can look for equity income. For us, we like the private market side of things. Yes, there is a bit of a valuation risk there as well, but at least we believe that the illiquidity premium is worth picking up for clients who can be really patient.” He said there are pockets of opportunity of course, but traditional fixed income is somewhat challenged currently across the board.

Is taking on more risk advisable to help boost yields?

He also explained that structured products could also be used to boost returns, assuming risks are carefully assessed. Moreover, leverage can be applied to portfolios, although to really make use of leverage, you need arbitrage opportunities.

“Traditionally, you invest long and borrow short, with sufficient slope in the curve that you can pick up enough yield to have that leverage make a significant impact. But while there is some degree of yield curve returning to the US in particular, which is welcome, it is not like before. Leverage can also be used to allocate more to spread paper, but this is not the most opportune time now, as spreads are really tight across the board, very compressed. In short, there is not so much you can do with leverage these days, even with borrowing costs so low for HNWIs. So, very selectively and discerningly, yes, but generally the risk outweighs the returns from using leverage.”

Private credit can offer appealing opportunities

This is why, he said, he directs more clients to the private markets. He cited two examples of recent trades they had executed, one involving acquisitions of data centres, which are in increasing demand due to data doubling every two to three years. The other private deal centres on music portfolios of marquee, evergreen artists, where the estate still produces constant annual yield. The names are household names that are still well-liked today and have appeal across the generations, and where the portfolios therefore produce stable and regular cashflows. “This is another lovely story of how we combine a growth story along with the dividend story, to kind of substitute fixed income out of client portfolios, and to some extent, substitute equity and, and create an alternative source of return,” he reported.

Expert Opinion - Darren Wills, APAC Head of Fixed Income iShares and Institutional Index, BlackRock: “Fixed income investors have turned to index vehicles, and especially ETFs, as efficient instruments to implement their views in their asset allocation framework.”

Expert Opinion - Alex Yang, Vice President, Institutional Solutions, Samsung Asset Management: “REITs are one of the very few asset classes that still generate attractive and stable dividends in a low yield environment. The sector also benefits from the current rotation into the value/defensive stocks.v

Can a greater allocation to Asian fixed income offer an answer?

Another panellist said he had a rather different view on fixed income. He reported he likes the Asian fixed income arena far more than the US market, for example. He said data shows it is possible to obtain yields of around 2.5% at around five years of duration in investment-grade paper. And for those to play duration and credit risk more aggressively, yield of 4.5% to 5% are possible.

He cited the recent closing of their fixed maturity fund with a maturity of about three years and yield of around 4.25%, and their flagship fund, yielding around 4.8%. He explained that they focus on dollar debt in the Asian market, but there is increasingly diversification into domestic debt, for example, Chinese local government bonds, where there is a roughly 1.7% pick-up at least over US 10-year paper, and where the opening of the Chinese debt markets is helping pull in more and more foreign funds.

China beckons but go for safety and avoid credit

But he cautioned against Chinese credit. “China is going through a very, very ambitious transition, and has been trying to do that for the past few years, switching emphasis from an export-led economy into being much more domestic demand economy, much driven by the ageing demographics,” he explained. “During this process, there is moral hazard and there can be a lot of volatility in the local markets as you go down the credit curve. So, for China, we recommend local government bonds plus only going along the credit spectrum in dollars, because that's much more liquid, and much higher yielding, even now.”

“Let me clarify,” came the riposte from the panel member who had sounded far more caution over the world of fixed income today. “Mine was a generalisation, so let me clarify,” he said, and reported that they had indeed been playing the China card, seeing opportunities there in terms of the currency and arbitrage. And elsewhere, he added that they had also been focused on senior loans and contingent convertible (CoCo) paper issued by the banks. “So, yes, there are pockets of opportunity,” he elucidated, “but now very selectively so.”

Investing after and during a natural disaster

A guest then remarked that the economic outlook is all about restarting, not recovery, so it differs from the fallout of the global financial crisis. “We see it more like a natural disaster. So, it is like a cessation of economic activity followed by a restart, rather than a traditional business cycle recession followed by a recovery,” he observed. This means there is now volatile near-term growth and worrisome inflation data.

“Yes,” he said, “long term yields have risen, especially in the US, less so in other developed markets, such as Japan and Europe, but it's been more muted than we've seen in previous phases of rising inflation and accelerating growth in past environments.”

Rates lower-for-longer and credit spreads set to remain tight

He said they see a far lower-for-longer path of short-term interest rates, and they see a more muted response of government bond yields to stronger growth and higher inflation than in the past because central banks are going to lean against any sharp yield rises. “This,” he reported, “means we expect short-term rates to stay anchored, and we think that's supportive for risk assets, both from an equity perspective, but also, from a credit spread perspective.”

And he concluded that they therefore consider financial conditions being constructive for spread assets from a carry perspective, and no immediate reason to expect any material widening in credit spreads in the near future.

Seeing fixed income as part of the broader portfolio

Looking at this from the portfolio construction angle, he then pondered how fixed income allocation fits a multi-asset view rather than a more direct view of fixed income markets. “The answer for us is that fixed income is not necessarily in people's portfolios to provide an absolute return from a positive sense,” he explained. “Clearly balanced portfolios have been supercharged somewhat in terms of their returns over the past 10 to 15 years because rates have come down from historic level,s but fixed income was not always necessarily in people's portfolios to provide that absolute return or that capital appreciation. It is there to provide income; it can be there to provide equity diversification and ballast and a negative correlation to risk assets. Accordingly, when putting together that fixed income part of the portfolio, fixed income as an asset class should really reflect the [client] view of what fixed income is trying to do in their portfolio context.”

He offered some examples. China, he stated, offers a good opportunity for example to increase allocation to the onshore China government bond or policy bank market. “We think it offers an attractive yield pick-up for similar quality in other developed markets, and we think that it has a lower correlation to both other risk assets and other developed government bond markets,” he stated.

Expert Opinion - Darren Wills, APAC Head of Fixed Income iShares and Institutional Index, BlackRock: “How you manage your risk and build your portfolio is crucial, and fixed income ETFs are an incredibly effective and precise tool that can potentially enhance portfolio outcomes.”

Expert Opinion - Alex Yang, Vice President, Institutional Solutions, Samsung Asset Management: “Historical data shows that REITs could be a natural hedge to inflation. As the post-COVID economy improves, housing price and rent would generally move up as well. So as the inflation expectation rises, this should benefit the REITs sector.”

Asian credit’s noteworthy pick-up to US paper

Looking broadly at fixed income, he said while rate rises will be subdued, the direction is upwards, so the question is as to how investors can maintain yield whilst not taking on additional duration or interest rate risk? Answering his question, he advised Asia IG corporate credit, as it offers a yield pick-up for a shorter duration and at similar risk levels to US paper.

“You also get a significant pick-up for investing in Asia high yield for similar credit quality compared to the US, with a pick-up currently still over 200 basis points,” he reported. In short, you must look closely at your fixed income allocation in terms of your overall portfolio construction, and what it's doing in your portfolio. Is it capital preservation? Is it equity diversification? Is it generation of income? And then seek areas that still offer value, even given the low-rate environment.”

But active strategies can enhance returns

“For us with our value fund, we are very benchmark agnostic,” he reported. “The benchmark might have 85% investment grade, 15% high yield, but we might allocate 40% high yield and 60% investment grade, but of course actively and selectively.” And he indicated this means that simply by moving away from the indices, the benchmarks, investors can achieve better results with the right active strategies.

And he remarked that active fees have come down quite sharply, whilst liquidity for ETFs is not as evident as it might appear on the surface, as there are technical and structural nuances that might result in ETFs not delivering quite the levels of value one might have assumed.

A balanced view - blending active, passive and direct strategies

Another panel member explained that their platform offers a wide variety of both active and passive funds, and that there are places for both approaches in portfolios. He said investors could benefit from blending these approaches, depending on their own ability to actually navigate between different areas of the fixed income market themselves.

He therefore recommended blending a combination of core index building blocks. ETFs for precision access to certain parts of the fixed income markets, be it China bonds, or high yield, or different parts of the US credit curve. And alongside active funds where investors achieve exposures that they can't access through an index vehicle, then layering in factor strategies is worth considering to thereby take factor tilts away from strategic benchmarks.

ETFs for precision

He explained that where he considers the ETF really comes into its own is for those investors of multi-asset funds looking at a whole portfolio level and themselves deciding on asset allocation within fixed income. “ETFs allow them to access different parts of the fixed income markets with precision as and when they want to, with low transaction costs and ease of access that can be considerably lower than you would find in traditional fund structures,” he reported. “Accordingly, when putting together your asset allocation framework, ETFs can be an effective way to implement your view, without potentially that view being allocated away by an active manager who is doing the same thing.”

Expert Opinion - Alex Yang, Vice President, Institutional Solutions, Samsung Asset Management: “In Asia, ETFs are being increasingly used by private clients and their advisors for broader use cases, from asset allocation and accessing restricted markets, to yield enhancement and liquidity management.”

Expert Opinion - Darren Wills, APAC Head of Fixed Income iShares and Institutional Index, BlackRock: “Fixed income ETFs have allowed investors to access international fixed income markets in a far easier, more transparent and cost-efficient way than how they might have traditionally done through investing in single line bonds.”

ETFs offer highly competitive access

This same expert remarked on the bewildering array of different options for investors to navigate, both in the index fund space and the active fund space. “If you don't have any experience or capability to do the research in fixed income space, it might be entirely appropriate to allocate that away to a traditional active manager who will do that allocation for you,” he reported. “If you do have the framework to actually allocate between fixed income sectors yourself, then yes, indices and ETFs are a very efficient, easy and cost-effective way of doing that. And yes, index returns, or ETF returns have been proven to actually offer a very competitive, cost-adjusted return across most market cycles.”

Another expert said he generally agreed with those comments, but added that in his view, ETFs do provide some additional benefits that active funds are unable to provide. ETFs, he said, were very low cost with management fees generally 50% or more lower than active funds. ETFs also provide greater transparency, greater flexibility and greater liquidity as well, because ETFs are listed on the exchanges, with settlement T+2 rather than a number of more days for active trades.

ETFs for transparency and low cost

“In terms of transparency,” he reported, “ETFs are actually required by regulation in many jurisdictions to disclose their daily composition, their daily holdings, as well as the weightings of each constituent. Whereas active funds will only disclose the holdings on a monthly or quarterly basis. This means investors can make more precise decisions with ETFs as to when and how they can capture market opportunities.”

Returning to the active/passive discussion another expert remarked that weightings are not like for equities, where the largest cap stocks get the highest weightings, as some of the largest companies might have very little debt. He said if investors follow the volume of debt issued for weightings, then they are merely getting exposure to the most indebted corporations, implying weaker credits actually or potentially.

Another panellist responded to these various assertions by remarking that high levels of debt for any company does not necessarily translate to weaker credit. “We do need to be careful about our terminology here,” he cautioned. And he countered an earlier assertion by commenting that if people properly understand how fixed income ETFs work in practice, they would understand there's no disparity in the underlying bond pricing obtained from any particular bank or liquidity provider by those ETFs.

Fixed income ETFs: liquidity tough to argue against

“In the fixed income space,” he stated, “the concept of a beta instrument being traded and being more liquid than its underlying constituents is fairly well accepted. CDS baskets work in exactly the same way - CDS trades more liquid at the basket level than the underlying constituents.” And he then expanded on this view to offer more explanation as to how and why ETFs in reality offer the best access to liquidity in the fixed income space.

Overall, this expert reiterated his call for a balanced approach by investors, restating that both active and passive approaches have their advantages. He said active managers can decide to move away from a strategic benchmark or an allocation to try and generate excess returns, but that is not simply deciding to take more risk to achieve higher returns, as that approach exposes portfolios to major selloffs. “There's no right or wrong here,” he concluded, it is just understanding the risks that are inherent within your portfolio and making sure that you allocate those vehicles accordingly.”

Active managers also increasingly use ETFs

Another perspective came from an expert who said that active managers have been increasingly using ETFs as an underlying tool for their portfolio construction as well. “This is particularly the case in areas where the underlying market is not liquid enough or when the markets are not easily accessible or are completely unavailable to them, so for example ETFs that are listed in the offshore markets will actually provide an additional tool for them to access that market relatively easily. There are two layers of liquidity, the underlying liquidity which is from the constituents in the ETF and also the secondary market liquidity which is the ETF traded on the exchange. So, when the underlying market liquidity is limited, the additional liquidity on the secondary market could actually provide additional ease and stability even for active fund managers.”

Another expert confirmed this view. He said that there is indeed a difference in approach required between developed and highly liquid markets and many areas of the EM universe, where there are far fewer fund managers around who can really outperform the indices consistently. “We ourselves implement with active in EM,” he reported, “but we would, for example, use the precision of ETF instruments to just manage our overall portfolio duration in developed market rates. So, there's definitely space for both [the active and also ETF] approaches in portfolios in both fixed income and equity.”

Asia and its role in expanding the universe of ETFs

A guest highlighted the ongoing expansion of the world of ETFs targeted at the Asian market and investors. He reported, for example, that his firm had been busy in South Korea as the largest ETF issuer there, representing about 52% of the market share. He reported they had introduced the first inverse and leveraged products in Asia and had opened their ETF operation in 2016 by introducing the first ever futures-based ETF in Hong Kong, and continue to innovate today.

He highlighted for example their high dividend APAC ex-New Zealand REIT ETF, which he said was ideal for low risk and enhanced income in the current low yield environment. “We saw the pandemic hit some income stocks in 2020 after the pandemic hit, including the bank sector, but as we search across the entire equity markets, we see that REITs are one of the very few sectors that currently still deliver relatively stable and decent dividends.”

REITs in Asia – a compelling story

He reported that their REITs ETF had an average yield of 5.15% looking back over the past 10 years, and that exposure to REITs offers both potential for price appreciation as well as attractive dividends. “The valuation of REITs, particularly APAC REITs, are still at a relatively attractive, and certainly more attractive than growth sectors, and also more attractive than their US counterparts in terms of PE and price to book,” he explained.

And he added that from the nadir of the markets in late March last year, APAC REITs actually rebounded over 90%, and during the same period, US REITs rebounded only 60% and European REITs just 10%. “This to our view demonstrates the stronger resilience of APAC REITs compared with their US and European counterparts,” he enthused. “But with the attractive valuations still in place today, it also means that now is still a relatively attractive entry point for investors”.

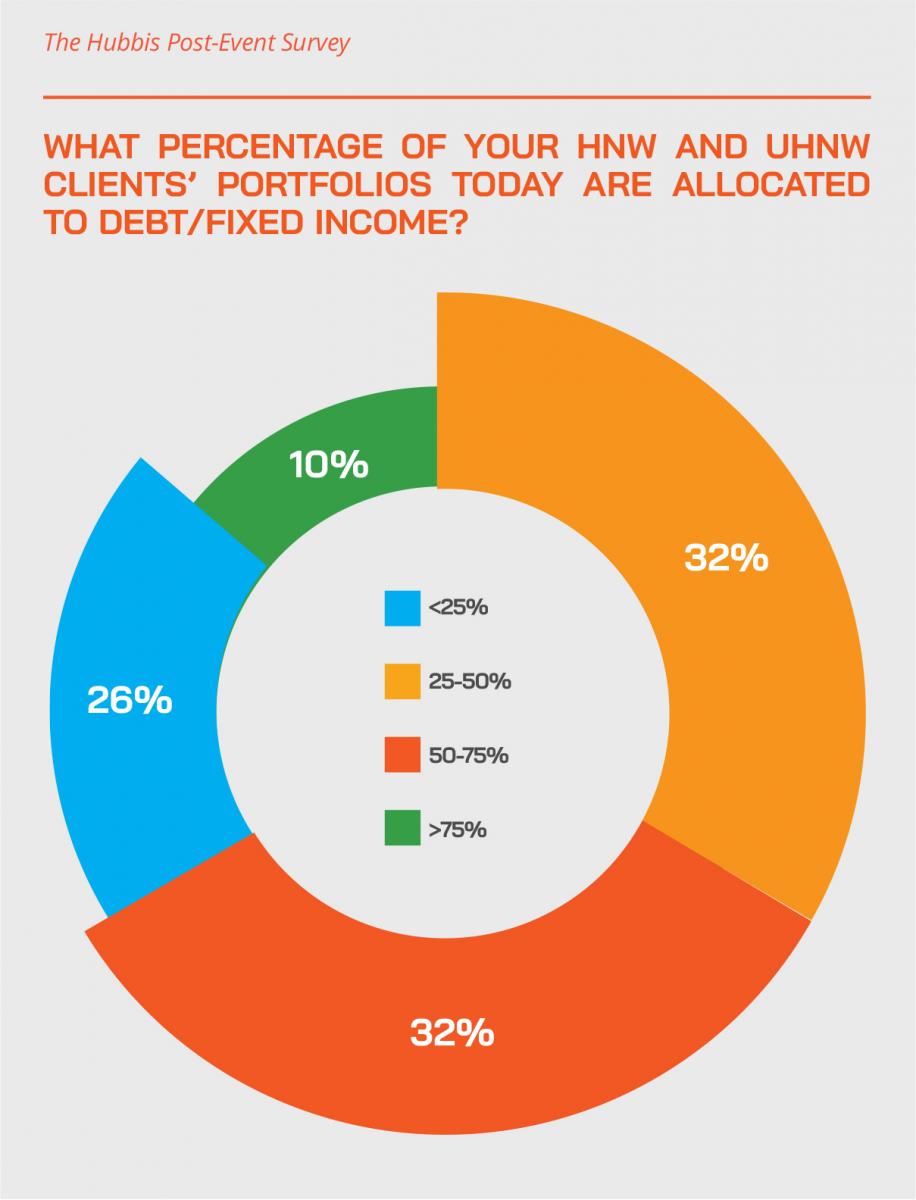

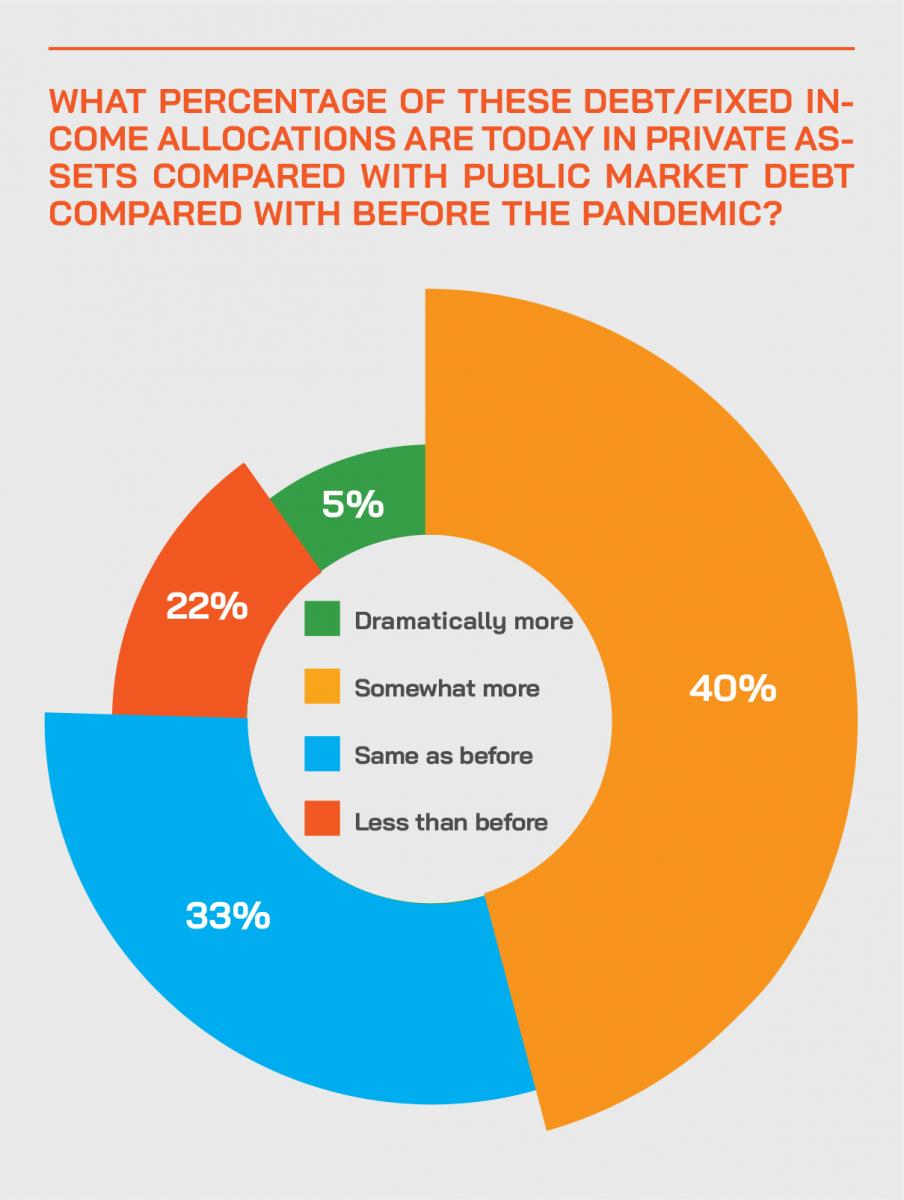

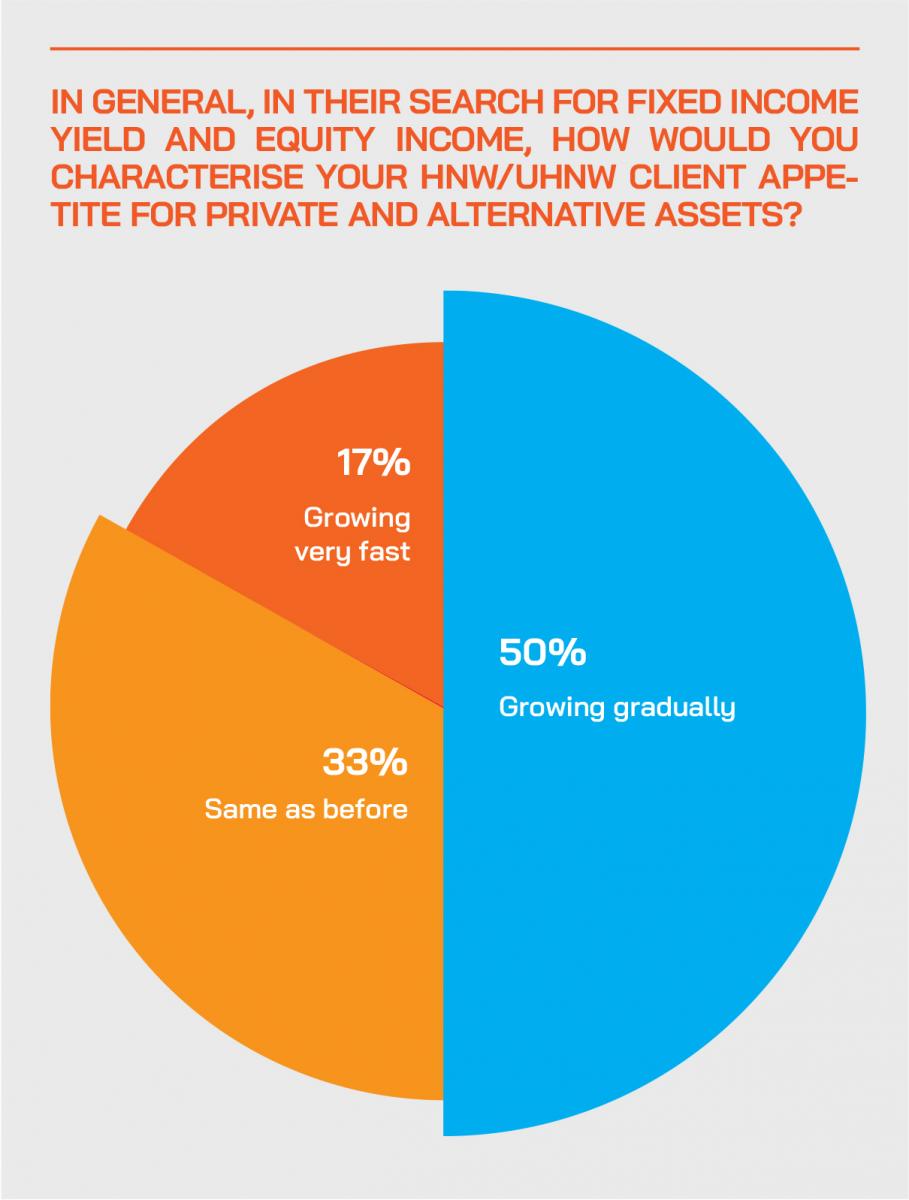

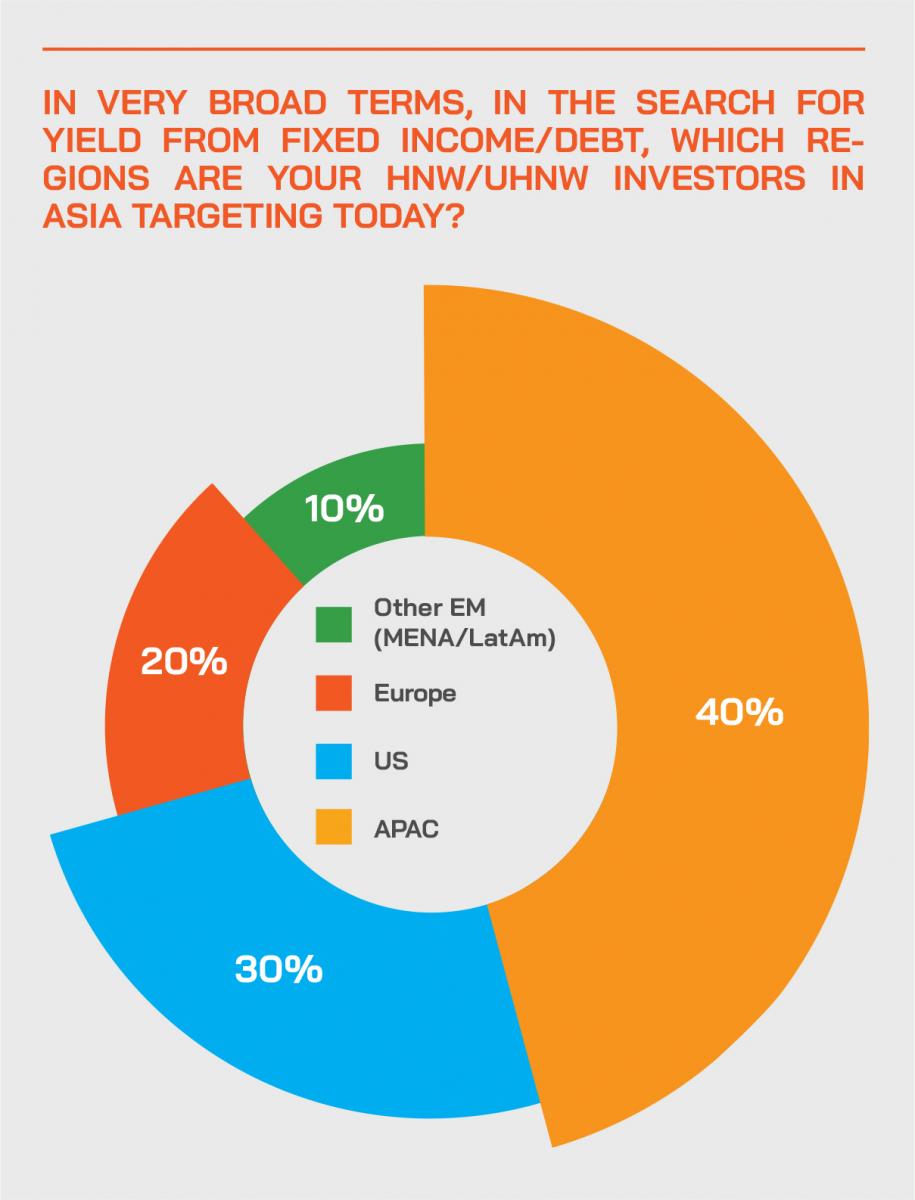

The Hubbis Post-Event Survey

As usual, we polled our delegates for their opinions on market trends and the advice their own banks and firms are offering, and how clients are positioning themselves. We have briefly summarised their many insights below.

Hubbis: In relation to the search for yield, do your HNW and UHNW clients in Asia today prefer the public bond markets or private debt markets, and briefly, why?

Those who preferred the public bond markets said this is because:

- There is more reliable coverage of research and information.

- Credit ratings, transparency and liquidity.

- More easily traded OTC.

- Lower default rates.

- Regular updates of information.

- Risk aversion.

- HNW and UHNW clients like the clarity of the public and liquid markets.

- Pricing transparency, mark to market.

- Stability.

- Due to uncertainties in yields and the uncertain global outlook, our clients prefer public markets.

- We find HNW investors prefer the public markets, while UHNW investors have the risk capacity to invest privately for higher returns.

- Private debt market entry costs are too high, investments required too large.

- Regulated markets, transparent pricing.

- The majority of Asian PB clients are still resistant to private debt and wary of exposures.

- More education required for both clients and RMs to encourage more private market investment.

- Holding period/time commitment too long in the private markets.

- Private market illiquidity means it is tough to exit if required.

Those who preferred the private debt market said this because:

- Private debt as this is more tailored and personalised.

- Private because we can find enhanced returns amidst a low yield public market environment.

- Private due to higher yields and less exposure to market volatility.

- Private debt markets are now enormous globally and offer a huge range of choice.

- Those prepared to take on more risk, illiquidity and longer time exposures are rewarded with higher returns.

Hubbis: Is leveraging fixed income portfolios practical/reasonable today for these clients, and why or why not?

- Yes. Compared to the unstable markets of big last year, there is more clarity, and it is safer to resume leverage.

- Yes. Necessary to boost returns given the very low yields and very low interest rate environment.

- No. With inflation looming in the horizon, interest rates are set to rise rendering leverage risky.

- No, it does not make as even with leverage the yields are not great.

- Leveraging up to 50% of the portfolio is alright but it depends on the client’s risk appetite.

- Yes. Low risk currently and higher return.

- Not really, as there is less opportunity for arbitrage than in the past.

- Not practical. The yield is so extremely low.

- Not meaningful as the spread available is not commensurate with the increased risks.

- Not very reasonable - we think volatility is around the corner and it is the time to start deleveraging the portfolios.

- Yes, reasonable. These clients need the regular income and more diversification from equities.

What to avoid? Duration and IG credit

As the discussion drew towards a close, a delegate asked what panel members would avoid currently in terms of fixed income exposures. One guest reported that he prefers to avoid or at least reduce duration. “We are definitely underweight duration, and we are definitely overweight rate spread complex at the moment. Another area that we're probably not so enthused about is IG, as the spreads are so tight and accordingly we prefer to barbell the approach and actually be really active on one side and then use passive instruments on the other side for our rates exposure.”

Another guest agreed, adding that he too sees IG spreads as so tight that it's almost not worth taking that risk. “You would rather take on something higher beta for higher returns, and then stay on cash or interest rates on the other side to barbell it,” he said. “It's really about being discerning, trying to pick names that make more sense, it really depends on the underlying bonds and the credits themselves.”

Sustainability and ESG: across the board

Another expert said that the discussion must also include a reference to the vital importance these days of ESG and sustainability, noting that he has responsibility for investment across both Europe and Asia, and that in Europe, there are very clear newly introduced rules in March this year, directing to the integration of sustainability considerations into any investment decision for fund managers, whether equity or fixed income.

“It's very clear for us that we have to include those considerations,” he explained, “and then it becomes more around what flavour of ESG you actually want, which data provider do you want to use, subjective data or objective data and so forth. We use objective data so that we can identify, for example, how adding or removing certain investments might increase or decrease the emissions of a portfolio, or how those moves might affect diversity. ESG is across the portfolio, it's in every asset class now, and I think you will find that as we progress, that's something that will happen more and more across the globe.”

Inflation – to be or not to be? That is the question…

The final element of the discussion saw the panel return to the question of inflation, with one expert stating that there are factors on both sides of the equation. He said inflation numbers will rise in 2021 but that in the medium to longer term view structural factors such as demographics and technology signal more of a disinflationary environment ahead.

“Asset inflation is real,” he stated. “It has happened, and it is happening all the time. But not so mainstream inflation, and I do think it's harder to see that play out meaningfully. Accordingly, while there's risk of overshoot, we still believe that long term, inflation is really not the most material risk that we're looking at right now. It's certainly not the base case for us.