Publications & Thought Leadership

The Evolution of DPM in Asia’s Wealth Management Market

Oct 7, 2020

A gradual but extremely important shift is underway in the approach of Asia’s wealth management community as private banks, and independent asset management firms strive to boost the prevalence of discretionary portfolio management (DPM) and advisory solutions and thereby decrease their traditional reliance on transactional revenues, which can be fickle and difficult to predict, and which can easily dry up in very difficult market conditions. Specifically, there are changes in investor appetite for different asset classes, the market is continually adapting to regulatory reform, and there has been persistent market volatility this year, as well as great uncertainty. The gradual evolution of the advisory model in the region, as well as incremental growth in demand for longer-term investment strategies, and a growing inclination for a greater allocation to private and alternative assets, are among the other key drivers towards more managed accounts and discretionary portfolios playing a more prominent role for Asian private clients going forward. It is slow and gradual, as yet, but this evolution offers an unprecedented opportunity to change the way the industry engages with its clients. It is slow in Asia, as Asian private clients have long preferred to control their investments and have a predilection not to pay for financial advice. However, this does not deter the wealth management community from driving towards these goals, and there are many who hope and believe that Asia can ultimately emulate the successful DPM and advisory model in Switzerland and Europe. The Hubbis Digital Dialogue of October 1 saw a panel of genuine wealth management experts assemble for what was a fascinating and highly informative ‘virtual’ discussion.

Sponsors: The Global CIO Office and Premia Partners

A senior banker opened the discussion by explaining that their business strategy for the past seven-plus years in Asia has been driven by building a reputation as a key DPM player and that the bank had already achieved a near 60% DPM penetration.

“While Asia itself is a late starter,” he remarked, “I don't see any reason why the kind of trends we see in other parts of the world and especially in Europe, in favour of more DPM will not kick in and actually it has already begun out here. And contrary to a very widespread opinion, it's not that difficult to convince Asian clients to put some of their portfolios, perhaps a tiny portion at the beginning into a DPM solution. And then with the passage of time to let them experience the fact that portfolio construction and a more institutional process might be more helpful in the long run.”

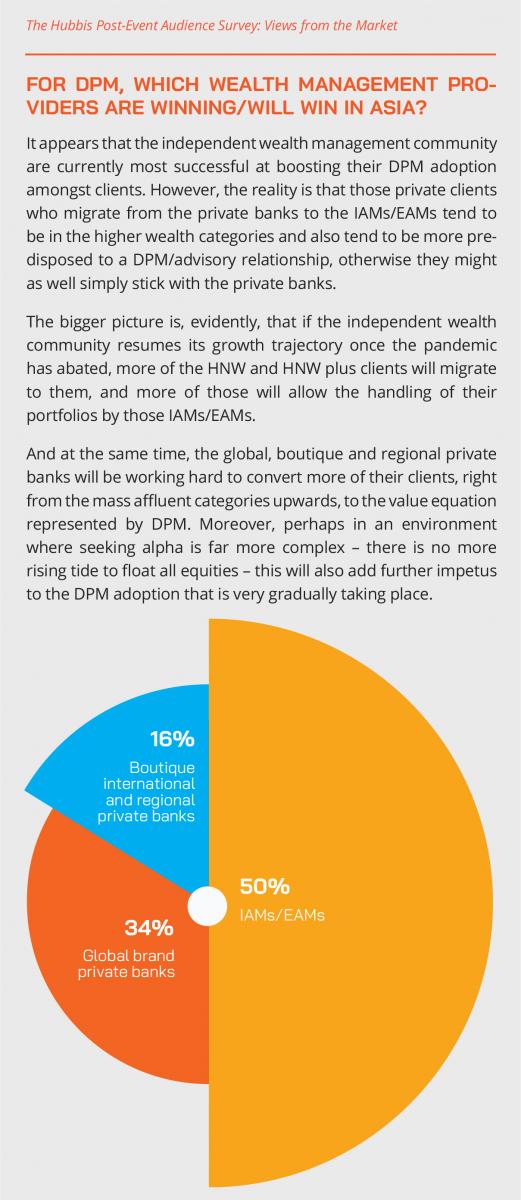

Growth of DPM in Asia is accelerating

Another panellist concurred, noting that their bank was growing its DPM mandates at double-digit rates each year. Clients he explained increasingly see the benefit of spending more time on other matters, or perhaps leisure, than trying to handle their own investment portfolios. “They see the value proposition with discretionary portfolio management,” he said, “and as a result, it has been a much easier win-win for not only the client but for RMs and for the bank as well.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific & CEO, Hong Kong, Lombard Odier: “While clients- or RM-driven portfolios often focus on securities or instruments selection, DPM processes usually put portfolio construction at the centre of their value proposition. There is no doubt that some highly concentrated or imbalanced portfolios can outperform, sometimes significantly. But, over time, superior portfolio construction translates to more efficient risk allocation and a higher capacity to compound robust returns”.

Expert Opinion – David Lai, Partner, Co-Chief Investment Officer, Premia Partners: “As an ETF manager, we see an increasing number of DPM teams located in Asia using ETFs as the building blocks in managing the portfolios. The features of high transparency, low cost, ease of trading, and diversified exposure, which are all highly appreciated by the DPM managers. Compared to a few years ago when we first began the dialogue with the gatekeepers at the private banks, the conversation now becomes more natural, and the acceptance is rising. More private banks and wealth managers are indeed building up their ETF specialist team to help support the rising demand.”

Gary Dugan, Chief Executive Officer, The Global CIO Office: “I think many of us have been doing this business for decades. And when you look at the available returns today, they are the most miserable post war. And yet institutionally, if you look around the world, endowment funds in the United States through to pension funds in Europe, everyone is scrambling to try and find the right solution. So, I think the big challenge to DPM, and it has been taken on by these family offices today, is trying to find other risk premia that they can put inside their portfolios to give them those long-term returns.”

A fellow panellist reported an increasing number of the DPM teams located in Asia using ETFs as a building block, shifting their attention from mutual funds. “They see ETFs as offering transparency, sensible costs, trading flexibility, liquidity, and diversified exposure,” he reported. “When we first started the dialogue a few years ago, a lot of gatekeepers in the private banks were quite yet accepting of ETFs, but they are now getting more familiar with different kinds of offerings, so they can go to more granular strategies, either a more thematic approach, or a more industry-specific or even sector-based approach. Many are also building up the Asian ETF special team, instead of relying on their US or European HQs.”

DPM must be embraced throughout

A different view was offered by another expert who said that a key is to make sure that the DPM proposition is front and centre in the bank or firm, including of course the compensation structures. “Right now,” he said, “there are still some very major banks in the region who are not able yet to put the DPM out there, although quite frankly, I think if you look at all the academic research, this is the best approach for the client rather than using a brokerage account.”

“Agreed,” said one banker, “and yes, to convince the management and to convince the client, first you must prove your performance and asset growth. Our DPM has outperformed almost 85% of clients’ self-directed accounts, not because we are smarter but because we focus on strategic asset allocation and a very disciplined approach. We do not suffer emotional or behavioural finance issues, either over-confidence, or over-anxiety. In DPM, if a stock goes up, as long as the valuation remains appealing, we will continue to hold it, whereas, for losses, there is strict discipline and actions accordingly. Once clients are convinced that you actually have a real value proposition, the assets will follow through.”

Total commitment to DPM required

Another banker said he completely agreed with the premise that the management must be fully committed to the DPM strategy for the long run. The view must be of the long-term for sustainable success, he said, and ensure the RMs are fully convinced over the value proposition and ready to play that game. “You need to convince the first wave of RMs and then new RMs coming in will follow suit,” he said. “But it's not easy. However, the bankers are increasingly very aware that it will be very difficult in the future for a private bank to develop without a strong DPM proposal. Accordingly, these RMs understand they should progressively transform part of their book into DPM because it's the way that they will sustain revenues and manage regulatory requirements, which on the transactional front are increasingly heavy.” Moreover, he added that more DPM means more RM time freed up for new clients and new propositions.

Expert Opinion – David Lai, Partner, Co-Chief Investment Officer, Premia Partners: “With the ongoing product development of the ETF industry in Asia, DPM managers can easily get market access through ETFs. For some niche exposure like Vietnam, a portfolio manager can now use our Premia MSCI Vietnam ETF to gain exposure of this frontier market for the purpose of strategic asset allocation or a tactical asset allocation.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific & CEO, Hong Kong, Lombard Odier: “Over time, investment success is less a question of guts, insight or even talent, but mostly the result of discipline. Professional investment processes offered through DPM mandates usually guarantee a high level of persistent discipline.”

Asset allocation in the world ahead

The discussion shifted to asset allocation, with an expert commenting that with financial markets and rates as they are, there is greater open-mindedness needed in terms of constructing an effective strategic asset allocation ahead.

“One of the aspects I see of daily life inside a single- or multi-family office at the moment is the work done on trying to find better instruments to reference a certain asset class and the hunt for real returns. When you look at the available returns today, they are the most miserable for decades. And yet institutionally, if you look around the world, endowment funds in the United States through to pension funds in Europe, everyone is scrambling to try and find the right solution. So, I think the big challenge to DPM, and it has been taken on by these family offices today, is trying to identify other risk premia that they can put inside their portfolios to give them those long-term returns.”

He then explained that opting for less liquid assets, or even illiquidity is one approach, meaning perhaps private equity, or venture capital, for example. “Many of the things that diversified your portfolio in the past don't achieve that in the foreseeable future,” he cautioned. “So, the focus is on finding those new asset classes, and not just finding them but actually deploying them. We have seen some mainstream consultants recently going around some of our clients, explaining that the future is going to be 65% in illiquid investments, that a family if it sits down today, that plans for the next 30 years in terms of growing their wealth, they have to adopt these assets, this type of strategic asset allocation. In short, we really have to start the conversation around the use of more illiquid strategies, that is becoming a mainstream conversation today.”

Expert Opinion - Jean-Louis Nakamura, Chief Investment Officer, Asia Pacific & CEO, Hong Kong, Lombard Odier: “The Covid-19 crisis may have been a bit challenging for DPM mandates. Firstly because the nature of the shock was as difficult for professional investors to apprehend as it was for individual investors. But more importantly, because many individuals were suddenly faced with more available time to try to play with the markets. However, this situation has been normalizing quickly.”

Expert Opinion – David Lai, Partner, Co-Chief Investment Officer, Premia Partners: “DPM managers are using ETFs to express their different market views precisely, such as using our Premia China New Economy ETF to benefit from the structural change in China, or our Premia Asia Innovative Technology ETF to capture the growth opportunity in Asian leaders in digital transformation, robotics and AI, health and life science.”

Gary Dugan, Chief Executive Officer, The Global CIO Office: “I have to say the number of valid and I stress the word valid, valid instruments that you can use out there at the moment is very, very limited. I think there was 130 funds globally, on reasonable criteria, that call themselves fixed income ESG. And when you went down to it, there's probably only two or three that would be acceptable. So, I went in there, checked what the bond holdings were, 15% in the energy sector. So, the clients’ expectations are that you will be able to find them an ESG colour to their portfolios, but it is still very, very difficult.”

A holistic perspective required

A guest agreed but added that a challenge for many Asian clients have is that they have businesses which are illiquid, they have substantial real estate holdings, which are also relatively illiquid. “We need to therefore look broadly at the entire wealth of the clients,” he advised, “because when you're doing a strategic asset allocation with the client, you can't just look at their bankable assets you need to be looking at their entire wealth dispersion, their succession arrangements, their intergenerational transfer requirements and so on.”

Another guest commented that the old 60-40 kind of allocation does not currently work. “We need to find niche products and also lower the correlation among different asset classes,” he said. “We have accordingly been developing some unique products for the asset allocator to use, for example China new economy, which offers growth but also at a much lower correlation compared to broader market. And technology, so we have promoted AI, robotics and other trends through an Asia innovation fund, or perhaps frontier markets such as Vietnam, which offers growth while most other economies move into recession. As product developers, we identify the gap in the market, and then we try to provide a suitable offering for the DPM manager to use and also other institutional investors.”

Expert Opinion – David Lai, Partner, Co-Chief Investment Officer, Premia Partners: “DPM managers start to see ETFs offer more than a simple beta and would be a better option versus active mutual funds. For example, our Premia China New Economy ETF does not only outperform most mainstream index trackers say A50 or CSI300 year-to-date, but also beat more than 75% of China active funds by ranking in the first quartile.

Diversification and risk assessment

“We think asset allocation actually is very different from the traditional mean values framework where you are effectively trapped by this impossibility to go beyond 1% or 2% of investment rates, and no leverage,” said another banker. “As long as you get rid of that constraint, you can afford to think about a different way of constructing portfolio and this is our philosophy. We build portfolios not based on return expectation, but based on their risks, on risk allocation. And then we try to have a portfolio which is diversified enough, with much less risk allocated to pure equity risk, for instance, and then what is at stake for us is just to achieve a positive return, even if it's modest, because after we can use leverage to achieve the level of risk we want to target.”

He observed that what people tend to forget is that from a historical perspective, today we are at a very, very low point in terms of return expectations. “This downward trend in returns has come with a downward trend in volatility, actually,” he reported, “although of course not this year. However, for some years volatility has been compressed by the policies from central banks, and there is no reason to believe that going forward with lower and lower returns and very low yields, we will not have also the return to low volatility, because this is what is at stake for central banks.” The result is that lower returns from a well-diversified portfolio can be enhanced by the application of sensible leverage to produce enhanced returns, and to achieve this, the bank follow a highly systematic risk assessment process.

“Over time,” he explained, “you need discipline to keep your overall level of risk as stable and as aligned as possible with your own risk profile. This is the overall philosophy.”

Knowing the client’s goals

A slightly different view came from another expert who espoused the merits of goals-based investing as the cornerstone of the whole journey. “And we emphasise to clients that DPM is a service, not a product, and we can adapt the asset allocation along the way, while taking the long-term perspective.” He explained that the bank offers different, tailor-made building blocks for DPM, including fixed income strategies, new economy offerings, strategies focusing on mega-trends, dividends and regions. He explained that with this choice of building blocks, the clients can choose different types of investment style within their DPM mandates. “Doing so,” he reported, “over a long period of time, we have achieved a very superior risk-adjusted return.”

DPM as a service

“Agreed, said another expert, “this should not be sold as a product. The RMs should be talking to their client about their needs, their risk profile, their tolerance, their asset-liability matching, their goals, and then match them to the portfolio that fits. You are not selling them a product; you are selling them the asset allocation process.”

A banker explained that their approach was the core and satellite portfolios, allowing for liability-driven investments that should remain more liquid for future obligations and longer-term less liquid assets for long-term gains, but eschewing short-term liquidity, as a quid pro quo.

The approach is based on suitability and directed by both goals and risk management, with DPM basically the core centre with strategic asset allocation with leverage to enhance returns where appropriate, and then the satellite approach driven by tactical asset allocation.

Another guest noted that DPM mandates must still offer the client the opportunity if required to liquidate and therefore many of the illiquid assets are not suitable, such as venture capital, private equity or CLO funds. “But we have put some structured products in to create a symmetrical return during a certain market performance and for protection purposes as well,” he said.

Audience Perspectives

Hubbis sent out a post-event survey to attendees of the discussion, asking them for their views on the evolution of DPM in Asia and what needs to take place for the market to move ahead more dynamically in the coming years. We have selected the following insights from their replies to our three key questions, which were:

What specific efforts is your bank/firm making to convert more HNW and UHNW clients to DPM and advisory?

Is your bank/firm succeeding in converting a greater number of HNW and UHNW clients to DPM?

What do you consider the outlook for DPM adoption in the region in the foreseeable future?

The Audience Comments:

- We need to prove to the clients that we, as firm, are able to give them better performance and asset growth/capital gain. DPM is a service, not a product. Therefore, we can make it 'tailor made' for bigger client accounts. We must ensure the firm has a good front manager platform, convinced of the DPM advantages for both the firm and for the client, who must receive a real value proposition.

- Our bank is definitely making efforts to convert more HNW and UHNW to DPM but over in this part of the world, it is still a challenge getting Asian HNWIs to convert and accept the fact that they have to pay a fee but we are making small progress over time.

- We are already 100% DPM.

- We must drive the RM scorecard towards a sizeable weighting of managed solutions (discretionary & advisory mandates) in order to align to the bank's increasing strategic focus/emphasis on recurring revenue on top of transactional revenue.

- We need greater engagement to explain the need for advisory services to tap into our investment specialists knowledge and research.

- We want to have more conversations with clients on alignment of interest.

- We should encourage RMs to have more confidence in selling the benefits of DPM. Generally, the longer-term the relationship with clients, the better the uptake of DPM.

- We are an EAM with highly professional and experienced private bankers from global private banks and hence we are expert at converting their clients to DPM. Private banks may convince clients to trade more, as this will generate banks more revenue for them, but the trading may not really help in clients’ portfolio growth. Our focus is much more on achieving clients’ investment targets (portfolio growth) as our revenue is not driven by and does not rely on trading activity.

- We need to see more training of the RM to introduce and convey the advantages of DPM. We need to educating clients on the long-term benefits of the DPM model.

- The outlook for DPM and advisory is one of growth. For the WM businesses, it is an important service to their long-term survival because it provides more stable annuity income. It also lessens the regulatory burden for the WM business as the regulatory requirements are less onerous for a DPM mandate than for a transactional trading account. From the client side, more of them are appreciating that the DPM service is a sensible home for the core element of their wealth balance sheet, being professionally and actively managed, allowing the client to make more tactical trades with the satellite element of their wealth.

- We are still far from the level of DPM we want to achieve, and need to push this mandate harder. Asian clients need to build trust and want to have say over certain investment decisions

- Yes, we are very good at what we do and achieving what we set out to achieve.

- More and more clients realise that the banks may not put their portfolio growth as their first priority because more trades generate more revenue for them. Clients are more likely to choose an EAM for discretionary portfolio management as the EAM concept stands for the same goals and targets as the clients - portfolio growth generate more management fees and/or performance fees.

- We are slowly seeing some progress as clients see the benefits of the DPM model.

- Slowly, as Asian clients are still uncomfortable of giving up full control of their portfolio.

- We are making most progress with non-Asian clients who have a better understanding of the merits of DPM.

- DPM is positioned as a core offering for our clients. They are directing more clients into DPM because of the reassurance it brings to clients in that a core element of their wealth is being actively and professionally managed.

- More and more families/ clients are willing to take a DPM mandate for part of their assets, especially if they don’t have time to invest/knowledge of the markets. They see the DPM investment as a long-term investment, while their trading account is more focused on the short-term investments.

- Clients are beginning to open up to this, but a lot more engagement is needed to make them truly understand the benefits of DPM and how it can help their overall investment portfolio and to complement their self-directed portfolio activities.

- I think DPM will win more acceptance from Asian clients as they gradually prefer simpler mandates to grow their wealth.

- The outlook is bright, albeit from a low base. Clients are finally beginning to see the value of the offering.

- As some of the panel speakers mentioned, we are getting a bit more traction, and there are tremendous opportunities.

- We see increasing client interest and traction seen across both HNW and UHNW segments, particularly so in the areas of ESG, sustainable or impact investing.

- There is potential grow of DPM and advisory amongst Asian HNW. It will be growing as clients are increasingly looking for professionals to manage their funds while they concentrate on their business/other aspects of life.

- It’s appealing as markets have been rather volatile. It is good to be nimble while still having the long-term objective in mind.

- We see this as generally positive as clients realise the need for asset diversification which DPM can provide.

- The outlook is encouraging and improving as clients prefer the risk management and well diversified approach.

- More HNW and UHNW clients consider DPM in Asia as they start better understanding how DPM service can help their portfolio achieve long term growth. Better decision and advice is indeed needed for their asset allocation and investment.

- There are very good prospects, but progress is being greatly slowed by financial illiteracy. The outlook is therefore positive, although the client mentality does take time to change.

- DPM is still in its infancy, yet with significant potential. A broader understanding of why DPM is better than chasing rates of returns in the general population is not yet commonplace in HNW/UHNW clients, so we as an industry must work hard to improve and deliver the message.

ESG rules

The moderator asked to what extent ESG was being incorporated in regional DPM offerings. “We are certainly getting more and more queries about ESG,” replied a guest, “but you must select valid instruments.” He estimated about 130 funds globally that call themselves fixed income ESG, but very few that are truly ESG, adding that ESG is also extremely difficult to define at this point. “We really don’t have th tools to be able to determine what is truly ESG, at this point,” he said.

“We have been heavily into ESG for many years,” came another voice, “but we enter into this with a fully integrated approach we call sustainable investing, where we analyse both the sustainability of business practices and business models and also the compatibility of what the companies are doing in practice. We therefore prefer to speak about sustainability rather than ESG, investing in the companies that are truly aligned with some core key sustainability criteria which we believe are relevant for the long run, and that we believe will become more and more rewarded by the market. The environment will have a huge price in the future, and we have already seen this in the market.”

Audience Perspectives

In our Hubbis post-event survey to attendees of the discussion, we also asked them if DPM is winning more mass affluent clients and why or why not?

The Audience Comments:

- The DPM mandate allows smaller clients to be managed and diversified at the same time. This can be done through a fund (DPM) managed by the FI and where smaller investors can take part of it by buying units of the fund rather than invest directly in the product/shares/bonds.

- No. Most clients still prefer to be able to select their own investments.

- Yes, one at a time from our perspective.

- In my opinion, DPM is more suitable for HNW clients due to its minimum initial investment requirement.

- No, due to the larger investment amount to start.

- Not really, as there are not enough fees for companies from small DPM mandates.

- Yes, because they are increasingly informed of the merits of DPM, and DPM does not strictly need to have an exceedingly high entry points in terms of funds.

- Yes. Usually these types of clients are younger and more receptive.

- Mass affluent clients are probably better suited to a DPM service, and I think this is the biggest area for growth, due to the fact that they can outsource the mandate to a professional service that works for them (the client), as opposed to someone paid by or working for the investment platform or fund managers themselves.

- At the moment not yet, because the understanding in Asia is not there yet.

- Yes, but only with banks with good research and advisory teams, where the clients feel informed and safe.

- The ability of DPM managers to bring the cost down of such a portfolio through the use of, for example, ETFs makes the service more accessible for the mass affluent market. In addition, a DPM mandate can be a portfolio of funds whereas where direct holdings are involved, a minimum mandate size is required from a risk perspective usually beyond the investable wealth of the mass affluent.

Going digital

The final comments were centred on the use of digital for DPM expansion, with a banker noting their DPM app that allows RMs to construct a certain portfolio and generate a proposal based on future market simulations and various stress environment. He explained the RMs and clients can then see how returns and risks look over many years ahead against different scenarios.

Conclusion

DPM as a proposition is remarkably sound, but it stands or falls in the world ahead on the banks, the EAMs and the bankers who work for them truly embracing the concept and adapting their business models and even remuneration to help build out the proposition. DPM is a service, it is not a product, it is all about asset allocation and working with the clients to adopt the right strategies to cater for their shorter-term or unexpected needs and their longer-term goals. Older asset allocation models do not work as they used to in the current environment, new strategies and unique propositions are required to build return in a world where returns from all asset classes are dwindling. Asia’s wealthy investors have historically been somewhat reluctant to give up control of their investment portfolios and pay someone for doing so, but this is changing, gradually even if somewhat slowly.