Publications & Thought Leadership

The Dawn of a New Era: The Implications for Digital Technology & Solutions in Wealth Management

Jun 9, 2020

To what extent has the global pandemic accelerated the need for digital solutions in the world of wealth management, and to what extent this would have occurred in any case, albeit over a somewhat more extended timetable? A fascinating discussion unfurled on June 4 in the latest edition of the Hubbis Digital Dialogue Series, which brought together four eminent speakers to offer their insights into the digitalisation of wealth management. They explored not only what must happen, but also what might happen, with a particular focus on the UHNW and HNW segments, and also due attention to the source of tomorrow’s wealth, the mass-affluent space. Right from the initial contact with a prospective client through KYC and onboarding, and all the way through all the different stages and elements of the client lifecycle, digital solutions have been revolutionising the client’s interface with their banks and advisors, with the goals of enhanced differentiation and value creation. Where precisely along this chain will digital solutions be in even greater demand in the months and years ahead? What does all this mean for the workplace we knew before and the work methodologies of the future? What will all this mean for the relationship manager of tomorrow? And as to the providers themselves, how will they need to adapt their planning and investment to cope with this potentially new environment? Can they embrace digitalisation to their core for a radical transformation that will future-proof them for the world ahead? These and many other questions were debated at length during the one-hour discussion, and the outcome supplemented by the Hubbis audience survey.

Why Digitalisation is Essential

Take 6: Six Pointers to the Road Ahead

- Margins for the WM community, even before the pandemic, were squeezed, and likely to be even more so

- Cost-income ratios have been too high for too long

- Digital or digitally enhanced competitors are on the rise

- Customers are more likely to shift providers or move assets than ever before

- The second and third generations of private wealth are more digital than ever before

- Digital adoption will drive customer acquisition, integration and retention

Irrespective of market conditions, one expert began, everyone in the wealth management (WM) industry in recent years has experienced pressure on cost-income ratios, and with the pandemic, these challenges have become exacerbated.

Leveraging digital

“Most, if not all, WM firms have far too high cost in a market where margins will continue to be squeezed, and digital propositions eat into their space,” this expect opined. “This is true even for upper tiers of wealth, not just retail and mass affluent, so the question is how firms can best address their cost problems by leveraging digital, analytics and technology, and help derive insights to drive personalisation and relevance. What must they focus on, what drives ROI, and how can these firms drive adoption by RMs and by clients? These are all vital questions to address.”

The mission for the wealth management (WM) industry must, therefore, be to focus on the key trends and needs and define where they want to invest and where they should focus most of their money and effort.

Step by step

“You cannot renovate the whole edifice at one shot,” they said, “so the key is to make the vital shifts that achieve differentiation. If everyone does the same, that still doesn’t help to take market share or maintain and even improve profitability, in particular given that there will be a constant flow of new entrants, including technology firms, businesses entering from other regions, digital banks, and others. So how can a private bank or other wealth manager get their differentiation right while moving towards digital?”

Another expert highlighted how banks are struggling to meet the demands of the rapidly growing mass affluent population of Asia, which is clearly a large market for the WM community to target. He explained that most of the banks he speaks to are saying they are hampered by legacy IT systems, making it especially difficult to tap into newer growth markets such as Indonesia, Philippines, Thailand, and Vietnam. Everybody sees that opportunity, he noted, but then it is a question of how to enter into those markets at an acceptable cost and with the likelihood of success.

But see the big picture

Step by step does not mean that banks and other WM providers can lose sight of the big picture. A guest noted that during the lockdown, there had been even greater interest in digital solutions, but the vendors must deliver value, to achieve solutions that truly feed through to the bottom line for WM firms. He explained that there needs to be a wide-angle picture formed of the wealth industry end-to-end.

“One of the big questions at the moment,” he said, “is client acquisition from the home office, then onboarding remotely, something we have been talking about for years. And for revenue models, clearly advisory has been a focus area for a considerable time, as recurring revenues are even more in focus now. Digital can truly help, but we must focus laser-like on where the value is going to be driven, and where the profit pools are. And perhaps the biggest question right now is what does profitable wealth management look like post-pandemic.”

Purer digitalisation needed

A guest commented on how many conversations there are on what the new normal will be post-lockdown, but we need to do more than simply muddled through collectively. Financial institutions have got through so far on skeleton staffing in offices, but a truer form of pure digitalisation will in the future be needed, whatever the world looks like post-virus.

He said his particular story in front of clients is unlikely to change that much, apart from slight nuances to the software, and moreover, the working patterns of the financial institutions in WM are also unlikely to change that much, as people like working in offices and also private wealth clients like face to face, no more so than in Asia. He concluded the new normal perhaps wouldn’t be quite as revolutionary as some commentators indicate.

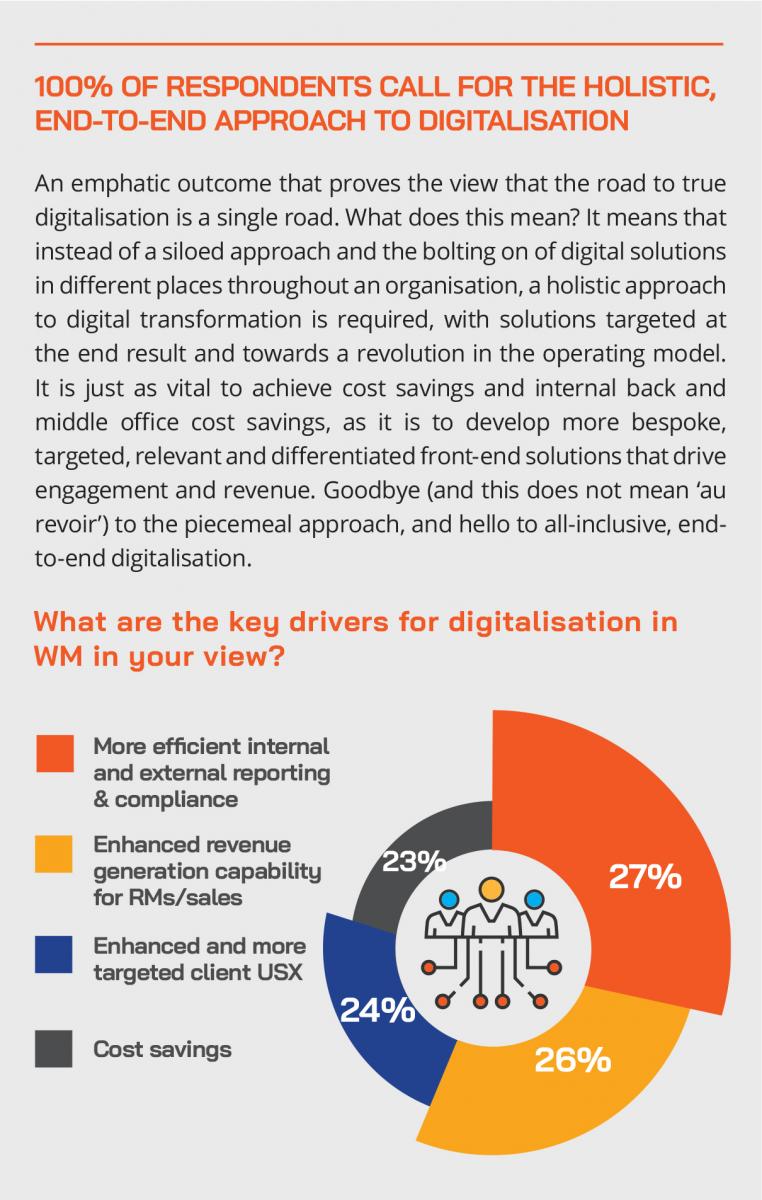

Hubbis Audience Survey Question: Given the need for the WM community to achieve cost-reduction, revenue expansion and a better USX, exactly where within your organisations will digital be most essential and most effective?

Selected Audience Comments:

“In my point of view, it will be in lots of different areas may it be front, middle and back-office. This pandemic has forced every organisation to adopt a digital approach, and maybe costly for some who are just developing their digital capabilities and/or just adapting to it. But in the long run, it may prove to be more cost-efficient as technology can streamline processes, eliminate the needs for costly office space, and produce many more advantages.”

“I believe the whole spectrum of my working organisation has to be involved.”

“Digital will be most essential in both internal and external areas. Internally to reduce manual operations and speed up processes, externally to enable clients to have access to basic tools such as viewing their portfolio positions. It is a surprising reality that clients, at times, don't have access to such basic functions on the digital platforms offered by financial institutions.”

“For a digital transformation to succeed, the required characteristics fall into five categories: leadership, capability building, empowering workers, upgrading tools, and communications. Any transformation is hard, but for a digital one, it is even harder, and all five categories must work together to succeed as a whole and not where within an organisation.”

“I think all areas in each organisation need digitalisation. Digital technology is needed for services platforms that are integrated with banking solutions to manage their non-core activities, including bookkeeping, payroll, procurement and HR, allowing them to focus on their core business. Additionally, digital will help focus on target customers to achieve enhanced customer experiences. Digitalisation can also make use of data analytics, AI and intelligent automation to improve and accelerate lending decisions and to flag up suspicious transactions much more reliably.”

“As a solutions provider, I would say it needs to be end to end. Outsource what is non-core to providers who are reputable and successful, so that private banks/wealth managers can focus on their core business, client acquisition and wealth management.”

“People tend to focus on the areas that directly increase revenues, such as onboarding, trading and so forth, but in reality access to data and the delivery of meaningful interactions with customer and RMs will have the biggest impact across the board.

“It seems digitalisation will be most useful for our sales team, which is in charge of client interactions. It may seem superficial, but transforming the entire experience into virtual effectively reduces the expenditure of not only capital but time as well. For example, gone are the days that require individuals to traverse the city to go from meeting to meeting for clients and colleagues alike. The majority of interactions can now happen from home or at the office via social media, video chat, phone conversations, which are far more efficient and less costly than entertaining at restaurants, bars, clubs, and so forth. Moreover, this can allow for a vast reduction in transportation costs.”

Achieving the goals

Take 6: Six Pointers to the Road Ahead

- The digital transformation journey must be better planned and more effectively executed

- Step-by-step digital enhancements must be aligned with a big picture vision of digital transformation

- There must be a laser-guided focus on the end client and the target markets

- Investment must attain the desired results, ROI must be projected at the outset, and then measured in reality

- Outsourcing for all but the very biggest FIs is more likely to yield the best digitalisation outcomes

- Technology providers must improve how they convey the proposition and work better with clients on implementation

Seamless execution vital

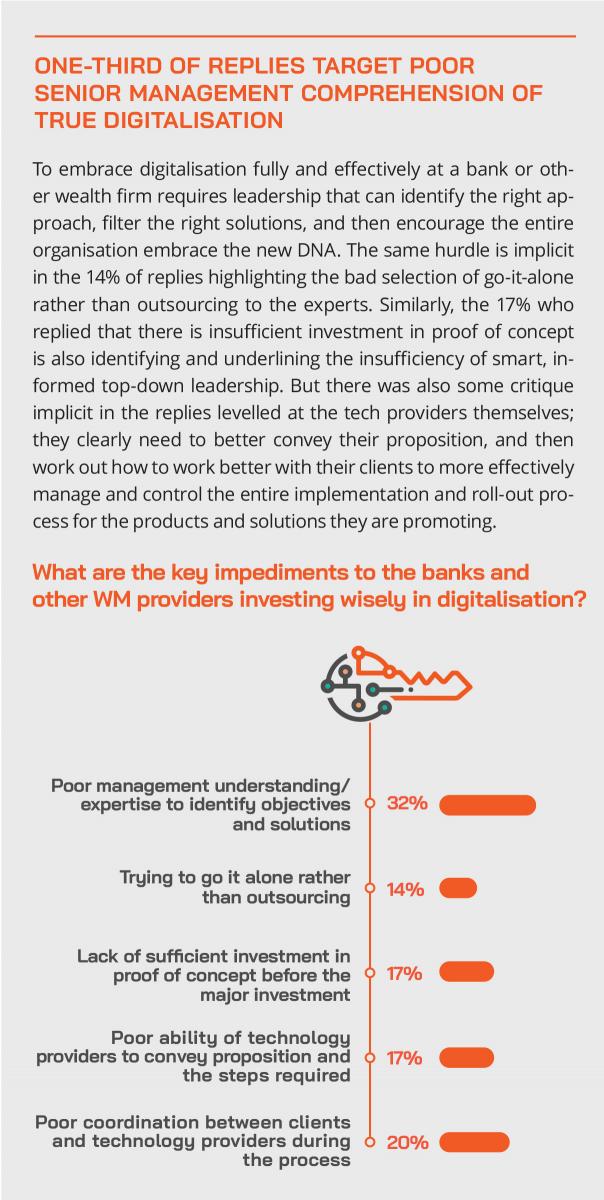

An expert commented that in reality to date, there is still a disconnect between the upfront planning around the return on investment on digital transformation programmes, and the final ROI, with execution hampering many of these projects.

There are the usual questions about where to focus digital efforts “Many banks want to do digital without understanding they really need to be digital,” he said. “A lot of the banking projects that we have seen in the past were very waterfall, but clearly we are now in an agile world, and we need everyone on the same bus at the same time and sprint to the line. The value disruption has often occurred because we haven’t had the guidance, the clear vision upfront, and in some cases, we haven’t really understood some of the nuances of actually executing in the local countries.”

He added that banks don’t really want to pay for proof of concept in this environment, but that it is essential. “Unless there is absolute clarity at the start and throughout the process, many projects will fail,” he stated. “Being nimble is essential for translating things to operational reality.”

A fellow panellist concurred, adding that the digital adoption taking place as a key trend in recent years is now a digital necessity and that all change must be viewed through the prism of the client, the end customer. They said that WM firms could see what is needed, whether it is for transacting, interaction, enhancing the RMs’ capabilities and productivity with AI and analytics, but it is vital not to get bogged down in administrative issues; it is essential to continually focus on the end customer, and even to work on co-creation of solutions with the RMs themselves, as it is they who must deliver to their clients.

Client-Centricity, Relevance & Differentiation

Take 6: Six Pointers to the Road Ahead

- Never lose sight of the end-client, in fact the client must be the focal point of all digitalisation

- The RM is a vital key, especially for the upper echelons of wealth, so empower them to achieve more

- Growth is needed ahead, so KYM – Know Your Market – and target digitalisation to those markets

- Shiny and new is fine, but this is not a PR exercise - deliver accessibility, relevance and differentiation

- The personal touch is likely to remain highly valued by HNWIs and super-wealthy, so focus on hybrid solutions

- Follow the leaders – there are some banks in Asia and globally which have set the bar very high – look and learn

Another panellist agreed, adding that in a project he had worked on a few years ago, it became obvious that the client had lost sight completely of their end customers. “Internally,” he commented, “we often get very focused on the RM enablement and on what the management needs, but customer-centricity is key to it all.”

Laser-guided

And an expert said that taking this view further, he has seen shiny new front-end apps that give the clients more user portfolio construction and management options, bells and whistles than the RM sitting back on the desk. He argued, therefore, that there must be a greater connect between clients and the forward-facing advisors and RMs who serve them. “In the past couple of years there has been a lot of focus on either one,” he said, “but it really is the whole journey now, both RM and client go hand in hand.”

A guest then addressed issues surrounding digital delivery. This, they said, for building into new markets and building market share is about a variety of objectives. These might include making sure there is an enhanced USX, aiming for transparency, opening up extended sales service channels for the clients to access any time, understanding who the partners are WM firms can work within their markets, understanding the evolution of new players in the market, how to make APIs available, and how to source and deliver the best data analytics. A fellow panellist agreed, adding that AI and data analytics as tools to achieve relevance are increasingly important.

Hubbis Audience Survey Question: What does client-centric mean to you when it comes to digital solutions in WM?

Selected Audience Comments:

“To fulfil clients’ requests as much as possible, that is, to enhance the USX by developing digital solution as per client requests and expectations. The solutions should be designed for the client, not for our convenience.”

“Putting customer experience at the forefront of any digital technology developments.”

“Building digital solutions aligned to the crucial needs of clients across the wealth continuum. Really being able to identify what clients want and need and to build solutions based on this.”

“The customer is firmly in the driving seat and with it comes a required change in how you build and nurture relationships with potential and existing customers. A customer-centric way of doing business is a way that provides a positive customer experience before and after the sale in order to drive repeat business, enhance customer loyalty and improve business growth.”

“Whatever sector they are in businesses are embracing digital transformation, implementing new technologies and ways of working in a bid to differentiate against increasing competition and to get ahead of rivals. The customer experience is the most crucial. Customers want the ability to switch between channels during their journey. They might start online, move to email and finally to give instructions digitally online. Accordingly, simply focusing on the digital parts of the interaction in isolation doesn’t deliver the required levels of integration.”

“Delivering what the customer wants when they want it - and it must be personalised. There is no point just looking on improved internal efficiencies unless this drips down to tangible improvements for the end customer.”

“Re-engineer business processes and turn the focus (currently inward to outward) to then be from the client perspective of needs first, in other words outward to inward. That will truly change the way we service our clients. A lot of current business processes are entrenched and attempts to change to adapt to new reality and competition an uphill battle because change management is not driven by individuals but by project managers or coordinators. Once we sort this out, client-centricity will naturally fall into place.”

“It is a business strategy that's based on putting your customer first, and at the core of your business in order to provide a positive experience and build long-term relationships and in terms of digital solutions in WM, we have to establish a truly ‘digital-native’ culture within the bank or industry. We have to offer a broad range of user-built digital solutions for various clients, to relook at how things were done traditionally and how things are being done now with the current situation. Perhaps one day, perhaps soon, physical offices will be a thing of a past with everyone embracing and utilising technology effectively and efficiently.”

“Client-centricity equates to accessibility. In an increasingly digitalised/virtual era, WM firms need to always remind clients of their existence. In these times, it is crucial to take advantage of technologies such as Zoom and others to reach out to clients and address any concerns they may have. It has been a common theme across these webinars that WM firms are unfamiliar with what clients genuinely need and want. These times, in particular, are when clients need assistance with figuring out their next move as well as resolving ad-hoc problems and concerns, and so forth. Being able to demonstrate availability and readiness during the pandemic should allow companies to stand out amongst peers and become the clients' first choice.”

KYM – Know Your Market

A colleague agreed that it all starts with a rigorous analysis of which markets a bank or firm operates in, competes effectively in, which clients do they target, what products or services can they best offer and achieve profitability with, how can they differentiate themselves, and then how do they invest in tech to deliver. “In short,” they advised, “focus on the operating model and technology for automation, that is the vital combination.”

Players in the industry, as they expand into different markets or even countries, need to leverage some of the network effects that are out there in the market, for example, the super apps, said another speaker, as well as replace some of the other ecosystem partners such as product providers, and then, of course, make sure that they are fully automated and completely omnichannel.

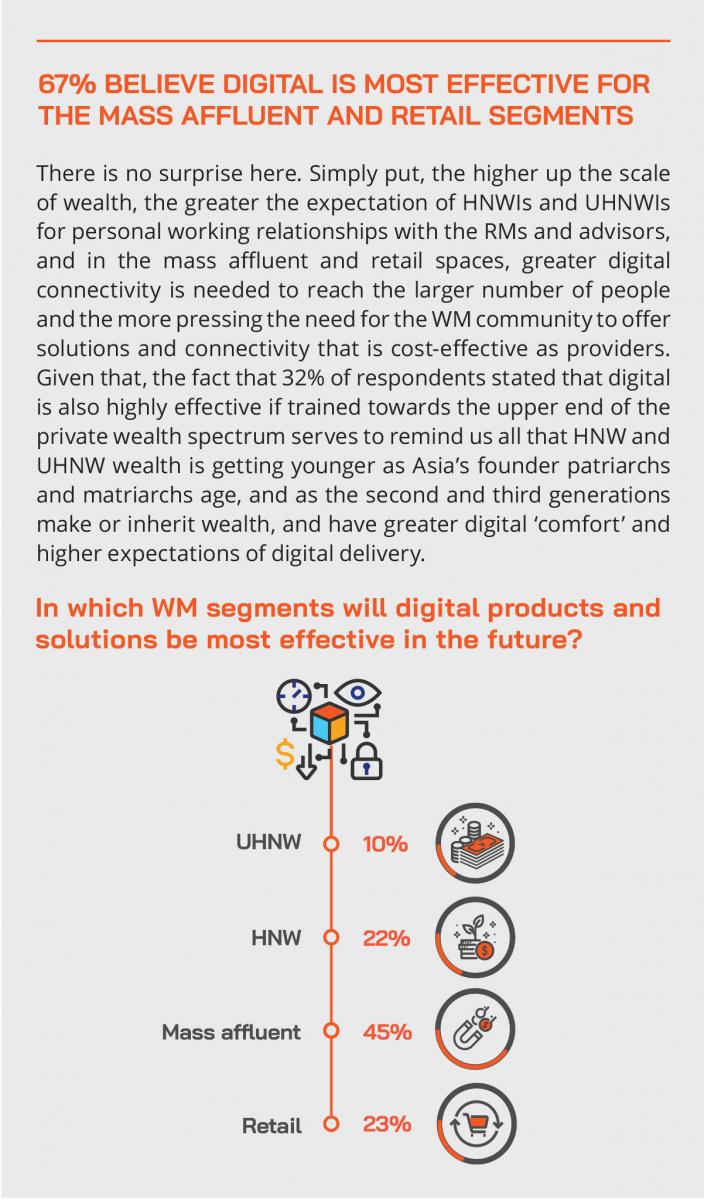

“There are different challenges in each of the target market segments,” said another guest, “so again it comes back to understanding the target customers, whether UHNW, HNW, or mass affluent. The higher you move up the spectrum of wealth, the more human involvement you require, for example, but while there are clearly differences in all segments and areas of the offering, there is a valid digital element in all of those areas.”

Hybrid and omnichannel

He added that the pandemic has proven that the world does not end if providers can’t meet clients face to face, and digital adoption is higher within and outside the firms as RMs and clients need to see positions and digital can help that and has been actually proving beneficial to these relationships. WM operators therefore really need to think about how the omnichannel solutions that digital and human married together provide, and appreciate that the human element needs to be focussed on the higher value services where there is hyper-personalisation, and then service each segment of wealth with laser-like precision.

“I totally agree,” came another opinion, “I really do believe digital is relevant across all the different segments. But it's relevant in different ways. We see a lot of technology silos inside of firms, for example historically a lot of focus on core banking and portfolio management systems, then a more recent focus on digital onboarding, but in reality, marrying everything up internally is still rather a horror show in most organisations.”

Agility essential

He added that as the market evolves, the industry is still in danger of homogenisation. “When it comes to client service,” he said, “having a great app in the mass-affluent segment, for example, is becoming a hygiene factor for these financial institutions. I hope that when we fast forward five years ahead and look inside these institutions, a lot of the technology innovation, marrying up the end-to-end client lifecycle, has moved on leaps and bounds. So, the industry has to keep on innovating externally or internally facing because the competitive advantage between these firms is so narrow right now, especially with entrants coming in from outside the financial industry, firms that are very nimble and very technology savvy, both client-facing and internally.”

A slightly different perspective came from a specialist who said that UHNW clients do not always want a high personal touch. They said Big Tech firms are shaping experiences, and there is ever greater demand for optimal digital experiences. “I think it's a bit of misconception that they want that extra white glove high touch,” they commented. “Yes, they might want that, but they also want to get a great digital experience. One of the biggest complaints of clients I heard was when they got moved up the spectrum, e.g. from mass affluent to HNW, or HNW to UHNW; their experience got worse. So, if you believe in the wealth continuum and bringing your clients up that curve, you have to have the same capabilities throughout. So, yes, there will be differences throughout, as digital utterly dominates lower down the wealth ladder, but UHNW clients should also have the best digital interface as well as the best personal connections.”

Follow the leaders

The same expert added that there remains complacency about new entrants and competitions, noting that more and more well-to-do people, those who might not be pure private banking clients in terms of wealth, will go for digital advisory and digital portfolio solutions on offer. The banks that offer the best such solutions will best compete and thrive, they concluded. The incumbents, therefore, need to adopt digital as a mantra throughout their organisations, truly push the boundaries and not be complacent. The result will be the ability to truly compete and achieve profitability across all the wealth segments.

DBS was cited as the market-leading exponent of such digital transformation, with the experts agreeing that the bank’s approach from the top-down and throughout every nook and cranny of the organisation and its DNA was winning both plaudits and clients. “It is really a fantastic example, a great case study of where they have invested in technology front and back, and achieved a snowball effect,” said one speaker. “The more investment that is going into both of those angles, the more financial rewards they are reaping year on year, and indeed the further ahead they are getting of competitors.”

But he also noted that their competitor banks, those in tiers below DBS, tend to approach digital transformation more piecemeal, as sort of a chance of patting themselves on the back for launching some shiny new app to shout about in the press, but not truly working out how to achieve digital transformation, or even convert clients to use such apps and solutions. “So often you look inside such as institution and it is a mess.”

Watch out, your customers might be taken!

The discussion shifted to customer portability, with an expert noting that analysis his firm had conducted has highlighted how the propensity to switch banks right now is remarkably high.

“We are seeing, particularly across the Asia-Pacific markets, that about 30% of clients are willing to switch [banks] over the next three years, which is far greater than we saw in the previous three years,” he said, “so this comes back to the crucial importance of differentiation.”

Relevance, relevance…and more relevance

To address these trends, he advised that banks can for example leverage data analytics to give a heads up if a customer is likely to leave the bank, they can start to look at the behaviour to see is that client slowing moving some assets away, or if they are trading less than normal, or if the RM has not called them, or vice versa. “These are fairly simple measures, but vitally important,” he said.

He also addressed relevence, noting that it is not enough to simply communicate regularly through all sorts of channels, but to dig down into the behaviour and history of the clients, then offer them relevance, for example in the form of research on sectors or markets or countries those investors actually like in the past, rather than offering research on, for example, the car industry, to an investor who is into science and tech. “Yes, we want to deliver the latest and best ideas and information and insights,” he said, “but it must be relevant.”

He expanded on this thought, remarking that a key value-added area for the WM community is advisory. “We have seen a substantial increase of assets in this region moving into DPM and customised mandates over the last few years,” he said, “but they also need to deliver relevant discussions on risk and portfolio construction, using data analytics and AI, but making these part of your core; the best banks today are leveraging digital through the firm, they have an understanding from a terminology and from a cultural perspective on how to drive change and adopt.”

Empowering the client-facing experts

Another panel member agreed wholeheartedly, adding that RMs must be empowered with the right tools, and a wider range of tools. These might include delivering alerts, content, portfolio alerts, product ideas, in short empowering the RMs to boost their relevance to the clients, and to monitor their activity and behaviour, right down to the mass affluent levels as well.

“This does not need to be rocket science,” he said, “it can simply be prompts and alerts, but entirely relevant to those clients. This dynamic makes relationships stronger, and potentially more profitable. I do think we are now at a fundamental turning point now, especially post-pandemic, where a lot more financial institutions are embracing this digital transformation era, and thinking the right way.”

Look to the future

The discussion drew to a close with the panel gazing into their crystal balls. “Remote advisory is the future,” said one guest. The WM community needs to be able to really offer the best advisory to remote clients, wherever they are, without necessarily the need to travel to meet them. For example, there are numerous wealthy people across countries as huge as Indonesia, and they need to be served with the best apps, the best analytics, the most relevant and tailored ideas.

Look at the major global banks and investment banks, for example, the same expert said, who are wondering right now what the future trading room might look like. However, these same banks have handled immense volatility and activity from their home offices. “Wealth management is not that much different,” they observed. “There will always people that want that personal interaction, but honestly they are generally older, and the next generations of clients, me for example, don’t really want to talk to anyone, I am really busy, and then want a digital interaction and highly efficient and relevant advice and ideas, so I can make my money work. Digital is what more and more people will want.”

A differentiated future

The final word went to an expert who called for increased agility. “If you think about it,” he observed, “we have achieved a massive amount more in the last few weeks than we have achieved in the last few years when it comes to actual agile working and adoption. We have all shown that we can change, that we don’t have to meet face to face, we have shown that it is possible to do things differently. Hopefully that mindset will continue to an ever-greater focus on digitalisation and digital transformation, while at the same time we will all pay a lot more attention to the customer and to be differentiated and relevant going forward.”

Hubbis: Has this pandemic in any way changed the trajectory of digital technology and solutions for the wealth management industry?

Audience Comments:

“No, the value brought about by face to face interaction cannot be replaced by digital solutions.”

“Yes, the traditional customer servicing and sales effort mainly rely on face to face interaction

with clients, but now we have to more rely on the digital marketing channel and digital online

client servicing channel to perform these functions.”

“Definitely. With the expectation that such pandemics may become more frequent, the WM

industry, in particular, the bigger FIs will rush into enhancing digital solutions to enhance, but not replace, the Relationship Managers to better handle their clients.”

“Yes, the Covid-19 pandemic has sparked dramatic changes to the WM industry, making clients more cautious, more digitally savvy and even more interested in sustainable investments and ESG.”

“A split decision. Yes, as technology nowadays is improving a lot. Employees can meet their clients anytime, anywhere online, so this saves transportation time, and it makes everything easier, especially when clients are in a different country. No, as there are always employees that like meeting their clients face-to-face. And in order to use these technologies effectively, RMs and clients both need to have the technological know-how. Some may find the use of new technology difficult, especially for the older generations, who may find it less convenient.”

“We are very much performing our services as seamlessly as we can, except that we cannot have that face-to-face interaction, which in wealth management is still important. I think that a personal touch makes the relationship very different. Video Conferencing helps, but it is different if we could have a meal with a client or meet up for a chat. At the end of the day, we are relationship-driven creatures. On the administrative side, I think digital technology has helped us get more things done online, and in the cloud, and we have more leeway for documentation and correspondence in this pandemic, which makes a lot of things easier.”

“Yes. The world has become more digital and has changed the way wealth management engage its clients, combining face-to-face and digital channels. Clients are also showing more awareness.”

“This pandemic has certainly hastened the deployment of digital technology for Work from Home. IT folks everywhere have had to enable staff to operate remotely as a result of the split team contingency. However, its impact on client relationship in wealth management is minimal. Relationship, the primary driver in wealth management, has to have the human touch and cannot be easily replaced by digital technology.”

“I believe it has accelerated the need for more cutting-edge technology in how clients interface with banks/private banks. Clients would expect more going forward as they are getting a taste of webinars and video presentations that would allow more convenience to those clients as they can now participate in what they want when they want, without any obligation of attending in a physical setting.”

“Yes. The wealth management industry has thrived mainly on a face-time relationship platform. The change to embrace digitalisation has already started but not as wholeheartedly across the organisational hierarchies. Clients have been more willing to go digital far earlier than the pace at which bankers and banks have been are prepared to transform. The pandemic has torn down all resistance and forced the mindset change needed for a proper digital technology culture change. This is a positive outcome of the pandemic as it forces management to rethink the whole concept of corporate working arrangements, interaction with colleagues, and also service delivery to clients.”