There have been a number of recent legal and regulatory changes in Taiwan that have impact from a wealth management perspective.

by:

Michael Wong, Partner

Andrew Lee, Tax Specialist

Baker McKenzie, Taiwan

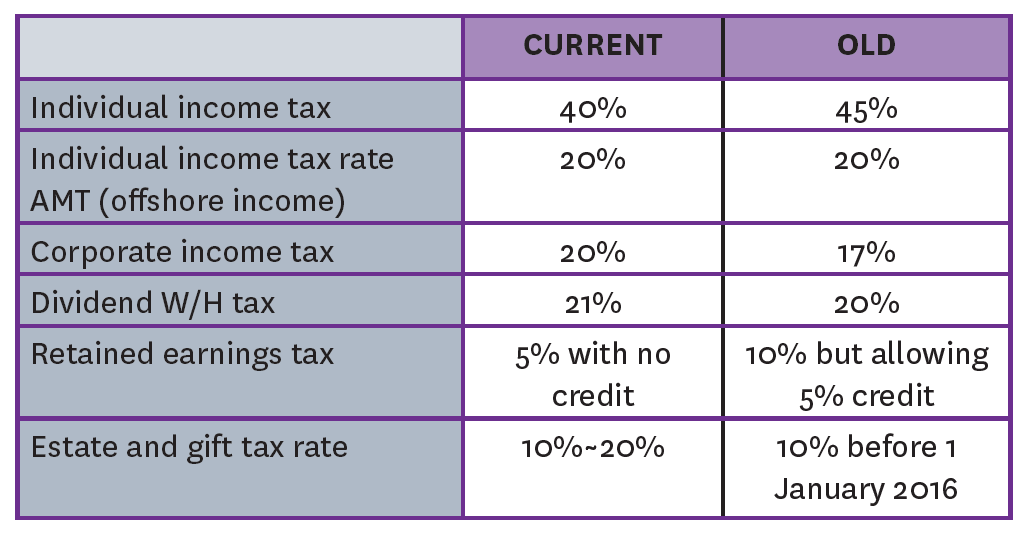

Tax Rates Changes effective 2018

Effective 1 January 2018, the new tax rates for Taiwan are:

Local foundation tax rule tightened

Effective 1 January 2018, dividend for local foundations are now subject to income tax at 20%. Prior to the amendment, dividends from shares were tax exempt for a locally registered charitable foundation.

This has been criticised for creating a loophole where large controlling shareholders of public companies have set up charitable foundations as means to retain management control within the family after the death of the major shareholders, while at the same time allowing the foundation to operate businesses (such as a public hospital) with tax free dividend income earned from the controlling block of the public company.

The background

The amendment came as a result of a public backlash against the charitable foundation set up by the founding patriarch of the Formosa Plastic Group (one of the largest business group in Taiwan controlling a number of listed entities).

The 2016 financial disclosure shows that the foundation was in control of 17 hospitals and clinics throughout Taiwan.

While the foundation reported net income from the hospitals in the amount of NTD321 million, it also received dividends of NTD11,421 million, which is about 35 times more than its “operating” net income, and all of it tax free.

New CRS regulation announced

In order to join the CRS network, targeted to be the end of 2018, Taiwan has promulgated new CRS rules that largely follow the OECD template.

Among the highlights, Taiwan financial institutions are required to diligence their customer accounts by the end of 2019 (for accounts in excess of USD 1 million) and by the end of 2020 (for smaller accounts).

New reporting will commence in June of 2020. The MOF has also announced its intention to prioritise countries who have double tax treaty with Taiwan for automatic exchange of information prior to the implementation of CRS.

These countries include about 32 countries such as Singapore, Japan, Australia, New Zealand and Canada. US and Hong Kong do not have a double tax treaty with Taiwan.

New amendment proposed for the Company Law in light of implementation of Anti-Money Laundering legislation (AML)

The government has proposed comprehensive amendments to the company law which will include the requirement of beneficial owner disclosure. As currently contemplated such information will require the disclosure of beneficial owners behind any insider (director or supervisor), manager or shareholders who hold more than 10% shares.

The information will be uploaded into a central database with the requirement of monthly update.

If implemented the amendment will apply to private companies as well as public companies registered in Taiwan.

Senior Consultant at Baker McKenzie