Publications & Thought Leadership

Singapore as the ‘go-to’ Centre for UHNW Families and Family Offices

Jul 8, 2020

As we cautiously emerge from a world changed irrevocably by the current pandemic, and as some economies begin to tentatively return to what we once considered normal, Hubbis assembled a panel of six leading experts to explore just what makes Singapore such an appealing choice for the UHNW families of Asia, and from across the globe, for their relocation and also for the establishment of their family offices. In the July 2 Hubbis Digital Dialogue, the panel members, representing top names private banking, law and consulting explored the many appeals of the city-state as a regional and global wealth management hub, as well as highlighting some areas that can still be improved. They discussed the benefits of Singapore for family offices, reviewed the government’s tax and other incentives, the regulatory framework, considered the new fund vehicles such as the recently-introduced Variable Capital Company (VCC), discussed the depth of the financial, legal, accounting, trust and other professional services, and they analysed Singapore’s appeals as a metropolis to appeal to multiple generations of discerning clients, and ultimately how competitive it is compared to other jurisdictions in Asia and around the globe.

Exclusively sponsored by Henley & Partners

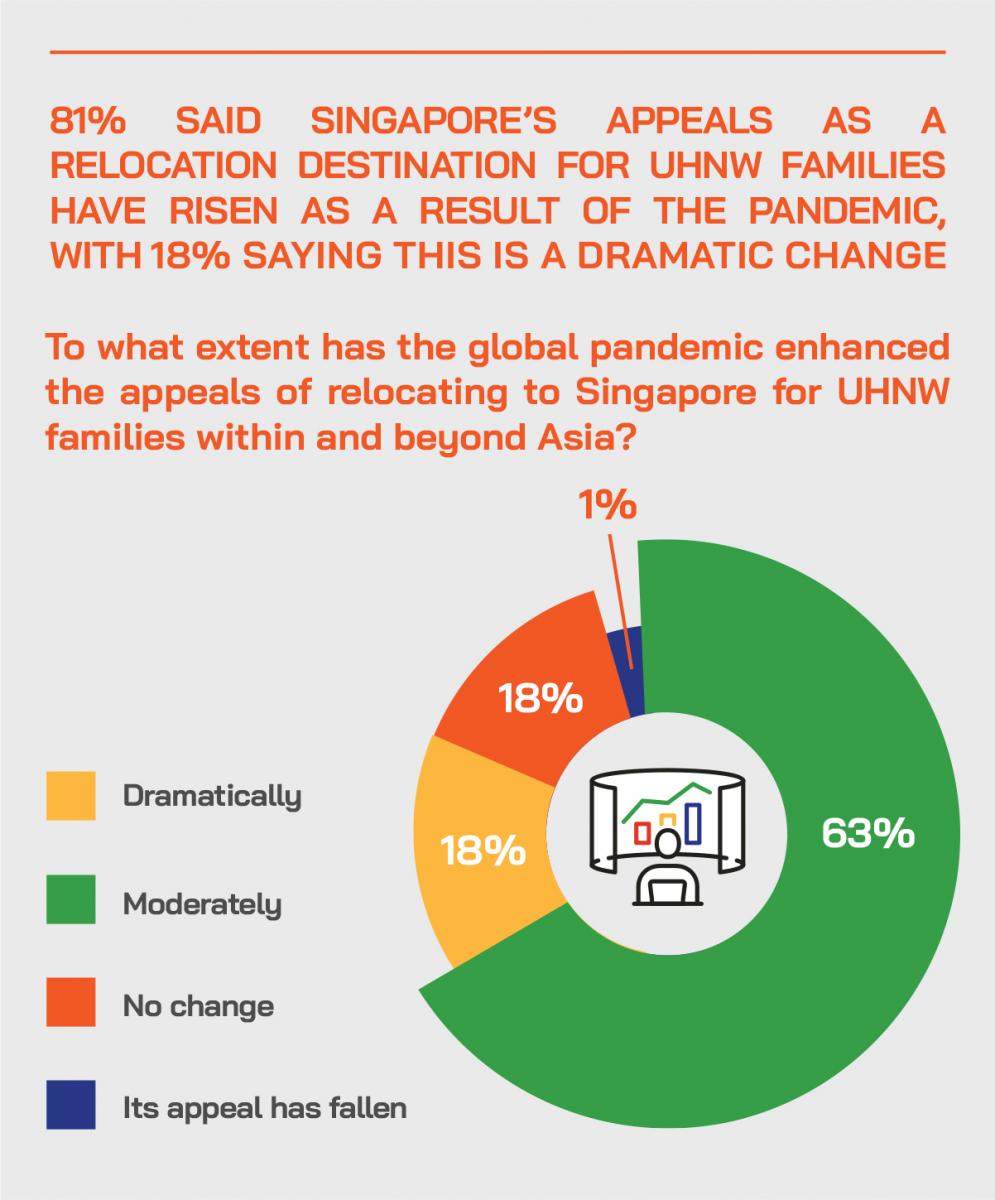

Singapore’s magnetic personality

“The fiscal perspective is the first consideration,” a panellist began. “Singapore has been ahead of the game, as we know, with a variety of tax incentives. Essentially if a fund is managed by a fund manager in Singapore, or by a family office, any capital gains are considered tax-exempt, provided they fall within certain streams, for example, any gains from trading in equities, bonds, and actually a wide range of investments. And there are so many other fiscal and lifestyle and business incentives.”

Another perspective on Singapore came from an expert who said that UHNW families look at the very big picture. “Seeing that broadest picture,” he said, “Singapore is a huge magnet as the policies, ecosystem, and operating philosophy of the whole country epitomise what I call the three ‘T’s; Tenacity, Transparency, and Trustworthiness. These macro concepts are what appeal, first and foremost, before the families look into the micro issues such as tax and other key details.”

Another expert highlighted the low tax regime in Singapore. “In terms of onshore tax, we are what I would call a low-tax jurisdiction,” he said, “but not a no-tax jurisdiction. In Singapore, our corporate tax rate is 17%, but Hong Kong is at 15% corporate tax rate, although we have other incentives, including zero capital gains tax. We have, for example, particular incentives for safe harbour provisions, so 13A states that if you own at least 20% of a particular company for at least two years and you dispose of it, that would not be considered a gain which is income in nature; even though that tax incentive was supposed to expire in 2020, IRAS actually came up earlier this year way ahead of time to say that it will be extended until 2027. In short, we are a comprehensive lower tax jurisdiction.”

Expert Viewpoint - Edmund Leow, Senior Partner, Dentons: “Singapore is a compelling location for family offices because it ticks all the relevant boxes. It is a global business and financial hub, where the required financial and professional services are available. It is also a place where high net worth families like to live and bring up families, with a favourable tax system, physical safety, the rule of law and political stability. Some other locations can offer some of these advantages, but few can offer all of them.”

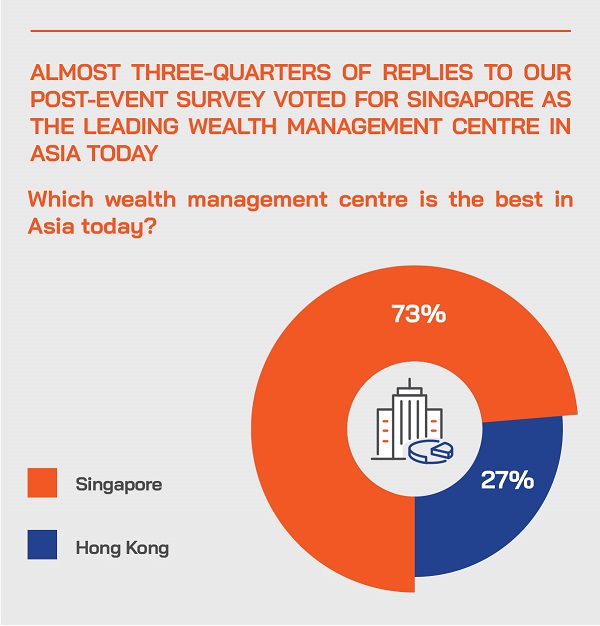

Post-Event Perspectives from the Audience on Singapore’s ‘go-to’ appeals

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on what they consider Singapore's key attractions as a ‘go-to’ Asian centre for UHNW family relocation and for family offices. We have edited their replies to provide the following insights from the wealth management community.

- The combination of government incentives for family offices and family relocation.

- The ‘13’ Suite of tax incentives and exemptions.

- Business-friendly for family offices.

- Rule of Law.

- Safety.

- Political and social stability, rule of law, language, tax incentives.

- Financial stability.

- Competitive tax regime, stable political system, rule of law, quality education and healthcare

- systems.

- Infrastructure, transparency and political stability.

- Investor-friendly.

- Transparent, robust rule of law.

- Flight to safety from political unrest in Hong Kong.

- Singapore is shining, as many UHNW families worry about the changes taking place in Hong Kong.

- Solid leadership.

- Common law jurisdiction.

- Only one super-regulator.

- Superior financial services infrastructure.

- High-quality professional services community.

- New VCC structure with tax and permanent residence incentives.

- No capital gains tax.

- Independent judiciary.

- Pragmatic, pro-business approach.

- Corporate governance.

- Politically independent of any major powers.

- Tax incentives for fund managers.

- Common Law jurisdiction/English-based legal system.

- Stable operating environment and corruption free government.

- Centre for technology and FinTech.

- Efficiency.

- Geographical advantage.

- Strategic location.

- Cosmopolitan city.

- Liveability.

- Quality of life.

- World-class city and amenities.

- Language skills of the workforce.

An expert pointed to the Monetary Authority of Singapore and the Economic Development Board and their many fiscal and other incentives, sensibly created and tidily carved to suit the UHNW community considering a move to Singapore.

“Interestingly,” a panel member remarked, “in the midst of the pandemic, we see many families realising that just having assets in Singapore is not good enough if they don’t have the right to live in Singapore permanently then the assets themselves do not add much weight. So, they are starting to look into a plan B, with the Employment Pass (EP), and the Permanent Resident (PR) programmes both excellent attractions. And looking at the Monetary Authority of Singapore (MAS) scheme for families who have adult children, for instance, we see a lot of them applying for family office structures where they would then appoint the children who are of age to act as investment professionals to fulfil the criteria required by either 13X or 13R. Then later they can apply for PR.”

And for clients who have an even higher asset value to their name and willing to commit serious money to Singapore’s economy, they can then look at the Economic Development Board (EDB) and its Global Investor Programme (GIP) as option C for a family office, if they have a minimum of SGD200 million in assets and with the understanding that by year five they must be able to employ 10 people in this company of whom five must be Singaporeans and three of whom must be investment-related. “These schemes,” he observed, “also attract many UHNW families to Singapore, aside from the taxes and apart from the macro, regulatory attractiveness of Singapore as a jurisdiction.”

Expert Viewpoint - Tan Woon Hum, Partner, Head of Trust, Asset & Wealth Management Practice, Shook Lin & Bok: “Singapore is the obvious choice as the asset & wealth management centre, especially for Asian UHNWIs and wealthy families. Given the stability, strong legal and regulatory framework, independent judiciary and pro-active and forward-looking government policies and regulations, many clients have set up operations and family offices in Singapore. As a result of our regulations and tax incentives conditions, families will have no issues meeting the substance requirements that remain a challenge in traditional offshore jurisdictions. In addition, with the available tax incentives, DTAs and new VCC structures, we are indeed in a very sweet spot.”

Expert Viewpoint - Lee Woon Shiu, MD & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “Singapore distinguishes itself in the Family Office as a class apart by having policies, an ecosystem and an operating philosophy which exemplify the 3 ‘T’s which are crucial in the minds of all HNW families – tenacity, transparency & trustworthiness.”

Another expert, a lawyer, highlighted the numerous positives Singapore has away from tax and other government incentives, citing the cosmopolitan character, English language skills and Common Law base, the full ecosystem in the asset and wealth management space, stable government, clear rule of law and independent judiciary.

Then on top of all that, and more, he noted the government-inspired incentives, the regulatory environment and of course availability of residence and possibly citizenship, and it makes, he said, a very compelling story for his clients, especially Asian UNHW and HNW families, to choose Singapore for single-family office or multi-family office setup.

Similarly, the GIP was first introduced as a scheme to encourage people to come to Singapore, to establish any type of commercial company, and thereby also create jobs for local people. “And the government and authorities have since adapted the GIP scheme to fit family office as well,” he reported. “It is clear that the government is proactive enough and flexible enough to adopt and adapt their schemes.”

Expert Viewpoint - Lee Woon Shiu, MD & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “The pandemic highlighted the agility, as well as transparency, throughout Singapore’s regulatory system, the legal system, as well as its ecosystem of advisors. Some clients have remarked that these qualities are precisely what encouraged or reinforced their view of Singapore being a long-term choice in which to base themselves and their family assets.”

Another expert observed that there is a region-wide trend towards the creation of family offices, as families institutionalise and professionalise their wealth and organise more efficiently and centrally across the generations.

“As well as wealth preservation,” he said, “we see a more multi-generational focus and planning, succession planning, and we should be expecting to see more philanthropic type causes being pursued, more concierge-type services from healthcare to education, and accordingly we will see a broadening of the perspectives and activities of these family offices. With Singapore infrastructure, business ecosystem, strong government and rule of law, this jurisdiction is ideally placed for the future.”

Another guest pointed to the versatility of family offices during the pandemic, commenting that centralisation aids agility. And a fellow panellist added that working with the right partners and advisors, who are also flexible, transparent and offer good advice and governance, is similarly vital.

Singapore’s standing vis-à-vis Hong Kong

The panel debated the relative appeal of Hong Kong. “For any incredibly wealthy family wanting to have a piece of the action in China, Hong Kong indisputably still stands to be the main gateway into China, and we have seen how the Chinese government has repeatedly made the point that they will develop the Greater Bay Area into one of the key hubs for the country,” one expert observed. “Hong Kong’s attractions are, I believe, here to stay. But UHNW families can diversify the risks, and they are, spreading their eggs into other baskets, the main one of which is Singapore, which also has the best current incentives and rules for family offices.”

Another guest commented that North Asian clients continue to view Hong Kong as very important, with Singapore as a very viable alternative for them, hence the arrival of more parallel structures.

“Those types of clients tend to continue to use Hong Kong as a base for the China investments and projects,” he noted, “but they use Singapore for things outside of North Asia, especially for ASEAN and Australasia and sometimes what they are looking at is an alternative venue for them to look from outside where they are right now.”

“What our clients often say now,” he added, “is that they have concerns about stability, so this, of course, is centred on new laws in Hong Kong, and new practices. Which is why more diversification of jurisdictions is taking place.” He added that in the aftermath of the GFC, European families also started having parallel structures in Singapore as well.

Singapore’s Suite of 13

The panel looked into some more detail on the key family office incentives Singapore has in place, essentially the three ‘13’ incentives.

The first, 13CA, is considered the entry-level incentive where if the fund is offshore, control and management of that fund are offshore, and the only link to Singapore is the fund manager or family office then all gains derived by that offshore fund would be tax-exempt.

Then for those wanting to take advantage of the extensive double tax treatments that Singapore has in place, the 13R tax incentive is relevant but requires a minimum expenditure per annum of at least SGD200,000 and at least one full-time investment professional. And for those who want the flexibility to have either a Singapore vehicle or offshore vehicle with no restrictions on ownership of the respective funds, then 13X would be the broadest exemption available, but in this case, in addition to the SGD200,000 minimum expenditure per annum, there is a requirement to hire at least three investment professionals.

An expert noted that it is worth considering how proactive the government and the regulator have been. “For example,” he observed, “if you look at the 13R and 13X tax incentives, these originally came about to attract the fund industry to Singapore, but then they realised this would really boost the family office space, and in reality, there has been more take-up nowadays from the family offices than from the traditional fund houses.”

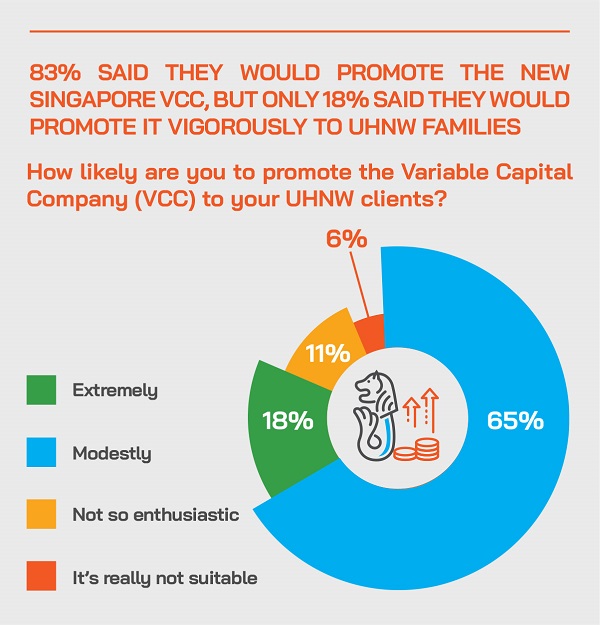

A New Kid in Town – The Variable Capital Company

A lawyer then highlighted the appeals of the relatively new VCC, the Variable Capital Company, which came into effect on January 15 this year.

“Single-family offices can use a VCC, but if it manages the VCC, the family office must obtain the relevant CMS licence or registered fund manager license, or appoint such a party to manage it,” an expert commented to explain its relevance. “The VCC is very useful, as it could also be used for different family units, perhaps a very big and wealthy family with first, second, third, or even fourth generations, so maybe the main patriarch/matriarch wants to use sub-fund A, the second-gen wants to use sub-fund B, part of the second-gen wants to use sub-fund C, so on and so forth. Moreover, the VCC is extremely flexible, so you could slice it up in different ways, and the tax incentive will still be available, the DTA will still be available. It is a very, very good option for UHNW families.”

Whilst Singapore has long been a location of choice for fund managers to physically base themselves, jurisdictions like the Cayman Islands have traditionally been used to house the fund structure itself. This is largely due to the Cayman Islands having a flexible fund regime with little restrictions, as well as a quick and straightforward fund registration process, leading to lower overall setup and administration costs. As a result, it has long been the case for Singaporean fund managers to manage assets for Asia-based investors via Cayman Island fund structures.

But Singapore VCC’s structure is specifically designed to compete with the investment fund structures traditionally found in the Cayman Islands, Dublin and Luxembourg. A VCC can be used for traditional and alternative open-ended and close-ended fund strategies. Open-ended funds are structured so that investors can invest and redeem their investment units or shares in the fund at any time, usually seen in hedge funds. Close-ended funds are structured with a fixed number of shares and an investor’s ability to redeem their investments is restricted during the life of the fund, usually seen in private equity funds.

Expert Viewpoint - Lee Woon Shiu, MD & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “Singapore’s VCC structure is for institutional investors and presently multi-family offices, and we can expect more of the latter to use it as its popularity rises. We’re already seeing a trend where some families come together to say, ‘instead of a single-family office, let’s consider a multi-family approach via VCC’, which won’t prohibit them from separately establishing a single-family office in future.”

As one of the experts present reiterated, one of the VCC’s key features is that it can be set up as a stand-alone single fund or as an umbrella entity with multiple sub-funds which may have different investment objectives, investors and assets and liabilities. Traditional fund structures are often hindered in diversification as they are constrained with one discrete investment objective.

The tax-free incentives available in Singapore under 13R and 13X are extended to approved VCCs. These incentives provide that specified income derived by a prescribed person from a fund managed in Singapore is exempt from tax, provided the income is derived from designated investments.

The Monetary Authority of Singapore (MAS) has also launched a VCC grant scheme to co-fund qualifying exemptions paid to Singapore-based service providers for work done in Singapore, in relation to the incorporation or registration of a VCC. With up to 70% of qualifying expenses, such as tax, legal and administrative services co-funded by the Financial Sector Development Fund established by MAS, and sums up to SGD150,000, it is now cheaper to set up a VCC in Singapore, than a traditional Cayman Island fund.

In the eyes of many Singapore protagonists, the VCC therefore provides another reason why Singapore should be the first pick to house any corporate structure. Furthermore, the grant evidences Singapore’s commitment to growing its fund domiciliation capabilities and catalyse early adoption of VCCs, ensuring that fund managers consider the VCC alongside traditionally used fund structures.

Trusting in Singapore

The discussion turned to private trust companies in Singapore and their appeals. “Some families would use a Singapore private trust as part of the family office option,” commented a panel member, “but not necessarily so, as they can actually just use a private limited company, they can use a single investor fund that’s self-managed or managed by third-party licensed or registered fund manager, but oftentimes they interpose a family trust which is a private trust under our trust law which has its roots from the UK trust law, in between the family and the family fund.”

Accordingly, this trust provides additional control in terms of the distribution of the family income derived from the family office or the family fund. It also provides additional confidentiality.

“And,” he added, “if you operate via a VCC, that is actually already confidential, so the trust gives you additional confidentiality. Some of our clients actually choose a family trust to overlay the family fund or family office to lock up what we call the enterprise of the family, so they may hold the controlling shares of listed vehicles or listed REITs or family enterprises that they do not wish to get lost before it gets passed to the third and fourth generations. In short, they lock up the economics and controls there and just allow the family members to get the distribution on a yearly basis.”

He elaborated on these points, noting that the choice of a Singapore or, for example, a Jersey trust is really about choosing very similar entities. “They are very similar,” he reported, “and a lot of clients either choose Singapore or Jersey, but they really stopped used BVI, Cayman and New Zealand trusts several years ago.”

He added that the Jersey trust is still preferred if the family insists on using the trust as perpetual, while in Singapore the trust mandate is limited to 100 years. “I believe there are many professionals, including some here today, who are trying to encourage the government to accept the merits of the perpetual trust, so hopefully you will get some good news,” he commented. “But an important point is the trust is not mandatory, and we oftentimes listen to what a family wants, and then we advise them to opt for a trust, or not.”

Singapore, ‘onshoring’ and substance

An expert highlighted how, in the wake of the arrival and implementation of global reporting standards such as CRS, and substance requirements in traditional offshore jurisdictions such as the BVIs and Cayman Islands, there has been a worldwide shift amongst HNWIs and UHNW families to ‘onshore’ structures into places like Singapore.

A lawyer commented that people tend to confuse the lines of demarcation between onshore, mid-shore, or offshore, but he stated that Singapore has for long seen itself as an onshore jurisdiction, and certainly not an offshore jurisdiction competing with the BVIs, or Caymans of this world.

Another expert referred to a McKinsey released on June 1 this year, highlighting the trend in onshoring amongst Asian UHNW families, noting that from 2016 to 2019 the percentage of funds which were onshore increased from 46% to 49%.

“The reason,” he explained, “is because, with greater transparency, reporting standards and such like with the respective tax amnesties, there is less of an incentive to offshore assets. And Singapore is a major destination. I recall a report on Channel News Asia saying that in April we had SGD66 billion of new deposits into banks from foreigners, a 44% increase from April last year. That is part of a very visible flight to safety.”

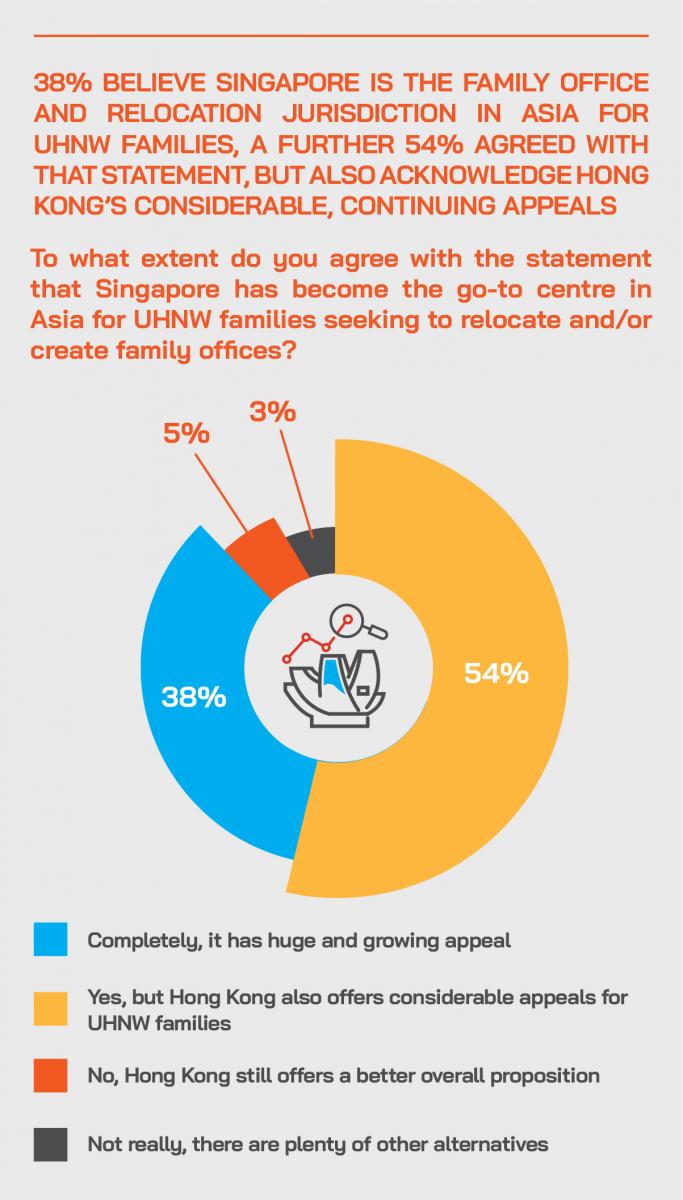

Post-Event Perspectives from the Audience on Singapore’s standing on a global basis

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on whether Singapore now competes effectively on a global scale as a UHNW centre, or if Singapore is thus far only competitive within Asia. We have edited their replies to provide the following insights from the wealth management community.

- Yes, it is globally competitive as the political stability is a huge selling point given the mess in many parts of the world.

- Yes, in recent years, the government has done a great job in introducing new schemes to compete on a global scale, and certainly such schemes are not only intended for clients within Asia; global clients are definitely attracted to the overall package that Singapore offers.

- Yes, it competes on a global scale as it has broad and seamless access to a global offering of assets. Singapore is competitive on a global scale and is developing rapidly as an ideal bridge between Asia and the west. It has a solid and stable working environment as well as international standards of law. It rivals the best in terms of infrastructure and regulatory framework. It provides investors with a stable investment environment and has a rich pool of expertise which they can tap into. We have already seen the shift made by several renowned global UHNW families to Singapore.

- Yes, because Singapore has a strong track record of corporate governance and is also competitive in terms of tax benefits and other incentives and attractions, and the government's recent handling of the pandemic also highlights its efficiency in handling crises.

- Yes, for many reasons, including the Asian mentality, culture and hospitality which trump all other cities.

- Yes, however, some neighbouring countries are catching up, and in order to stay ahead, we definitely need to do a lot more in terms of technology and innovation to compete effectively not only within Asia but on a global scale.

- Yes, Singapore has always been attractive to the Asian investors due to the time zone, the infrastructure and the connectivity; and with the negative outlook of the traditional tax haven jurisdictions, Singapore has become increasingly attractive to global investors outside of Asia as well. The traditional offshore centres are under attack and Singapore emerges as a compliant and stable jurisdiction with the backing of strong legal, financial systems, and with a stable political environment.

- Yes, Singapore competes well globally especially in the era of the OECD’s Base Erosion & Profit Shifting (BEPS) initiative, where substance is becoming more of an issue.

- Yes, Singapore competes on a global scale for families that are comfortable with the Singapore legal and regulatory system, the Singapore Companies Act, and the Singapore Tax Code. The strong infrastructure should be viewed positively as protecting a UHNW family's interests and providing for recourse. Singapore's numerous Double Taxation Agreements also allow for UHNW families that still own operating businesses to centre operations in Singapore with stronger assurances than other emerging markets.

- Yes, I believe that Singapore is now ready to compete on a global scale as UHNW centre. Whilst the policies and laws have been enhanced for quite a while, it is really the ecosystem of talent and solution providers required for the front, middle and back offices of family office structures which have truly come of age in the last few years and which have propelled Singapore to be ready to serve the global UHNW community.

- Yes, and it is continually improving. It is attractive both regionally and globally. However, it is not the only 'game in town' from a global perspective. Hong Kong, at least for now, serves as a better gateway to mainland China for those 'assets' needed to support the mainland business. However, now that many wealthy families now increasingly consider it prudent to have all other assets away from Hong Kong, Singapore is the natural and ideal candidate.

- Yes, Singapore is still more competitive within Asia as its safe-haven status appeals to Asian UHNW families from regional economies where there is relatively more political risk. Globally, there are also competitive ‘safe-haven’ centres in Europe and the US, as well as offshore tax havens that offer similar advantages, together with geographical proximity.

- Maybe, as Singapore is capable, however we are limited to our capacity and resources; if we have more resources, we will definitely be able to compete globally.

- No, I believe Singapore is only competitive within Asia, as it has not reached the point where UHNW families from Europe and other locations outside Asia will put their money in Singapore.

- Not yet, as we have yet to see more European or other UHNW families move in numbers, so we need to do more to attract them to come here, especially with specific attractions for their younger generations.

- Not yet. It is competitive within Asia, but for it to compete effectively on a global scale, Singapore needs to have a more thriving cultural scene and less censorship. In terms of legal, regulatory, governance framework, it is quite competitive with other jurisdictions.

- No, it is so far only competitive with Asia, because overall, the standard of service delivery is not on par with traditional UHNW cities.

- No, I still think Hong Kong is better, due to the China connection and cheaper tax, costs and other infrastructure facilities.

- No, Singapore is so far competitive only within Asia, and not competitive enough yet with regard to products and talent in centres such as Switzerland and London.

- No, I don't believe so - Switzerland is still perceived as the ultimate UHNW centre, and until we see a major influx of money from Russia and the Middle East to Singapore, Switzerland will remain the centre.

- No, Singapore is only competitive within Asia as it lacks the financial expertise yet to take it forward.

The discussion’s focus on onshoring trends led naturally to the panel to look at the role of new substance rules and their impact globally.

“Singapore is an onshore jurisdiction, and we are a substance jurisdiction, and in fact our government has focused on substance even before the OECD did,” one expert opined. “The government has actually never encouraged people from outside Singapore where no substance is required to set up Singapore companies. Now, some people have done that, in fact we have clients who have done that too, but that has never been encouraged by the government and that is not the kind of Singapore company that we are trying to attract today.”

“Essentially,” he clarified, “the government’s position plays to our strengths. Just to give you an example, if you have a Singapore company and if you want to make use of Singapore’s double tax treaties, you go to the tax authority to apply for a residence certificate and the first question they ask you is how much substance you have in Singapore. And they were already asking these questions well before the OECD started pushing substance. That is very clearly quite different from many of the offshore jurisdictions where they were essentially forced to enact substance requirements due to OECD and EU demands, whereas Singapore never needed this. We are very different from those jurisdictions.”

Talking specifically about the trend away from offshore structures in locations such as the BVI, or other well-known historical offshore markets, an expert noted how Singapore has encouraged re-domiciliation through amendments to the Companies Act a few years ago, allowing for a foreign company to re-domicile and to become a Singapore company.

Singapore is perceived as a reputable jurisdiction, he remarked, whereas there are reputational concerns about working through some of the more exotic offshore markets.

The trend will likely continue as some of the more exotic jurisdictions tighten their rules and practices under the combined pressure from the OECD, the EU and some national governments.

“On the Cayman front there are some new laws that are really of interest to clients with funds in the Cayman Islands,” a panellist noted. “The Cayman Private Funds Regulations 2020 require existing private funds to register with the Cayman Islands Monetary Authority before August 2, 2020 and for new funds to register within 21 days. Annual audits, cash monitoring new data points and so forth, so all these changes should be noted by anyone there is thinking about using the Caymans. And this of course is making Singapore even more appealing.”

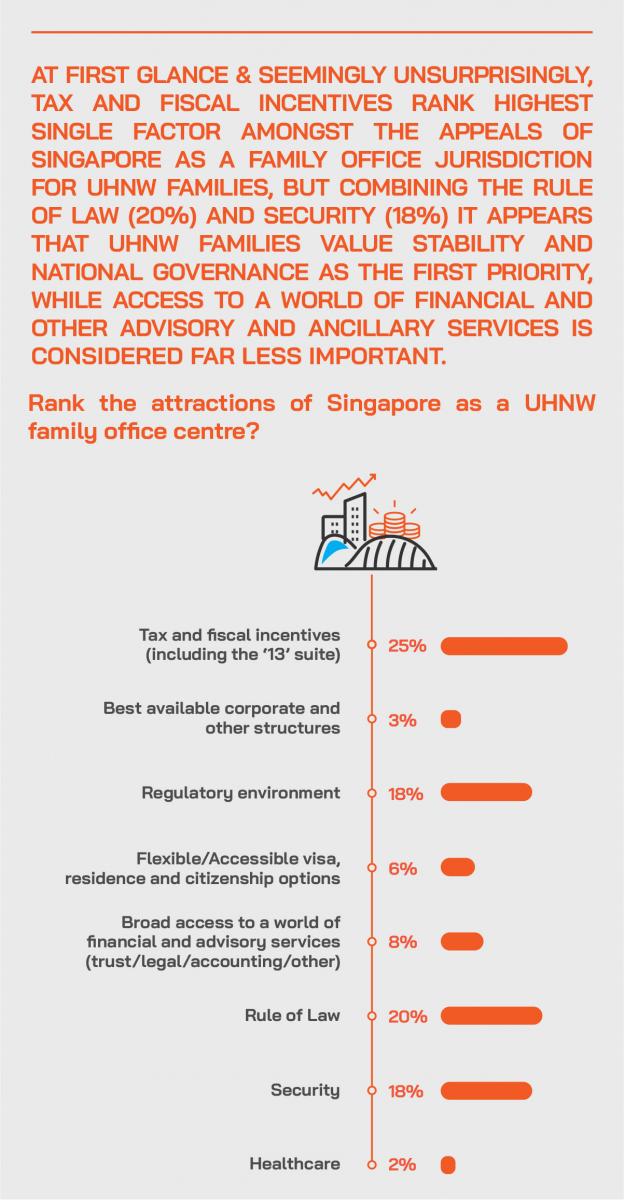

Post-Event Perspectives from the Audience on what more Singapore can do to improve

After the discussion, Hubbis immediately sent out a post-dialogue Survey to delegates. We asked them to briefly comment on what more the government and regulator can do to boost the appeals of Singapore for UHNWIs and families in the decade ahead. We have edited their replies to provide the following insights from the Hubbis wealth management community.

- Be more transparent, and somewhat less strict in some regulations.

- More tax incentives, less stringent documentation and moderated compliance costs.

- Become less bureaucratic and more straight forward, as we find things are still complicated in Singapore.

- Increase the depth and the reach of the capital markets to offer more investment choices for the family offices housed here in Singapore. The growth of such family offices will also increase if more wealth is created through a more active IPO market.

- Ensure that the legislation within Singapore reflect the focus of the UHNW as the wealth moves to the next generations, and especially focus around technology, ESG, and philanthropy.

- Assist the banks in smoothing out the KYC and account opening processes, which are today too cumbersome.

- The government and regulator need to strike a fine balance between relevant and smart regulations and less regulation. Singapore needs to be able to maintain its rule of law and good regulatory environment, while ensuring a minimum of red tape or unnecessary and cumbersome regulations that serve to impede rather than protect.

- Allow one Singapore-based property of at least SGD5 million, as primary residence, to be considered as part of but not exceeding 10% of their assets held in Singapore; this would ensure a stronger commitment into the country.

- The government and regulator need to continue to expand their programmes to attract smart investment talent so that the UHNW families have a broader pool of talent for their family offices.

- Offer more tax incentives to attract more wealth, and to attract more family offices to set up operations here.

- Grant more incentives to businesses who wish to locate in Singapore. Greater relaxation of capital requirements as well as business-related requirements.

- Improve the investment product range, financial flexibility, FinTech, and scale/size of stock market.

- Develop a more competitive digital platform and FinTech ecosystem. Digitalise more functions to create further efficiency.

- More talent. Provide sufficient infrastructure to cater for a bigger population, perhaps reclaim some more land. Embrace greater diversity and attract more talent by opening up the immigration from around the world. Allow dual citizenship and reduce army time to 6 months maximum.

- Greater privacy.

- More culture, more diversity. The common trend I have found is that a lot of UHNW families find Singapore to be limited, even dull in terms of the range of appeals within Singapore for UHNW families.

- Improve the relationship between Singapore and certain media, allow for more criticism.

- Put more resources on the branding and promotion of Singapore Inc., and the Family Office package. More promotion to families/businesses in Europe and the USA. Promote more connections like China-Singapore connect.

- Singapore needs to step out of Hong Kong's shadow and work harder at truly being ASEAN's

- port of call for Asian UHNW families. There is still some lack of understanding of neighbouring countries' cultures and UHNW family needs. There is a lack of understanding of their regulatory and financial environments, and hence less effective in offering advice on onshore assets of ASEAN UHNW families.

Relocation, Talent, Residence & Citizenship

Turning more specifically to investment migration front, an expert remarked that the pandemic had shifted the dial somewhat.

“The main driver for clients seeking such alternatives was historically they are looking for more travel freedom,” he observed, “especially of course for those with weak passports, for example Bangladesh, especially if they want to be entrepreneurial and do business around the world. Plan B in case of political or economic turmoil, or security was another vital driver to obtain a second citizenship or maybe just permanent residence in another country. But with the pandemic, we have seen clearly how even with border closures, countries are still open to still receive back their permanent residents and citizens, so it offers an insurance policy in that regard that will be even more important ahead.”

Expert Viewpoint - Lee Woon Shiu, MD & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “Social capital has come to the fore ever since Covid-19 emerged. Some clients shared their intention to deploy resources to support hard-hit communities in their home countries. Others expressed interest in giving back through the likes of venture philanthropy; such as helping social enterprises under the care of DBS Foundation to further their cause through funding or mentorship, or setting up philanthropy trusts.”

Expert Viewpoint - Dominic Volek, Managing Partner, Head Southeast Asia, Henley & Partners: “Investment migration was once a deeply discreet process, but now represents a transparently-marketed financial services product for the global HNWI, designed by sovereign states as an alternative, debt-free capital raising platform that can diversify economies, thereby creating societal and sovereign value = what we refer to as “sovereign equity”. This is becoming more and more important with regard to post Covid-19 recovery.”

Expert Viewpoint - Dominic Volek, Managing Partner, Head Southeast Asia, Henley & Partners: “The Covid-19 pandemic has impacted the lives of global citizens everywhere. While in the past, wealthy clients sought to establish a second citizenship or residence in countries that provided the best access, resources and opportunities, now the ability to reside in a country with a world-class healthcare system is at the forefront of wealthy families’ motives for considering investment migration. As the curtain lifts, people will seek to move from poorly-governed and ill-prepared places to more proactive countries with greater resilience and a better standard of medical care. Health security may also become a key consideration for countries in future when negotiating visa waivers, thus impacting global mobility and access.”

He added that Singapore is not the only beneficiary. Many people at the same time are seeing Caribbean countries and their investment migration programmes in even more positive lights, as their tiny populations make them apparent safer havens for escaping the pandemic.

“Border controls in those places are much easier,” he noted. “And Singapore has been amazing in its handling of the pandemic and with their job support scheme. In short, how governments responded and how will they respond the next time will certainly be more of an issue from now on.”

A panel member then commented on Singapore’s particular investment migration regime. “Of course,” he commented, “Singapore has high thresholds these days, with the government aiming to boost the economy with high level entries and investors that bring substantial funds here, but we receive many inquiries and a lot of interest, because Singapore is such a great place to live for these very wealthy families. Singapore has been successful via the GIP in ensuring that the families are actually physically coming to Singapore and residing here and the children going to school, as the education, lifestyle and healthcare and so forth are world class, it is immensely safe here and the rule of law is transparent and effective.”

A panellist remarked that Singapore is focusing on quality and financial strength in its incentives and rules, wanting to keep Singapore stable in the years ahead, as well as to maintain growth while elevating value-added throughout the economy. “Singapore,” he said, “has no need of foreign direct investment for the sake of it, they don’t necessarily have the space, so they are only looking really to attract the best of the best and the most successful entrepreneurs to come here and set up shop and move here with their families.”

Another explained that Singapore is today very competitive with other major jurisdictions that attract such UHNW and HNW families, for example Australia, New Zealand, the UK and the US to a certain extent.

“The programmes there might be a little bit more straightforward,” he observed, “for example typically there are no job creation requirements, and investment is usually either into a government bond or into the stock markets, sometimes into real estate, while the Singapore processes are more complex, but Singapore has nevertheless been very successful in appealing to families to move there full time.”

He elaborated on those comments, adding that for the top end of visas in Australia or New Zealand, the holders don’t really have to spend that much time there, so for example Australia requires AUD5 million, but only demands the holder stay 160 days there over a four-year period to get permanent residence. New Zealand requires NZD10 million but only 88 days there over a three-year period to get permanent residence. But Singapore has really been focusing on bringing these families to Singapore for full time residence and with their families in tow.

“The government here has also handled the pandemic very well,” an expert stated, “and that has actually helped drive increased interest, particularly from clients from Europe and even the US now looking at Singapore.”

Expert Viewpoint - Dominic Volek, Managing Partner, Head Southeast Asia, Henley & Partners: “The destruction of value in a range of investments across the globe has made HNWIs reconsider their portfolios and investment management differently. Hence, we have seen a rush for European property purchases via investment migration, which is now seen as an asset class in its own right and a hedge against further volatility and market uncertainty. Real estate has always been seen as an investment with staying power. Meanwhile, real estate–linked investment migration has the additional value add of enhancing the investor’s options for relocation or retirement.”

Expert Viewpoint - Dominic Volek, Managing Partner, Head Southeast Asia, Henley & Partners: “In the current context, many strategic global investors are already engaging in ‘post-pandemic planning’ – assessing their wealth portfolios and opting to diversify via real estate-linked investment migration programs. And the proof is in the figures – we’ve seen a 42% increase in clients wanting to proceed with an application in Q1, 2020 when compared to Q4, 2019.”

Expert Viewpoint - Dominic Volek, Managing Partner, Head Southeast Asia, Henley & Partners: “An investment migration application today might not help with the current pandemic, but it might help with the second or third waves of this one – or whenever the next one hits. The perception of investment migration has shifted from being about living the life you want in terms of holidays and business travel to a more holistic vision of life that includes a better lifestyle, healthcare provision, quality education, and so forth.”

Expert Viewpoint - Lee Woon Shiu, MD & Regional Head of Wealth Planning Family Office & Insurance Solutions, DBS Private Banking: “Covid-19 has prompted clients to deep-dive into broader structural and strategic issues such as wealth preservation, succession planning and family governance, and to plan with stability and longevity in mind. Domiciliation has also popped up in our conversations, as crises remind us of the importance of ensuring loved ones and assets are in a safe jurisdiction.”

Conclusion

The discussion closed with the panellists and some voices from the audience agreeing that Singapore, while still not perfect from certain aspects, is most definitely the rising star of Asia’s wealth management constellation. Singapore is clearly not out to benefit from any shortcomings or miss-steps that might befall the other regional wealth centre in the region, Hong Kong, and in fact the stronger the region’s financial centres and overall health, the better the wealth generation and stability for the entire region. Singapore will keep focusing on what it does best - driving its wealth management offering forward with the aim to becoming one of the pre-eminent global centres for UHNW families and for the management of HNW assets. In that regard, Singapore is doing a remarkable job