Private Markets & the Asian Wealth Markets: An Expanding Universe of Opportunity

May 27, 2021

The leading mainstream equity indices, in the end, performed relatively well in 2020, despite the chaos of the early months, but the performance was highly selective and often resulted in excessive inflows into a relatively limited number of huge capitalisation technology, healthcare and selected other stocks. And meanwhile, the growth of the private debt markets has been phenomenal over the last decade as the market has developed to offer additional yield to investors who are prepared to accept less liquidity and potentially longer holding periods. And of course, the public fixed income market since early 2020 has had investors on tenterhooks, as the market reacted first to the unprecedentedly low interest rates, but later to the spectre of inflation as it broke the surface amidst the latest tsunami of QE. The remarkable volatility and uncertainty afflicting the public equity and debt markets have only served to further reinforce the enthusiasm of many leading sovereign, quasi-sovereign, institutional and of course, private wealth market investors for the ever-expanding world of private equity, private debt and other private market investments. For our Digital Dialogue of May 20, Hubbis assembled a top-flight panel of expert to look in-depth at the evolution of the private markets, looking from a 360-degree perspective at the pluses and minuses and analysing where the market is heading and how the Asian wealth management community is positioning itself for what will very likely be the ongoing and rapid expansion in the years ahead.

The Panel

- Gary Leung, Head of Managed Investments and Private Equity, Hong Kong, Bank of Singapore

- Neeraj Seth, Head of Asian Credit, BlackRock

- George Boubouras, Executive Director and Head of Research, K2 Asset Management

- Gareth Lewis, Chief Executive and Co-Founder, Delio

- Arjan de Boer, Deputy Chief Executive, Head of MIS, Asia Markets, Investments & Structuring, Asia, Indosuez Wealth Management

The Expanding Universe of Private Markets

The world of private markets encompasses private equity, private debt of all types, venture capital, distressed debt, hedge funds (often considered more in the alternatives basket) and some parts of real estate, and all are non-listed. An expert observed how many of these world’s leading institutions are allocating more and more to these types of assets, and that the investor pool is truly gigantic, with Australia, for example in the trillions of dollars of savings to invest. For HNW and UHNW clients, they need access via private banks and other key specialists filtering and promoting such opportunities.

Another expert noted that by shifting to private markets, the lack of exposure to the increasingly volatile public markets is a great appeal. He remarked that the key skills for those promoting the deals involve sourcing and due diligence, and that involves a lot of networking and partnering with various asset managers, private equity firms, private debt firms or real estate private equity firms to access these opportunities.

He explained that his bank’s platform seeks to identify and offer best-in-class opportunities and managers, including in-house managers, through a fully open architecture approach, adopting top-down analysis to sort the best from the also-rans.

Another expert offered his clarifications around what might be considered alternative assets and what private markets might include. “We have seen the definition change all the time,” he explained. “We look at the space quite broadly from private equity, private debt linked into the direct co-investment piece, and then social impact investments. We are increasingly seeing more and more inclusion of different propositions around real estate as well.”

The lure of elevated IRRs

“On the positive side,” he reported, “private markets offer better risk-return trade-offs. If you are looking at a top-quartile private equity manager on a global basis, you will see IRRs in the high teens to mid-20s. In the public equity markets, you might get lower returns and higher volatility. In private credit, you should get a higher yield on similar types of credits, but in exchange, you give up liquidity away from the public market, and you sacrifice potentially some information transparency, although that can be alleviated by partnering with a good manager who has good access to these companies and good data as well.”

A banker observed that wealthy investors are becoming increasingly knowledgeable and that his bank had been driving these opportunities to clients for some two decades.

Risk mitigation through co-investing

“The way we risk manage is through direct co-investments, or we have funds of funds as another way for our clients to participate,” he explained. “We partner with big names, for example, firms such as KKR, which have very strong risk management. Illiquidity is often a disadvantage, but an advantage in a recession, because for private equity firms, a downturn represents an opportunity to plan and invest over the long-term, to deploy capital at more attractive terms, make bold moves without being hamstrung by public markets, they can make add-on acquisitions when prices are low.”

Another guest reported that PE is more established globally, especially in Asia, where the private credit market is relatively young. Nevertheless, despite the proliferation of debt globally, ultra-low rates have meant the search for income is even more difficult, while at the same time, the need for income is greater.

He said the corporate sector also understands the value of flexible capital, understands the flexible solutions provided by the alternate sources of debt providers, creating more private credit supply at the same time as demand and need for returns are rising.

Expert Opinion - Neeraj Seth, Head of Asian Credit, BlackRock: “Overall, given the attractiveness of risk premia in Asian Private Credit markets relative to developed markets, growth of the asset class with acceleration in the disintermediation of the banking system post Covid, and diversification benefits, we see an increased focus on Asian Private Credit from global investors. We continue to see a robust opportunity set in India and China. In India, the broadening credit gap and rising NPLs present opportunities in performing private credit and distressed opportunities. In China, deleveraging efforts and onshore defaults lead to further gaps in credit availability across growth capital and stress refinancing. And ESG has become an integral part of the investment process globally and we do see similar trends emerging in Asian private credit.”

The illiquidity risk premium

The same expert reported that the illiquidity risk premia is one of the least understood and least used elements of the toolkit for investors in private market assets. “This is a huge differentiator for us globally and more specifically in Asia, where we are one of the very few large platforms with a strong capability across the risk-return, liquidity and the country spectrum,” he explained. “Understanding risk premia across the spectrum [of asset classes] is critical. If you don't understand how risk premia work in high yield, it's harder to say what the right risk premia for liquidity you should be charging, for example.”

He said solutions could and should be designed to what the clients want and expect, rather than having opportunities driven more by the product-push type approach, which has too often prevailed in the world of Asin private banking.

Art and science combined

He explained to calculate the illiquidity risk premium involves a combination of art and science. “The pure illiquidity risk premia can be anywhere between 50 to 500 basis points,” he reported. “The way you would think about it is, the higher you go up in quality, the more shrinkage there is in the illiquidity risk premia.”

Accordingly, if an investment grade company tries to do a private placement, they might actually get away with 50 basis points of illiquidity risk premium, but if you move into the sub-investment grade segment, the lower end of the high yield market, there the premia will be considerably higher.

Asia’s high yield premium

“To put actual numbers in perspective in Asia, if I look across the region today, the average high yield market is dealing close to 7%, while the US is sub 4% right now,” he reported. “When we look at the private deals of the region, they tend to be between low double digits to high double digits, somewhere between 11% to 19%.”

He added that part of it is due to the illiquidity risk premia that is captured, and also the complexity and the opaqueness. “So, if you split it up, you're picking up 300 to 500 basis points in illiquidity and then obviously, you're getting paid for solving a complex problem for a number of these corporates alongside the illiquidity,” he explained. “That is why I said there is both art and science involved. It's not pure science; you can't mathematically say this is exactly how much to charge on illiquidity. But I know how much based on where the markets are on the public side, how to price a private deal in a certain sector with a certain credit matrix of a company and also depending on the complexity of the issue.”

Plenty of growth ahead in Asia

His last comment was that, relatively, Asia’s exposure to private markets is below the global norms today, especially in private credit, and in his view, less crowded markets tend to be less efficient, and where there is less efficiency in the market, there are opportunities to drive more alpha and return.

Another expert explained that his firm helps financial institutions of all sizes offer more to their clients in the private markets, by helping design, deliver, configure digital propositions that enable the distribution of private deals.

“We are mainly asset class agnostic, and work with a range of financial institutions from large global banks through to smaller boutiques,” he reported, explaining that the genesis of the firm was to broaden access amongst financial institutions to these private markets, partnering with those banks and firms to help them achieve their goals in these areas.

Technology, expertise and network

He explained that the platform consists of three core elements - technology, expertise and network. “The core of the business is our technology-enabled, white-labelled platform,” he reported, “whereby we can help build a platform that enables financial institutions to offer deal flow to their clients in a compliant, efficient and effective way, then help mould the propositions. We've also got a network of deal flow providers who are able to help with the curation, the due diligence, and in ways that enable a wealth manager to offer the kind of solutions that they think resonate with their clients.”

He explained that from their somewhat unusual base in Wales, they now cover many regions, having built out from the UK and Europe, and with their Asian office now open in Singapore. He remarked that activity levels had risen markedly in Asia, where there is a highly entrepreneurial approach to private markets, and that he sees great potential ahead, hence the new office in Singapore.

The Post-Event Survey

Hubbis: In your view, what has been driving the growing global demand for and liquidity allocated to private market investments, and what trends have you seen amongst wealthy investors in Asia?

- The low interest rate environment and an increasing complex investment environment with exciting opportunities in transformational change.

- Better risk-adjusted returns in private market investments.

- With lower rates, private markets, especially equity and VC, can serve as great drivers of return enhancement.

- Volatility and uncertainty in the public equity and debt markets and low interest rate environment.

- The search for yield, and diversification away from traditional listed securities and volatility.

- Persistently low global interest rates have driven liquidity to chase higher return assets.

- The easy availability of cheap funding.

- High valuations in the public markets, and increasingly companies have been delaying going public.

- More education and ease of information and more product flows.

- Investors are increasingly keen on niche investments.

- Clients are increasingly drawn to high IRR projects, even if this means holding for longer and losing liquidity for some years.

- More UHNWIs in Asia and more demand from them, taking 10% to 20% of allocations to the private markets, sometimes more.

- Generally, these private market investments are not available or offered to the retail or mass affluent segments, so they have some unique appeals and tend to offer more return, albeit over time, and meanwhile investors feel less anxious as they are not actively trading on the market.

- Money printing from the governments and central banks has resulted in greater diversification from traditional investments. Private markets offer low correlation to the public markets and higher ROIs.

- A larger and larger contingent of deals are going public later and later, which makes investing in private market investments more attractive for clients. It's matching the pipeline with the demand.

- Rising allocations to higher returning alternative investments such as private equity but also distressed investments in private debt and unlisted real estate and infrastructure/projects.

- We see more and more younger generations of HNW and UHNW clients taking these opportunities.

- Savvy investors from their 40s onwards are moving further and further towards private markets.

- ESG and climate change are key talking points among clients.

- They are looking to reallocate or rebuild their financial portfolio and are more open to private market investments, as rising interest rates and access to alternatives are steering the trend.

- Many have been attracted by opportunities to buy into future tech unicorns.

- They can express themselves via ESG, Crypto, Blockchain and FinTech opportunities.

- Clients are looking for more tailor-made products designed for their needs.

- They are attracted as there is greater accessibility, better due diligence, and improving information transparency.

- We increasingly see a higher proportion of total investable wealth allocated to private markets and there is increasing trust in outside managers as opposed to internal expertise in family offices.

Funding private markets via funds

Another expert explained that his firm’s clients range from sovereign wealth funds to pension funds, family offices, and also HNW/UHNW via private bank relationships. He explained that his firm helps investors buying various ETFs which belong in the private market space, that they do not work directly on specific opportunities, but their model is to support the fund approach, whether for private equity or private debt or VC. He reported strong and rising liquidity from all quarters for private asset funds from his perspective.

The discussion shifted to tokenisation to bring opportunities to a wide array of investors. “We believe that blockchain or tokenisation in general is actually potentially a next step for the industry,” he reported. “If you think about having a feeder fund, and actually distributing to a number of underlying investors, that is very much what we call the unitisation of investments. In fact, tokenisation can potentially be a more cost-effective and a more efficient way of doing this, and this is an area that we are actually exploring at this stage, but with no conclusion as yet, so we focus right now on the traditional feeder fund route.”

Place your bets…

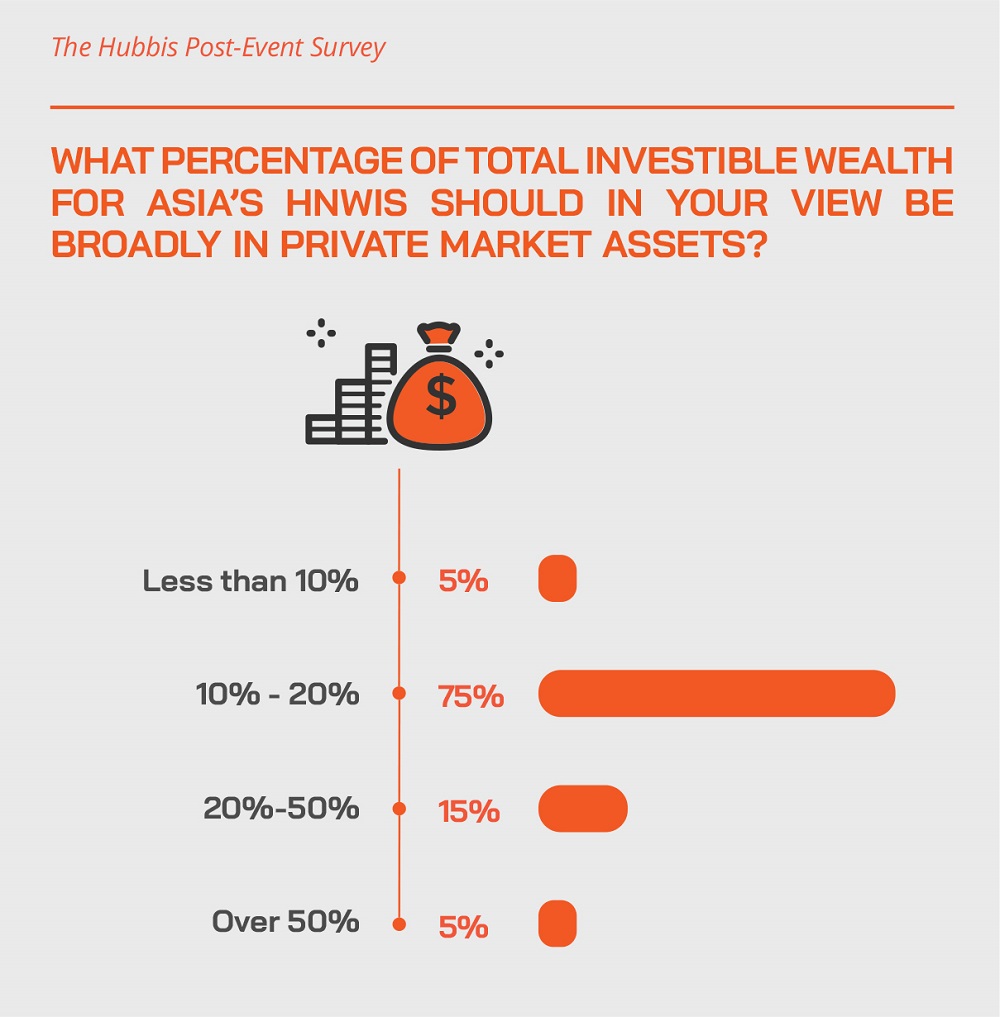

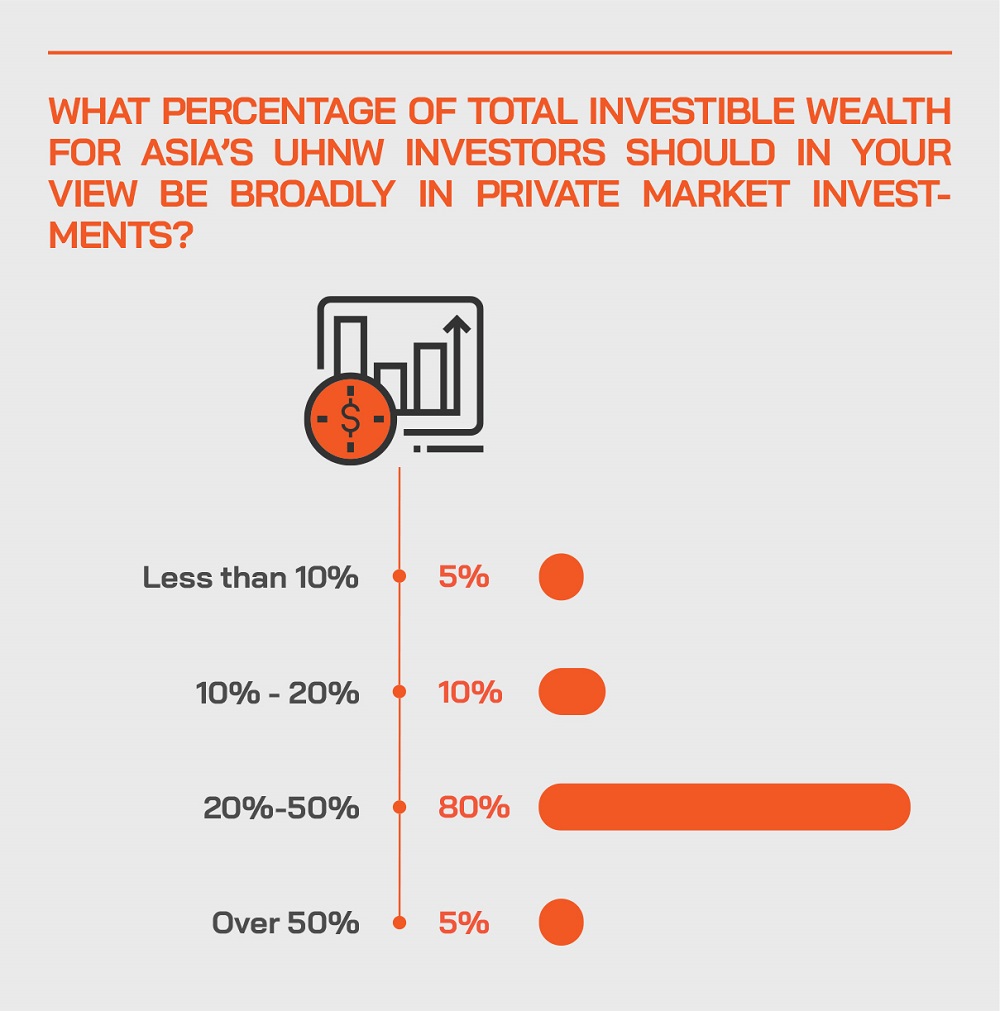

As to the advisable levels of allocations to private market assets, a guest said this must depend on the individual situation, including their age, wealth, their inclination or lack of to risk, whether they might need access to liquidity for themselves or their businesses ahead, what their time horizons might be, and so forth. He said that given all those elements in the mixture, 20% to 30% allocations are reasonable, with some investors going for considerably more than the upper level. The discussion was framed mainly around HNW and UHNW type investors, rather than the mass affluent or retail markets.

“When we invest into various parts of the private markets, be it private equity, private debt or real estate, we actually try to help clients diversify their portfolios,” he reported. He added that there is also significant interest in areas such as private credit funds that offer quarterly liquidity for clients, so that clients do not need to be entirely locked up with no liquidity for many years.

He said the general trend in Asia was for investors to have become increasingly savvy with their allocations to private markets, and better engaged in learning more about the opportunities and the deal structures.

Another guest added his views on the Asia market, reiterating that the exposure in Asia to private credit would be far lower, at perhaps 7% or less. “When you look at Asia in terms of the size of the banking system, the size of the GDP and the growth rates, and given the pressure on the banking system with COVID-19, I would expect that these numbers will actually accelerate meaningfully from here over the next 5 to 10 years,” he predicted.

Looking far ahead

Another banker reported that they promote the PE markets only to clients who have higher levels of risk appetite and who can comfortably adopt a 10 to 12 years standard investment horizon. “That sort of length of investment is clearly not for everyone,” he said. “We see in the upper tiers of wealth, especially the UHNW segment, that clients are often willing to commit 20% of their portfolios to private assets, sometimes even more.”

He said he generally sees more knowledge out there in the market Asia, but also that it had become harder to find the right investments with the right risk metrics and the right projected IRR to give to clients because demand outstrips supply.

“And as Asia is not as developed yet,” he observed, “we agree with an earlier comment that with the right due diligence, actually, the opportunities going forward are actually here in Asia.” He added that the bank managed around USD5 billion of PE investments globally, of which around 20% are in Asia, including Australia. However, of course, Asia’s share of GDP is far larger as a percentage and growing faster than most.

Linking private assets to ESG

He also explained that the allocations can also fit neatly to the thrust for sustainability and more ESG-driven investing. He cited for example some large real estate projects in China, where private market investors can obtain a seat at the board table, also look then at diversity, workplace processes, building methods, and so forth. “Many of our clients investing in private equity are somewhat older clients, and they take a real interest in these issues,” he said. “If they do direct co-investments, they can influence these important areas.”

Another guest commented that ESG is front and centre in everything his firm does with sovereign wealth or pension funds, as well as with wealthy private clients. “ESG must be deliverable in all these strategies these days,” he stated.

The Post-Event Survey

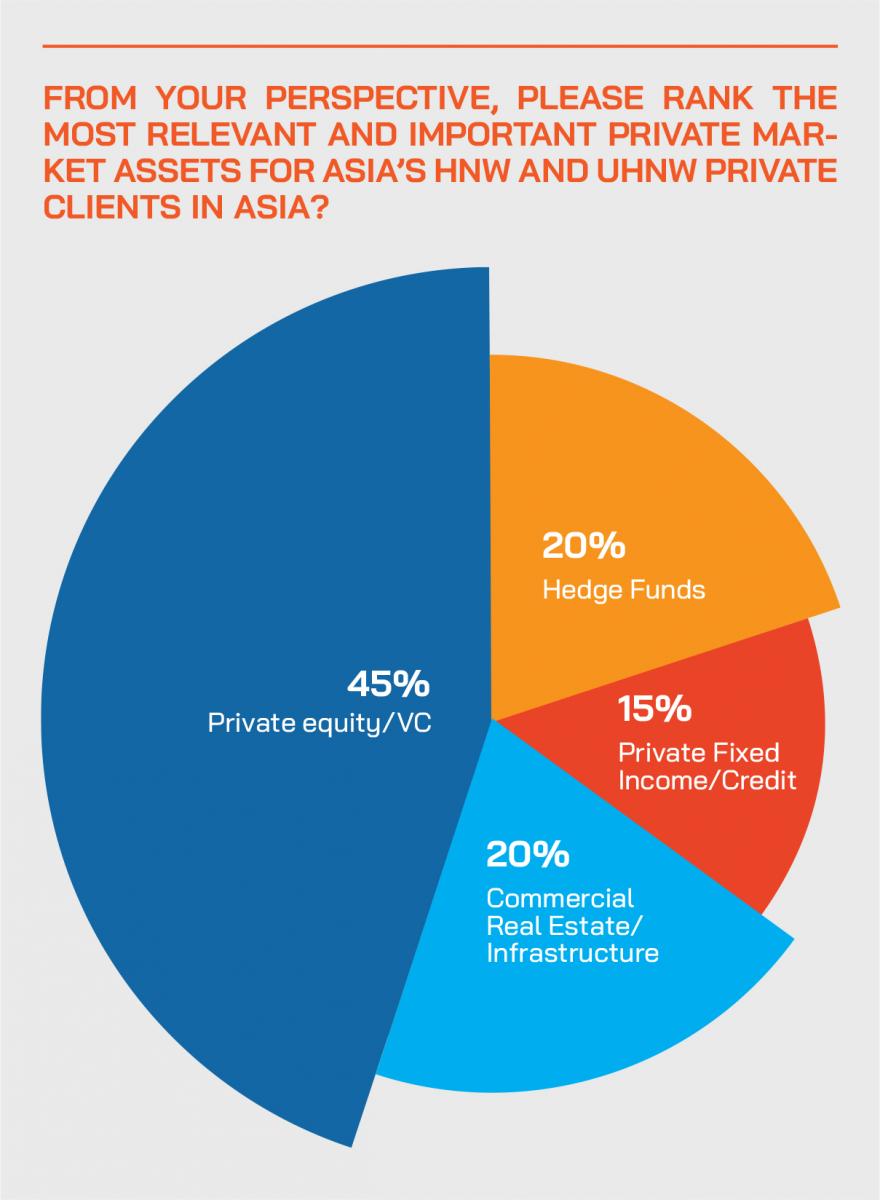

Which key industries/sectors are investors focusing on for their private equity market investments, and why?

Comment: There were numerous ideas here, many of course repeated many times by different delegates. We have summarised them as below:

- Sustainability and Technology (secular trends that are likely to yield better returns).

- Technology via venture capital opportunities to get involved early stage.

- ESG-driven investments

- Electric vehicles

- Agricultural alternatives (alternatives to meat production)

- New economy

- Renewable energy.

- Healthcare, BioTech, MedTech

- Sustainable finance

- Real estate, selectively e.g., logistics, retirement, sheltered housing etc

- Cryptocurrencies and blockchain

- AI

- Environmental

- Transformational industries and products

- Distressed assets

- Asia-centric opportunities

- FinTech

- Financial Inclusion

- Education

- Sustainable Food & Agriculture,

- Climate and Water Solutions

- Smart Cities & Liveable Ecosystems

- Infrastructure (very predictable, assured returns)

- Logistics following changing economic activity post-pandemic

- More in Asia, where more deals and opportunities are already arising

- Hospitality, selectively for recovery

- Digital transformation

More support required in private markets

Turning again to risks, an expert observed that these are no different from any economic or financial or business risks as expressed in the public markets. However, he noted that on the private side, it typically harder for investors to try to manage all of these risks by themselves.

“Once you understand these risks, the last step of the process, which we still have to do, in addition to the due diligence, is to be able to do your documentation effectively,” he observed. “You can negotiate the best of the term sheets and the best of the deals and give it all away, for example as a creditor with weak documentation. We therefore spend a lot of time on making sure that the creditor protection framework in different countries is taken care of, all the way from structuring documentation aspects.”

Assessing the various risks

He added that the promoters and investors need to assess the macro country, industry, and then the idiosyncratic risks that you're managing. “And then you then need to tighten it all up, bring it all together in the proper documentation in these private investments to make sure you have the protection you need and expect,” he advised.

“From my perspective,” said another guest, “managing the risk by assembling a diversified set of holdings across asset classes, across different investment sectors and opportunities, and providing that holistic proposition, these approaches can really help clients in this private markets endeavour.”

Experts needed to filter the deals and assess risks

He added that as long as those promoting such investments engage professionally with the clients and focus on their relationships externally as well as internally, they can do well potentially in these private markets. “I think it's all around the building out the proposition and getting those kind frameworks right and having those good relationships. Any institution, whether boutique or global, has a far bigger reach than their clients, realistically.”

A banker remarked that the EAM/IAM community, working closely with their custodian and execution/trading banks, can certainly curate an interesting private markets proposition.

A guest added that they should not forget hedge fund strategies in private markets, which are considered alternative investments, but that fit neatly to private markets, as they are unlisted.

The dynamic approach

Private debt, being non-listed, all up and down the capital structure offers some defensive characteristics, with lower annualised volatility in exchange for the illiquidity premium, this expert also commented. He added that pension funds, for example, will now approach these markets dynamically, allocating actively between private markets and private market alternatives, such as a hedge fund strategy. He said diversity in the allocations was key to assembling the right sort of portfolio.

Focusing in on sectors and industries, a guest said that the Asia private credit market offers significant potential. He said that banks are more risk averse today than for example leading to the global financial crisis, and private markets have stepped in to provide the shortfall in capital, seeing opportunities in this sector. And technology and its impact on our daily lives will continue as a key theme, he predicted.

Another banker cited PE opportunities ranging from homes for the elderly, student dorm rooms in Germany, high tech companies in China, and other areas. Private equity, he said, reflects the diversity of their client base as well, representing so many different types and sectors and businesses.

Analysis and due diligence

Looking again at risk, he said their co-investment approach alongside large, well-known investors and arrangers in this space offers the best approach to risk management, as well as ensuring the portfolios are well diversified. “And we have teams across the world who are private equity specialists that engage with our clients and explain and educate and all the details what private equity or private debt or private real estate or private real assets, what it actually entails.” And who reassure clients in their approach to due diligence and deal selection, as well.

He noted that the private markets business in Asia is increasingly subject to regulatory scrutiny, to ensure that those promoting opportunities are not overcharging, that they are offering deals that are suitable and properly researched and that there is full transparency throughout the processes. “Regulators might ask to see how we have done our due diligence on products, just as with mutual funds, and what type of clients you allow these clients to invest in them,” he noted. “That is why for our bank, only clients with the highest risk profile and the longest investment horizons are allowed to invest in this particular asset class.”

The Post-Event Survey

What key skills and qualities are investors in Asia seeking from the banks/firms they will work with for private market investments?

- Negotiation and networking skills. You need to meet and speak with investment bankers, venture capital investors and other market participants.

- Opportunity, access and transparency.

- Extensive Private Markets expertise

- A solid track record

- Access to Top Quartile managers

- Track record, knowledge, risk management and the ability to sniff out good deals.

- Deep connectivity in the industry to identify and deliver good deals.

- Banks that have access to variety of money managers globally.

- Expert due diligence on underlying companies and business models.

- Access to exclusive transactions.

- Networks and connections to choose the right targets.

- Strong regulatory and compliance background, negotiation and networking, venture capital expertise, strong credit assessment capabilities.

- Research skills and a solid database of deals past and present.

- The ability to share and explain the product and investment structure.

- RMs and ICs must be able to communicate clearly and in depth.

- The ability to differentiate from the crowd.

- Obviously in private markets manager selection is key so the clients would demand access to top tier managers from their private banks.

- Reputation, track record, the ability to source for the more limited offers by the banks/firms.

- Ease of onboarding into a PE subscription.

- Industry insights. Networks and access. A proper exit strategy.

- Technology solutions to easily see investments updates on a regular basis.

An accelerating proposition

Another guest added that it is vital to assess the durability and consistency of the managers, to ensure those managers are both highly capable and have access to deal flow. “And given the time horizon is long, during which you don't have access to liquidity, once you make a commitment, you want to make sure that the manager is going to be around five, seven or 10 years from now,” he said. “That stability of the platform becomes critical.”

After reviewing some of the obvious sectors and countries in Asia that would be open to more such opportunities, for example China or India, or specific industries such as real estate, technology, medical technology and biotech, and so forth, the final word went to a guest to comment on the impact of the pandemic on this market.

“During the pandemic, maybe trends that might have taken 5-10 years have taken a lot, lot less time to come to fruition,” he said, “especially around technology and how the way the world's working these days. Similarly, obviously, there are lots of interesting opportunities around how different businesses are tackling the challenges that the pandemic has created. We've seen some interesting deals within infrastructure focused around the pandemic, essentially the wider trend around the way that the world works now in terms of the world had worked before. In short, there are more and more opportunities.”

Opportunity out of diversity

The panel closed the discussion in broad agreement that the investor market in Asia for private markets will continue to expand in the foreseeable future, with the key challenges being the filtering required to deliver the best opportunities, and the ongoing commitment to delivery information and transparency on the investments that clients choose. The Asian market itself will also likely deliver more of the actual deals to bring the flow more into line with the economic power in the region. Across such a vast region that is so diversified in terms of languages, cultures – so different from the US and Europe – this will present even more challenges ahead, driving an even more professional approach from the promoters and the investors alike