Wealth Solutions & Wealth Planning

Maximising the Impact of Discussions around Wealth Solutions and HNW Insurance in Asia

Nov 11, 2021

It is never easy for private banks and wealth managers to start and then successfully pursue what are rather personal life insurance conversations with private clients, even though they may be both highly relevant and very necessary. But the drive to optimise estate and financial planning through the involvement of life insurance solutions has been made somewhat easier due to the arrival of the pandemic, as intimations of mortality have moved much closer to home for anyone and everyone. Life insurance solutions clearly have a prominent and indeed elevated role in helping HNW and UHNW clients protect their wealth, and also in providing the family with liquidity in the event of a death, as well as helping facilitate more efficient estate and even succession planning. In our Digital Dialogue discussion of October 21, we explored the state of the life solutions industry today, reviewing the latest trends in products, identifying the optimal solutions for individual needs, analysing where demand is on the rise from amongst the different segments of clients in the Asia region, and most importantly defining how the various industry participants can boost the take-up of these solutions in Asia by better communication, enhanced education of all parties involved, and greater transparency in terms of approach. This is actually a topic dear to our heart at Hubbis, and we have for quite some years now worked hard to promote the use of life solutions with our friends and partners in the industry. The mission is to help spread the word amongst our universe of clients and partners in the private banks, the financial advisories, the brokerages and the other wealth/asset managers, in order to help them focus on these solutions and also to help them promote the right conversations with their colleagues, partners and private clients.

Panel Members

- Berry Wong, Chief Executive Officer, Asia Pacific, Charles Monat Associates

- Simon Cheng, Regional Head of Money Markets & Insurance Collaboration, HSBC Private Banking

- Regan Shum, Head of Insurance Brokerage, Hywin International

- Lee Sleight, Head of Business Development, Asia, Lombard International Assurance

- Will Price, Head of International Distribution, ASEAN, Quilter International

The October 21 panel discussion focused to some extent on the products themselves – whether UL, VUL, Whole of Life, PPLI, or others – but as much on how the wealth management community should be promoting and selling these solutions.

This is especially pertinent since the pandemic hit, which has, of course, focused the world on issues of mortality but has also impeded the vital face-to-face communication so often vital to the sale of larger policies, as well as impeding the health checks that have historically been needed in order to write such policies.

As the pandemic has exacerbated financial markets volatility, as local and national lockdowns have been imposed, as travel and social interaction have been so impeded, how then has the wealth management community managed to keep the life insurance solutions market forging ahead, and what role has technology/digital been playing in helping deliver these conversations and then ultimately the solutions duly signed and executed?

A dynamic market

The market is most certainly there to be grasped - despite the virus and market uncertainty, the HNW and UHNW population remained robust, growing by nearly 8% in 2020, and Asia-Pacific remains one of the world’s fastest growing major regions for HNW individuals (HNWIs), according to a recent study by WealthX.

And at the same time, naturally the pandemic has also increased awareness amongst HNWIs in the areas of health, longevity, and legacy planning. The result is that many HNWIs are now looking at life insurance as part of their overall protection and wealth management plans. Moreover, HNWIs who are business owners are also continuing to look to life insurance for business protection, including partnership coverage and insuring key employees in the event of an unexpected death.

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “Regarding the need for tailored solutions, and reflecting what we have experienced in Europe, Asia-based advisers are already seeing an increasing demand for tailored wealth planning solutions. These must be flexible and capable of adapting to the changing needs of families spread over multiple jurisdictions – advisors recognise that they need to broaden their offering and advice to reflect the diverse and ever sophisticated needs of their clients.”

Expert Opinion - Will Price, Head of International Distribution, ASEAN, Quilter International: “We are seeing a growing interest in solutions which help remove complexity, redundant layers of structures and costs, whilst achieving clients’ desire to retain investment control. Robust, flexible and portable personalised wealth structuring solutions, which are legally recognised and jurisdictionally compliant – being PPLI and VUL are gaining awareness as a core component in wealth planning.”

Building the right approaches

Opening the dialogue, a guest reported that business volumes had risen significantly since 2019, with the pandemic having forced people to consider mortality and therefore planning much more urgently and carefully. Moreover, he noted how life expectancy had dropped the most since World War II, while remote working has given people more time to organise their lives and financial and other planning from the comfort of their own homes.

“There have been some impediments, such as the difficulty of obtaining medical certificates, but generally people have worked around these issues and found ways to obtain the benefits they more clearly understand now. Online adoption has been key, and we have all had to adapt rapidly. But generally, it has all been positive.”

The importance of being earnest

And amidst this overall environment, it is of course absolutely critical for the key players in the wealth industry in Asia to maximise the quality and efficacy of their approach to clients to ensure that these complex products move through to completion and deal signed.

A guest pointed to the importance of a broad-based dialogue between the various parties who are working to develop the business in the region, with leading brokerages needing to collaborate highly effectively with the bankers and the wealth planners to ensure that they spot the right opportunities to promote life solutions to their clients, and in order to do so, those bankers and estate planning experts must see how those solutions fit into the bigger picture of estate and legacy planning.

Education and more education

Another expert observed that time at home had helped spread the world around the subject, with education amongst partners and associates improving as they have taken the time to improve their knowledge and expertise.

“Education I think is key for this industry,” he reported. “And we're not just talking about advisors, we are talking about the clients themselves. Because information is available on the various insurance solutions, wealth planning solutions, other wealth management solutions out there, many have used this time constructively to educate themselves. And we have had a lot of interest, many questions on structures and products, and all this creates a major plus situation for us.”

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “There is a great need for education, education, and more education. Providers must support advisers in educating them on how these solutions work and the advantages they bring, so in turn advisors are in a position to educate their clients on the benefits of each solution.”

He added that this means the distributors such as the bankers, the RMs, the EAMs and IAMs and family offices, all of them are now more comfortable in putting solutions in front of their clients. “They do not need to put forward the entire solution, but they are now much more attuned to spotting opportunities, to identifying the client's needs, and then thinking about where insurance can match with those,” he reported. “The result is many fewer missed opportunities.”

Carpe diem

Another guest concurred with these views, adding that the banks and brokers do not necessarily need to understand every detail and nuance, but they do need to see the value, be able to communicate the key elements of specific solutions and then work with the different experts to advance those from concepts with the clients to completed deals. “It is impossible to know everything in detail, but you need to know what's out there, and if you aren't talking to your clients about these solutions, someone else will.”

They might not just lose the insurance business, they might lose the clients as other banks or firms pitch insurance as part of a broader estate and legacy planning scenario that draws those clients to their own banks or firms, this expert warned. “My call to action I guess is to sort of reach out and engage with your professional network,” he advised. “Continue to educate yourself but be comfortable with outsourcing some of that knowledge where appropriate, because if you're not doing that, there are some inherent risks.”

‘Heat-seeking’ advisors and brokers

“Typically, these days, our client is in the age range of 40 to 65, and gradually becoming younger actually, but the legacy planning is always the same,” a panel member explained. “In terms of the entire relationship, the RMs at the private banks are still constantly looking out for the so-called ‘hot buttons’ to press at the right times to ensure that when they see their clients expressing certain concerns and objectives, they raise the topic of reviewing what their risk exposure is, and therefore what solutions they might be able to consider.”

He observed that the pandemic had given his firm an interesting opportunity, as clients have gone back to their existing solutions and portfolios and re-assessed the potential liquidity issues that might occur should any unexpected death occur. “Moreover, the investment market has been volatile and is rather uncertain,” he commented. “For all these reasons, clients are these days particularly keen to look at solutions to reduce their risks as well as stabilise their returns.”

Refining the solutions

“This environment,” the same expert elucidated, “offers us the opportunity to mine down into clients’ existing portfolios and, working with the bankers, to help identify the so-called ‘hot button’ to press that will encourage them to consider the different ways to improve their returns as well as enhancing protection, and all within the wider perspectives of legacy and succession planning.

“In short,” he observed, “I certainly still believe that communication with our clients as well as the private bankers and wealth planners are essential elements in the broader, entire selling process. If we are talking to them and if we understand their needs, we are well placed to succeed.”

Core to the wealth management offering

Another expert reported how important a part of their overall wealth management offering insurance had long been. “We see this from two major perspectives,” he explained. “First, insurance is central to the more traditional wealth planning objectives, offering an ideal tool to pass on wealth to the next generations, so it is not simply about protection. Secondly, this can be viewed as more central to the asset and jurisdiction diversification missions, and here in Hong Kong this has been especially important as we see more clients seeking to emigrate, especially those from the second or third generations of wealthy families. Many of the typical clients are mostly invested in Hong Kong, China or the near region, but insurance is a vehicle potentially to diversify asset types and geographies globally.”

He added that their firm is also continually advising clients that they should be diversifying in terms of their assets and that life insurance helps with this objective as well. “We have seen crises, for example the Evergrande situation, as well as other problems emerge, and all such surprise events simply reinforce our view that it is well worth diversifying into more different asset classes and geographies,” he told delegates. “Insurance comes in very handy as a structure through to diversify. The clients need both protection and at the same time insurance still plays a very important part in terms of both their asset and also their wealth planning.”

Building from within

A guest explained that a key mission for him and his team is to encourage their RMs and advisors at the bank to bring insurance front of mind, even though they are generally much more comfortable discussing mainstream markets and investments. “Insurance has not really been considered an asset class before, but I think things are gradually changing and these discussions are moving more in line with broader discussions on estate, legacy and succession planning, all important themes to really cement the client relationships,” he commented.

“Because once you get into these deeper conversations, the relationship generally will be much more enduring,” he added. “And this is why we set up a team to directly promote the benefits of insurance and to educate the client advisors about the importance of talking about this subject. The inclusion of insurance in the whole concept of wealth planning is at the relatively early stage, but it is becoming viewed as one of the important solutions in the toolbox.”

Improving the dialogue

“There are more and more wealthy people and as they look into these matters, especially proper, robust wealth planning, they see more and more that insurance offers an excellent solution,” a guest reported. “When you talk to them about this essentially as a new asset class, that is really rather an interesting topic for them. We cannot say we execute this perfectly in every conversation, but at least we at the bank are really trying to get our client advisors to delve into these subjects as much as possible with their clients, from both perspectives of diversification and as part of wealth planning. By engaging into these deeper level conversations, usually we find we are able to cement the client relationship better for the future.”

China – vast, enormous, huge potential

An expert agreed with these views, adding that life solutions fit very neatly into their firm’s holistic wealth management proposition. “We have enjoyed strong demand from our Chinese clients for insurance solutions,” he reported, “although like others we have since the pandemic struggled to service some of those Mainland clients out of our base in Hong Kong due to travel impediments. However, and luckily, we have different partners dotted around the world, and we opened a Mainland insurance desk that has seen strong demand. So, nowadays, we can capture the demand that is there through a variety of avenues, including through our Macau operations.”

Concerns over common prosperity

He told delegates that Mainland clients have some growing concerns about the common prosperity initiative of the government. At an economic leadership meeting in August, Chinese leaders agreed that China must pursue a goal of what they termed ‘common prosperity’, whereby citizens share in the opportunity to be wealthy as the main objective for the next stage of national development. They stressed the need for the economy to offer a smoothing out of wealth, in other words that wealth distribution and redistribution needs to become more of a proactive agenda.

“Clients there are genuinely increasingly concerned about the potential imposition of the estate tax or even gift tax in the future,” this guest reported. “They want to contribute to society but on the other hand, they want to see if there are solutions that allow them to bypass certain taxes legally. We have no definitive answer to give them, but insurance clearly has certain advantages, as we can see from developed markets around the world.”

He also pointed to the opening of their firm’s onshore insurance desk on the China Mainland, a move that has proven very popular and that is generating strong business volumes. He explained that many of these clients also have family increasingly dotted around the world, either for study or work, either temporarily or permanently. Accordingly, their firm’s mission is to address both the current and future onshore and offshore needs of those clients. “We are of course also trying to help them to reduce their tax burden overseas alongside enhancing their succession planning and structures,” he told delegates.

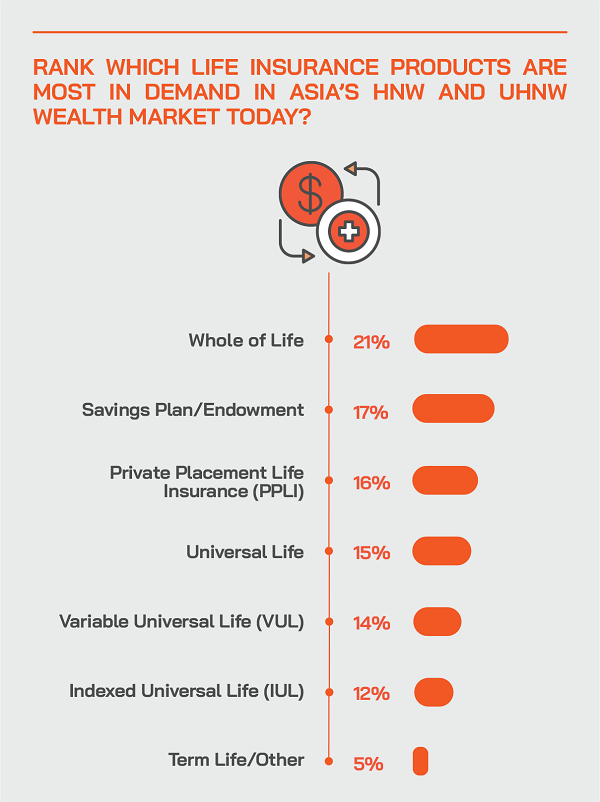

The product mix and key trends

As to what is popular from the life solutions menu currently, a panellist told delegates how the entire product mix for their firm in APAC had changed significantly in the last 10-20 years and even more rapidly in the past few years. “The traditional Universal Life (UL) has been diminishing in importance because of the reducing credit interest rate as well as risk premium, making it very difficult for this product,” he reported. “Accordingly, many more carriers have been offering alternatives, especially Indexed UL, Variable UL, and Private Placement Life Insurance. These are considerably more acceptable structures these days.”

He added that clients also like the Savings Plan, which in the past couple of years had grown robustly and had become a very unique asset class to help clients to diversify their portfolios as well as to stabilise their returns.

Savings Plans are firmly in favour

He offered more detail on the Savings Plan, telling delegates how this is a very useful tool for rebalancing portfolios, adding in new investments and generally raising returns as well as stabilise their entire risk exposures.

“The Savings Plan is very popular in Hong Kong, generating more than 40% of our revenues there,” he explained. “The product has been evolving constantly, and while a few years ago nobody was much interested, today it is leading the way in Hong Kong. It also resolves some key issues such as people’s unwillingness to step inside medical facilities for assessments and certificates. Instead, clients prefer to engage themselves into a Savings Plan and further their investment exposures and family succession planning in that way. And that is why it is especially in demand today.”

He also told delegates how the Whole of Life product is also increasing in prominence in this region. “Accordingly, we believe that with these various appealing options on the table, the product mix we offer clients today is well-balanced, with an interesting range of alternatives to suit their needs,” he reported.

Another expert explained that their firm in Hong Kong had also been selling a significant amount of savings plan policies, although they call it the Power Plan, as it is a participating whole of life plan. “It has evolved now today that you can even pledge your savings plan or power plan into a private bank to get leverage, so you can even get a more handsome potential long-term return from your policy,” he noted. “However, we have to be aware of what is happening to interest rates as well.”

Scrolling down the life menu

Additionally, PPLI and VUL type structures are of interest to those clients who are considering a full or part-time move to another jurisdiction, so clients like to transfer some of their assets to those types of vehicles before they make those moves, an expert reported. “Personally, I used to be a fan of UL, but those days have passed and because of the interest rate situation and the curve, those are now pretty ugly. Accordingly, the providers themselves have switched to whole of life, so that they can capture long-term money, more commitment, so there is room for more assets in the investment portfolio, and so they can provide the clients long-term growth.”

PPLI and other solutions are in favour due to portability and are also at an advantage in some jurisdictions around the world that are not quite so welcoming of what are often quite complicated and sophisticated trust and other structures that HNWIs put into place and that in some cases, present a somewhat negative scenario and impact.

“Let's say, in the USA, if you have an offshore trust, you have a negative tax implication, relatively compared to anything onshore, so I believe we often need something simpler,” he noted. “I think insurance is capable of filling this the gap, as it is not a highly complicated structure and is transparent.”

PPLI – part of the fireside chats in the US and Europe

A panel member observed for example that from the European perspective, it is commonplace planning to use life insurance such as PPLI in the day-to-day succession discussions. “This sort of progress is coming now in Asia and as I said, education and understanding is key to enabling such conversations,” he said.

As PPLI offers this element of portability, and many wealthier clients like to remain mobile, their families as well, he advised clients to think carefully about the value of such policies and their adaptability, both for civil and common law jurisdictions.

Moreover, PPLI is very well embedded into the global financial ecosystem, having been around for decades, especially in the US, and extensively in Europe and the UK, Australia also and the product has stood the test of time, and tests from the authorities. Insurance in general is a legitimate planning tool, it is well recognised by governments around the world, and there is major economic and political imperative for governments not to start messing around with people’s protection and the future financial security for themselves and families.

“Picking a solution that works for clients in their home country today, but knowing that at some point in the imminent future, they're going to move, give them something that is locally compliant with the legislation, have them use those strong regulations in their future country to their advantage, and make sure you've got something that is robust, and that is going to give them not just the fiscal benefits but ease of reporting, succession planning, all these are really valuable,” an expert commented.

Expert Opinion - Will Price, Head of International Distribution, ASEAN, Quilter International: “Next generations tend to be highly international-mobile, so their current and future residency and where the family assets are held create complexity and tax implications. It is vital to engage the next generations from the outset and having the client value propositions aligned across the families often helps building stickier relationships with next generations.”

Expert Opinion - Lee Sleight, Head of Business Development, Asia, Lombard International Assurance: “Customised solutions are needed and must be capable of catering to complex needs. Customised solutions may have many moving parts, all of which can be fine-tuned to work well together to achieve the specific aim of legacy and succession planning in a compliant structure. This is where PPLI comes in.”

Have PPLI, can travel

Another expert agreed that the PPLI product also fits very neatly into the broader wealth planning theme and agreed this was especially relevant for those clients who wish to be more mobile.

“The PPLI product, I think, fits very nicely into the investment migration and mobility theme, particularly for local clients who are more accustomed to a much simpler tax kind of regime in Hong Kong and who are emigrating full or part-time to a much more complex and complicated regime,” he explained. “There are many wealth people and families relocating from China, for example, to Europe, availing themselves of investment migration programmes to find a diversified lifestyle and an alternative base for themselves and families.”

A fellow panellist agreed, noting that his firm had been seeing quite a lot of clients picking up on the theme of portability and warming to the ability to take a solution that works today, that they can move around with them without having to restructure, whether it’d be in a civil or common law jurisdiction.

Expert Opinion - Will Price, Head of International Distribution, ASEAN, Quilter International: “As Asian wealth continues to grow, PPLI and VUL are legally recognised wealth structuring solutions facilitating clients’ growing, protecting and passing on wealth tax-efficiently. Today, clients are increasingly aware of wealth structuring solutions. To stay ahead of the game, bankers and advisors should no doubt include the core theme of wealth structuring in all client wealth planning conversations.”

Keeping it in the family

PPLI, an expert reported, is also advantageous for banks and wealth management firms as the assets themselves in the structure can stay with those banks and EAMs.

“The banks and other firms do not have to lose the AUM, which is sometimes a concern with traditional products like universal life, and others,” he explained. “PPLI basically changes the ownership structure of those assets to being wrapped in a life insurance policy, but the clients can keep those assets held within their chosen wealth institutions. That brings with it a number of advantages, it gives the policy holder clients flexibility, control, and the portability we have discussed. Having a product that can move, that you can perhaps divide into several sections and transfer parts of a product to the next generations, those are great advantages.”

He also said there are some potential tax advantages. “As government finances are stressed the world over, HNWIs might be an easy target for increased tax tolls, so clients need to consider how they're structuring their wealth post tax, and again PPLI offers that flexibility and portability and control.”

Flexibility is a key advantage

Another expert pointed to the value of insurance as a tax deferral mechanism, to help the client have more control over when he or she pays the necessary dues on accessing the assets and investments. “You have an established international recognition in the developed economies of how these structures work, the tax treatment, and a broad acceptance of the legitimacy of how they are treated within a succession planning perspective as well,” he explained.

Whilst assets are held within a product like VUL (as with PPLI), clients are deferring tax until a later date and also to some extent choosing where it might be due. An expert observed that the assets delivered into these policies become technically owned by the life insurance company, but life insurance companies are typically headquartered in tax efficient jurisdictions such as the Isle of Man and other centres, allowing for those tax savings are essentially passed on or deferred for clients.

Choosing your time and place

“That gives clients flexibility and choice as to when they potentially pay the taxes down the road,” he reported. “So, you're deferring that tax until such time as you take money out of the policy and that gives you that flexibility. You can then decide where you will be resident at the time of drawdown, you can decide if you are passing the wealth to the next generations so that they're utilizing their own tax brackets in the jurisdiction that they're living in. In short, these policies give you a lot of flexibility to manage that tax output.”

The other area that VUL in particular can help with this is that liquidity requirement in the event of a death. “Obviously, by having a higher death benefit that pays out in the event of a death means you have liquidity at that moment in time for jurisdictions where you have estate tax, inheritance tax and considerations to deal with,” a guest observed. “The UK is one such place, for example, where a product like VUL can provide that liquidity to fund the inheritance tax bill. Now in the UK, that tax bill has to be paid within six months, which isn't always easy for the size and complexity of the estates that HNW clients usually have, and it is therefore a key planning tool for such people and their families.”

An expert pointed for example to the potential for assets in a VUL policy exposing the policy to domestic taxes in Singapore or Hong Kong. “A very quick answer is the nature of the asset or the ownership of the asset is changed with a VUL policy or PPLI structure,” he reported, “to the effect that the assets are owned by the life insurance company, for example the Isle of Man, so they are taxed at Isle of Man rates because it's the life insurance company that are trading those assets, meaning no Singapore or Hong Kong exposure, for example.”

The closing words

A panellist closed what was a lively and highly informative discussion with the comment that whatever the course of the pandemic and lifestyle and travel restrictions, all of the insurance products and solutions will continue to be set within the broader contexts of more robust estate and succession planning. “Those major concerns are what are driving the market forward and helping clients select the right life insurance solutions for them and their families.”