Publications & Thought Leadership

International & Regional Wealth Managers – Improving the Digital Platform & Capabilities

Sep 23, 2020

On September 17, an eminent panel of six leading technology and wealth management experts assembled for a Hubbis Digital Dialogue discussion covering the world of digital technologies and how digital transformation is helping to develop the offshore and onshore wealth management markets in the Asia region. There is absolutely no doubt that the pandemic has further accelerated the drive towards digital solutions and delivery in the region, indeed globally, as face-to-face contact is so severely hampered. And it now looks like this situation is likely to remain for the foreseeable future. But the course of the digital journey has not altered – international, regional and local private banks, independent asset management firms and a range of new purely digital entrants have for some years recognised the absolute need to invest in digital transformation, from the back-end to the front-end, from seamless digital onboarding and KYC, through mid-office cost-saving technologies, RegTech compliance solutions and of course to a wide range of tools and solutions that can significantly enhance the capabilities and efficiencies of the client-facing relationship managers, thereby boosting relevance, client satisfaction across the different segments of wealth, and ultimately, revenues. The experts discussed the nature of the Asian wealth management market, defining the needs for the years ahead. They pondered whether this broad digital revolution is being properly embraced and if not, who might get left behind. They debated whether technology investment is being properly targeted and executed, and they considered how the wealth management organisations competing in the Asia region can best adopt and then assimilate these new technologies.

The reality is that much time and money can be wasted by not taking the right approach to digitalisation, but that smart, targeted investment with clearly defined operational and business goals in sight – all with the end-client’s needs and experience front of mind - can and will significantly boost their competitive position. An expert opened the discussion by explaining therefore that any well-organised digital transformation journey must be planned well in advance, the proponents must expect the project to take some years, and the mission should be to transform the business.

They looked at the inside-out approach, meaning they looked at transformation of what is on the front end but also on the middle as well as the back office, with three core angles, recognising the need to prioritise certain areas first, specifically for digital wealth. They explained that having built and solidified the platform, over several years, they are now looking at how to launch siloed features, and beyond that to really focus on what are the critical parts they need to address to really pivot the business to a whole new level.

Prioritise and plan

“It’s really based on business criticality,” they explained. “We really look at prioritising what's going to help address key clients concerns right away, what's going to deliver the maximum impact for our customer and for our business and really work towards that and the two key areas - the customer experience and also how we then leverage data and insights in a smarter way as we move ahead.”

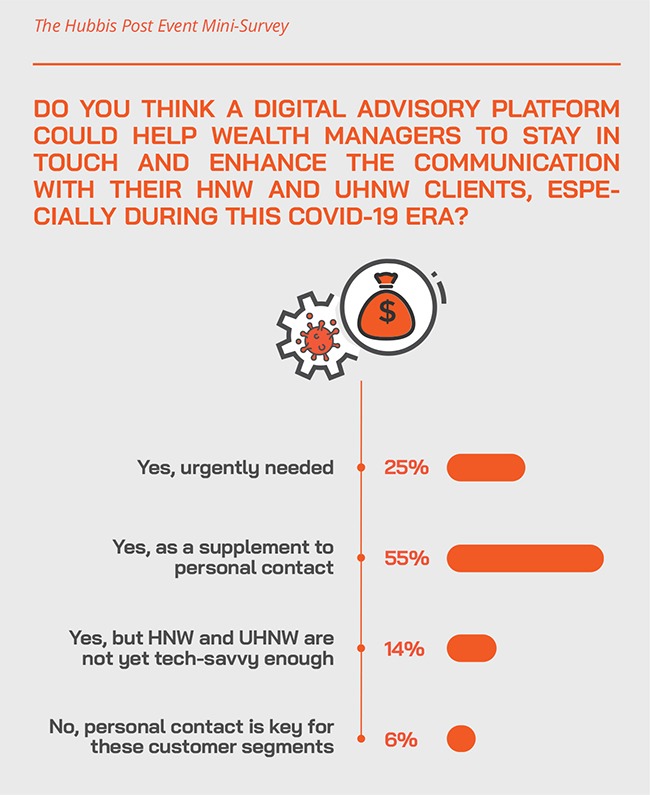

The Hubbis Post Event Mini-Survey

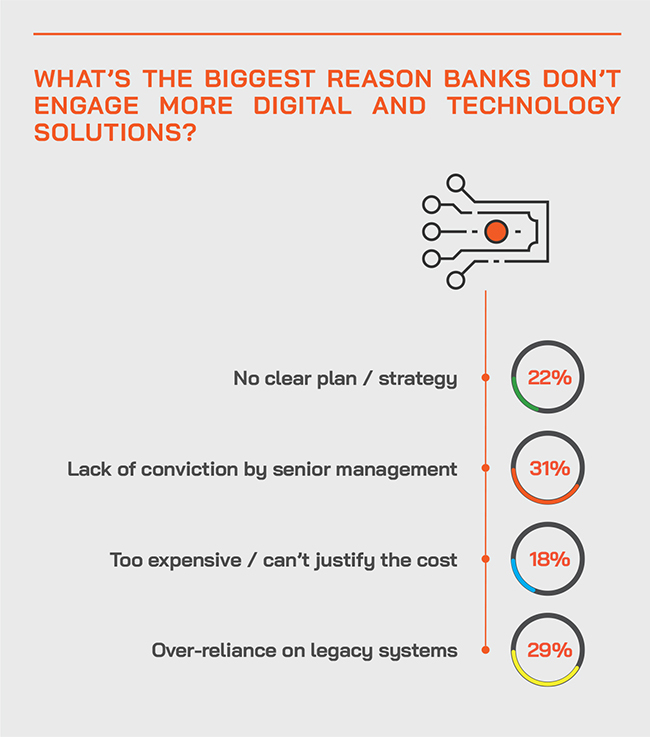

The results from our post-event survey paint a very clear picture. We have summarised these as follows:

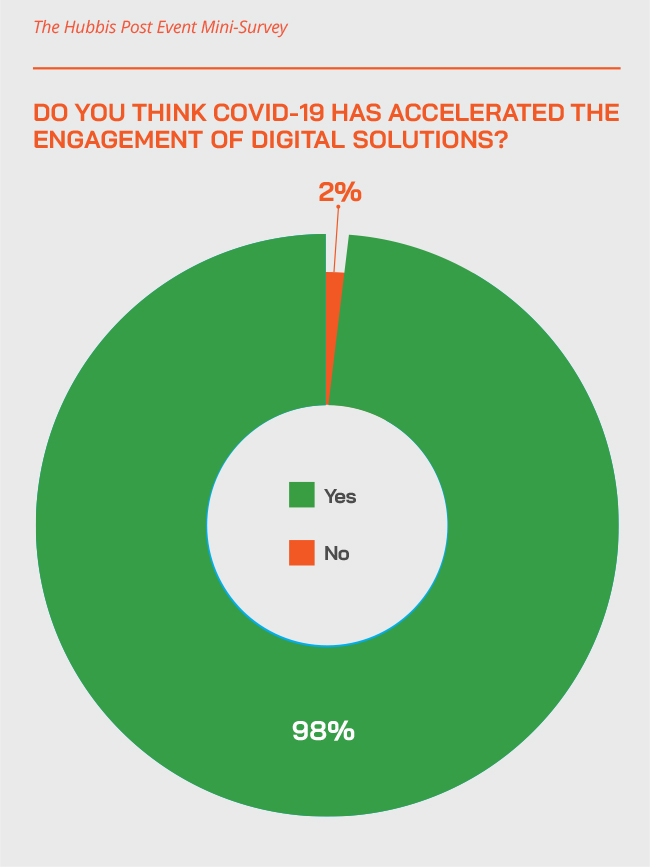

- The Covid-19 pandemic has dramatically accelerated the rollout of and engagement with digital solutions

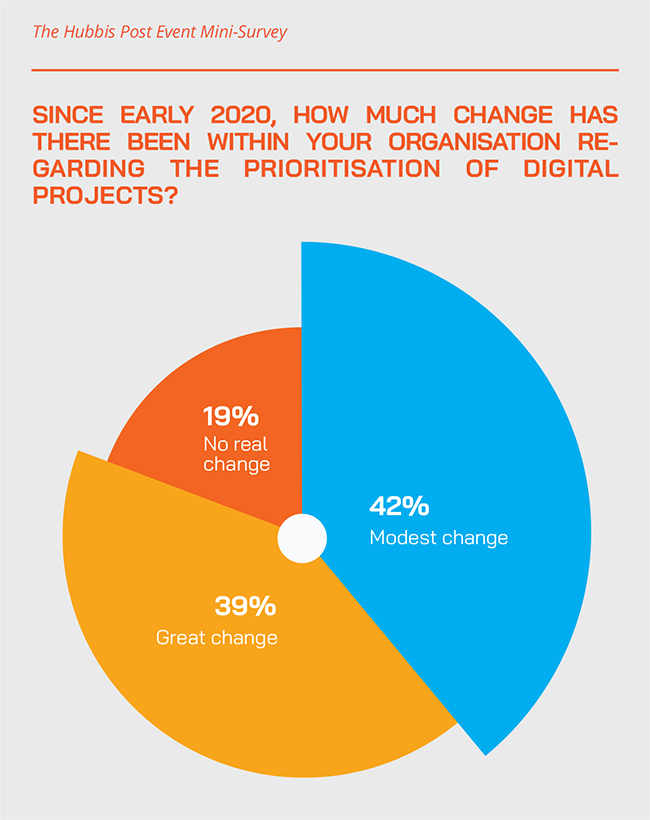

- Since early 2020, there has been a great change within organisations in how they prioritise their digital projects

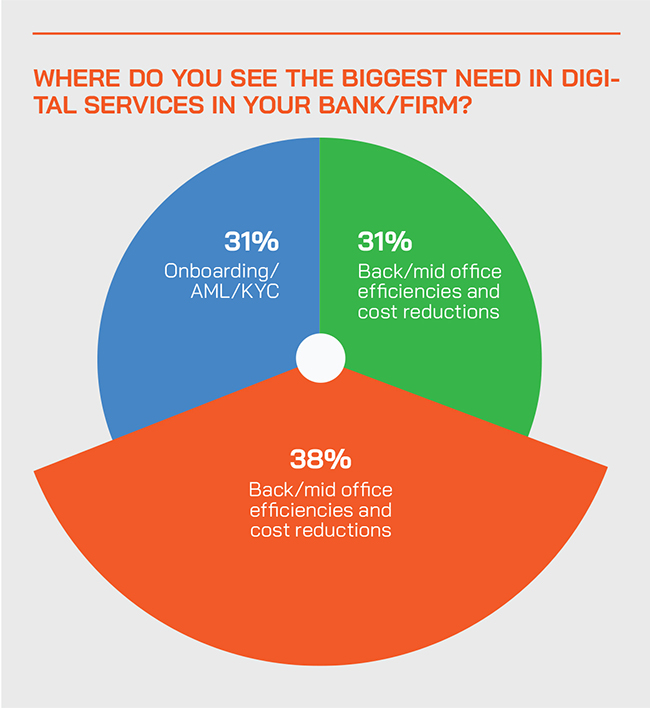

- Priorities are well balanced between onboarding/KYC/AML, the back- and mid-office efficiencies and savings, and boosting the capabilities and productivity of the RMs

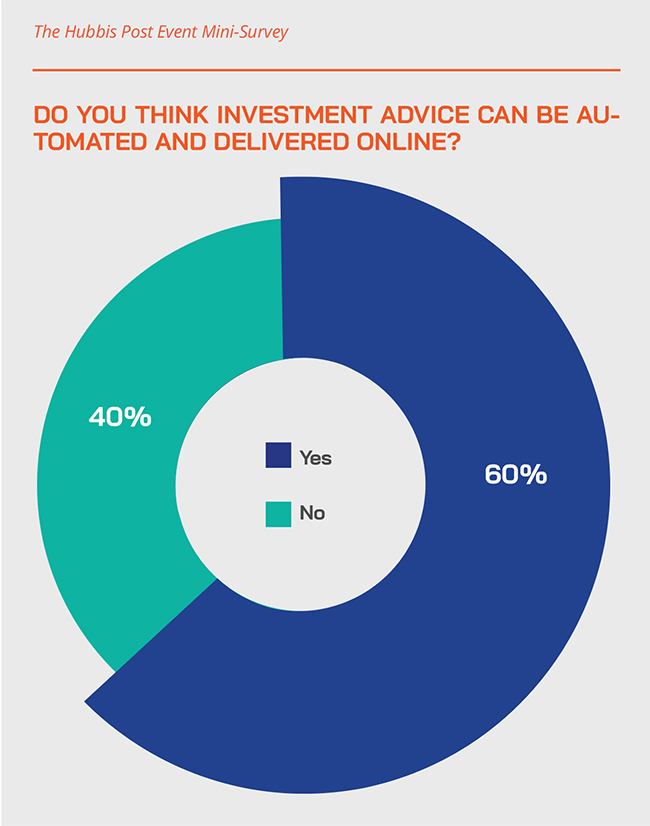

- 60% of respondents believe advice can be effectively delivered digitally

- 80% of replies indicated a digital advisory platform is both vital and effective during this time of limited face-to-face engagement

- There are several key reasons for poor use of and engagement with digital solutions, mainly the lack of a clear strategy and poor leadership decisions, but also excessive reliance on legacy systems and also difficulty in justifying the cost benefits.

Another panel member who focuses on core platforms explained that whereas back in the 1990s banks tried to do things themselves, today they're focusing on their core business which is being in touch with clients, developing the business, trying to get new clients, growing business with existing clients. He observed that the biggest global banking giants could continue on their own, can invest in their own solution, but the segment of banks with between USD5 billion to USD100 billion assets under management, at this level or size, partnerships are optimal to help develop these platforms in a more cost-effective manner.

Segmentation and geographic differentiation

“Regarding segmentation,” another expert said, “typically, the retail part of the wealth management business is faster in terms of going digital than the private bank, which relies more on relationship management and interpersonal connections with a client, but what has been achieved in the last five to six months in terms of going digital is more than what happened in the last 10 years.” However, he said that a lot of the activity is fairly basic advances, more scratching the surface with video conference calls, webinars, messaging with clients, video onboarding, doubling the number of people using the apps but the apps are not very sophisticated. “In short,” he said, “a lot more can be done.”

Expert Opinion - Kimberley Ho, Senior Vice President, Digital Wealth Lead, Consumer Banking Group, DBS Bank: “In the new norm, digital is now a pre-requisite for a sustainable business. In addition to seeing digital engagement grow amongst our clients, expectations have also increased. The client is now exposed to a far wider set of digital tools than ever before, hence it is imperative that we continue to improve and innovate our digital capabilities.

Expert Opinion - Sébastien Buchard, Chief Sales Officer, Directeur Adjoint, Sales and Relationship Management: “We believe that outsourcing of non-core banking activities are beneficial to banks not only from a cost but also from the functionality and time to market perspectives, and can act as a lever for continued innovation and business growth.”

Expert Opinion - Damien Piper, Regional Director, Asia, Finantix: “My hypothesis is that while robo advice has an important role in the toolkit of a modern wealth manager, technology will have more impact augmenting human advisors rather than totally automating investment advice leading to banks setting up pooled Advisory Desks to make human advice more efficient.”

Expert Opinion - Damien Mooney, Managing Director and Head of Aladdin Wealth Tech, BlackRock Solutions, BlackRock: “Aladdin Wealth continues to be a key enabler of wealth management industry transformation with our strong focus on data-driven business management, deep portfolio content and analytics in end-client engagements. This is allowing wealth managers to differentiate their value propositions in advisory and discretionary wealth management and ultimately transform their business models over time.

And with that, he highlighted the power of FinTechs and their solutions, as well as the trend towards M&A by global financial institutions that want to rapidly advance their wealth proposition.

Partnering for excellence

“In our experience in the past five or so years,” said another expert, “with the drive towards omnichannel, the drive towards mobile-first, what we've noticed is it's really become common for our customers not wanting to build, preferring to buy and developing via partnership where they would take our building blocks, and they would actually have their developers then work on top of that. So, what we see both in the very large banks, but also the challenger banks there is a lot more of a mode where they look to put together different digital artefacts to help them accelerate their programmes; that gets them live much faster, and it follows the general trend in the tech industry that I've noticed towards agile style developments and the roadmap style, as well as continuous improvement.”

Another guest highlighted how since the Covid-19 crisis the cloud solution approach has obviously gained a lot of pace, although that was a trend taking place well before that. “Cloud is also a much cheaper solution to implement now,” he stated.

The catalysts for change

An expert in asset management technology explained that their focus ranges from a simple advice type of engagement through robo-type solutions and then highly sophisticated portfolio advisory technologies delivered by UHNW-focused wealth management firms.

He explained that while as catalysts for change everyone talks about the customer experience and user experience ironically the most dramatic catalyst for change has been Covid-19. “That has been the accelerant for the industry, and as I see it, the reality is we will not go back to prior behaviour because people have got that experience around convenience and accessibility. Accordingly, the bar around that is going to stay high and wealth firms cannot at all be complacent.”

Seeing behavioural change

He added that the future of what they do would not purely be on the technology, but more around what they call engagement, adoption and commercialisation. “The real focus for us is behavioural change, nudging people into different better ways of doing things. Maybe accelerant number two will be when markets ultimately crack, as they might well, then the banks who have sat on the side not doing enough will be forced to towards greater digitisation, as it will then be really driven by saving costs and driving efficiencies.”

An expert raised the question of how a bank develops its core banking systems and interlinks seamlessly between various booking and execution centres.

Satisfaction levels rise

“We have some clients who have enjoyed the best increase of their satisfaction levels amongst clients during the crisis, because for them it has been a huge advantage to run one platform from several different countries,” he remarked. “As to the size of assets, either you have the critical size in one country, or the critical size for many countries but you need to be on one platform for all of them. When you want to open a new country, you just take and outsource a package or platform as it is with the back office services and the time to market to a new area is therefore much faster.”

He cited the example of a Swiss client that decided to open an entity in Hong Kong and Singapore. “It was impossible for them to develop everything themselves, even if they were a very strong player in Switzerland and they decided within four months to open in Asia with our existing platform.”

Post-event delegate Survey

Hubbis also asked delegates for their opinions on several elements of digitalisation in our post-event survey.

Hubbis: What are the key objectives you have regarding digitalisation within your bank/firm, and briefly, why?

- At the global/group level, we are in the midst of rolling out a unified portfolio advisory tool.

- For automation, and for productivity enhancement.

- The key objectives are to enhance work efficiency and better record keeping. Digitalisation with my firm can really help in data analysis and investment decisions, helping provide better solutions to clients. It is also helping general work efficiency as it helps avoid much manual work and helps prevents errors.

- Cloud storage, API, easy searches.

- It helps with understanding market trends relevant to the firm, helps us understand considerations for stakeholders and investors’ priorities.

- Digital offers client tools for intermediaries with valuable connectivity solutions and the end-client portal as part of our EAM value proposition.

- To best leverage our digital capabilities in providing great customer experience and helping our clients build better financial futures.

- Reduce cost, increase the scalability, more automated process, less paperwork, eliminate minor human errors, data accuracy.

- Cybersecurity.

- To enhance the RMs’ skills and to increase the revenue delivered by HNW clients.

- Optimising the workflows.

- Digitalisation is part of our business contingency plan, and the Covid-19 experience had made all companies speed up their digitalisation to keep business running in an efficient way.

- Customer service excellence.

- To harness the vast sea of information & data.

- To streamline our operations and processes to reduce operation/overhead costs, to meet the

- growing demands among the second generation and the millennials.

- There is some digitisation, but it is far from complete. The most obvious area is AML/KYC and Client On-boarding.

- Digitalisation also helps to eliminate transcription errors, there are no physical storage limits in the Clouds, while digital helps to integrate business systems to improve accessibility to information where multiple users can share and use the data at the same time to improve efficiency. The main objective is to improve communication and enhance access to critical information during a hiatus period, such as during this pandemic.

- It is good to have a digitalised system for EAMs where we can view all the bank accounts at once.

- For the mobilisation of the trading platform as customers are switching to mobile trading.

- At this moment in time, I would not dare have any objectives regarding digitalisation within our firm due to the close-minded mentality of our shareholders. As was hinted at in previous webinars, the key to digitalisation seems to be a common mindset across the entire organisation, which we do not have. Unfortunately, our digitisation initiative is limited to general client inquiries and WFH with next to no online platform for clients or any other fancy internal systems.

- We need to build for scalability but as we have grown from a small start-up with limited resources to begin with, much of the technology used have to be upgraded for rapid growth and scale.

Is your digitisation journey going to plan, or are there unexpected hurdles or delays?

- As far as the portfolio advisory tool is concerned, most of the key challenges stem from the compliance/regulatory constraints.

- We are actually on track.

- The digitalisation is delayed as the costs are high and there is a lack of conviction from the senior Management.

- There are some unexpected hurdles such as compliance and regulation issues which need to be overcome.

- Current market conditions have slowed things down.

- As planned.

- Good progress.

- The delays are due to the budget adjustments that my company is planning to have and the strategic planning issues.

- There seem to be plenty of unresolved issues.

- Digitisation is a trend and need, however, it is slowly undertaken.

- There are fewer hurdles and delays since the Covid-19 crisis, which escalated and accelerated the urgency to continue the digitisation journey.

- We are exploring opportunities in this space, especially with the government grants made available now for such initiatives.

- The digital journey is not easy and is expected to be slow; it requires knowledge, and it costs to have an in-house system connecting the digital tools. Maybe 5G technology is the way forward.

- It is slow at the moment and behind schedule. But we are hopeful that with a fresh round of investment from investors, we should be able to overcome current delays with a larger skilled team to expand our tech stack and scale.

In which key areas is digitisation making your business, or your working life more productive and efficient?

- It provides efficiencies to trade operations, investment and trade decision, record keeping, and easier to monitor business performance.

- Personal accounting, banking, payment.

- Account Opening and other day to day admin matters.

- Post Trade Execution Confirmation.

- Customised portfolio selection in line with ESG demands

- Easier submission of documents and servicing of clients.

- Communication, reporting, co-working.

- Marketing, operations.

- Time saving.

- KYC, investments and portfolio tracking.

- It is really cost effective to minimise the time for marketing and the needs for physical meetings.

- Online signatures and forms.

- The segment of order execution/management and video meeting makes life more efficient in particular under this travel ban environment.

- Client engagement.

- Workplace automation, remote working enablement.

- Reporting, order placement, credit control, client query, pitching, marketing, prospecting, risk control.

- The only positive has been the digitisation of our CRM app. Contacting and updating the client to follow their preferred method.

- AML/KYC and on-boarding of clients and data analytics, Financial Modelling and enhancement to help to improve better decision making and more accurate investment. It helps integration of business systems to allow multiple users to accessibility to information and improves efficiencies of business. Digitisation makes business more efficient and accessible during the unexpected period like pandemic of Covid-19 where business continuity can be carried out without difficulties and without any compromise.

- Ubiquity – we can be more easily accessible by clients when and where required.

- Accessibility - we can remotely access the office and work from home as needed.

A guest highlighted the segmentation between different categories of wealth and also geographic demarcation, explaining that their digital solutions and offering are tailored precisely to the end market clients. They explained they try to look at what is relevant for these markets, determining their priorities, and what key services they introduce where. “It is really important that we give them a consistent front be it offline as well as digitally,” they remarked, adding that for rapid growth markets, for example, India, Indonesia and Taiwan they have been accelerating a lot of their investment capabilities in this market, given that there's a surge in wealth and increasing demand.

Market specifics

“And for India and Indonesia,” they noted, “we took a deliberate approach into a mobile-first strategy given that these countries, they've pretty much skipped the desktop, so we see a surge in mobile uptake, and investments are very much focused on mobile as a channel.”

The discussion shifted to China, with the panel remarking on the immense onshore wealth management market potential there, but also the difficulty of entering that market to compete. “There are real challenges in China onshore,” they said, “and one of those challenges is there are no products. The bulk of the wealth is invested in real estate, because financial markets are not that liquid. However, it is changing, as there are more and more IPOs both in China and in Hong Kong. But the market is extremely volatile, perhaps because institutional investors are not that present to stabilise the market. You need institutional money in, and you need mutual fund money. You need more education of retail investors who are extremely volatile. You need money to move from real estate into financial assets as opposed to real assets; you need more regulation; you need greater expertise.”

China forges ahead

Nevertheless, he observed that what China already has is what he termed “an absolutely unbelievable digital experience”. “When we talk about digital, so acquiring the client online through digital marketing, onboarding online, everything in terms of getting the customer onboard, trading, offering support constructing portfolios online, managing the risk profile online, sometimes digital is first and physical is second. Yet out in China, digital is first, second and third. Anyone wanting to compete there has to have all those skills or as I mentioned earlier must acquire those skills either working with FinTechs.”

He explained that some of the major global financial organisations are building these vital complete set of digital capabilities and customers through acquisitions and then leveraging those into new markets. But M&A does not always achieve the anticipated results and the best deals can be incredibly expensive.

Another expert commented that China is indeed cracking the code. “We are really seeing digital wealth management at scale there,” he said.

Expert Opinion - Damien Mooney, Managing Director and Head of Aladdin Wealth Tech, BlackRock Solutions, BlackRock: “Adaptability and resilience are key to Aladdin’s capabilities to provide the firm and our clients a robust risk management system to help clients understand the impacts on their portfolios – for example through portfolio stress testing and scenario analyses.”

Expert Opinion - Kimberley Ho, Senior Vice President, Digital Wealth Lead, Consumer Banking Group, DBS Bank: “Looking ahead, we seek to better leverage data and technology to better understand our clients, be cognisant of their preferences, anticipate their needs and provide personalised propositions to address these – ultimately ensuring a best-in-class experience for our clients.”

Expert Opinion - Damien Piper, Regional Director, Asia, Finantix: “While banks are correctly now looking at how AI can assist RMs in highly personalised recommendations, I am finding many organisations do not have the data infrastructure that is mature enough to achieve meaningful results.”

Broadening the landscape

A vendor shifted the discussion to the broadening and accelerating landscape for digital solutions. “We have certainly been seeing greater speed of evolution and innovation across the various different markets that we're servicing, everyone from high-end private banks through to some mass retail growth managers. Some markets such as Japan have seen a slowing down, but others, for example Singapore and Thailand, have moved up a gear in terms of that delivery pace and that expectation, especially since the pandemic hit. And we have seen the private banks moving ahead at pace, introducing some truly cutting-edge innovations, for example in the way they use data.”

“Our role is really to help advisors and investors build better portfolios, but yet so much of the regulatory approaches around product suitability does actually lend themselves to helping advisors build really well diversified portfolios for clients, yet it's still in its infancy,” said another guest. “So, where we have really made the most impact is with the high net worth end of the market where they require the analytical and technological capabilities that we have to really build the portfolios according to their clients demand and need. It's quite easy to plug and play a digital wealth offering when you're building them based on publicly available stocks or mutual funds, perhaps ETFs. Once you've got a portfolio that's built with structured products, private markets, real estate, bigger and more complex portfolios, you need a different level of technological capability to do that. That is where we are focusing, asset management and the highly sophisticated end of the marketplace.”

Great opportunities ahead

He added that there are huge unexploited opportunities in the onshore markets, where there is so much wealth, and also for what he called scaled advisory propositions where you the providers aim to build a business where they can annuitise revenues. “If you look at the performance of some of the big banks and firms in the last six months, it looks like they're doing fantastically well with revenues, but AUM could be down because actually, a lot of that flow has been into flow type products. The opportunity is therefore into managed wealth in our industry, which is still much lower than it should be.”

A panel member highlighted how one of the key challenges faced in providing advisory related solutions for portfolio management to Asian clients is to aggregate and consolidate the data. “There is obviously dysfunction in the Asian markets where not only they are multi-banked but also multi-jurisdictionally banked,” he said. “So, the challenge obviously is to get a real portfolio oversight is to get data on a common platform.”

Aggregation: a key mission

“We are seeing propositions in the marketplace, with Canopy a good example,” said another expert. “They're looking to solve that pain point for a customer and I think that notion of aggregated wealth through one portfolio and there is a lot of value you can add around just bringing together disparate product holdings into a single portfolio, and have a single view of the portfolio, the overall risk exposures.” Accordingly, he said the notion of aggregated portfolio across multiple providers is certainly a priority mission, but it is as yet early days with the technology.

Expert Opinion - Sébastien Buchard, Chief Sales Officer, Directeur Adjoint, Sales and Relationship Management: “A partnership is a long-term commitment, choosing the right partner to suit the bank or wealth manager’s needs is crucial. To this end, Azqore conducts a thorough study prior to onboarding a new client to ensure that requirements and expectations are clear from the beginning.”

Expert Opinion - Damien Mooney, Managing Director and Head of Aladdin Wealth Tech, BlackRock Solutions, BlackRock: “We partner with wealth managers to enhance their value proposition to their end clients. The Aladdin Wealth platform provides a common language across the investment lifecycle and enables a culture of risk transparency to equip wealth managers with the information they need to make investment decisions and understand the impact on client portfolios.”

Expert Opinion - Kimberley Ho, Senior Vice President, Digital Wealth Lead, Consumer Banking Group, DBS Bank: “Our ongoing investments into digital have enabled us to scale and adapt quickly when Covid-19 emerged. Digitising of processes across the front, middle and back-end, have left us well equipped to serve our clients effectively.”

Expert Opinion - Damien Piper, Regional Director, Asia, Finantix: “My view is that the build versus buy debate is dead and that modern wealth managers are building journey-based digital experiences that pull together a series of best of breed APIs.”

Another guest highlighted how self-directed trading this year had also ballooned, estimating a roughly five-fold increase in online trading requirements. “I believe that is here to stay,” he stated. “And we see this demand from retail through HNW customers.”

MFOs, SFOs and EAMs – expanding fast

Responding to a question from the audience around family offices and IAMs/EAMs, an expert note that this sector is growing very rapidly, and that portfolio aggregation needs are rising sharply amongst those customers. “But actually,” he noted, “they are growing fast but from a very low base, so it is far, far more developed for example in Switzerland than in Singapore.”

The discussion closed with the panel agreeing that there remains much work to be done in all facets of digitisation, from improving cost-income ratios to enhancing the capabilities of client-facing bankers and RMs, to portfolio formulation, aggregation, open banking, and so forth.