Publications & Thought Leadership

India’s Wealth Management Market: Embracing a Remarkably Bright Future

Jan 13, 2022

The trajectory of the Indian wealth management market remains the same, but the speed of travel in certain directions has accelerated due to the global pandemic. Hubbis assembled a panel of wealth management leaders on December 21 for our final Digital Dialogue of 2021. The panel of experts Hubbis assembled cast their expert eye over a variety of key topics, including market development, the growth outlook and challenges across the different segments of wealth, the democratisation of the wealth management offering in India, the evolution of the onshore investment universe, the efforts to shift the model from transactional and self-directed more towards advisory and discretionary, the expansion of estate and succession planning amongst the upper echelons of wealth, and the search for talent to help the industry expand in the decade ahead. The panel highlighted the main evolutionary trends and will zoom in on the incredible potential that the hugely populous country has, especially (hopefully) when its economic growth gets back to its full dynamism in a post-Covid world. A vital topic in such a vast country is the rise of digitalisation in India, itself one of the fastest-growing technology centres in the world, and the panel agreed that there is much more to achieve on the road to digital transformation and optimisation. Amongst the key characteristics of India’s wealth management market and approach has been a very high-touch client engagement model in the higher wealth segments, and while the pandemic has impeded this type of personal engagement, the panel analysed how the banks and other players have coped, what digital tools they have employed, how personalisation and hyper-personalisation are evolving and why, and discussed how and where digitisation has been helping the incumbent players cope with the new normal and the new age of wealth management ahead.

The Panel:

- Arpita Vinay, Co-Head, Centrum Wealth

- Anshu Kapoor, President & Head, Investment Management, Edelweiss Wealth Management

- Anupam Guha, Head of Private Wealth Management & Equity Advisory Group, ICICI Securities

- Lakshey Gangwani, Regional Sales Director, InvestCloud

- Aman Rajoria, Managing Director- Head Private Bank, India, Standard Chartered Bank

These were some of the key questions addressed by the panel:

- What has been happening in India’s wealth management market, and what are the key developments ahead?

- Is growth sustainable even if the equity market were to cool down?

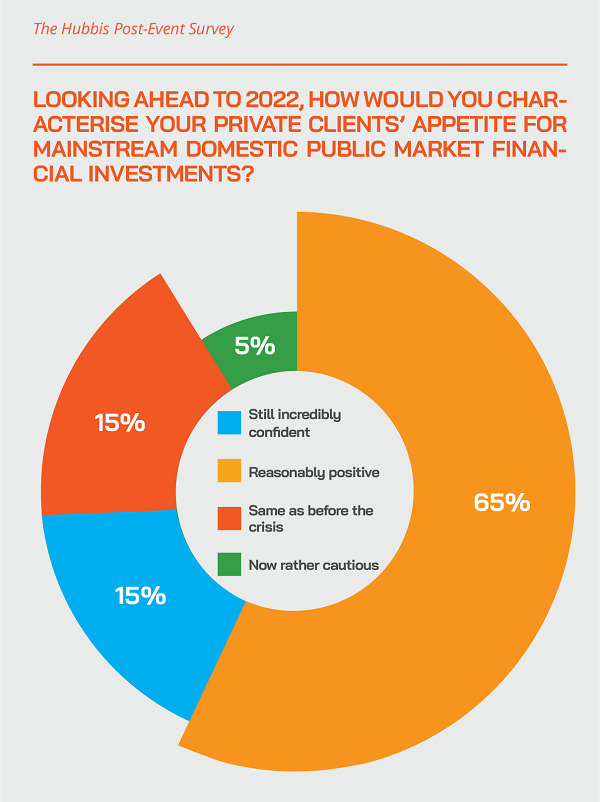

- What are India’s wealthy private clients investing in, why and what is the outlook?

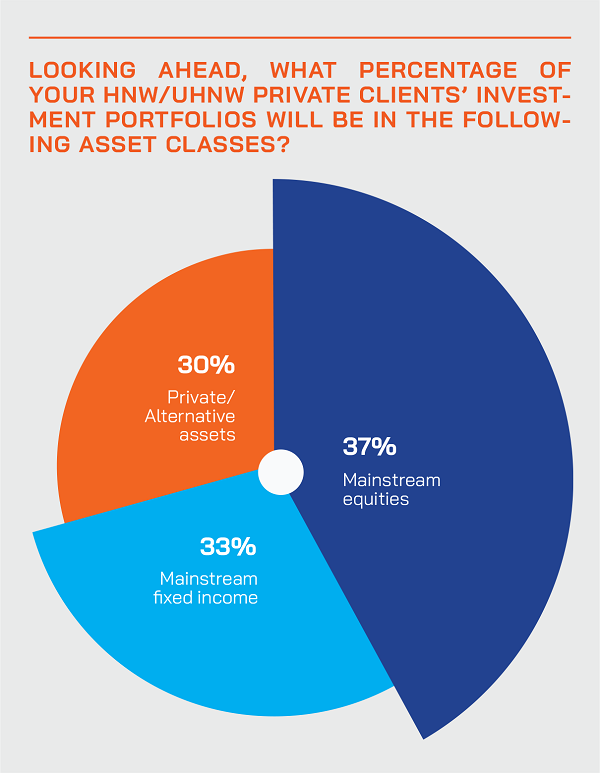

- Are alternative assets of increasing importance for HNW and UHNW clients?

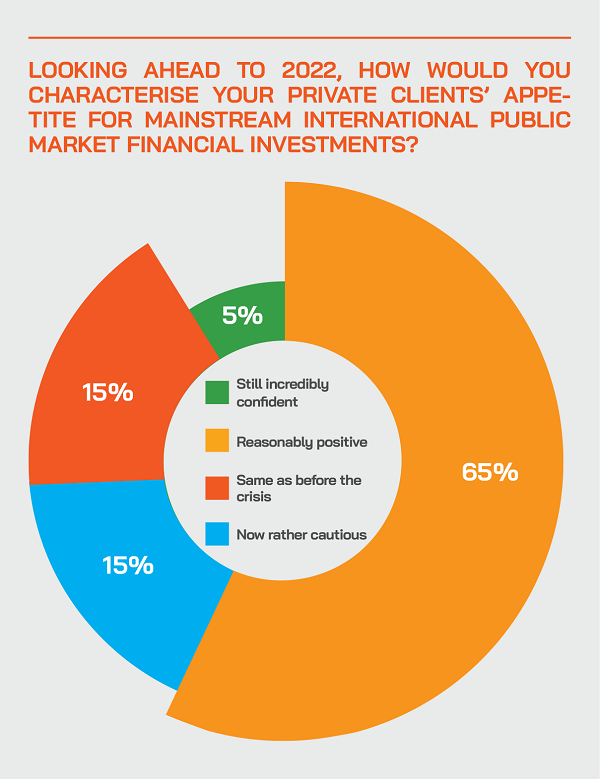

- Are India’s private clients investing more into international assets, and if so, why, what and how?

- What is happening to the world of investments in the vast mass affluent space, and how can these clients be properly reached and serviced?

- What are the key enhancements the banks and other competitors have been making to their value proposition, products and service offering?

- What is happening in the world of estate and legacy planning, and what are the key ingredients required to successfully help private clients in these endeavours?

- What is happening in the life insurance market for wealthy Indians, and how is the wealth industry catering to these needs?

- What about India’s next generations of clients? How can they be reached successfully and engaged with properly?

- The transfer of wealth across generations – how is that evolving in India and what are the implications?

- How is technology helping the banks and other wealth management firms engage with and properly service their clients and prospects?

The Key Insights & Observations from the Panel of Experts

2021 in India – a remarkably good vintage and a solid platform for sustained growth, diversification and dynamism ahead

A guest opened proceedings by reporting how great a year it had been in 2021 for India’s wealth management market. “Nobody really expected how bullish things would turn out across asset classes,” he reported. “India is in a very good position from many different aspects, so we expect some of the bullishness to continue. A key trend we are seeing and getting deeply involved in is the rapid development of the private markets in India, which have already become both rather sophisticated and large. Over the last 10 years, you might be surprised to learn that the amount of private equity that's come into this country exceeds the FDI inflows to this country, which is quite incredible. India now gets about USD40 to 45 billion of private equity every year, and the average for the last five years is about USD35 billion.”

India’s wealth market in 2021 has proven itself to be remarkably agile as well as dynamic, hence the great potential ahead

A leading banker reported how dynamic the Indian wealth market had been since the recovery from the onset of the pandemic in 2020. “After early uncertainties, the Indian wealth management industry has emerged much stronger,” he stated. “The entire industry has been able to navigate with agility, changing and adapting with the changing times. Smart technology has been adopted and we have embraced the new normal. There is some face-to-face activity as well, and the combination of digital and personal is, I think, the way forward for all of us.”

Far greater activity, although uncertainties remain, and volatility lurks

The same expert observed how the very buoyant equity indices and IPO activity had helped private wealth creation, although external factors including the pandemic keep advisors and investors on their toes in terms of how to play the market. The demographics are also highly favourable, with the older generations looking more towards estate and wealth planning and the younger generations planning more for their financial futures and later retirement. “And the Gen X are in the phase of wealth creation and accumulation, and all of these elements offer all of us all a key role to play.”

India’s Alibaba moment as the capital markets evolve and more directly reflect the new era underlying economy

A guest reported that there was a “beautiful transition” of the capital markets in India underway. “I call this India's ‘Alibaba moment’,” he stated, “and what I mean by that is that the US market transformed with major new era, with new age listings in the years 2000 to 2010 such as Google and others, and then China’s Alibaba listed in 2014, followed by a spate of Chinese new age companies that came into the markets and transformed the markets.”

And that, he said, is where we are in India today, right at that inflection point, and the index will look very different three or five years down the line, with a spate of new age companies heading to access the public markets. “It is beginning really,” he explained, “and even though we have seen the highest amount being raised in IPOs over the last 10-12 years, but I would argue that this will continue, and exciting times are ahead in the public markets as well.”

India has also seen significant diversification of markets and asset classes amongst private clients

Another expert highlighted the robust returns across a broadening array of asset classes in the public and also private markets. “Most things investors touched in last two years have turned into gold,” he commented. “As a natural extension, the wealth management industry which services these investors particularly HNWIs and ultra-HNWIs is booming too.”

The demographics are extremely appealing and support the vision of an even more dynamic future

This expert also pointed to the expanding Indian economy, rising per capita income and increasing urbanisation as tailwinds for the wealth management industry. He noted that the number of mass affluent middle-class people is also on the rise, explain that the World Economic Forum estimates that 80% of India's population will fall in the middle-class segment by 2030, up from 50% in 2019. “This will all produce strong growth in our business,” he stated. “So, we see growth across all segments, from the mass affluent to the hyper wealthy billionaires, of whom there are more and more.”

Priorities are changing for some key segments of the market

A guest reported how there is greater inclination towards prioritising goal-based planning over financial accumulation. There is also increasing demand for alternative asset class versus traditional public market assets, with rising allocations to private or alternative assets and to globally diversified portfolios. There is also a greater expectation of quality and service from the clients, especially the first-generation entrepreneurs. And the wealth in India is now more diversified across the country, not only in the major urban centres, meaning that wealth managers need to access those other customer opportunities the country offers.

Adapting to the key trends with agility is essential to the delivery of a new age wealth management offering

“A lot of us are maybe serving one category and this whole transition to try to straddle different, and very large and growing, segments will be of great interest as it unfurls,” a panellist said. “There is a lot of excitement ahead in delivering all of these products and innovation across this dynamic and rapidly growing market.”

He elaborated ion these views, noting that differentiation in the world of wealth management must centre on solving the needs of customers. “When I put on my investment management hat, I see four large unsolved needs of our customers,” he reported. “The first is access, so for example reckon 98% or more of India's best new age companies are owned by global private capital and we need to give India’s investors greater access to them. Secondly, we need to deliver a post-tax yield on investments that is higher than inflation. Third, we need to address volatility, as every three to four years, clients end up losing 30% to 40% of whatever they invest in equity markets, so we need to manage volatility better. And finally, we need greater diversification, as 99% of our wealth is onshore in India, and we need to boost access to and understanding of international investments. And in all these areas, we can prove our differentiation, because our thought process begins with the customer.”

The product suite is being revamped to make them more customer-centric and accessible

The same expert also noted that traditional products are getting rebooted. “Mutual funds and other products are all getting rewired, there is more innovation happening, and they are becoming more transparent,” he reported. “Meanwhile, as products become commoditised, the pricing obviously goes down, but service levels go up, you can create stories around the products, baskets around them for clients to make decision and easily move from one asset to the other, or from one fund to the other, based on how they would want to look at the market. And we can be more efficient, for example crediting the clients with their money from a stock sale within a matter of minutes, that is a real ‘wow, real innovation. And we can offer lending to these customers based on their holdings, and do it all digitally within a few clicks. The more seamless the journey and experience, and given that many products are commoditised, the user experience will really make these clients choose one bank over another.”

He added that there are more products as well as more international products available, “There are the newer age products coming in, for example direct indexing is a big one, passives are increasing, there is more smart beta, there is greater global allocation,” he reported. “And we must make it easy for the customers, offering the same simple access to US stocks, for example, as to local shares, providing similar levels of information and insight, recommendations and advice. And we need to really focus on lending, as for the major banks, there is a huge opportunity there, and big data and analytics will play a key role there, boosting access and delivery of all types of loans, from mortgages to personal loans, to business loans and so forth. We need to be able to cater to both the personal side as well as the business side of these clients.”

Catering to rapidly evolving segments of wealth in India is immensely challenging but potential hugely rewarding

An expert highlighted the rapid growth of the mass affluent segment in India, pointing to a survey they conducted. “We found, for example, that many of these Gen Z and Gen X actual or potential customers do not like mutual funds, they see them as boring and ‘fuddy-duddy’, they like cryptos, ETFs and so forth. So we need to bear all this in mind, devising our business strategy, choice of products, and the choice of delivery models around these realities. Those people are the future, after all.”

He elaborated on these views, noting that on their mobile trading platform and the mobile app, there are more and more low age yet high income clients, for example IT professionals who love to invest and trade actively. “To cater to this smart, sophisticated sector of the market we realise we should go and partner through an open API and build alliances to deliver to this growing segment. We cannot do everything ourselves. So, we need to find people who can build these additional solutions, in order to deliver true service to the customer.”

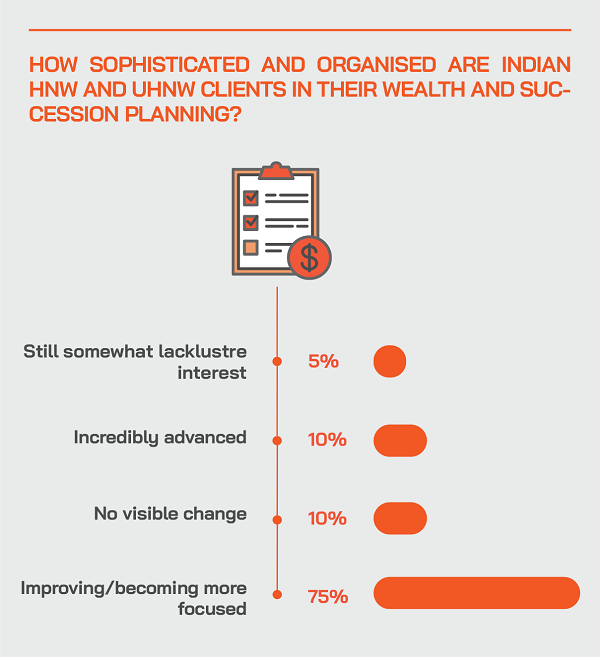

Estate, wealth and legacy planning is a boom sector of the wealth advisory business in India as demand soars

Indeed, in terms of the ability to adapt rapidly to the changing and evolving needs of clients, a wealth management leader explained that their firm covers the full spectrum of wealth management business, from gathering and then looking after clients to investments, as well as digital transformation and align their ‘big picture’ strategy accordingly.

They explained that the ‘softer’ side of client advisory, centred on wealth, estate and legacy planning was a boom segment in India. “The past couple of years has seen great uncertainty offering us a significant opportunity to help focus our clients on estate and legacy planning, which has increased significantly within our business, with the dedicated team having now expanded to four professionals and their output more than double in the past 18 months what was achieved in the previous three years,” they reported. “The coverage ranges from advice on creating documents as simple as Wills to far more sophisticated structures for holding assets and for later transitioning wealth amongst the generations and other beneficiaries.”

This expert also noted that leading business owner families in India had had to sit up and take notice of what can be termed a “seminal judgement” in May by the Supreme Court of India opining that any lenders could recourse beyond corporate obligors to the personal guarantors. “That made many promoters sit up and think a lot more carefully about the way they structure their assets,” they reported. “Indian families would in the past commingle their private assets and their business assets, but there's a lot more work and thought that's going now into more appropriate structuring.” She explained that, accordingly, there is significant progress taking place in overcoming these challenges of compromising personal against business assets.

The guest also pointed to the increasing globalisation of the larger Indian business families. “There is an increasing cross-border footprint, and that means in areas such as inheritance tax there needs to be a lot more thought going into structuring it all properly,” they explained. “In all these areas, there is a lot more thought, a lot more work and a lot more activity, meaning that our estate planning desk has seen dramatically higher activity levels in the last 18 months.”

“There is a great opportunity in all these areas, and as Indian clients spread their financial and immovable assets worldwide, as they need to consider inheritance, their next generations and therefore need to address a wide variety of structuring and estate planning issues,” this guest continued. “And it is not easy, look for example at the UK, where in recent years the whole concern about domicile has impacted matters hugely. For example, you could have been an Indian national, essentially living in UK but not subjected to the global inheritance taxes but all that has become a very real concern now.”

As the wealth industry is increasingly competitive and commoditised, differentiation must increase, and talent must be nurtured

The same guest explained that as the Indian wealth industry is increasingly competitive and commoditised, differentiation must increase, and indeed customers are highly demanding, and their needs constantly evolve. “The wealth management business revolves around three things – Platform, Processes and People - but people are the most important part of this business,” he observed. “As a business, we deal with entrepreneurs and professionals who are our core base, we provide them with solutions to adapt to the new realities around them. Wealth management services in India is still at a very nascent stage, but there is rapidly growing demand amongst the higher segments of wealth, driving significant growth in the need for our services and the expectations of those clients. A negative is that the talent pool in our industry has not grown as much.”

Yes, there is a shortage of talent in the wealth industry, so banks and firms must be agile and imaginative

Another expert agreed and highlighted the very real concerns about the relative lack of talent in the local wealth industry, compared to the potential growth in the market that surely lies ahead.

“The talent pool and the cost structure are really important problems facing us,” they reported. “Firm-specific attrition rates have been very actually and perhaps up to 60% of employees are at their firms or banks more than five years, and all in all it is difficult to find the right people. When you look at talent, there are two key things that you pay for, firstly the access to the client, and then the RMs’ skills and their understanding of markets and their behavioural and emotional tenacity to handle matters for their clients. The readymade talent is therefore someone who is at another private bank or firm who has enough access and who has enough experience. That is the kind of talent everyone is running after, and two-thirds of our talent comes from that pool.” But it is of course costly to bring that sort of talent over to any competing bank or firm.

They expanded on these comments, noting that there might be people in other sectors, for example the high-end luxury market, with the right access to clients but without the expertise in private banking. Similarly, there might be those with the right understanding of the financial markets and discussions but who do not have the necessary access to the clients out there.

“It is a challenge,” this expert observed, “but we are also prepared to experiment in the way we hire. We are prepared to take on RMs with the right access and then spend two to three years taking them up the curve in our industry,” she said. “And we also have some excellent performers this year from an investment banking and corporate banking background, and we help them expand their connections with the clients. In short, we are imaginative and flexible, and combined with low attrition rates at the firm, we are quite well positioned.”

Expert Opinion - Lakshey Gangwani, Regional Sales Director, InvestCloud: “In 2019, BCG stated that if you improve your frontline experience, you will see an upside of 8% to 15%. I believe there must be more investment into making RMs more productive, because producing hybrid platforms without RM education is not cost nor client effective.”

Digital-driven personalisation is essential to success in India’s wealth market of the future

A banker observed that given the overall picture the panellists had painted, the wealth industry will have to continue to play smart, to use technology, boost advisory, to use smart analytics in order to really reach out to clients and create hyper-personalised journeys. “Amongst key themes that have emerged in the last one year plus for the entire wealth management industry we see tech-first or digital-first, creating an ecosystem for clients,” he reported. “Given that you've sharply segmented your clients, you want to then hyper-personalise the journey and the experience. And for that, one will have to create an ecosystem, so there has been a fair bit of innovation on the product stack and there's been a fair bit of innovation on the delivery stack, and all the while keeping the client in the centre.

Another expert concurred. “So far, we have all really only scratched the surface of digital transformation actually,” he said. “We might now be able to digital enable investments, but some of us are trying to deliver even more complex solutions digitally, or with a hybrid model, so, the great interplay of a human and technology is emerging.”

Digitisation – the journey continues, and the direction is omni-channel and where possible at higher levels of wealth, significantly human-centric

Another expert expanded on the topic of digitisation, noting that the ability to deliver more seamless transactions and reporting had improved markedly in a short period. “Many areas of friction have been eliminated,” he said, “so much of that heavy-lifting has been done. It is now important to deliver advice, both omni-channel and the hybrid approach, where the role of the RM is transitioning to more of a problem finder and solver and away from nay of the more mundane tasks that they faced each day. With greater freedom and more tools, they can help address client needs and offer the right solutions, delivering with both digital and human interface.”

And he said that his firm’s platform already offers an edge. “It appears to me that this omni-channel, hybrid model will have value as we move forward, which is what we have seen in the most evolved markets. The role of the human advisor has not gone away, and we see that in the US, the top four or top five advisor firms or wealth managers will have about 60,000 to 70,000 advisors. And the real point is how your existing customers will evolve, and how the customers of the future will evolve and positioning for that evolution.”

As digital transformation remains in full swing, the ever-smarter suite of technologies and solutions can open more doors and leverage more business

An expert pointed to the ongoing efforts across the wealth industry to smart digital transformation, especially in expediting the use of AI, machine learning, next best action, and gaming theory into what they are offering. “The client wealth journeys need to be hyper-personalised,” he commented. “There is a substantial need for getting into hyper-personalised journeys, and what we have seen in India and other markets is as more people move online and they become more comfortable with platforms, the ability for a bank to deliver hyper-personalised journey is improving. It used to be an impossible task. But they are getting there by the use of AI, machine learning, using the right data, analytics and so forth.

“Where I think it really helps banks in India is because the target demographic is so large, the numbers are huge, meaning that while a hyper-personalised RM assisted journey could be a solution for ultra HNWIs, you need to cater to the HNWIs and the mass affluent segments, and those are also relatively large in numbers, so it is a major challenge to bring in this hyper-personalised journey to all those customers.”

Additionally, he agreed that there is a shortage of talent in the wealth industry. “I see it everywhere,” he reported, “nobody says there is an abundance of talent, so we are seeing the banks now focusing on enabling and boosting their RMs with technology, making them able to deliver more hyper-personalised solutions, and to make them more productive, to give them the edge over competitors, helping them truly transition to advisors.”

Hyper-personalisation manifests itself in two key areas of wealth management – platform and content

The same expert also offered his own insights into how hyper-personalisation plays out. “It can manifest itself in two ways,” he reported. “One is on the platform side, and the other is the content side. Regarding content and ideas, the banks can follow the lead of YouTube of LinkedIn and so forth, honing their offerings based on usage by customers, what they are liking and offer real customisation that is adjusted all the time. The same is possible in wealth management, where the banks and firms can constantly learn about your portfolios, your interests, your preferences and so forth. This helps them deliver very structured, very targeted information to customers, and propose next best actions and so forth.”

And on the platform side of hyper-personalisation, the banks are increasingly being benchmarked against social platforms, so the customers want to see an experience that works for them, that fits their choices and preferences. Some want to see more content-based experience, some want to see a more statistical experience, with graphs, charts, and so forth. So, with hyper-personalisation on the platform side, you are giving the customer a platform of their choice. And when you map all these together a hyperpersonalised platform, hyperpersonalised content and ideas, then you would have something like a super hyperpersonalised experience, if I can take that superlative word right now.”

Wealth management is and will remain a personal business, especially for the upper tiers of wealth, so digitisation must align with human connectivity

A panellist commented on their firm’s commitment to digital transformation, noting that across the HNWI and UHNWI segments, the firm focuses on omnichannel with a rising level of RM interface the higher the wealth of the clients. “The communication interface, transaction processing, even equipping the clients with detailed analytics reports occur at the touch of a button,” they explained. “But the final advice and the delivery centre on the RMs who will continue to play a major role for us. In our key HNW and UHNW markets, we will continue to see a good combination of high touch, and whatever can be, communication and engagement, but with a lot more productivity supported by technology, while in the broader mass affluent market, the primary engagement will be led primarily by technology.”

The opportunity is so vast that the drive to digital transformation is not a luxury, it is an essential

A guest reported that his institution sees a market of some 1 million people with more than USD1 million to invest, and that the mass affluent segment is some 20 million people with more than USD100,000 to invest. He concurred that there is a shortage of talent in the market as well. “So, the challenge is to service this vast number of clients across multiple locations, multiple cities, numerous states in what is a huge country,” he said. “And that is where the omni channel model wins, and we need a sophisticated and established platform to reach, onboard and service these customers, to navigate them according to their needs and preferences across investments, insurance, borrowing and so forth. We need tech to be able to nudge the customers in terms of the next best action, to help them with goals-based investing or life-stage investing, lifestyle investing, and other curated journeys.”

Some people, he said, will be able to navigate their own directions, but a large part of the population where wealth creation is happening would need hand holding. “And that is where the omni-channel model will work very efficiently where both tech and the human talent is able to engage with the customer in a meaningful manner,” he observed.

Expert Opinion - Lakshey Gangwani, Regional Sales Director, InvestCloud: "Wealth continuum will become a very interesting conversation. Those financial institutions that operate across the spectrum have a big advantage, because they can start when the customer is at retail or mass affluent level and nurture them from there. The question is how do you nurture clients from the retail level into a multi-generational client?”

Agility and dynamism are essential in the new age of wealth management in India

A guest closed with the prediction that the wealth industry will require great agility and imagination to cater to the different segments of the Indian wealth market of the future. “Some 10 years back, we used to only segment by income, and it was all rather basic, categorising them as older generation business builders, newer-gen entrepreneurs, wealth inheritors, family offices and so forth,” he remarked. “But I think as we go along, the whole approach to segmentation is evolving and emerging in this country, and it is really quite fascinating. Whichever firm can get their head around this, who can deliver to the major segments that are emerging, that can truly build the proposition for them and find a way to deliver that properly, those business will win and win beautifully in this market. And that is exactly how our firm and other leaders in the business are thinking.”