Impact Investing & Asia’s Wealth Management Market – Aligning Interests and Opportunities

Jul 20, 2021

In collaboration with responsible investment fund manager Regnan, an affiliate of J O Hambro Capital Management (JOHCM), Hubbis conducted a mini-survey of 436 senior wealth management industry professionals across Asia to ask for their insights into the drive to boost impact investing amongst their clients. We have summarised their numerous views here into this review of what is clearly a segment of the investment world that is gaining increasing traction across the vast Asian private client landscape. We hope that we have not only gauged the state of the market, but that we now also better understand the inclination of participants towards impact investing, what the limiting factors might be, and what the central characters believe they can and should do to encourage greater participation from amongst the key wealth market protagonists in Asia.

Impact investing amongst Asia’s wealthy investors is at a relatively early stage compared with the participation of the region’s high-net-worth and ultra-high-net-worth peers in the US and Europe. But from a very low base, mostly driven by Australia and Japan and pockets in the major centres in Asia, the growth is accelerating. There are more and more parties aiming to deliver education and ideas, and there is a growing body of products and opportunities of all types – from private equity and private market offerings to dedicated private or public bond issues, passive ETFs as well as actively-managed fund strategies.

The Key Findings in Brief

Growth aplenty across the world, but Asia’s wealthy private clients are behind the curve

Private sector impact investing across the world has been growing apace, as part of the worldwide drive to sustainability and alongside the growth in Environment, Social & Governance (ESG) driven investing. In the private wealth management market, UHNW and HNW investors in the US and Europe have been driving these trends, along with mass affluent and even retail investors. Asia is slowly beginning to catch up, and therein lies a great opportunity for key participants in Asia’s wealth management industry.

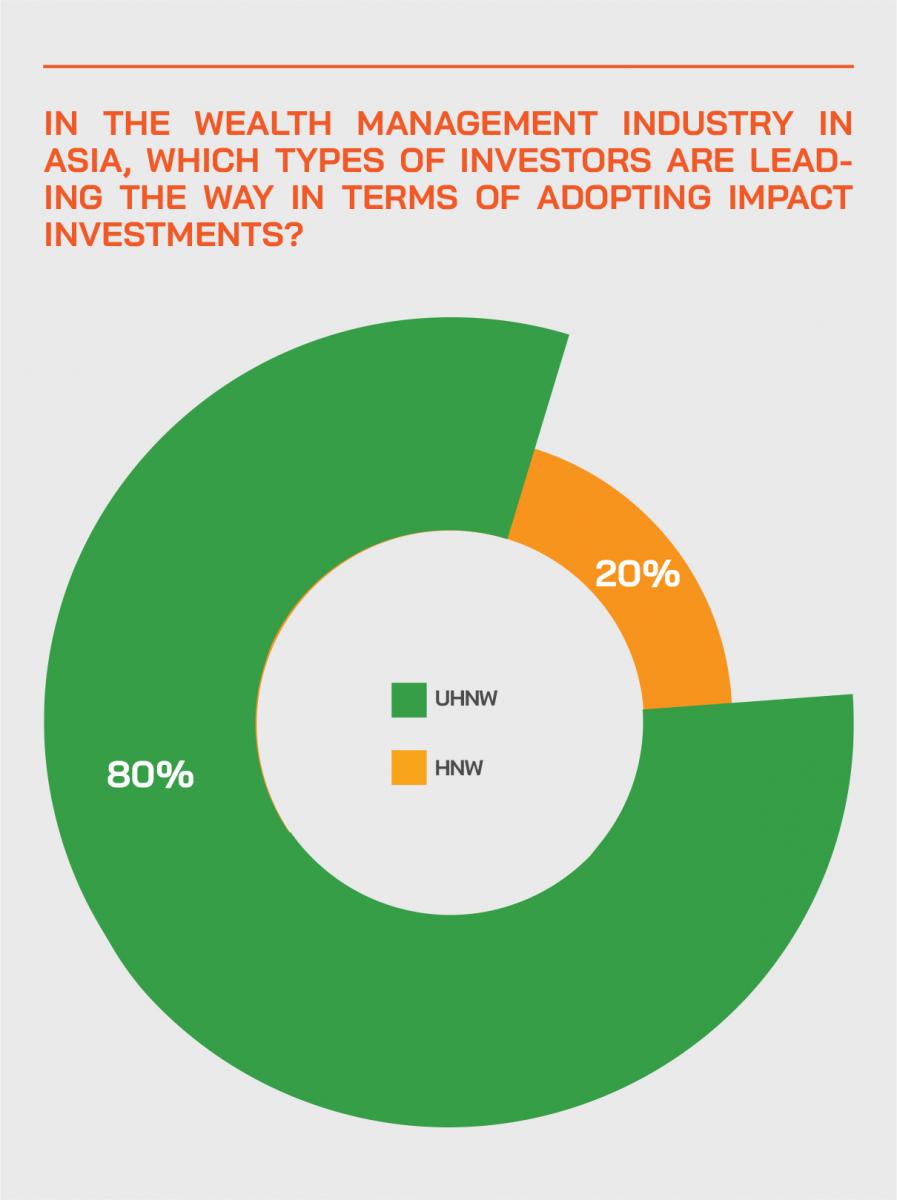

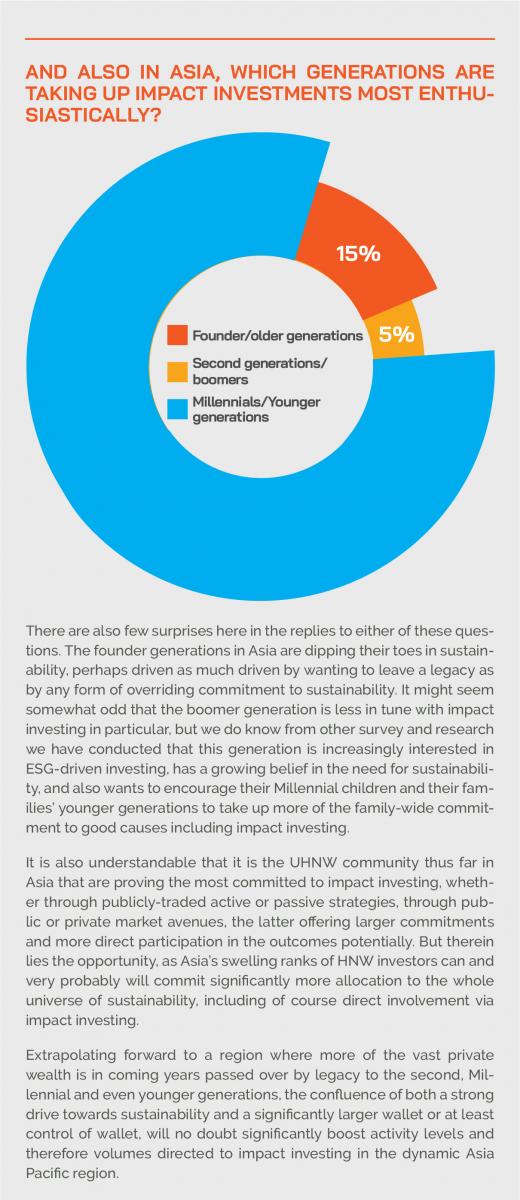

Impact investing growth in Asia is driven by the wealthiest, and the Millennials are helping the impetus

We found that 80% of respondents consider UHNW clients the most active in impact investing in Asia to date, and 20% think HNW clients are active. We also discovered that 80% of those we polled think that Millennials and the younger generations are taking up impact investments most enthusiastically. This augurs rather well for the future, as so much of Asia’s vast private wealth is due to be passed over from the founder and even second generations in the next two decades, which should certainly help propel sustainable investing of all types and within that drive significantly more demand for specific impact investment opportunities.

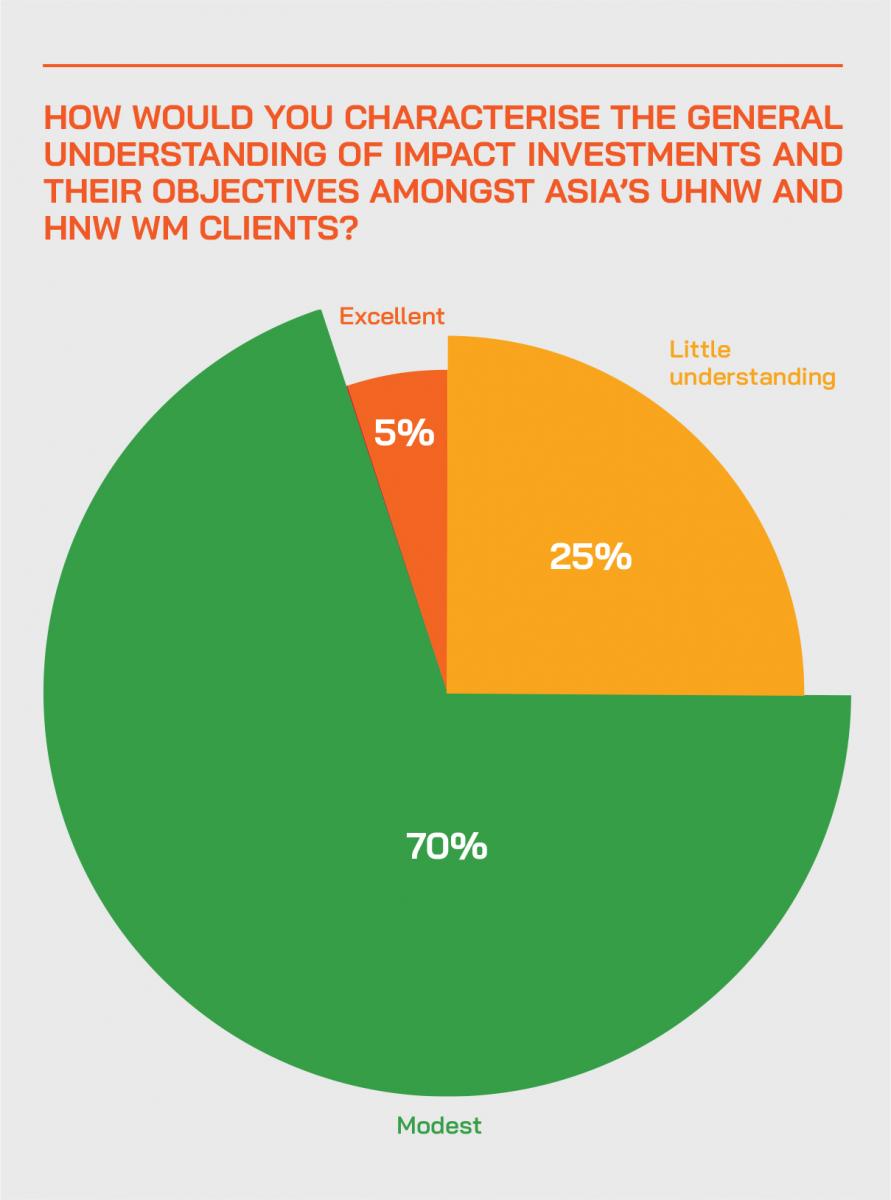

But education needed! 70% say clients have only a modest understanding of impact investing

To boost the growth of impact investment in Asia, more education of the client-facing relationship managers and advisors is needed, and in turn, they need to help their private clients better understand the opportunities and the potential. The survey highlighted how 70% of respondents consider their UHNW and HNW clients to have only a modest understanding of impact investing, and 25% said their clients have very little understanding. Meanwhile, only 5% said that clients have a really firm grasp of these investments.

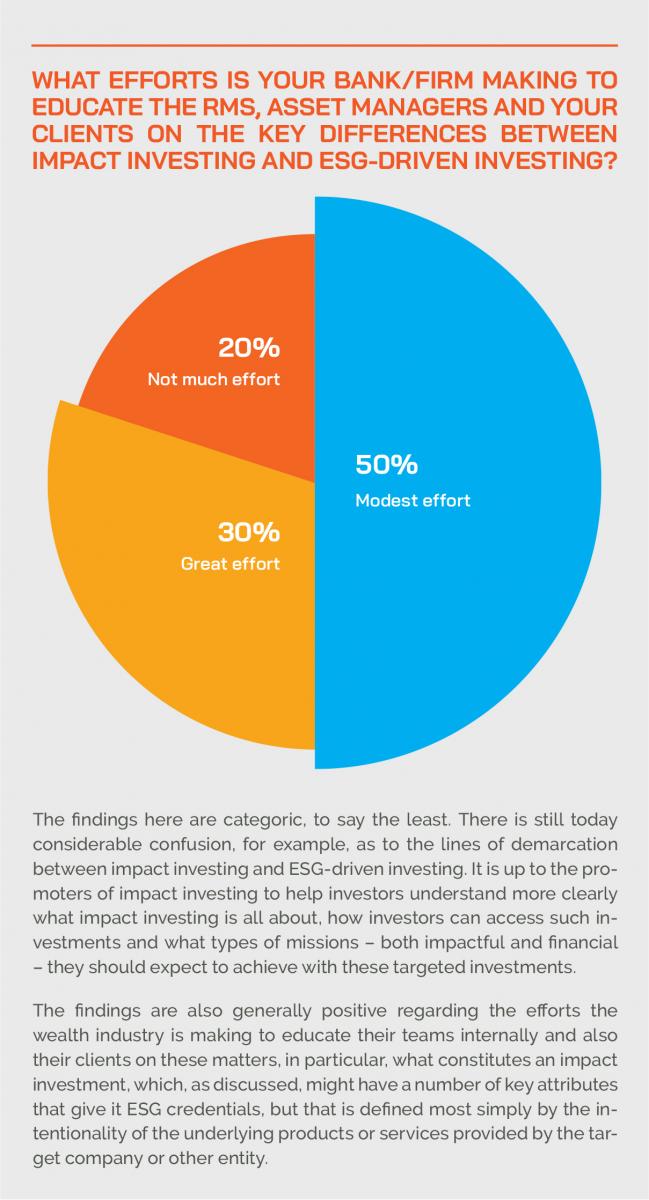

Asia’s wealth management industry is reacting, but more needs to be achieved

Only 30% of replies indicated that their private bank or IAM/EAM firm is making a great effort to boost education amongst its RMs and investment managers and also clients on, for example, the key differences between impact investing and ESG-driven investing. However, encouragingly, 50% said that modest efforts were taking place. Less encouraging, 20% of replies indicated there was not much education coming through from within. The reality is that the more the key client-facing advisors understand, the more likely they will be to solicit and then promote opportunities to their private clients.

Impact investing for private investors is also about returns as well as achieving ‘impact’

If more private wealth is to be driven into areas such as impact investing, then private investors should expect returns commensurate with their other investments. This will help engage them in the market and keep them involved and potentially increase their exposures later on. In this way, there should be a snowball effect ahead. At this stage, there are some encouraging signs that this message is getting through in Asia, as 15% of replies indicated that impact investing might significantly help their investors’ returns, and 80% said they think this should help at least modestly. The rationale is simple – impact investments are targeting investment towards companies that will make an impact through their products and services, and this should help create a virtuous cycle of enhanced top and bottom-line growth. Moreover, the target companies themselves should exhibit many of the key ESG characteristics that are increasingly valued by investors of all types across the world.

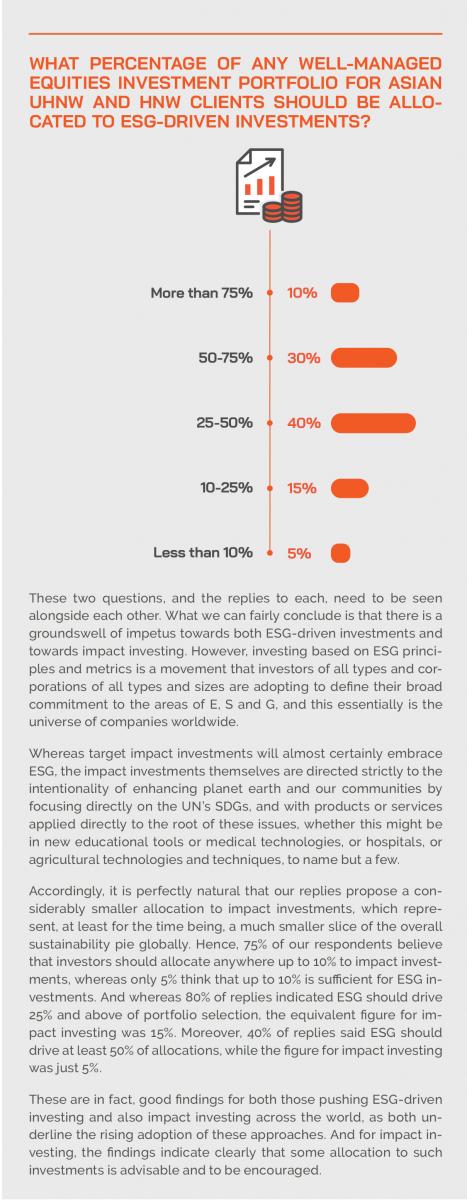

Allocations amongst Asia’s UHNW and HNW investors to impact and ESG investing show encouraging signs, at least in theory

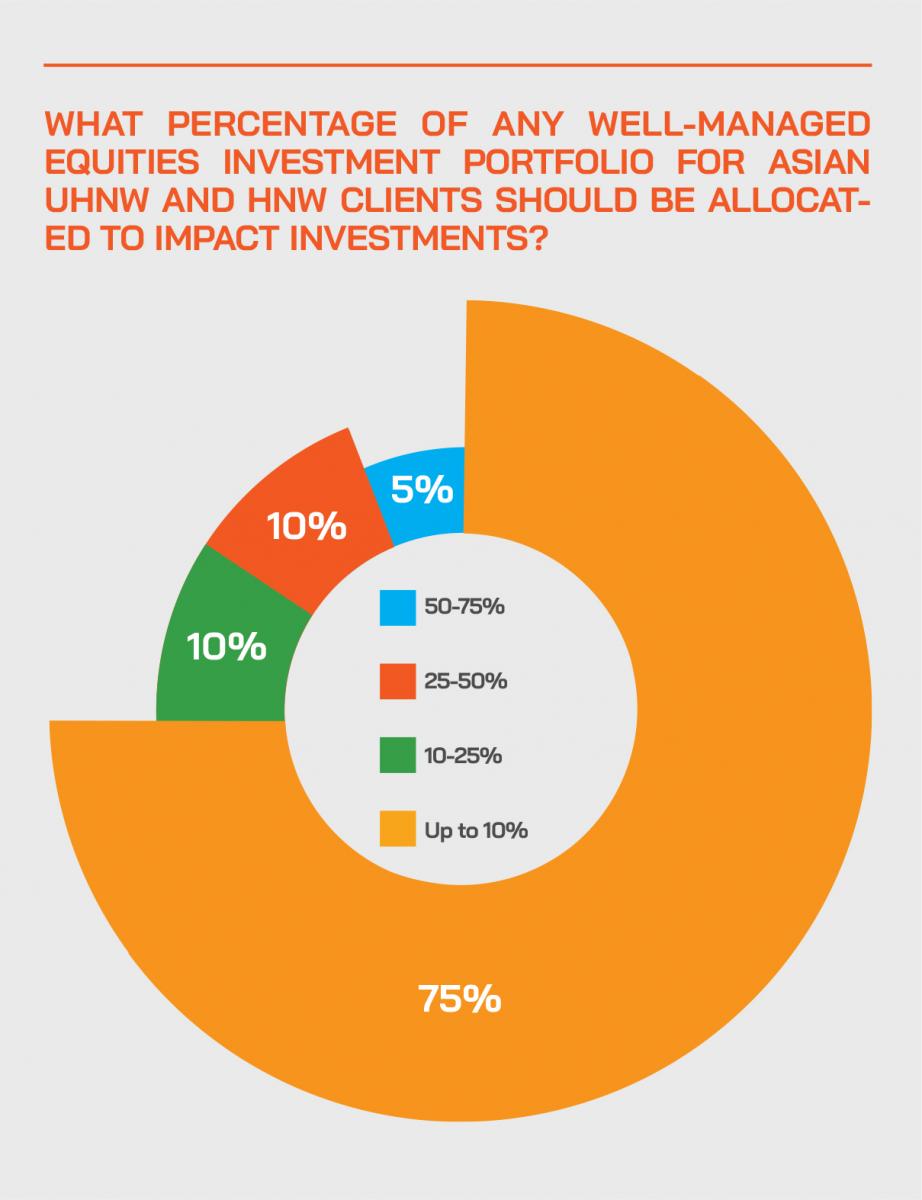

A very positive 80% of replies indicated the ESG should drive 25% and above of HNW and UHNW portfolio selection amongst private clients, while the equivalent figure for impact investing was 15%, which is also encouraging as ESG is a catch-all for all companies potentially whereas impact investing is a much smaller, more targeted (but also fast-growing) portion of the corporate world. It was encouraging to learn that 75% of our respondents believe that investors should allocate anywhere up to 10% to impact investments, and to set this in context, only 5% think that up to 10% is sufficient for ESG investments.

The leading global and boutique international private banks are ahead in Asia in promoting impact investments

Some 40% of replies said they felt that the global brand-name private banks are ahead in terms of promoting impact investing, which gels with the reality that thus far, private clients in the US and Europe have been more active in this field. Similarly, 35% of respondents indicated that the boutique international (mostly Swiss) private banks are active, and 20% said that the IAM/EAM/MFO community is active. In their associated commentaries on these findings, almost all replies indicated that more can and should be done by all parties but that they are generally encouraged by the development and the outlook.

The Survey Review in Full

Few would disagree that the world is currently experiencing unprecedented levels of change. We find ourselves now in the midst of several major transitions that involve technology, climate, geopolitics, and demographics, all of which will have some undeniably negative effects on our planet and on the societies in which we live. On top of all these challenges, the pandemic remains rampant and threatening. It is as a part of the general awakening to this realistic view of a ‘challenged’ world that impact investing can best be understood; it is one of the funding solutions that can help address some of the major problems of our times. And private-sector capital can not only help to generate positive environmental and social effects; impact investing can also potentially boost financial returns for the private investor.

Accountability and responsibility

Many now believe that businesses should be held accountable for the consequences of their actions and required to make amends for the environmental and social losses and injuries that they cause. Excess intermediation and short-termism within the investment industry have to a large extent, potentially broken the positive connection between private capital and its commercial and societal purpose. And the need for impactful businesses and investments has been brought into sharper focus and indeed accelerated by the dreadful events since early 2020 when the pandemic began to take full force.

Many of the proponents of impact investment therefore regard the present time as a moment of awakening, a broader recognition that the challenges blocking the growth of a sustainable and inclusive economy need to be solved sooner rather than later and cannot be pushed back any longer.

For the wealthiest and most privileged elements of society, for example, the HNWI and UHNWI community, their participation in impact investing will greatly help close the wide and expanding funding gap between public finance available for such initiatives and the private sector funding.

Reducing risks

Moreover, allocating funds to the impact sector will potentially boost investor returns, as there is a growing body of evidence that impact investments produce robust returns while also mitigating many environmental, social, and governance (ESG) risks.

This is because the UN Sustainable Development Goals (SDGs) can help investors to integrate ESG factors into their financial analysis by identifying companies with a material revenue exposure to products and services that assist in overcoming social and environmental challenges, thereby managing and improving their returns, and vice versa, of course.

Impact investing in focus

A good definition of impact investing is provided by the Global Impact Investing Network (GIIN), which is the closest body that the field has to a trade association. “Impact investments,” the GIIN explains, “are investments made into companies, organisations, and funds with the intention to generate measurable social and environmental impact alongside a financial return.”

The key here is the phrase ‘alongside’. Impact investments do two things: in addition to (or alongside) generating financial gains for investors (which can vary, depending on the investor’s strategy, from below market to market rate), they also help to bring about specific social and environmental effects which will be of benefit to the world and its inhabitants.

Impact investment is therefore, today a rapidly growing market that should be providing capital to address the world’s most pressing challenges in sectors such as sustainable agriculture, renewable energy, conservation, microfinance, and affordable and accessible basic services including housing, healthcare, and education. But also produce robust returns for private sector investors.

A Singaporean private equity case in point

An example of this practice in Asia comes in the form of impact funds such as UOB’s Asia Impact Investment Fund (AIIF II), a private equity fund, which is committed to improving the well-being and livelihoods of low-income communities which exist at the ‘base of the economic pyramid’ in Southeast Asia and China.

The AIIF II’s first round of fundraising has received capital commitments (totalling in excess of USD 60 million) from institutional and accredited investors, which have then been used to make private equity investments of about USD1 million to USD15 million into private, high-growth companies in sectors such as agriculture, education, healthcare and logistics or that focus on improving the accessibility of affordable housing, sanitation, clean water and energy.

Bonding with impact investments in Japan

Another very simple example of impact investing comes from Japan’s long-established domestic impact bond market. These are bonds issued in Yen for domestic investors, but on behalf of international entities.

Daiwa Securities and other leading securities firms have pioneered the market for the past two decades and the types of bonds might, for example, in the past have been an IFC Microfinance Bond, a World Bank ‘Green’ Bond, an Asian Development Bank Water Bond, an African Development Bank Education Bond, an IDB Poverty Eradication Bond, and a host of other direct impact issues, such as vaccination bonds, women in work bonds, so on and so forth. The typical buyers of such bonds are Japanese institutional investors, including life insurance companies, banks, asset managers and pension funds, as well as ultra-wealthy individuals. They do not sacrifice either return or security, as the issuers are mostly entirely AAA global credits, and the returns are in line with the types of yields investors would expect from other non-impact bonds issued by similar credits.

Great potential from targeted products and services

Private sector companies that have built their businesses around solving the most pressing environmental and societal problems of the age are discovering huge new opportunities to solve these problems and are experiencing commensurate revenue growth as a result. Accordingly, companies and investors who are responsive (rather than resistant) to turning points and who are willing to embrace innovation (rather than clinging inflexibly to tradition) are finding excellent opportunities to drive top-line and bottom-line growth. Within the healthcare sector, to cite just one timely example, the transition to immunology is likely to maroon some of the previously dominant but increasingly obsolete drug manufacturers.

Meanwhile, individual consumers, governments, municipalities, and the larger corporations of the world are not only becoming more impactful themselves but are increasingly employing the products or services of smaller to medium-sized impact-driven companies. Manufacturing and services businesses are increasingly looking towards the more responsible companies for solutions to the environmental or social challenges that they face.

The impact sectors

Because of the scale of the problems that impact investment has the potential to help solve, the industry spans a huge variety of asset classes, geographies, themes, and instruments, all relating back to the UN’s SDGs ultimately. Impact investing opportunities abound across a wide range of sectors that together constitute significant percentages of any country’s GDP.

This range includes: Community development; Small business finance; Health and wellness; Education; Microfinance and financial inclusion; Sustainable consumer products and fair trade; Natural resources and conservation; Renewable energy and climate change, and Sustainable agriculture and development. Moreover, it is not only the poorer or poorest countries that receive the benefits of impact investing – there are more and more funds targeting segments of society within the wealthiest nations.

A groundswell of investor demand

There is certainly a rapidly growing number of private investors around the world who are motivated to target more of their investment portfolios on advancing our communities and for the betterment of the planet. These investors range from vast institutions such as pension funds or other asset managers representing potentially tens, even hundreds of billions of investment dollars, to the UHNW and UHNW segments, and indeed to the man on the street who wants to put perhaps USD1000 into an impact investment fund.

These investors are often dramatically different in their intentions and constraints. An institutional investor might, for example, want to allocate more of its portfolio to social issues in its clients’ communities. A family office representing UHNW wealth might want to allocate more of its often-vast wealth to philanthropy and philanthropic capitalism. A mass affluent type private investor might be seeking diversified investment opportunities that make him, or her feel a bit better about himself, to feel as if they are making a positive contribution to positive change, however tiny.

Lines in the sand…

It is important to appreciate the lines in the sand that separate impact investing from other popular approaches in the broader, catch-all universe of sustainable investment. Education around these topics is vital, because investors are often somewhat confused as to where impact investing fits into the universes of Socially Responsible Investing (SRI) and Environmental, Social and Governance (ESG) investing.

Impact investing itself is driven by intention and mission; it is not driven by (ESG) integration or ESG risk mitigation, although it is fair to say that impact investment might indeed tick many of the ESG boxes. The mission for impact investing is to deliver capital that will do good for the world and society at large by investing in and supporting businesses that are genuinely impactful.

Returns are indeed vital - this is not concessionary finance

However, private sector impact investors (unlike philanthropists) expect to generate a financial return on their capital or, at the very least, a return of their capital. Impact investments target financial returns that range from below market (sometimes called concessionary return expectations) to risk-adjusted market rate (known as non-concessionary return expectations), and it is these market-driven returns that the private investment community requires in order to mobilise capital in volume.

There is therefore little doubt that a concern for private investors is whether they need to sacrifice returns for their good intentions, as few investors, even amongst the ultra-wealthy, often want to sacrifice investment returns for impact. If they do forego returns, it is more likely to be for direct philanthropic purposes in their local communities, near and dear to their history and social lives. Part of the education drive around impact investing is therefore to push home the message that when investors provide private capital to such objectives, that will be taken and delivered on a commercial and not a concessionary basis.

Recycling funds towards sustainability

The private sector must achieve adequate or even attractive returns because it helps drive funding to the sector and helps retain those investors for the future, creating a snowball effect. As more and more companies realise an attractive cost of capital is available for their impactful products, services and ventures, so the theory goes that more and more companies and other entities will focus on delivering more and more impactful products, services and ventures.

From the perspective of private sector capital, the proponents and principals of impact companies and vehicles target attractive long-term investment returns from these solutions, the success of which will drive the financial value of target companies. Those promoting the sector must continually review companies’ effectiveness in helping solve the numerous environmental and societal problems by measuring their impact in hard numbers and tracking the change such engagement helps to drive.

Private and public market access

Investing for impact extends across asset classes and across private and public market assets and opportunities. And the overall market for impact investing is already substantial as well as growing apace. The Global Impact Investing Network (GIIN) estimates the impact investing market had grown by the end of 2019 to USD715 billion, based on the comprehensive GIIN Annual Impact Investor Survey.

Curating an impactful portfolio

To meet the rising tide of demand for funding and of supply from investors, there are numerous asset managers and other parties delivering ever more relevant and interesting direct equity or fund investments. They are aiming to capture a wide variety of sectors, companies, products and services that will directly benefit from these powerful trends and in which private investment can participate.

By way of example, our partner for this survey, Regnan, itself focuses its asset management curation on eight core themes, all of which fit tidily with the UN’s Sustainable Development Goals (SDGs) that form the bedrock for the impact investment industry. Adapting those SDGs, Regnan has systemised this into its eight core themes in order to tighten up the focus and help inform potential investors of where asset managers and investors can truly make a difference, but also to help identify where they can boost their investment returns.

Example – Regnan’s eight core themes

By way of example, our partner for this survey, Regnan, itself focuses its asset management curation on eight core themes within the Regnan Global Equity Impact Solutions Fund. All these themes fit tidily with the UN’s Sustainable Development Goals. Health & Wellbeing focuses on improved life expectancy and quality of life. Energy Transition is all about transforming the energy system to power a low-carbon economy. Future Mobility is linked to this as it is promoting low-carbon transportation. The so-called Circular Economy centres on the cycles of resource efficiency, reusability and recyclability. Food Security takes a global perspective on sustainable food supply and productive farmlands. Education naturally targets global access to quality education. Financial Inclusion is about the democratisation of access to financial services, especially for the underserved populations around the world. And Water, naturally, is about the preservation of water and ensuring access to water for all.

To refine these further, Regnan then makes a five-step impact assessment to narrow down the universe of potential target investments. To identify whether the company that offers a compelling solution to a problem makes the cut, the team needs it to pass five key Regnan-devised impact tests. For those targets that pass these tests, Regnan then conducts its financial analysis, centring on the company’s history and potential, centred of course on whether the company’s potential for value creation is already reflected in the share price and a deep risk assessment of where things might potentially go wrong.

Creating a virtuous circle of funding and impact

Regnan is one example, but of course, there are many other professionals out there dedicated to building more private-sector impact opportunities. Indeed, the actively managed impact funds in the market today are designed to at least match, but hopefully also outperform the broad global equity market indices; if assembled correctly, the portfolio of impact-driven targets in the growing array of impact funds in the market will enjoy stronger than average growth, as demand for their products and solutions grows.

The mission for such fund managers is therefore to invest for a positive impact on societies and the planet, often by identifying early growth opportunities that meet a structural, underserved need, and hopefully also taking advantage of market inefficiencies in valuations.

Private Equity Market Impact Investing – An Example Born in Asia

As an example of the private markets access available to impact investments, ABC World Asia, a private equity fund dedicated to impact investing in Asia, earlier this year launched its inaugural impact report to share details of its investment activities and portfolio impact performance for the full 2020 calendar year. They raised an inaugural SGD405M fund in 2019 and deployed about S$98M in 2020, adding five companies to the portfolio, addressing key challenges in climate, financial inclusion, healthcare, and sustainable agriculture, the firm said in a press release.

David Heng, Founder and CEO, ABC World, said: “By sharing our learnings and experiences through this report and its future editions, we hope to encourage more dialogues in impact investing in Asia. Impact investing is a pathway for capital and businesses to drive positive change in the world. This report represents the first step in our impact journey, and we hope to grow together with our stakeholders to help shape a better world for everyone.”

In 2020, ABC World evaluated over 200 opportunities and invested in five businesses in Asia Pacific, deploying SGD98 million from its first SGD405 million fund.

Under the banner of Climate Solutions, the firm invested in Singapore-based solar firm Sunseap Group addresses the decarbonisation challenge by assisting Asia in transitioning from emissions-intensive energy sources to clean energy. And in v2food, an Australian producer of plant-based meat using protein extracted from legumes. Its products help accelerate consumers' transition to a more plant-rich diet. This in turn, helps to reduce the adverse environmental impacts of animal agriculture such as greenhouse gas emissions, land degradation, water scarcity, and biodiversity loss. The two companies generated a positive impact outcome on the environment, avoiding about 1.1M metric tons of CO2 emissions in 2020.

Under the flag of Financial and Digital Inclusion, ABC invested in CD Finance, which provides financial services to rural populations in China. Over 460,000 people and microenterprises have gained access to credit and financial services through CD Finance in 2020. The company is driving further financial inclusion through digital technology, and connects households and micro-enterprises to credit and financial services that help reduce poverty and promote economic development.

In the realm of Better Health and Education, Kim Dental provides vital dental services to communities in Vietnam, with over 129,000 people having received oral health treatment along with prevention in 2020. Oral health is often neglected and continues to pose a major public health concern in many developing countries, despite being an important component of primary healthcare. The company delivers a large panel of oral health solutions to meet the needs of underserved and emerging middle-class populations across Vietnam.

And under the umbrella of Sustainable Food & Agriculture, ABC bought into India-based agri-tech platform CropIn, which assists smallholder farmers in building secure and sustainable livelihoods. In 2020, over 1.5M smallholder farmers globally have gained access to its customised farming advice and information. Its farm management solution drives greater efficiency in agri supply chains and improves the productivity of smallholder farmers, many of whom earn less than USD2 a day.

Capital helps impact providers stay the course

After investing, asset managers are also able to positively engage with management teams to influence strategy and try to keep them focused on business areas that contribute to solutions, promote better business practices and disclosure, and reduce negative impacts by talking to the management of portfolio companies about issues such as the environmental footprint of their supply chains and working conditions in their suppliers’ factories.

The impact investment industry is also supporting management teams by investing in companies that they believe should outperform the market in the long term. That can mean accepting underperformance in the short term because the management prizes long-term potential over the near-term earnings. But the allocation of capital to these businesses helps to ensure that the target companies can stay the course to be impactful and make the requisite returns anticipated.

Building exposures

Diversification is also important to many investors, and so too in their impact investments. That is why so many HNW and UHNW investors prefer the funds approach, as that allows them to gain exposure to a diversified collection of carefully selected names across different sectors and geographies.

In practice, the companies in this portfolio will be typically a smaller or medium-sized business, whereby the value of that company, the equity value of that company, is dependent on the success of this particular product or service that the company offers, which is solving either an environmental or social problem.

Accordingly, the ability of these companies to grow in valuation terms over the long term is dependent on their ability to grow their revenues by selling a successful solution to either an environmental and/or social problem. The equation is, therefore, a simple one, whereby we have issues to solve like water shortages or emissions, or social problems, such as, of course, or even to help in a pandemic-type environment. These are problems that increasingly need to be solved and need to be solved quickly. And that translates directly into revenue growth and therefore profit growth for these companies.

Bridging the private and public markets

Impact investment can therefore be directed to both private and public market companies as both are invaluable to the expanding impact-driven corporate universe. Very simply, private equity or unlisted opportunities are usually taken up by the very wealthiest investors, as the commitments required are considerably larger and the timeframes for investment considerably longer. And for those seeking or needing liquidity, the more liquid fund approaches, whether via ETFs or actively managed strategies, are usually preferred.

In the public markets arena, the companies are also already at a more advanced stage of their development, as they are already listed, and there is accordingly far more information available on their performance, their structures, their strategies and their outlooks. The private markets should, in theory, offer higher returns over time as compensation for needed to stay invested for far longer, for the lack of liquidity and for the lack of public market accountability and reporting.

This is why the private markets’ arena for equity investing is really more institutional or ultra-HNW private investors. It is also a broad but fair generalisation that in the world of fixed income, impact bonds are generally also the province of the very wealthy or institutional type investors, as denominations are very large and very often regulatory demands will require distribution only to the larger funds and certain accredited investors.

Meanwhile, HNW and mass affluent type investors tend to navigate the world of impact investing largely through public market funds, funds of funds and perhaps selected individual impactful stocks.

Looking ahead

There seems little doubt that significant growth lies ahead for impact investing and that the pandemic has helped sharpen the minds of investors and open their imagination to the reality that we live in one world and that overcoming problems in countries or regions that seem remote from our lives will indeed help all of our communities and people.

There is no doubt that this is an awakening to a broader recognition that these sorts of challenges need to be solved sooner rather than later and cannot be pushed back any longer, and that so much of our endeavours are inter-related and have a broader negative impact on the world around us.

This, in turn, means that the region’s wealth management industry has a great opportunity ahead to offer more impact investment education to its RMs and advisors and thereby deliver more and better opportunities to their private clients. As wealth expands, as the Millennials and younger generations inherit more of the region’s truly vast private wealth, the demand for and interest in impact, sustainability, and ESG-driven investing will most certainly increase rapidly. The opportunities are there to be grasped.

The Final Word – Seizing the Opportunity

Environmental and social issues are no longer be simply considered external problems, the cost of which can simply remain unaccounted for, and the inter-connected nature of our world has been highlighted dreadfully and unremittingly by the pandemic. Individuals, consumers, voters are increasingly demanding change, and investors are increasingly trending towards allocating some of their investments to help these causes and will no doubt build those exposures if they see the effects on the world and also on their own portfolio returns.

The wealth management industry in Asia has both a duty and a great opportunity to help boost the momentum. Impact investing is a remarkably clear and direct approach that should benefit all parties concerned. And therein lies the opportunity…