In recent years there has been rising Asia-wide adoption of digital solutions in the world of independent wealth management. The rollout of these digital enhancements and solutions across the region has by broad acknowledgement been accelerated as a result of the pandemic, but this is actually the next and faster leg along a journey already underway, it is not a sudden or unexpected revolution; the path towards digitisation has been clear for some years already. Hubbis, along with our exclusive partner for this project, cloud-based investment management platform and SaaS provider QUO, recently conducted a mini-survey focusing on the challenges surrounding the trading and execution protocols of the independents. The findings are not revelatory, but they are confirmatory – the independents have far from overcome the challenges and are in need to state-of-the-art processes and solutions to ensure the utmost efficiency of trading, execution and reporting, for their clients, for the custodian banks, fund houses and brokerages they work with, for internal reporting and compliance and of course for the ever-more watchful eyes of the regulators.

As a myriad of macroeconomic and geopolitical factors continue to affect trading strategies, there are also numerous daily logistical and regulatory challenges for the Independent Asset Managers (IAMs), the External Asset Managers (EAMs) and Multi-Family Offices (MFOs), which collectively for this report will be termed the Independent Wealth Managers (IWMs). The challenges pre-existed Covid-19, of course, but they have been exacerbated by the added difficulties of working efficiently and compliantly from home offices, and potentially as the lockdowns were eased from combining such activities with part-time office work.

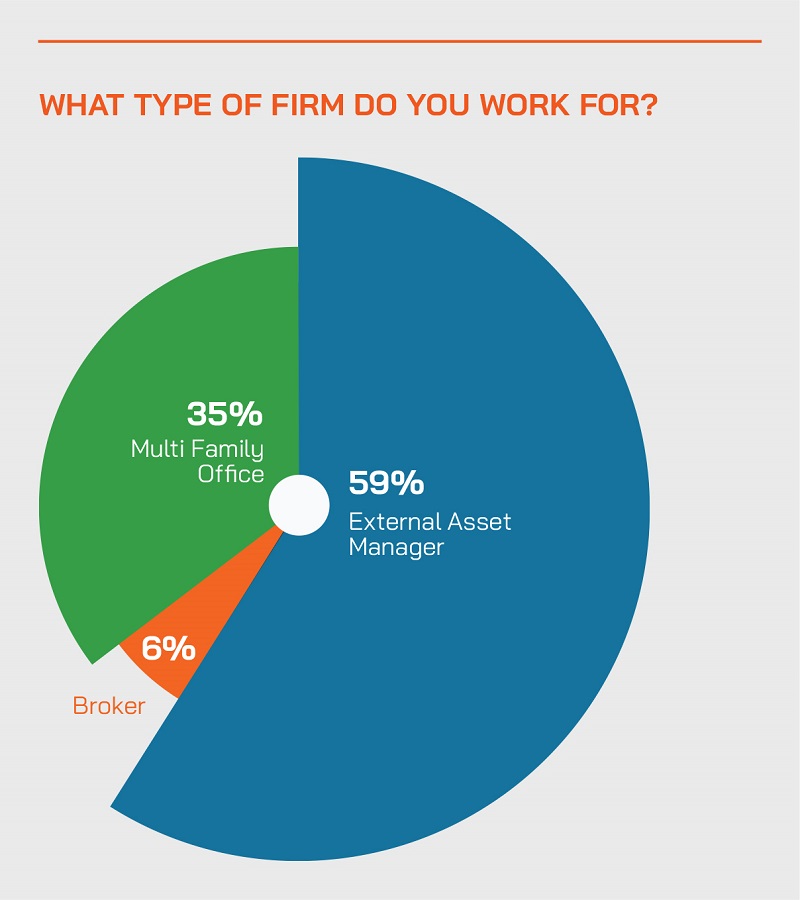

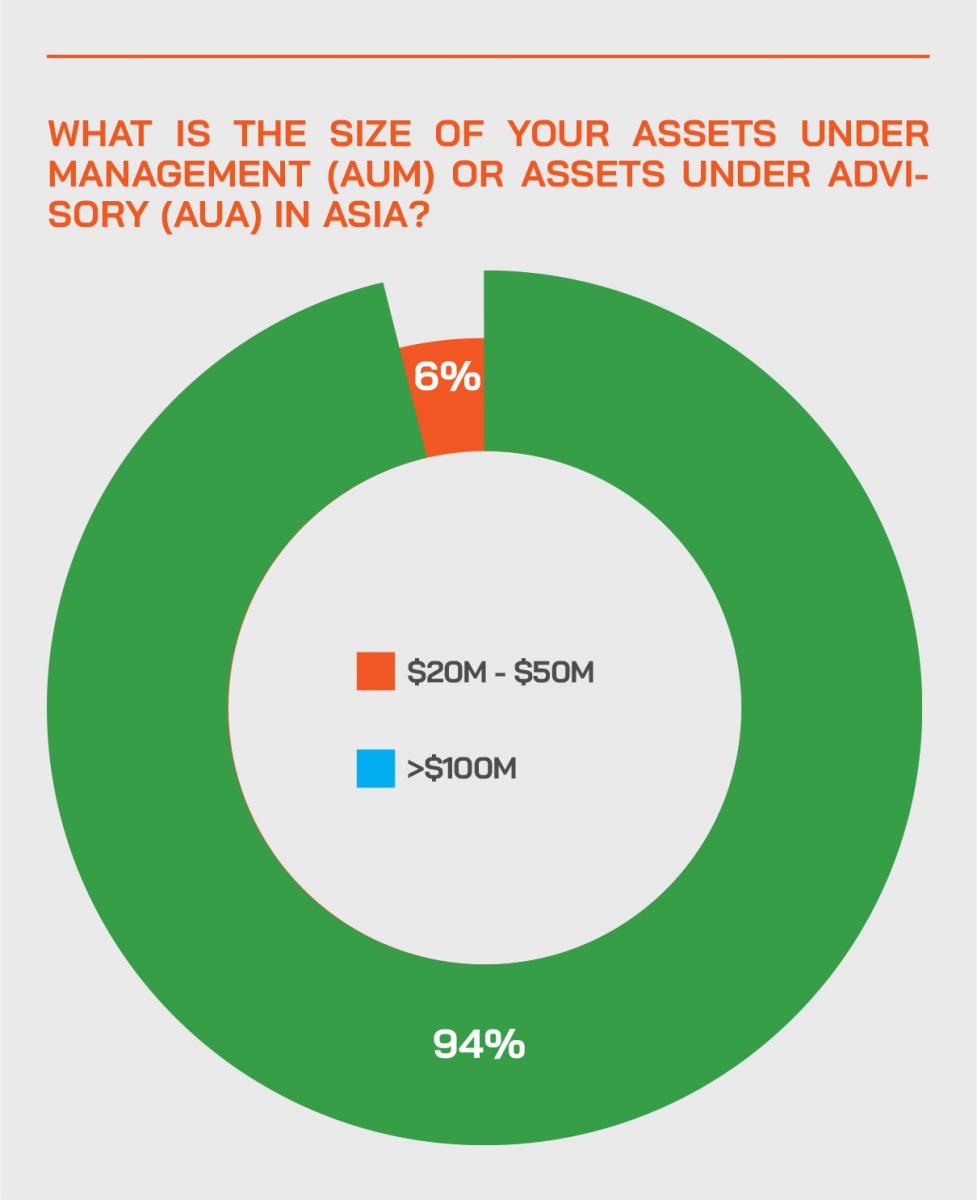

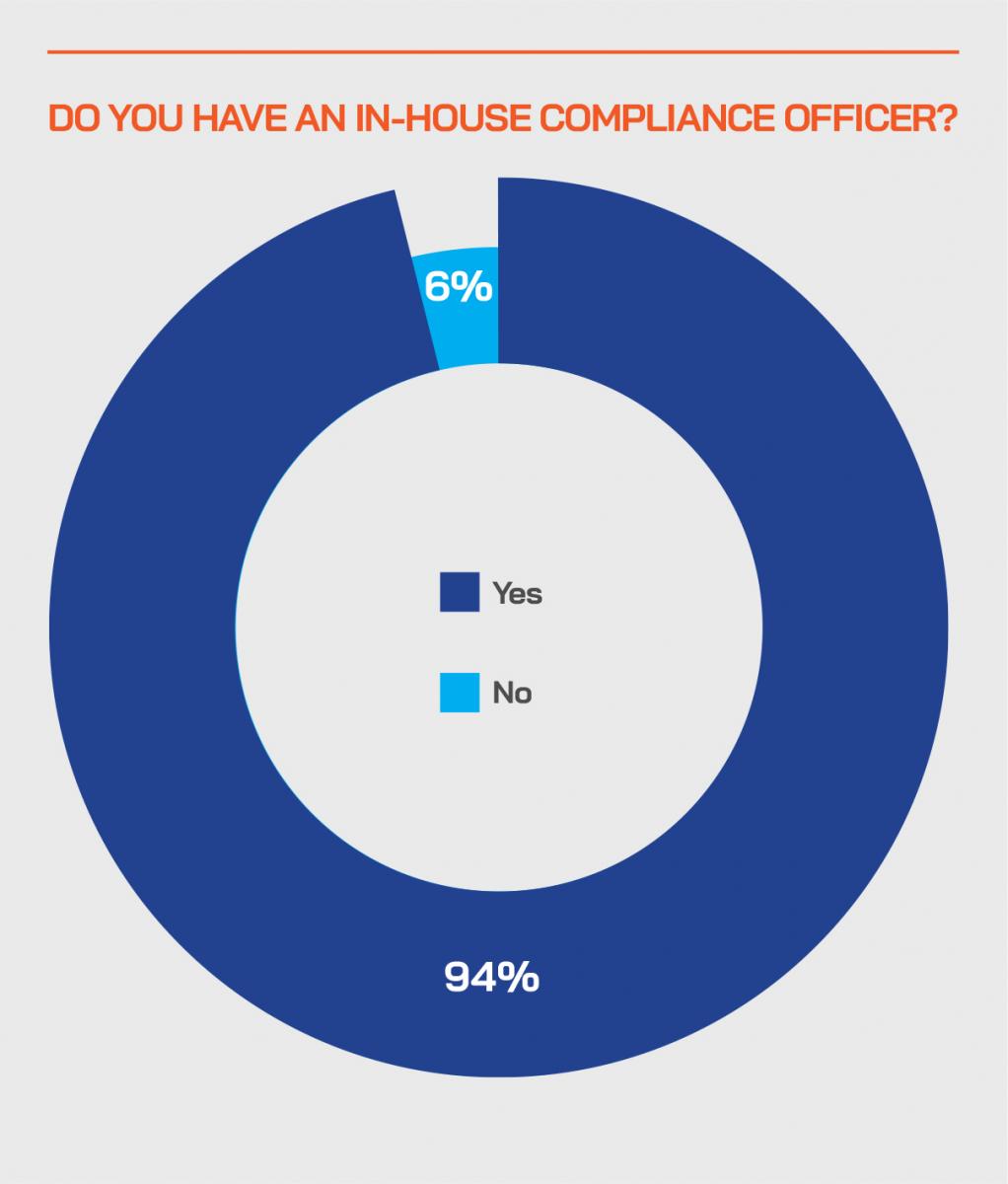

In conducting the Mini-Survey here, our objective was to glean a snapshot of the key issues and operational risks faced by these IWMs, 59% of which are IAMs/EAMs, 35% of which are MFOs and 6% of which are brokerages. Notably, 94% of these IWMs reported they handle asset of more than USD100 million for their clients, with a good number handling well in excess of USD500 million.

Many rivers to cross

There are numerous macro challenges to be faced across the globe today, but in the minutiae of daily working life for the IWM community, there are many very pressing issues to address, especially as it appears remote working will be here for some considerable time to come, in the absence of effective vaccines.

Rapidly increasing levels of digitisation are spanning vast swathes of the market – including wealth management. Wealth managers are under pressure to develop new strategies to meet the demands of a more tech-savvy high net worth (HNW) generation in Asia and Europe.

But whatever the challenges faced, the reality of the situation since the pandemic hit is how smoothly working from home has gone for many trading the global financial markets, nowhere more so than in the world of the IWMs, which are largely free of legacy systems and being much smaller, therefore, more adept at innovation and adaptability, indeed agility is a core element of their rationale and lifeblood. This will, in fact, help the IWMs continue their expansion of recent years, once the current Covid-19 situation settles down.

Independents see immense opportunity

The prospects are appealing for these IWMs – right now they are merely scratching the surface in penetration of Asia’s private client AUM/AUA pools, but imagine if they emulated the IWM scene in Europe, where according to McKinsey roughly a third of financial assets are under the management of these firms, whereas in Hong Kong and Singapore, UBS estimates that they account today for 5% or less of the potential market, in other words very little.

If they can indeed get all the various elements of their proposition right, they could therefore grow exponentially over the next few years. Imagine if they added 1% of the total pool available – that would boost them by 20% from 5% to 6%. If they won over another 5% of the pool out there, their AUM/AUA would double.

Fleet of foot

The banks themselves – with which the IWMs both compete but also work alongside - are sometimes weighed down by regulation and their risk-averse sensitive nature. A clear case of this is that banks are unable to deploy multi-asset online trading as their core banking systems are so often made up of legacy software. In contrast, the IWMs generally have no such or far fewer restrictions.

Still reliant on the banks

However, the IWMs must continue to rise to the many challenges. For example, many remain heavily reliant on banks for their expertise as custodians. While the independents in Europe enjoy more access to open banking, those in Asia still largely have to manage the challenge of working with various accounts across different banks. This difficult and highly sophisticated process is without question a major stumbling block and potentially a point of major weakness.

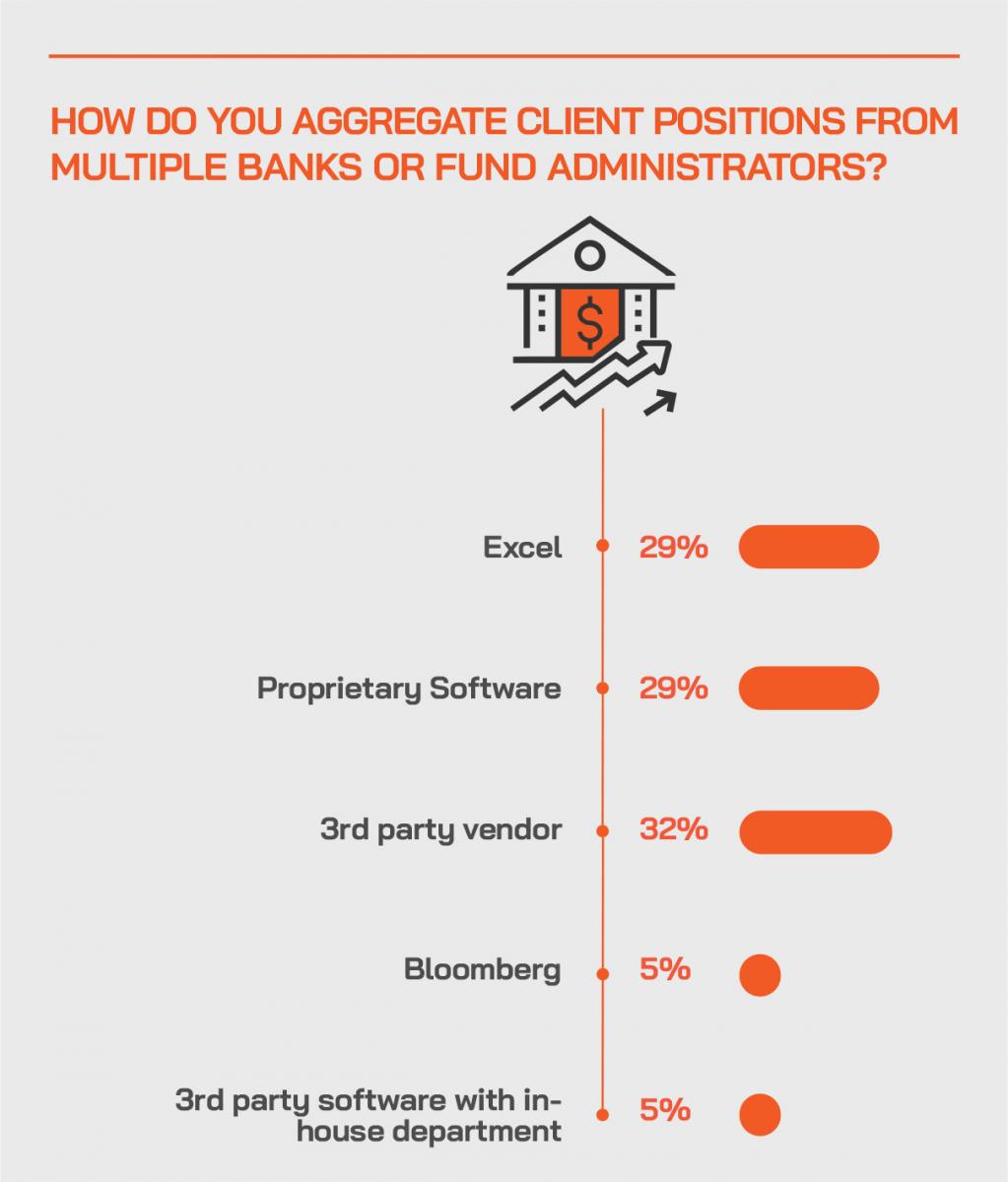

To overcome this issue, more and more IWMs are seeking ways to aggregate bank feeds to produce consistent portfolio return reports. However, for aggregation solutions to be of use, they need to be connected in real-time with a bank's trading platform. What EAMs require is some form of multi-bank solution, in the cloud, that enables them to execute

Boosting the customer experience

According to an EY survey in 2019, enhancing the customer experience is the key priority for 60% of private banks and wealth management firms. Key areas include: portfolio aggregation, because in a multi-custodian world, an aggregated portfolio view is rarely available, and market access for multi-asset trading, because poor execution has both cost and reputational implications, and there is also compliance risk management because greater and better automation of pre-trade checks and trade processing reduce this risks, including relating to privacy and cybersecurity.

Expert Opinion – Will Lawton, Global Head, QUO: “The Covid-19 crisis has and will continue to impact and change the way the wealth management process is conducted for the full spectrum of client segments, right up to UHNW. Clearly, like most industries, digital and particularly cloud solutions will be prerequisites; however, the investment and advice workflows will also need to change significantly with both the end client and the RM being given more tools to support the advice process.”

Many challenges to address

Client experience can only be enhanced by gaining real-time access to different jurisdictions and by having an unprecedented amount of control over the portfolio. As interest in the independent wealth sector continues to expand, it is essential technology keeps up to speed, because adopting the right technology will go a long way to ensuring that these IWMs can be confident that they can manage their clients’ money in the most efficient and effective way possible, and of course this will help client retention and acquisition going forward.

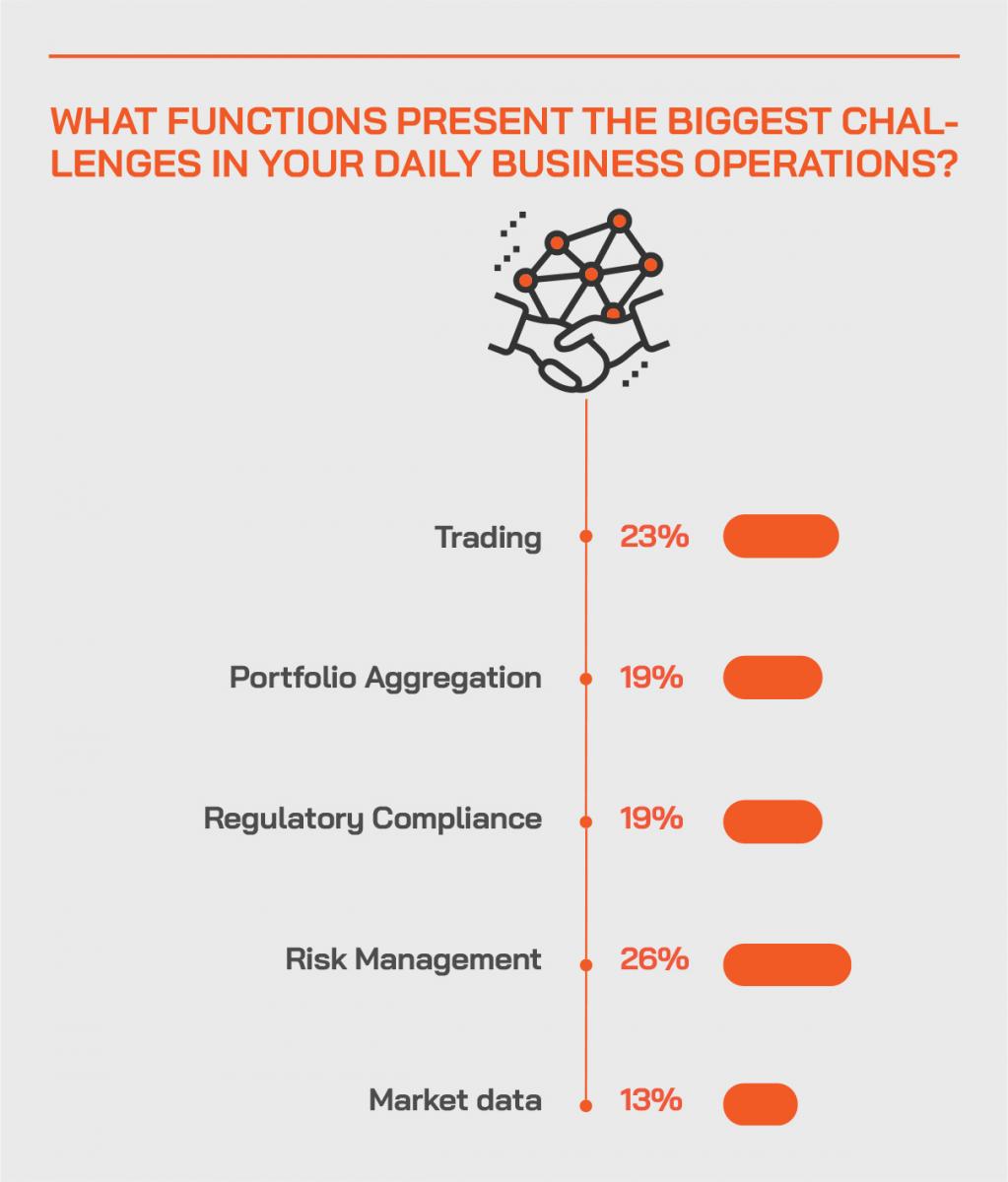

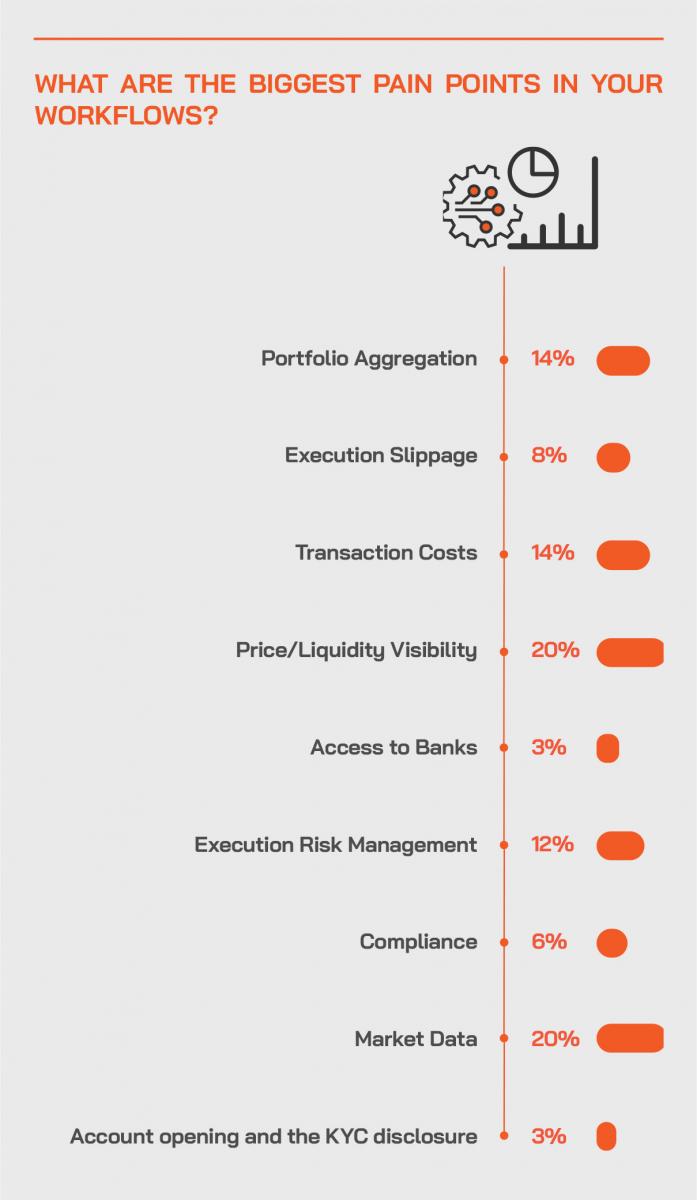

Essentially, there are numerous risks for the EAMs to handle when dealing with clients and in executing orders on their behalf, especially in a world of far stricter external regulation and internal processes and compliance. And certainly, the replies to our Mini-Survey indicated that concerns around trading, risk management, market data and compliance dominate their focus, along with needing to address portfolio aggregation reporting for their clients.

Many moving parts

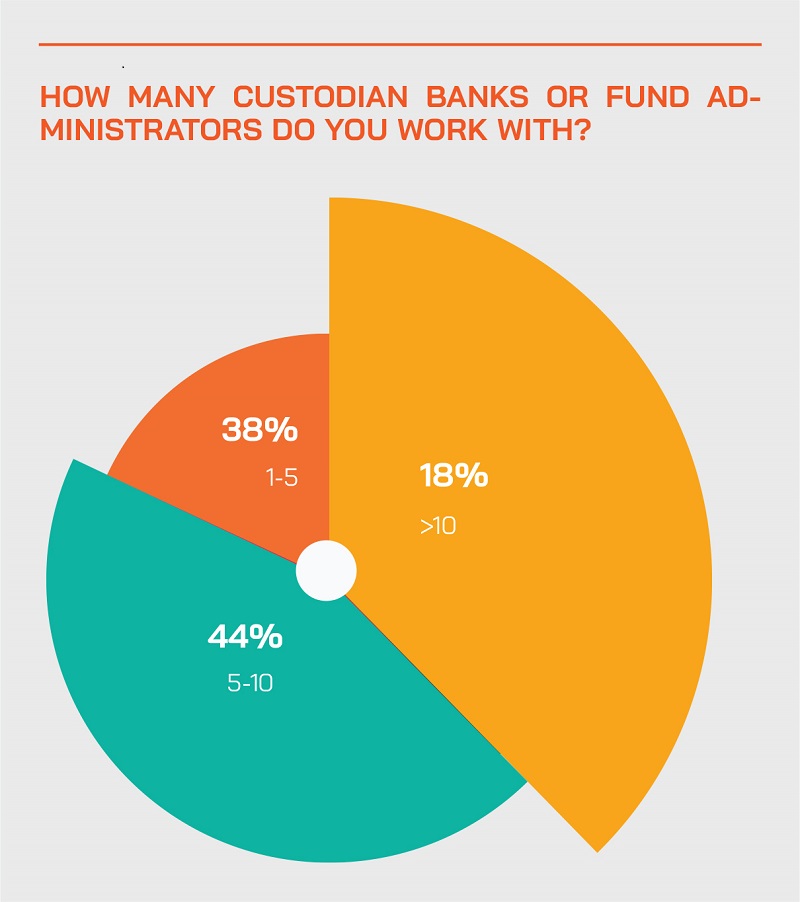

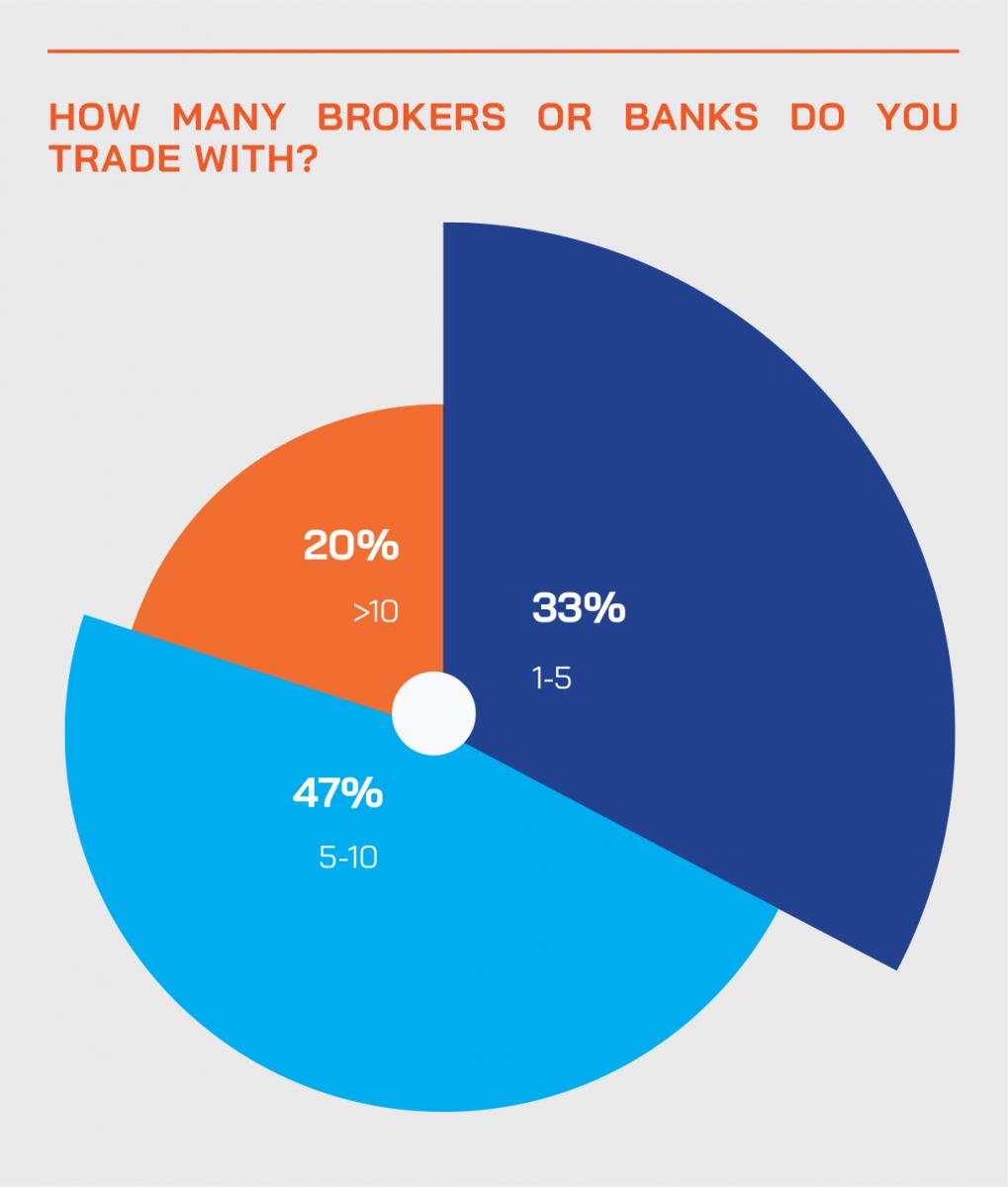

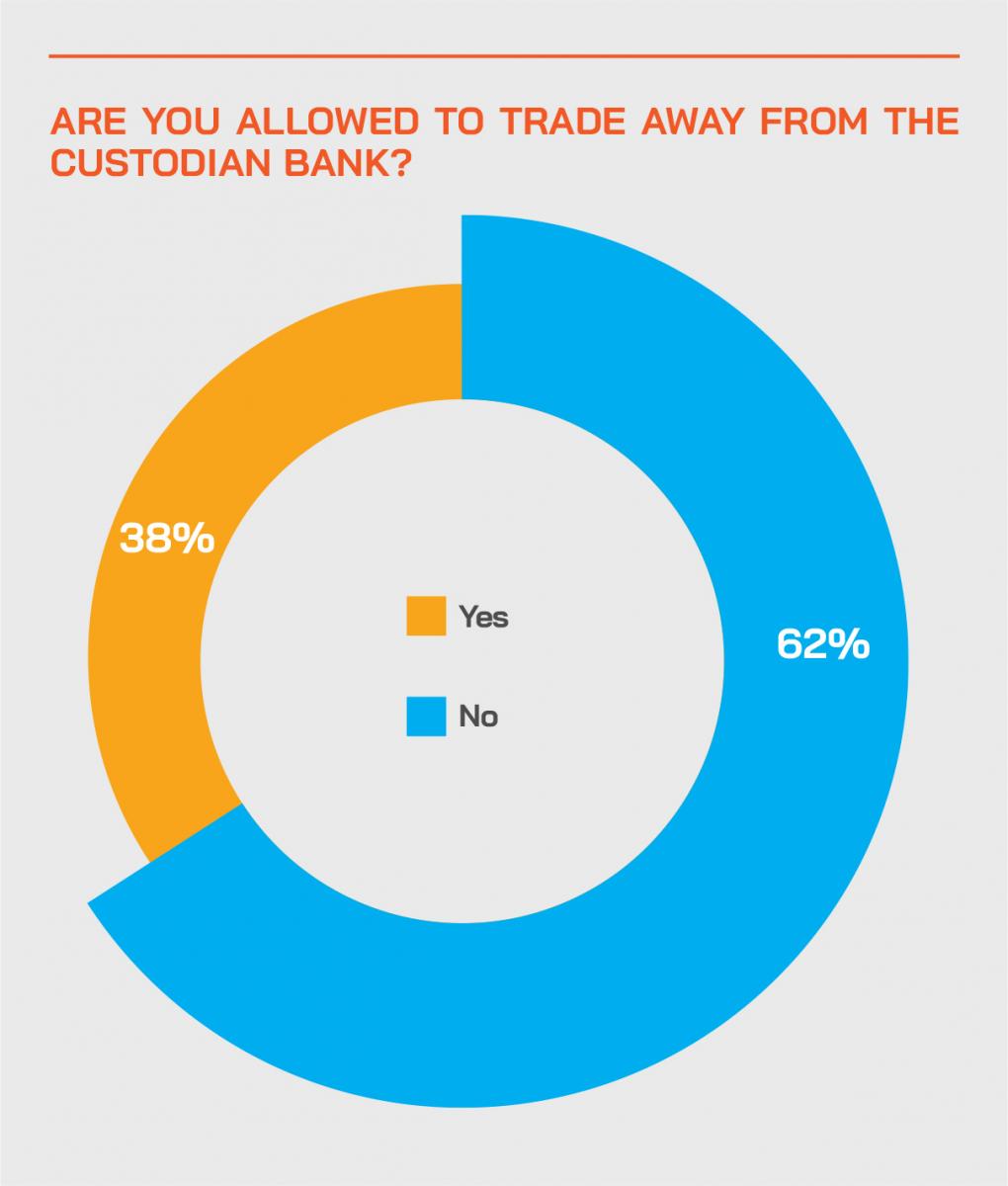

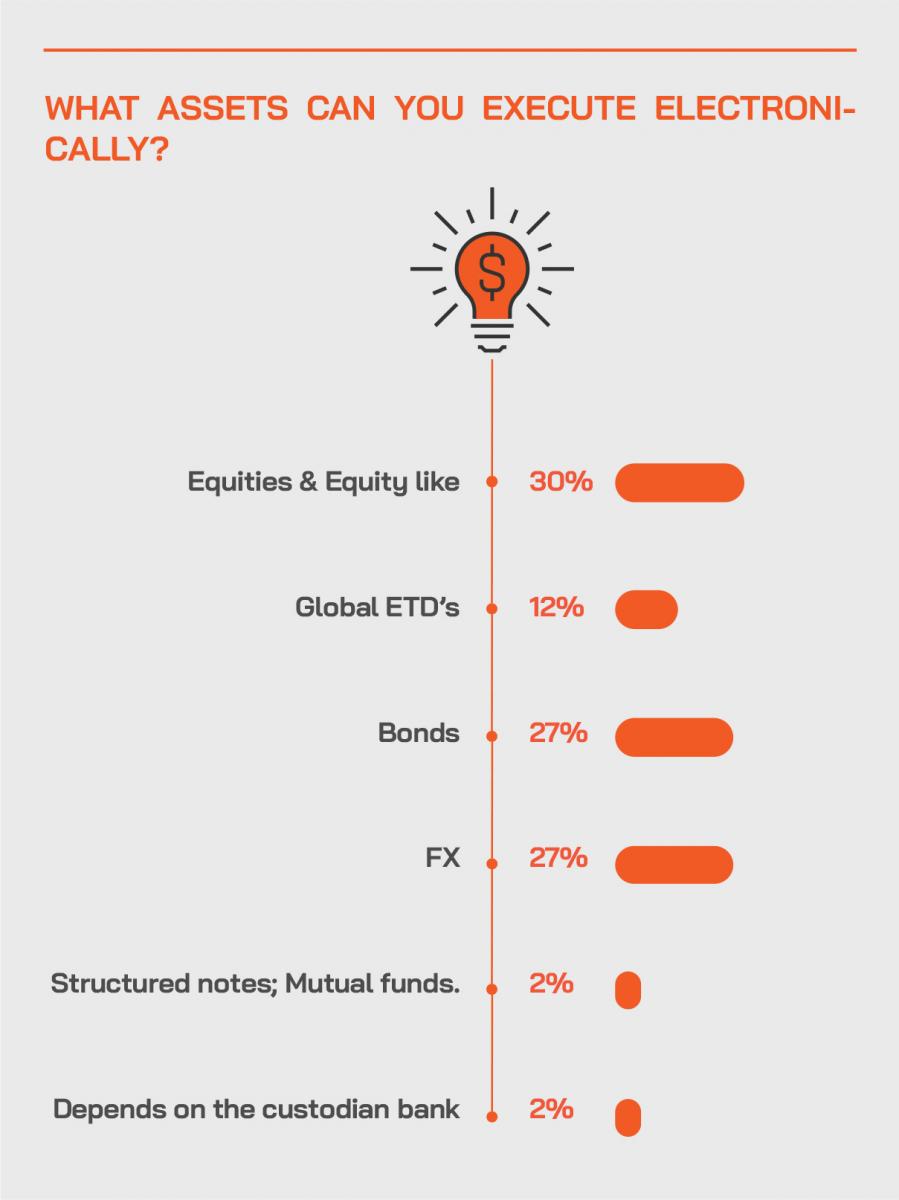

From the evidence above and below, it is clear that the problem is even more acute than it might first appear, as the IWMs work with a host of custodian banks and fund administrators, in fact, 62% of those we surveyed indicated they deal with more than five such institutions, while 67% said they trade with more than five brokers or banks, and 38% indicated they were allowed under their respective arrangements to trade away from their custodian banks, implying further diversity of interface, especially as these days it is rare that one single bank can meet all manner of the needs of these IWMs and their private clients.

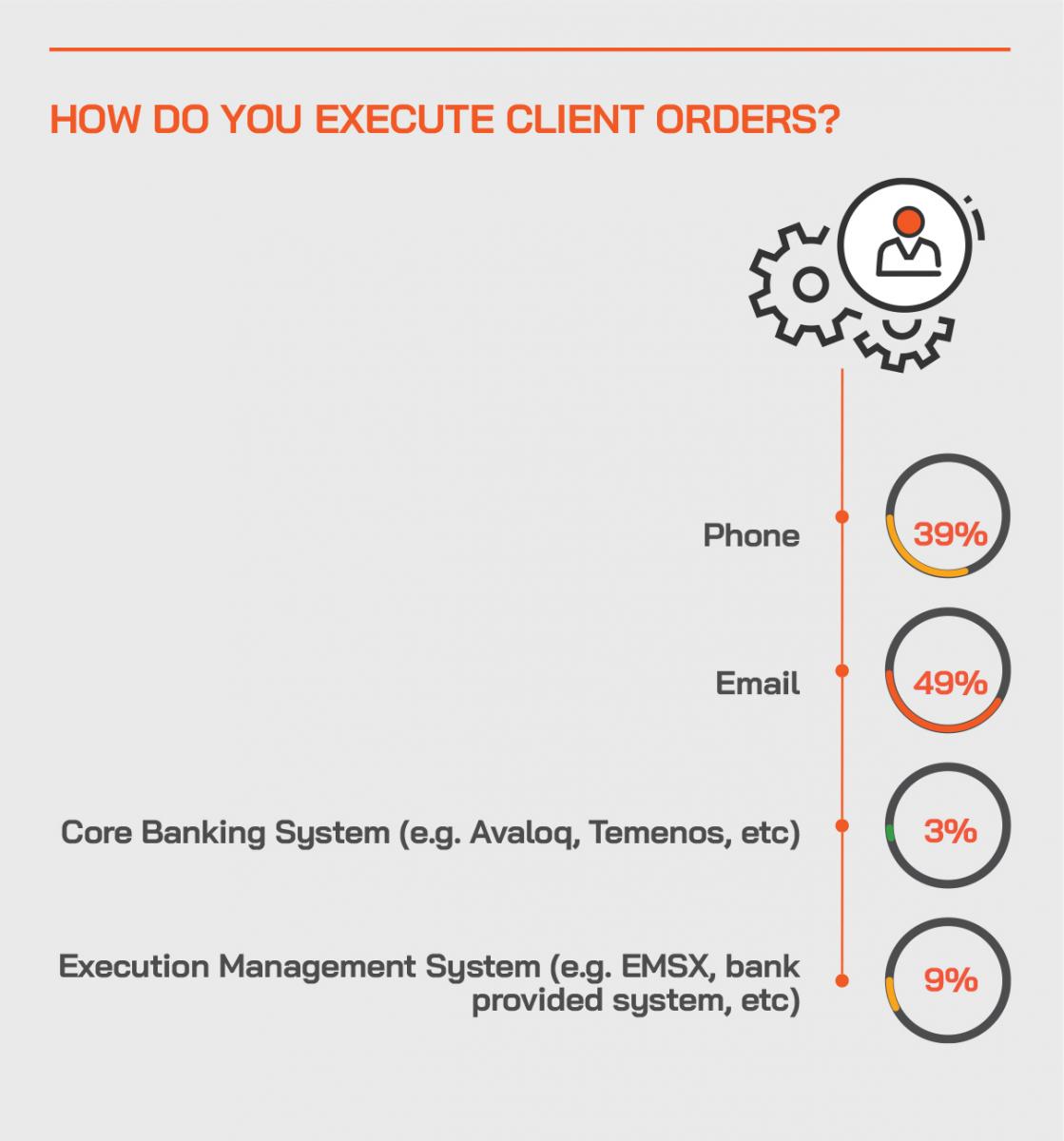

For trading, the IWMs naturally deal with both their private clients and the custodian banks, brokerages or digital platforms through which they place the orders. This process takes place through a variety of communication and confirmatory avenues, of which email represents 49% of the execution confirmations, and phone calls 39%, recorded of course if processes are followed correctly. In short, the latest digital solutions are not widely employed even today, even though such advances are widely and readily accessible, even for smaller IWMs.

Execution in a multi-asset world is challenging and ‘best execution’ is still elusive. Private banks and asset managers who make investment decisions need aggregate information about their clients’ portfolios, real price information, and to eliminate execution risk. Wealth firms and family offices need to integrate new technology, data and analytics across their whole ecosystem.

What is needed is digital systems that connect with legacy core banking software, so that the fairly daunting tasks of digitising workflows like trading, compliance checks and portfolio aggregation can be overcome. A workflow solution that can connect to banking legacy systems and provide the layer of digital efficiency to wealth and asset managers is very much in the foreground in terms of the answer to this conundrum.

The replies we received appeared to indicate with some conviction that the IWMs have fully recognised the issues they face and are prepared to address these head-on. For example, some of the more prescient firms have migrated workflows to the cloud, as previous concerns around the security of client data have been allayed by the experiences amongst industry participants and indeed the regulators.

Cloud and SaaS

Moreover, the pandemic has further accelerated this migration towards cloud and SaaS [software as a service] to the point where the cloud is now perceived as not only the safer and easier solution, but a cheaper option to implement. It also makes it easier for the RMs to implement orders effectively, as there is the one central warehouse for all communication and alerts, which at the same time is visible for the top management and for the compliance specialists.

Additionally, there are checks and balances in-built, if properly structured, with the potential for a safety net of a full audit trail in case anything goes wrong, including real-time pre-trade risk and compliance checks built into cloud-based technologies to manage orders. This is especially vital if market volatility surges, as it did earlier this year, creating much more pressure on order flow management, just at the time when key staff are dotted around their homes and a variety of locations.

Expert Opinion – Will Lawton, Global Head, QUO: “The wealth industry needs to address the need for streamlining and modernising many aspects of their service yet still maintain compliance rectitude and rigorous risk controls. The FIX connectivity for trading protocols has been the standard approach for execution across all asset classes in the institutional space globally for many years, yet most private banks and wealth managers in Asia have not even started to use FIX – energy and time should be spent by the banks and wealth firms on servicing clients and not paperwork and antiquated manual execution and order management methods which of course lead to slippage, time-wasting, errors and ultimately cost to the client and reputational damage to the providers of these services, let alone the compliance risks.”

Market Insights in Asia

Hubbis also asked our respondents for their comments on a few key areas. We have distilled their comments here.

Hubbis: What are the key business challenges you face scaling your business and managing multiple clients? What are the main operational hurdles you face today? And what would you do differently looking ahead to a post-pandemic environment?

- We are challenged by lengthy account opening procedures at custodian banks.

- Regulatory reporting and reviews are difficult.

- The whole area of digitisation is challenging.

- It is difficult to find the right balance between customisation and standardisation (reports, processes and investment strategies).

- It is difficult to reach the right balance between automation versus manual and customised.

- We struggle with support and administrative functions that are still relatively manual and people-based.

- Some clients have turned cautious in their trading due to fall-out in their own business during this pandemic.

- It is a challenge to collect and then assemble good quality data from the various custodian banks.

- We are uncertain whether presently is the right time to scale up given so many uncertainties.

- Portfolio construction, monitoring and execution are all challenging areas.

- Finding the right people and good support staff is difficult today.

- The larger the client, the more we need to customise for them, so we need more resources.

- Not being able to physically have the whole team together causes many issues.

- Not being able to travel for face-to-face client/prospect meetings.

- Inability to travel to source new clients.

- Fewer operational concerns, but it is difficult today in terms of soliciting new clients, as almost all face to face channels have not been available during the circuit breaker periods.

- Building new AUM is challenging.

- It is difficult to not be able to have physical presence of staff to discuss issues, raise ideas, prepare presentations and so forth.

- Prospecting of certain market segments has been a little difficult because of travel restrictions, but otherwise we have done well and things have gone fairly smoothly during this period.

- It has been challenging not being able to go office to exchange trade ideas and brainstorm with colleagues.

- We have fully migrated to cloud and remote working has caused no major issues.

- Business development and new client acquisition have been the most difficult areas to address.

- We would like to increase online order placement and have more tech friendly applications to communicate with clients as well as data applications that show client assets more effectively.

- We strive towards more online access to portfolios and market data.

- In the future we would aim for more zoom meetings and webinar conferences and reduce in-person meetings for greater efficiency.

- We probably will be more flexible with WFH, but we hope that eventually all staff will be back in the office.

Money must be well spent

Some might assume that the IWMs of Asia, most of them far smaller than many of the much larger independents in Europe and the US, have little or only modest budgets available for front-to-back digitisation, but the mission to elevate their efficiencies and drive customer and even RM satisfaction has come into even sharper focus since the pandemic hit and the value and logic of digital solutions came into even sharper focus worldwide and across so many facets of our business and social lives.

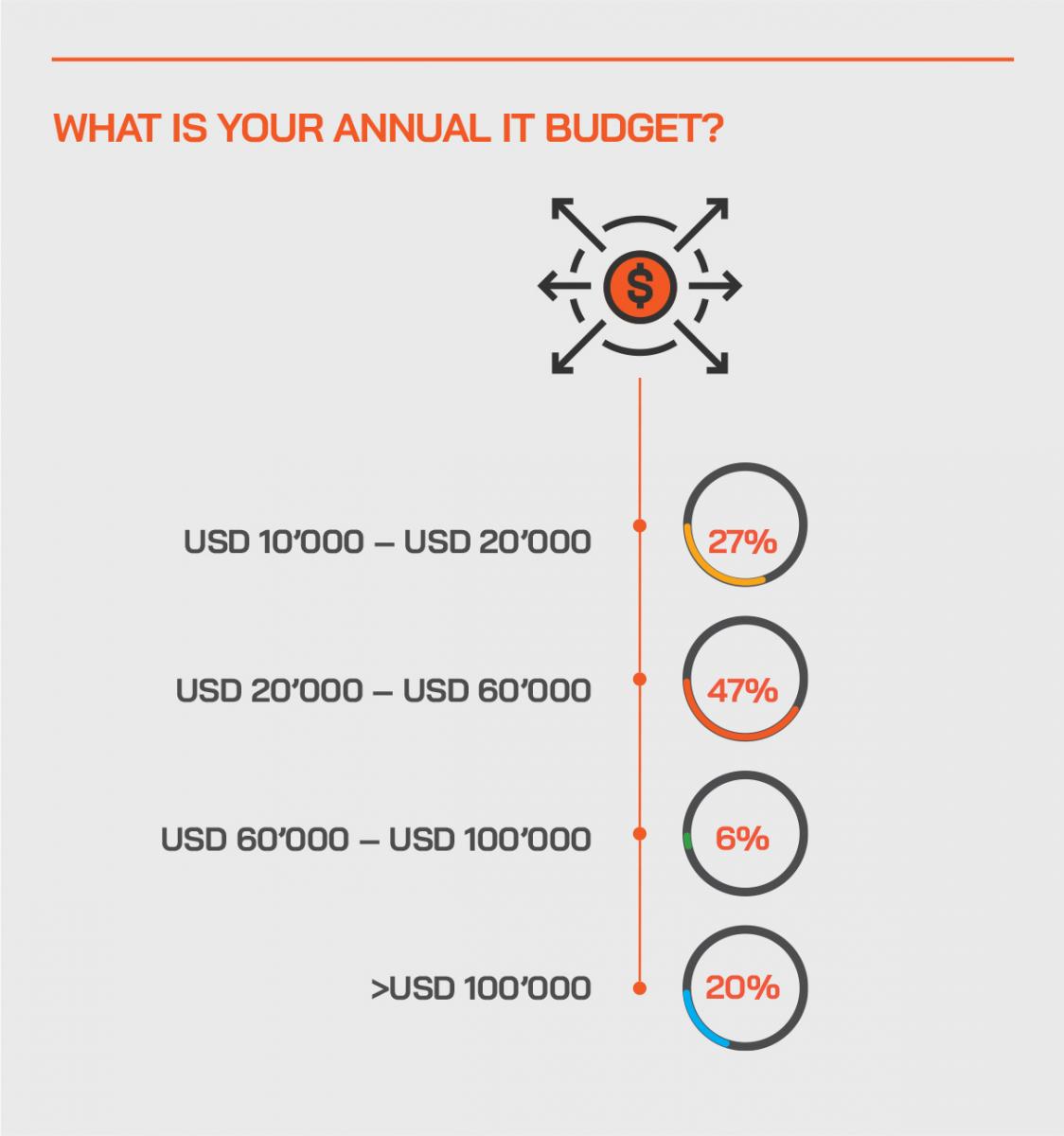

Our survey found that while 27% of respondent firms only have less than USD20000 annual IT/digital budget, 47% are armed with USD20-60000 and 20% more than USD100000. This means that their ammunition to target the weak points in their businesses is enough to make meaningful impact. But it is a reality highlighted in almost every Hubbis survey and event of the past year or two that these budgets can be wasted if there is not a clear vision of the objectives at hand, and a robust strategy for implementation.

Expert Opinion – Will Lawton, Global Head, QUO: Creating a future proof wealth practice requires a holistic approach to digitisation; simply buying technology tools isn’t a viable solution. Multi-custodian systems that integrate with legacy core banking solutions are the way forward.”

The final word

The private banks and IWMs of Asia have thus far weathered the Covid-19 storms rather well, better perhaps than might have been expected, and they have done so because they were already along the road to more comprehensive digitalisation. As they have passed the fear of survival phase, and as they have seen living proof on a daily basis of the real value of digital solutions, they now appear ready to be more critically engaged in bolstering the vital areas of their businesses that can and certainly need to still be improved.

There is no doubt whatsoever from our findings and from the body of work that Hubbis conducts daily and perennially amongst the wealth management firms in Asia that there is a great necessity to improve trading and execution, eliminate errors, especially relating to portfolio aggregation and reporting, in moving to a fully-fledged real-time regime, and generally in working more flawlessly on portfolio analytics and more seamlessly and harmoniously with the custodian banks.

QUO Looks to the Cloud to Help Wealth Managers in Asia Boost their Competitive Edge

It was in March 2019 that Trading Screen, a global provider of cloud-based financial markets technology for order and execution management systems (OEMS), announced the global launch of QUO, its latest investment management platform. Will Lawton, QUO’s Global Head, based in Singapore, has been hard at work elucidating his deep-rooted view that the independent wealth sector and the ‘neo’ banks can mount an ever more vigorous challenge to the incumbent private banks across the globe, but also that the banks can and will fight back, particularly against the challenger banks, as the entire industry propels itself towards streamlined administration, a much more user-friendly interface and connectivity, and perhaps the rise again of a new era for alpha generation and the wider wealth advisory proposition.

QUO offers a unique cloud-based ‘software-as-a-service’ (SaaS) investment management platform, providing investment managers efficient and streamlined execution across multiple workflow streams.

“For wealth and investment managers,” Lawton explains, “adding value to clients is at the top of the agenda, ahead of complex and costly IT solutions. QUO represents an outstanding lighter-touch OEMS that is easy to deploy and that simplifies investment management processes, from the start of day file uploads to order execution. We see this as an essential part of what is a vital and very pressing need to bring incumbent private banks and other wealth management firms into the modern world.”

Different features of QUO allow investment managers to adjust seamlessly between different trading strategies, giving them a more comprehensive view of their portfolios. The premise of the QUO ‘software-as-a-service’, cloud-based solution and platform is, therefore, to enable execution across multiple workflow streams, adjusts between different trading strategies, offers a wide-angle view of portfolios and allows users to trade directly without having to log into multiple portals. This means firms with various trading systems will be able to view all asset class activity using just one screen efficiently. By doing so, QUO can help propel the incumbent banks and their legacy systems and practices into a much more competitive situation.

Lawton is based full-time in Singapore, and was in fact born there to some of the earlier multinational expat parents, who then they stayed on and became Singaporean citizens. Lawton therefore has extensive experience of the local Asian culture and business environment, and also of wealth management, gained over some 30 years with leading banks, half of which was in Asia, including as Head of the Investment Group for HSBC Private Bank in Singapore.

Lawton is a believer in the power of technology, but he is not a believer that technology will replace the human capacity, as the human touch will, in his view, remain central to wealth management.

“The digitalisation that wealth management providers adopt must be aligned and structured to improve workflows, improve efficiencies, improve compliance, improve pricing and deliver coordinated information and support to the RMs, rather than just relying on his or her personal capability,” he states. “Accordingly, embracing these technological advances and opportunities is vital to future stability and success for those who want to be successful and sustainably so. Those who do not will risk losing clients and losing their business.”

Lawton also recognises that there is a divergence - some private clients wanting to continue the same modes of engagement with their banks and wealth firms, while others will want more seamless remote and full-service access. But whatever the type of client, all parties need to significantly improve their execution of orders, processing them swiftly and accurately.

The entry price for products is now much lower and more transparent than before, commissions considerably lower than in the past, but clients can lose out badly with poor execution of their trades, and that cannot be a source of discontent amongst the clients, given the immense and rising competition out there. Accordingly, he is promoting a major upgrade of execution practices and workflows, offering this capability directly to the clients or to the RMs, or both, rather than orders being processed, perhaps poorly and slowly, through some centralised desk.

Looking ahead, Lawton also sees a very different investment landscape from the past decade, and just possibly it might be one that will bolster the more traditional wealth management model, with the world very probably in for a sustained peak period of much higher volatility as the full extent of the virus’ impact on the global economy is felt. And that means more potential to produce alpha, and that in turn means more value in good advice on a relative basis.

Amidst this, Lawton is ever more convinced that there is today a rapidly increasing need for more efficient trade processing with risk monitoring, an integrated and consolidated view of trades across multiple assets, more streamlined execution and a better visualisation with data analysis features.

“Adding value to clients is now an increasingly important requirement, and now there is really a great OEMS option that we can offer that is easy to deploy, that offers simpler processes and does not require multiple log-ins and permissions for any investment strategy execution. The various key features of our new QUO platform will allow investment managers to adjust seamlessly between different trading strategies, giving them a more comprehensive view of their portfolio.”

TradingScreen itself is a privately-held company with over 200 employees globally with offices around the world. TradingScreen caters to four key customer segments: institutional asset managers, alternative asset managers, hedge funds and wealth managers, as well as catering to specialist segments like exchanges. It provides solutions in execution management spanning all assets including equities, derivatives, forex and fixed income with workflow including sourcing, accessing and aggregating liquidity and positions.

He concludes that as the Asian client base is generally multi-banked, even today, and also far more active across asset classes than the wealth management communities in Europe and the US, this situation neatly aligns with the QUO platform capabilities, hence the Singapore HQ he heads for the region.

“Our platform,” he says, “targets the wealth community covering private banks, asset managers, family offices and traders and features multi-asset position aggregation, navigation and compliance, trading, order management and market data provision. QUO is essentially a one-stop shop, so if you have various custody accounts or bank accounts and you have various brokers you deal with, the one platform can execute all of those, and direct all of those orders, and the QUO customer can holistically look at the entire positions and do some analysis on that.”

“And,” he concludes, “as technology adoption is the number one priority for wealth managers globally according to a Thomson Reuters and Forbes Insights survey of 200 wealth managers, it is clearly the vital key to gaining and maintaining a true competitive edge.”