Execution and Custody: The Key Trends and Developments for Independent Wealth Managers in Asia

Nov 22, 2021

The pandemic has wrought havoc and sadness across the globe, but in the world of wealth management, times have seldom been as good. For those providers of digital execution and custody platforms, the combination of increased remote working practices and ‘smart’ access to financial services of all types has fast-forwarded their business models beyond perhaps where they might have imagined if they had been asked for their projections in late 2019. The journey remains the same, but the train has evolved from the inter-city express to more of the TGV/bullet train variety. The Hubbis Digital Dialogue discussion of November 3 looked into the state of the independent wealth management execution and custody market in Asia and debated how much progress these platforms have really made against the historical incumbents – the traditional Tier 1 global private banks – and how the competitive arena has been shaping up, especially as there is no doubt that the banks have been upping their games as well. How then have the digital platforms refined their offerings, their marketing, their business models and their strategies to convince customers to turn to them for the most compelling, best-value custody and execution proposition? Who are their customers, and why? And what does all this mean for the Asia Pacific wealth management markets, where even amidst the impediments created by the pandemic, economic growth remains positive in most countries, and private wealth creation even more robust? Our panel focused most of their attention on issues around custody for this event, as custody represents an appealing annuity-type business with immense economies of scale available for those that win more and more of these clients. Moreover, perhaps custody is where private clients are more cautious about shifting their allegiances, often preferring the perceived safety of the major banking institutions and well-known brands. However, scratching slightly under the surface, it is easier to see that some of the digital platforms offer both a compelling execution offering and also a safe, secure and state-of-the-art custody proposition.

The Panel:

- Christopher O'Meara, Chief Executive Officer, Conduit Securities

- Urs Brutsch, Managing Partner & Founder, HP Wealth Management

- Rafael Weber, Head Institutional Clients, Swissquote

- Mithun Ghosh, Chief Operating Officer, Asia & Middle East Group Chief Risk Officer, Taurus Wealth Advisors

- Lucie Hulme, Chief Executive Officer & Partner, TriLake Partners

The Key Observations

There is no one-size-fits-all custody & execution proposition to suit all clients in today’s world

An expert opened proceedings by remarking that no one size fits all in terms of custody and execution. “Some simply need very low cost, others might need more help with private equity, and there are evidently many factors to consider when choosing a good custodian, including the services offered, the technology, the flexibility, and the value they truly offer the clients.

Quality data feeds between custodians and clients is crucial, pricing of the services less so

Another expert whose independent firm works today with some 15 custodians overall offered his perspectives, noting that they all have their pluses and minuses and that their firm looks for service quality, speed of execution, ease of working relationships, rapid turnaround time for requests or account openings, and so forth. “Pricing is not so crucial,” he reported. “There is somewhat of a race to the bottom in recent years, but for us, things like the quality of the data feed from the custodian banks into our system are more vital, especially with the more clients we onboard, because manual intervention becomes more and more difficult in trying to upkeep all your portfolios across all the different banks.”

Choice is essential for clients

Another guest concurred with the comments, noting that their firm had a similar number of custodian tie-ups and were platform agnostic. “I agree that no one size fits all, we like customised and we like to let clients have the entire suite of options, and for suitability, it really boils down to the profile and the match of the service suite from the providers end.”

Going beyond efficiency of execution, beyond ease and beyond cost

The same guest added that whilst a bank’s approach will typically be focused at acquiring a share of wallet of the end client, the EAM approaches it from the perspective of managing that end client. Accordingly, he said, EAMs want the ability to collate information across the different providers with which their private clients want to custodise their assets or execute their trades. “Personally, I feel that there needs to be more progress in aggregation, for common access to gain access and view your client statements.” Another panellist agreed that data aggregation is still lacking and a major ‘hassle’. “Asia is rather fractured compared with the US, Europe or Australia,” he reported.

The need for financial integrity and robustness

Another guest said that another key issue is the financial integrity of the custodians, even the brand names out there. “We need to separate the financial part and the operational side they are both very important, but I think the first test to pass is basic hurdles like credit rating, capital adequacy, key financial ratios, because that's the first conversation you're going to have with any private client.”

Key attributes

Another panellist agreed with the comment on financial stability as a base for custodian selection, adding that especially during the remote working since the pandemic hit, a high-end technology platform is vital for service quality and speed of execution 24/7. He explained that as rightly pointed out, the connectivity of the portfolio management system of EAMs is also crucial to help them build their businesses.

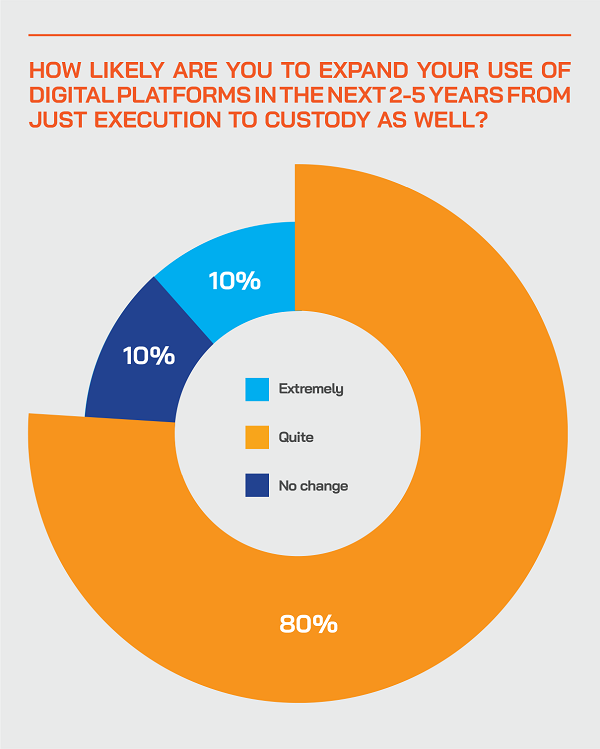

How significantly has the pandemic increased your likelihood of increasing your business with the digital platforms?

Massively 15%

Quite a lot 70%

No change really 15%

How well are the incumbent private banks competing to retain or win back market share of product selection/availability/execution?

Brilliantly 5%

Quite well 45%

No change 20%

Not so great 25%

Awfully 5%

How well are the incumbent private banks competing to retain or win back market share of custody?

Brilliantly 10%

Quite well 30%

No change 40%

Not so great 15%

Awfully 5%

Clients are wary of opening new accounts, hence the numbers of custodians EAMs continues to expand

As EAMs get bigger, there is no inverse consolidation amongst fewer custodians. This same expert added that instead of consolidating custodians, they have even been adding numbers in recent years, as they themselves grow.

Why should this be the case? “Clients are increasingly reluctant to start new relationships, to sign new forms and go through the KYC and onboarding hoops again,” he explained. “And I think asset managers are increasingly lazy to go through the process and are frustrated with the processes. We recently opened a new account with a major bank in Singapore, that took some nine months, that is truly disheartening, even though the client was already on the bank’s books, but it was just a new relationship under a different structure. That was an extreme case and not entirely the fault of the bank, as there were trustees involved, but it was a painful reminder.”

Another guest agreed, adding that their EAM has increased from some 8 to 12 custodians in recent times. “I don't think this number is going to decrease as well for exactly the same reasons cited, that clients are reluctant to change, because it's becoming so very difficult to open accounts. Moreover, many expat clients are moving, for example from Singapore moving to Europe, to Australia, and they need diversification in terms of jurisdictions and the custodians.” And as a result, consolidation, and data aggregation remain major challenges.

‘Pure’ institutional custody should be agnostic as to execution, but with private banks it really isn’t

A guest observed that custody in the purest sense is because is absolutely agnostic to execution. “You could be executing with every counterparty in the market, and the custodian’s job is to have that all fall in, settle, satisfy post trade, manage the MIS requirements, custody, corporate actions, and so forth. That to me is really what a custodial service will be about. But in the wealth management space, we're not quite there, it's aligned in the private banking offering, so it comes as part of the execution, the holding comes as part of the execution, you can't have one without the other. it's not a pure custody play. It should not be the case for pure institutional custody.”

Custody is simplest for simpler securities, so make sure the custodians can cope with diverse and sometimes complex assets

Another guest agreed, adding that due to scale, most of the EAMs don’t have that luxury of going to the institutional model of completely unbundling execution and custody, at least not with the traditional institutional bank custodians. “Most of our assets are not with private banks,” he said, “we try to avoid them completely; most of it is with digital custody and plain vanilla institutional custody. However, the operational complexity of separating execution and custody is not to be taken lightly, ensuring trades settle, what happens on exceptions when people are short securities. That becomes more difficult outside mainstream listed securities, which is why the digital platforms are very listed securities centric. As soon as you go off into complexity, structured products, bonds, OTC instruments, it gets harder. But demand for all those is increasing in wealth management circles.” Ergo, make sure the custodian is not only safe, offers excellent execution, provides seamless data and aggregation, but can also cope with a diverse range of sometimes more complex assets.

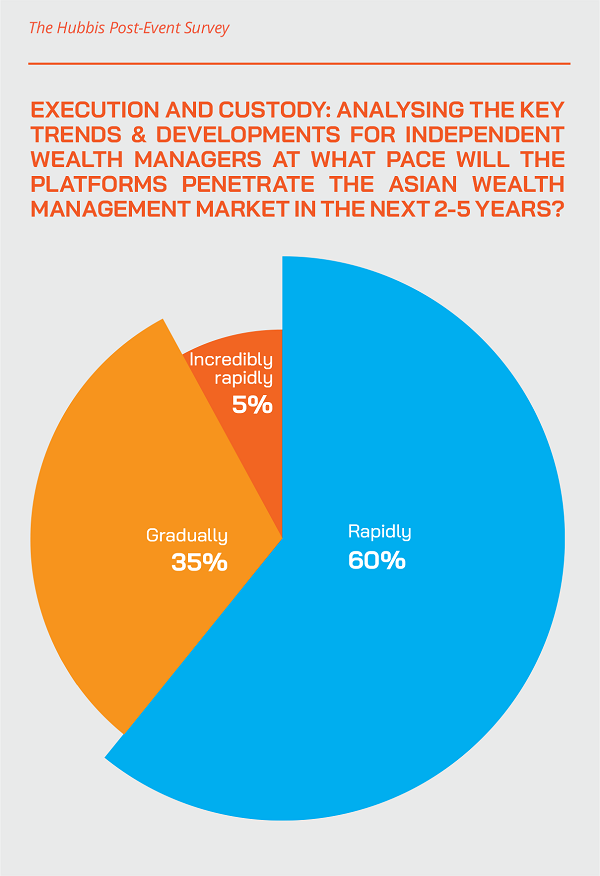

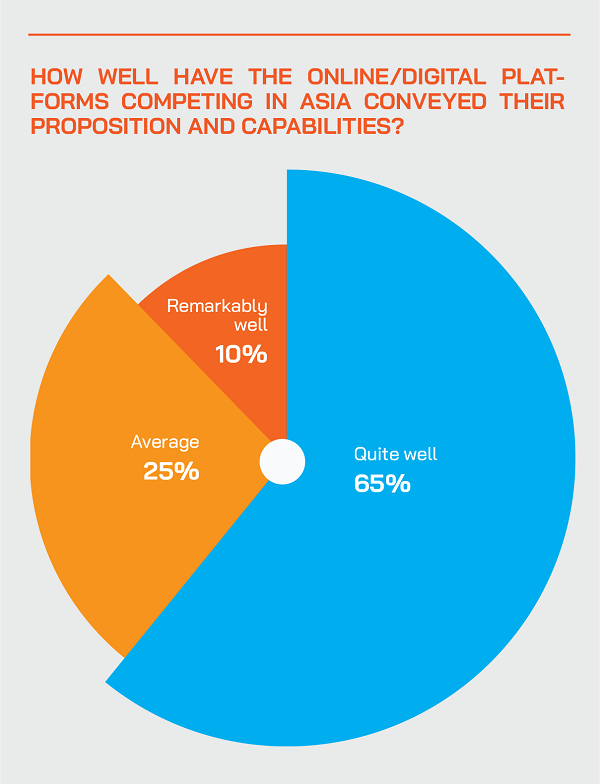

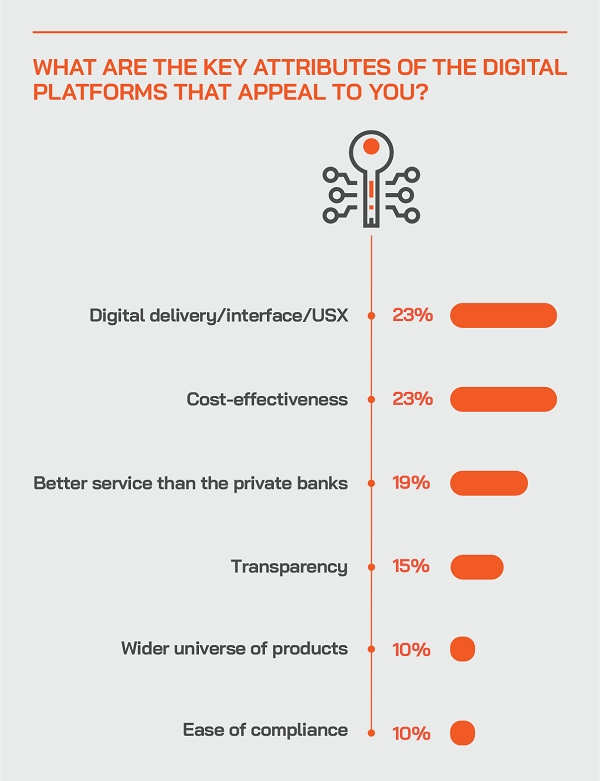

The Hubbis Post-Event Survey

We asked delegates for their views on these important topics. Hubbis has selected some of the more detailed replies from delegates attending the events, as follows:

Hubbis: What are the key attributes that the online/digital platform providers offer in terms of execution, i.e. their universe of investment products, their pricing, and your digital interface with such platforms?

- Low prices, sophisticated digital interface, although the product universe might be not as extensive as with other players.

- Pricing, updates, fast execution.

- I'm all up for it. It is definitely where we should be now. Especially with the pandemic and that most clients have less and less time to spend inside banks, and the availability of information can be very beneficial.

- Accessibility (price/cost, supportability, and usability) , user friendly interface, security, platforms which can be integrated not only to one system but to multiple systems.

- Pricing and a seamless digital interface.

- Speed, efficiency, reliability.

- In our experience, the online/digital platform for execution can deliver efficient execution results, and it is convenient for wealth managers when they are travelling or outside the office.

- Speed, directness without the need to go through the RMs each time.

- Breadth of products, multiple asset classes and ease of execution, as well as updated account reporting on a daily basis.

- Although the cost for execution from the digital platform is cheaper, as an Independent Asset Manager, I do care greatly for the asset custody safety. Therefore, we may still prefer to use the hybrid methods of both digital and traditional bank platforms for the clients.

- The pricing and definitely the ease of trade execution and the speed to execute those trades.

Hubbis: In your view, are the outsourced online/digital platforms winning hearts and minds in terms of custody versus the traditional bank incumbents, and why, or why not?

- Yes, I believe so, for price sensitive clients, and if the digital platform can prove itself to be safe and established, then they can offer big benefits versus traditional bank custodians.

- Yes, because they are efficient and user friendly.

- Taking out the layer of data security, custody is another level of audit and tracking which is both very useful to end users and banks/prime brokers.

- For my particular private client base, traction is thus far slow largely due to unfamiliarity and our client age demographics.

- Yes, they solve lots of effectiveness and custodian matters, as banks have too many cumbersome steps and matters like voice logs and confirmations afterwards, so on and so forth.

- It is hard to tell at this stage. For independent wealth managers, the traditional custody services offered by private banks have their merits, such as efficient credit balance updates, and sufficient staffing that helps IAMs in urgent events and emergencies.

- Currently they are still not fully winning the hearts/minds in terms of custody, as people still tend to prefer the historical, tangible custodians for their investment assets. Hopefully in the future this will change, as they have a good offering for the IAMs.

- Not yet, but the momentum is growing. It will take time to build up branding and reputation and break through in terms of market penetration. This is a multi-year game.

- I think the trust and integrity of the traditional bank incumbents are more important still, as they are well-regulated, for example by the HKMA here in Hong Kong. Hence, it is still difficult to entirely shift out from the traditional bank incumbents.

- To some extent yes, they are getting there, but more so for the price sensitive customers.

- While they are getting better than the traditional banks, I don't see state-of-the art proposition yet. In short, they have a way to go.

- Ease of accountability, and the ability to deal with multiple assets and multiple client requests.

- As to unbundling in general, it may not be able to unbundle due to cost and fee income factor. If custody and execution are separated, banks may raise custody charges, while the wealth managers may encounter increase of labour costs as well.

- It is really very difficult to unbundle custody from execution due to expectations of efficiency and accountability amongst end clients.

- We think there will be greater unbundling. The private bank network is a closed shop and execution is effectively an additional cost to custody. The banks do not trade, they arbitrage others’ prices with an added margin in my view.

- The private banks will endure and the smaller EAMs and IAMs will disappear or merge. It is already happening. As a result, we are not sure if an unbundling of custody and execution will take place anytime soon.

Should the EAMs lead the clients, or should the clients lead the EAMs?

Good guidance and smart selection curation by the EAMs certainly help many private clients. A guest pondered whether EAMs should take the high road and try to prevent the clients making all the key custody decisions, instead taking the advisory route and giving them the benefit of their wider knowledge of the custodian and execution capability and choices in the market.

“I personally think a good EAM should really drive the clients and actually should offer a solution,” they said. “Some clients arrive and don't know how to proceed or who to go, so going through a process with them is helpful. We can eliminate, so for example in the size of AUM, half the banks in Singapore won’t take clients who have less than USD5 million in AUM, then you can work through preferred jurisdictions, whether Singapore, Switzerland, Dubai, Hong Kong, and you can look at where the clients reside. Some banks won’t take clients in some jurisdictions, for example Thailand, other custodians do not take that approach. The final choice comes down to who is left, then who are the more flexible, who we know best, who will onboard the client rapidly, who offers the right pricing and the overall quality of their services.”

Why then do EAMs still work with the private banks? And will the overall wealth management offering unbundle further?

A guest asked this question, rhetorically, answering that private banking is young in Asia compared to other parts of the world, and the world of EAMs in Asia even younger.

“Before, a client will go to the bank and get advice, custody and execution, all at the same place,” he remarked. “Then the IAMs started to unbundle the advice and take that out and use the private banks basically for custody and execution. In the next phase, we will see more unbundling. Right now, this is somewhat slow, partly because of the onboarding and difficulties, partly there is client resistance from leaving their private banks, which might often be inviting them for nice vents and dinners and so forth. I would expect us to face resistance going forward in further unbundling the offering, but I do think it will happen. I wonder if in five to 15 years we might not be using the private banks anymore, we will use someone for custody, someone, maybe the same platform, for execution. And as to products, you can also buy directly from product providers, or asset managers, or fund managers. To sum it up, I wouldn't want to be in the shoes of a private banking CEO, because I think he will get disintermediated left, right and centre.”

But others believe the private banks are here to stay in the world of custody

“Private bank custody is here to stay,” another expert asserted. “It's not something that's going to walk away, they provide balance sheet leverage, which is probably the key component of why you would go to a private bank. I think, trying to build a wealth management business that competes on custody and execution alone is probably not the best strategy. Optimising execution, for example getting the right bond at the right price point in the market, is not too important unless you are a major institution. But for custody, I believe the banks are here to stay, as the operational complexity of going outside that arena is probably just too hard. Is it going to get you more business as an EAM? Will it make your clients more money? I am not sure…”

However, disruption of core private banking activities continues apace

Nevertheless, another expert observed that the disruption of private bank services in ongoing. He cited, for example, access to private market assets, which used to be the purview of the banks, but where there are more and more disruptors. He said the disruption continues, but he did agree that the private banks will remain as players in the world of custody, even if they are increasingly challenged in terms of services, quality, pricing and user-friendliness.

And even if more unbundling takes place and whatever the trends, EAMs must not limit client choice

Another expert concurred but said that EAMs must not limit client choice and tell them, sorry we don’t work with this or that bank. “There will be some guidance based on our experience for different profiles, and we do have some influence, but we need to offer the choice,” he said. He added that the onboarding hurdles could be better overcome with a more holistic approach from the banks, rather than simply throwing more people at these issues, which can actually increase the delays as there are then too many layers to go through.

“They need a real conceptual framework around how to do it more efficiently,” he observed. “But sadly, compliance as a function has lost any sense of accountability around the business delivery. I'm not saying it was right in the day where business got to sort of dictate the timeline within which they needed a KYC concluded, but we've sort of moved an entire 180 degrees to where compliance probably in most banks has zero accountability as to when they need to revert on a case and then it just goes to too many layers, too many approvals. Too many people too question, too many people to farm out to get those answers. You could approach this is a more focused and efficient manner, where it's well-defined, roles and responsibilities are well accounted for.”

The challenges of consolidating data feeds from different custodians are significant and constant

Returning to the earlier conversation around reporting and the importance of robust data and feeds, a guest said that their EAM always uses the bank statements to show their clients, because that is source data, supplemented with their own data, some as direct data feed, and some input manually. This guest explained that they have one person whose core mission is to handle this data management process into the host bank software. “It's a lot of work, for sure,” they said.

Another guest agreed, noting that their EAM has a whole team in operations, who ensure that the accounts are fully reconciled with the bank valuations. “We still have quite a few banks where we don't have a proper data feed, and that takes a bit longer, but it's worth it, because I think particularly a family office client or someone who has assets across five or six different custodians, it's very difficult for them to do it on the back of an envelope, or even use an Excel sheet to do it properly. And I think that's really where a proper system comes in. It's very expensive to run that, particularly if you add on the operations cost, staff costs. But I think it's the ticket to the dance if you want to entertain someone larger, maybe more complicated clients just in terms of aggregation of their wealth.” Another guest agreed, adding that it is also very important for the risk management of the portfolios.

But it all still remains rather too archaic in terms of process and technology

Another expert said this all remains so manual today that it is borderline criminal. “You do have pockets of electronic feeds and you try to gain efficiencies, but it is all still largely PDF reliant. “We have worked with optical character readers, and so forth, but they're not fool-proof technology, the banks keep changing the column widths and rows often enough for even your best OCR solutions to fail. So, there is a lot of manual intervention. And time is of the essence, you want your data at your end as real time as possible. Accordingly, we have tried to digitise what we can working with the elements that we have at our disposal but given the over-reliance on PDF statements within wealth management or private banking today, it remains a major challenge.”

And implementation, even of advanced data feeds, remains far too complex

He said it was ironic that even for the banks which have some capability for digital feeds, there is usually a significant gap to jump over. “The implementation, getting the data through an API, transposing it to your system requirements, it is all such an ordeal as you are often dealing with non-technical people to put in place a technical solution. In short, it is not just about the capability; the banks need to start thinking through where they have the capability on the delivery and the implementation of that with their end clients, meaning us the EAMs.”

Although regulation might demand concise reporting, do clients really need or use it?

Another perspective came from a guest who said compliance demands accurate and timely reporting, but he senses that not many clients use the statements. “Even if you have it all done perfectly with all the pretty charts and bells and whistles and consolidated reporting, how many people will actually use it?” he pondered. “Are you going to get more clients for doing it? I actually think the one-on-one link to the relationship manager is pretty important, many private clients would rely on that sort of notification when things are going wrong.”

But some consider that data feed and aggregation are far more than simple ‘hygiene’, indeed that it is core to their client engagement

Another guest said that for them, it goes far beyond utility for clients. “For us, it goes well beyond the regulatory requirement around the reporting,” he said. “In fact, I'd go as far as to say that our reports or our analytics on a holistic basis, once we've done the consolidation from the different source for each client, are a cornerstone of our client engagement in terms of walking them through, keeping them apprised on their portfolios. This is all quite vital or centric to us.

A fellow panellist agreed, stating that is is also central to the whole engagement with clients on their holdings, their performance and allocation and so forth. He did however concede that the time and effort required with so many manual processes are onerous. “It is worth the incremental gain,” he said, “but the point is, you basically do your aggregated reporting, you're spending money to do it, however you don't need to go full data analytics, that is not necessarily worth it.”

And in the future, the demand for and interest in holistic reporting and insights will increase

And a guest observed that in the future, the clients might well rely less on the personal connection to the RMs for keeping them up to date. “While the RM connectivity will remain important in my view, the next generations of clients will put much more importance to actually having a complete overview, and not only of the bankable assets, but also more importantly of the non-bankable assets as well. And the EAMs will be at an advantage with this full picture. With the right partners that offer simple connectivity, which is simple to use and implement, and also cost efficient to implement, particularly if you have a large number of custodians, they will be at an advantage.”

The combination of technology, processes and human connectivity will provide EAMs with the best solutions

To conclude the conversation, a guest highlighted how the combination of a personal relationship and independent advice combined with the latest platforms and technologies will definitely be the winning combination.