Publications & Thought Leadership

Creating a Robust Family Succession Plan that Embraces Governance, Tax & Compliance

Mar 24, 2021

As the founder generations of Asia’s wealthy and uber-wealthy families and family dynasties increasingly seek guidance for wealth, estate and family business transition to the younger family generations, it is important for the private banks and other advisory firms in Asia to understand how to deal with the clients in relation to the extremely sensitive and highly personal matters of estate, legacy and succession planning, while at the same time nurturing inclusiveness amongst the next generations that will, they hope, become their clients in the years and decades ahead. It is vital for Asia’s wealthy families to create the right wealth structures, to accept the need to distance themselves from those structures, and to work with those bankers, advisors and professionals who will truly help devise and revise the best possible plans. In the worst case scenarios, it all goes horribly wrong, and disputes dominate, rather than family harmony, and that is certainly not the legacy that Asia’s wealthy want to leave behind. Hubbis assembled a group of erudite bankers, lawyers, trust and other experts specialising in this crucial field of estate planning and transitioning to discuss why, and how to expedite well-conceived, well-executed estate and succession planning.

PANEL MEMBERS

- Kate Weiss, Managing Director, Asiaciti Trust

- John Shoemaker, Registered Foreign Lawyer, Butler Snow

- Paul Knox, Managing Director, JP Morgan Private Banking

- Vivian Kiang, Head of Wealth Planning and Trust Administration, Asia, RBC Wealth Management

- Markus Grossmann, Regional Managing Director, Trident Trust

- Clifford Ng, Partner (Hong Kong), Zhong Lun Law Firm

Wealth and business transition in Asia

Talking openly about succession with Asian families can be considered inauspicious and sometimes even taboo. Some families have embraced formal and semiformal frameworks using family charters, family arrangements, constitutions and so forth. In China, for example, many family businesses were born during the economic reforms of the 1980s, an entire generation of firms could be facing succession at the same time, creating significant risks at the same time. Unlike in Europe and the US, where many family businesses are in the fourth of fifth generation, many Asian business are still in their first-generation cycle.

An expert highlighted that according to a report from Deloitte on Asian business succession, some 81% of Asian families believe that the next generation will be able to take over the family business, while 93% of the first generation will work until their 60s and 70s.

But of course, Asia is vast, and markets and cultures differ greatly. But despite the sheer size and diversity of Asia, but that it is united in a widespread conservatism, which is endemic but varies somewhat from country to country and of course amongst different religions.

Expert Opinion - Clifford Ng, Partner (Hong Kong), Zhong Lun Law Firm: “How closely involved should the second and third generation be in the estate and succession planning: Clients need to consider carefully whether to involve their heirs in estate and succession plans. While transparency is a generally a good policy, information once disclosed cannot be ‘undisclosed’.”

An expert noted that Taiwanese clients, for example, want the second and third generations to join the family businesses, they are very conservative, wanting to extend the legacy that have created. Interestingly, they commented that China takes a somewhat different approach, being considerably more open minded to the roles of the second and future generations, and this type of attitude pervades Hong Kong and Singapore as well, where wealth is already often even in the third generations, and where there is far more diversity in the careers of those nextgens.

Another guest concurred, adding that the diversity means that one size will never fit all. “It's really important to look at the family values, look at the traditions, the culture and how that family works together. In Asia, those family values tend to be reflected in the way that the family business is run and is often bespoke to that family. Listening to the family, making sure how they want to see succession is really important when coming up with an idea of how the succession should look, and how best to plan for it.”

An expert cited a report that 57% of Asian families have a fear of sibling favouritism and/or rivalry and lack of consensus in the succession process.

“One further issue is the difference between the first and second generation,” she added. “Most first-generation business owners are entrepreneurs by necessity. The second generation tend to have gone to business school. There is a need to reconcile what the second generation has learnt in business school with the older generation’s expectations of appropriateness, courtesy and timing. In addition, it is important to document the knowledge inside the founder’s head, or the relationships the founder has made over decades and disseminate it to the next generation. These inherent conflicts can trigger family disputes, and that is why we need to involve several generations in order to avoid or to mitigate against family feuds later on.”

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “I believe recent events have heightened awareness that succession planning and the transfer of wealth should be carried out as a structured long-term strategy as soon as possible, seamlessly with communication, trust and support among all parties. The Covid-19 pandemic has brought mortality into sharp focus, forcing patriarchs of high net worth families to grapple with estate planning. However, this may not be an easy process because talking openly about succession with Asian families is often considered inauspicious and sometimes even a taboo. One way around this is to frame questions about the future or legacy.”

A lawyer offered his views, remarking that there is sometimes a disconnect between that families want to achieve that the family dynamics, which might restrict those objectives.

“Oftentimes,” he said, “you have to overcome years and decades of the family relationships in order to really make the succession plan work. And lawyers might not be best placed to help them there, as we tend to be more on the adversarial side, trained to act for one and not the others. We therefore have to be very careful in our advice and very open and transparent throughout.”

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “International families require independent fiduciary with multi-jurisdictional expertise. Though today’s rich, especially those in China, have built their wealth as entrepreneurs, conflicting priorities may arise during wealth transfer because for Asian business families, there is no clear distinction between personal and business wealth. Moreover, many of their family members and assets are spread across different jurisdictions, rendering taxation and regulatory compliance more complicated.”

Expert Opinion - Clifford Ng, Partner (Hong Kong), Zhong Lun Law Firm: “It is increasingly challenging for clients to comply with the maze of laws on tax, disclosure, economic substance, foreign ownership, beneficial ownership, control, etc. Add to that each institution’s different policies on all of the above means it becomes more expensive with more lawyers and paid advisors involved to ensure compliance. Cross border investments and planning has become a very expensive endeavour for a much smaller demographic of wealth.”

Another lawyer quipped that the crisis afflicting the British royal family highlights an age-old adage not to marry an American or move to the US, as you then get caught in tax and other potential traps. “Their situation right now,” he said, “has actually made it easier for us to demonstrate the complications that can arise when an American becomes part of a wealthy offshore family.”

Expert Opinion - John Shoemaker, Registered Foreign Lawyer, Butler Snow: "We definitely stress to non-US families that marrying an American or otherwise bringing the U.S. Federal tax system into consideration adds layers of complexity and is not to be taken lightly"

He added that the lockdowns had helped his practice, as people had more time and the virus had focused more attention on matters of mortality, succession and planning. He said it has also really helped the firm focus attention from a fee perspective. While the Asian market is notoriously fee sensitive, it is easier now to demonstrate value to clients, so they see the value in hiring a proper professional and a proper lawyer to protect their secrecy and the attorney-client privilege that the world of regulation has eliminated with their bankers.

The Hubbis Post-Event Survey

Hubbis: Are you seeing a much more active drive nowadays towards professional wealth, legacy and succession planning amongst private clients in Asia? Why, or why not?

The ‘Yes’ replies significantly outweighed the ‘No’ replies. We have selected some of the reasons delegates offered, as below:

- A really massive uplift in interest.

- Clients certainly value more professional advice on these matters nowadays.

- With increased affluence and education comes a more advanced appreciation of the needs for estate and succession in the modern, highly regulated world we inhabit today.

- The older generations have seen vulnerability in a starker light since the pandemic.

- Generally, clients are more sophisticated and more receptive to seeking professional assistance, especially the 2nd generation who often want to know more about wealth planning and succession planning.

- We are seeing more enquiries about succession planning, trusts, tax planning, and other matters, amongst wealthier private clients, as well as mass affluent.

- Succession plans are a priority project for Asian families nowadays.

- There is more awareness and education.

- The rich increasingly see the importance of succession planning, and want to ensure the next generation can either take over the business, or engage someone else to look after the business.

- In my opinion, many bankers actually take this opportunity to sell the importance of succession planning and build stronger relationships with their clients.

- More wealth means more planning ahead.

- A key driver is the younger generation, many of whom are not always willing to take over the family business.

- Better educated younger generations who see more of the ‘Western’ way of approaching these matters in a more formalised manner.

- Nowadays, it is essential to complement the financial planning with the succession planning element, or the two fail.

- Because the local and global regulatory environments are constantly changing and always becoming more complex.

- There are often highly visible stories of situations that ended up in disputes because the planning was non-existent or rudimentary.

- The pandemic is a game-changer for the mentality here and more and more families are embracing rigorous planning, and more and more family offices.

- The hiatus in activity globally has given business owners and families the time to reflect on these issues and also a clearer appreciation of their own mortality and therefore of the need to plan ahead.

- The Singapore government’s focus on attracting Family Offices and related financial services specialists here so we become the Switzerland of Asia has really boosted the focus and drive in these areas.

- The sense of impending doom since the pandemic hit has jump started the process in many cases.

Collaboration between the wealth and professional advisors

There is debate as to whether the private bankers and independent wealth management experts working efficiently with lawyers, trustees and other specialist advisors to help create and execute successful succession plans and structures that are also compliant with regulations and tax rules.

To answer this, a guest remarked that the success of any business succession strategy relies on effective communication. This is true both inside the family and with the advisors who assist in formulating and putting the strategy in place. “Involving external advisors in a succession plan may help with objectively balancing the collective interests of the family members,” she remarked.

She added: “The new normal where the trustees, lawyers, bankers and others are working more with video conferencing and more collaboratively is in fact helping with ensuring effective communication and sharing knowledge with regards to business succession. I am myself currently involved with an Asian family who are looking at business succession strategies. The patriarch and I were able to have a series of video conferences one morning with the tax advisors from jurisdictions around the world to discuss the tax implications of the planning that was put into place.”

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “It’s all about working together, and this is true both inside the family and with the advisers who assist in formulating and putting the business succession strategy in place. Involving non-family advisers in a succession plan may help with objectively balancing the collective interests of the family members. Trustee, lawyers, wealth managers need to engage in effective communication and sharing of knowledge to ensure a robust solution. Collaboration in a complex world, understanding the client, having the right solutions, and at times collaborating to assemble all the key elements in one package, are all vital elements for any provider wanting to survive and prosper in the fiduciary services world. We remain driven by devising and executing best-in-class solutions for our clients with the right structures onshore and offshore.”

The central role of family and business governance

A banker observed that there is a lot more focus now on family governance and business governance. He said that families operate their own governance in the normal course of their lives, working out between them all sorts of issues such as education, spending, and other matters, so that the offspring are gradually assimilated into that sort of decision-making process. However, in the context of major estate and succession decisions, the problems come about due to poor communication amongst key family members.

“What we can do is to share our experiences of where things have gone wrong in certain families and thereby encourage the right level of communication,” he advised. “The more you can avoid shocks and surprises, the more good, open dialogue, and the better transparency about what they want to achieve, the greater the chances of success.”

Asian family business companies are not typically run with the strict divisions between the chairman, the CEO and the board, according to one guest. Depending on the family, the family members involved in the business and the knowledge across the different generations depends upon how the business is made up. This family/business governance is usually on an informal basis and understanding the unique family governance goes a long way to understanding the way the business is run.

A lawyer observed that business governance is considerably simpler than family governance, as family dynamics are impossible to measure. To overcome key issues that so often arise, the vital first step and ongoing approach must be to enhance communication. “I try to separate the business side from the family side to the extent possible, and then when both are organised, we can try to bridge any gaps between them,” he explained.

Another expert commented that trustees can also play a role in advising on governance, and that he did not see any conflict of interest in that approach. “Trustees,” he observed, “often have quite a lot of information or can get a lot of information about the families, so they are well placed to ask such questions. In my view, it is actually an ideal position. I think it's a further development of a relationship with not only the settlor, but also with the different family members and to do this in a natural step by step way.”

Nevertheless, he also conceded there is also a question as to whether the families want such discussions, especially if in relation to straightforward trusts, where difficult discussions on governance and complex family wishes and dynamics are not so welcome or even required.

On the other hand, he also commented that the situations and assets and family mixes of these wealthy clients are at the same time becoming more complex, more cross-border and therefore the whole regulatory and tax environment becomes more complicated. “As a result,” he said, “in a good way, we kind of forced to have such discussions with customers, because those plain vanilla trust solutions are probably going to disappear in the times ahead.”

Expert Opinion - Paul Knox, Managing Director, JP Morgan Private Banking: “Alongside advising clients on technical issues, family governance in its broadest sense is likely to be an increasingly important area for private client advisers. If patriarchs and matriarchs want their wealth preserved over future generations, then they need to prepare their descendants to be stewards of the wealth.”

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “Family values and governance are key. Whilst an important factor, it is important that tax planning does not drive the family succession, but that the objectives, traditions, behaviour and values of the family drive the decisions. Once these have been determined, the tax planning, asset protection and timing of the business succession can be more effectively addressed.”

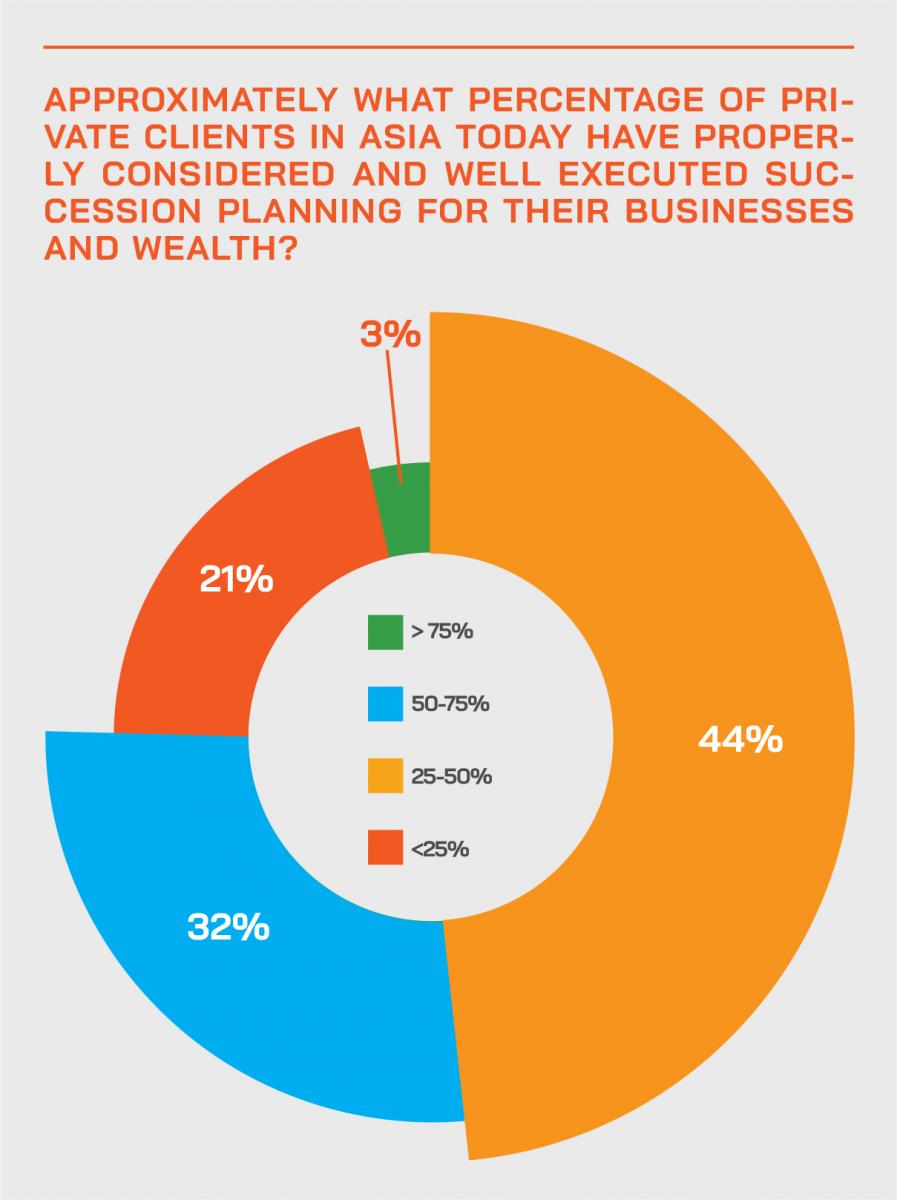

Family business succession – taking action

The focus shifted to the need for robust business succession planning and what might trigger conversations and then action. “In recent times,” they commented, “I have found that the patriarchs and matriarchs who I am speaking with, have suddenly got time where they were traveling around the world running their multinational, multi-million/billion pound empires or dollar empires, and they're now at home, and they have time to really think about their succession. That is triggering them to come and talk to us.”

And there is compelling evidence that this is an urgent need. An expert cited a recent study of 200 publicly listed Asian family businesses found that on average the stocks of these companies lost nearly 60% of their value during the years shortly before and after the transition from one generation to another. Estate and legacy planning is more important than ever to ensure that the value of the family business is not lost due to the succession. They added that the study also found that some 46% of Asian families fear discussing the future of the company beyond their lifetime.

Expert Opinion - Vivian Kiang, Head of Wealth Planning and Trust Administration, Asia, RBC Wealth Management: "Succession planning is more complicated for clients who have ties across multiple jurisdictions. To set up a structure, a team of experts including bankers, wealth planners, financial advisors, tax advisors, accountants, and onshore and offshore trustees are required. As with any project, a coordinator is critical for success. A Wealth Planner who understands the needs, requirements and restrictions of all parties can effectively play this role."

Succession planning is more complicated for clients who have ties across multiple jurisdictions. To set up a structure, a team of experts including bankers, wealth planners, financial advisors, tax advisors, accountants, and onshore and offshore trustees are required. As with any project, a coordinator is critical for success. A Wealth Planner who understands the needs, requirements and restrictions of all parties can effectively play this role.

To achieve these goals around succession, an expert advised, “these families need an experienced project manager to tie in all of the planning that needs to take place to put an effective business succession plan in place. They explained that with video call technologies now the norm, it was actually much easier to get all types of different parties together to analyse and discuss all types of challenges and propose solutions.

The same expert added that it is proving a really efficient period currently to effect business succession. “When it comes to working with different people, we are used to doing this as trustees,” they explained. “We have to work with lawyers, with accountants, with bankers, with other trustees, with directors of the family companies and others on a day-to-day basis, and it's really important that we understand that the different generations of the family, who may also have their own sets of lawyers, bankers, wealth planners, accountants who have got their own ideas, and are trying to discuss this planning with the person who's decided to take this planning up.”

They said that in light of this, it is vital to listen to all parties, from the wishes of the founders/creators, through the second and younger generations and also the various professionals involved.

Expert Opinion - Markus Grossmann, Regional Managing Director, Trident Trust: "You can’t have a functional relationship without trust, it’s the foundation of everything a trustee does. Trust is built over time through things such as open communication and listening, reliability and professionalism. It’s essential to make sure that the settlor’s wishes are properly carried out and that the assets are managed in the best interest of the beneficiaries: that’s a heavy responsibility."

“It comes back to communication and understanding, and right now there is an ever-greater impetus than before,” this expert observed. “For example, I had a client some six weeks ago who needed a trust for his family business, but then, sadly, he passed away last week of the Covid-19. We did nevertheless manage to achieve his goals and wishes.” But the clear message is to be more proactive and take matters in hand much earlier, whenever and wherever possible.

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “While legacy plans and structures should reflect a client’s intentions or how he wants to be remembered, a robust succession plan must also include clear, honest intergenerational dialogue about family values and governance, next generation development, and social and environmental issues that matter to them. This will build trust between the generations. Hence, it is essential to listen very carefully to a client's requirements, understand the family dynamics and unique challenges before customising a robust succession plan with an enduring structure.”

The panel also discussed what happens if there are no natural family successors to the business. An expert commented that there were various alternatives, such as a sale, strategic partnerships, management buyouts, but that the key issue was to address these matters of succession and control as early as possible, and not at the eleventh hour. Another guest remarked that if it appears there are no natural successors, then professional management teams could be brought in and the family gradually transition from running what had been a purely family business.

Trusting your trustee

The role of the trustee is central to any well-planned and well-structured plan. “The trustee is typically the trusted party that all the family members should be able to go to, and it should be the trustee having those discussions with them about family governance,” said one expert. “The expression of wishes to guide family members and set the tone can be very simple; it can be just the basics, for example a letter of wishes, or some very simplistic family governance document, all of which is very helpful. However, even the bare minimum is often not put down on paper, it is very often informal discussions that the trustee has with the settlor, and also very often, even the protector in trust is not aware of the exact intentions of the settlor.”

Expert Opinion - Kate Weiss, Managing Director, New Zealand, Asiaciti Trust: “An independent fiduciary like Asiaciti Trust with multi-jurisdictional expertise is well-placed as a dependable resource to help business families address these challenges. As a second generation family-owned business founded in Asia, we take a long-term view in our strategic decision making, guided by our core principles and the needs of our clients. Trust, breath of experience and deep expertise are critical considerations in the selection of service providers.”

He explained that over the last two decades, the trustee role had evolved dramatically. While the trustee historically had been the trusted appointee of the family, who knew them well, their dynamics, their problems and so forth, the world had transitioned more and more into a universe of bank and corporate trustees who had an increasingly mechanical role. He warned that it is a major risk if the trustee becomes little more than a box ticker.

He also explained that his strong preference and hope is for the trustee to actually be seen as what it was in the past, namely as a trusted person for all the family members to go to, and for that to happen the trustees must realign themselves by really understanding the families rather than just doing a mechanical job.

“It might be a somewhat romantic view of the world, and perhaps the world doesn't work quite that way,” he added. “We all want to make business, and complete structures and projects, but it is also generally the case that the more you raise such questions, the further it brings you away from closing that business. The risk is that clients might say, well, I did not really want to have these detailed, very personal discussions about my family, my history, my issues, I just wanted to set up a trust, so perhaps I can go to another trustee who just gets it done without making my life so hard.”

He concluded that this type of issue is what good trustees face on a daily basis. “How much do we actually try to even take that sort of role on?” he pondered. “How much does it make sense? And how much is it still appreciated by the clients that we take this more proactive role?” And the answer is that in the modern world, it is not always so clear, even if the trustee’s intentions are entirely right and honourable.

Another panellist concurred, adding that the more the various Trust Related parties are given a certain amount of information about the trust, the easier it is to help create a lasting structure that is understood and appreciated by all (or at least most of) the beneficiaries. This is particularly the case if the settlor retains all control, information and knowledge to himself or herself only, so if it transpires that they simply did not have time or focus to do this before they pass away, this can create a lot of tension amongst the family. “We have seen first-hand some examples during this pandemic, where sadly deaths occurred well before the family might have normally anticipated,” she said.

“It is the case,” they added, “that the closer the trustee is with the various beneficiaries, the easier it is to understand the dynamics in the families and can foresee potential conflicts or issues. But the work of a trustee becomes more and more “mechanical” due to the ever-increasing regulatory pressures and we need to tick a lot of boxes. However, it is more important than ever to have an inclusive approach and to make sure the entire family buys into the concept of wealth/succession planning and knows the benefits of a trust structure.”

Another banker concurred, adding that the act of establishing the trust structure was made more difficult these days by so many families have assets, family members, business and lifestyles in multiple jurisdictions.

“You will need to involve a lot of advisors, onshore and offshore trustees, bankers, lawyers, accountants and other parties when you set up the trust,” she commented. And that, she said, is where the role of the wealth planner can really assist the process, almost like a project coordinator. “My view is that for a wealth planner, because they know all the requirements, should be the ones who coordinate and help set up the structures,” she advised. And then once the structure is set up, the trustee should handle things on behalf of the entire family, with a strong eye on governance throughout.

A fellow panellist agreed but warned that sometimes clients think they just want a simple, commoditised solution, without realising that probate avoidance, retention of control and full asset protection do not simply go hand in hand.

“You have to take them, if possible, through deeper conversations,” she said. “Some people are happy to have that conversation, others are not. However, we find that increasingly, clients are also asking for the full pros and cons of the entities, the structures, and all the issues involved.”

She added: “You just have to start with the client and hope that they are going to be comfortable and have that more prolonged conversation and realise that if they want something sophisticated, it's not going to be an off-the-shelf solution.”

She also offered a word of caution to those families that simply had BVIs or other simple structures, and little or no thought around estate and succession planning. “You have to point out to them issues surrounding these offshore structures, probate, what might happen if they lose mental capacity and so forth. If people in Asia see this as a commoditised product, we have to explain to people that actually, and increasingly, this world is getting more complex and more sophisticated and they really do need to stop, think, take proper advice before they take the plunge with these types of structures.”

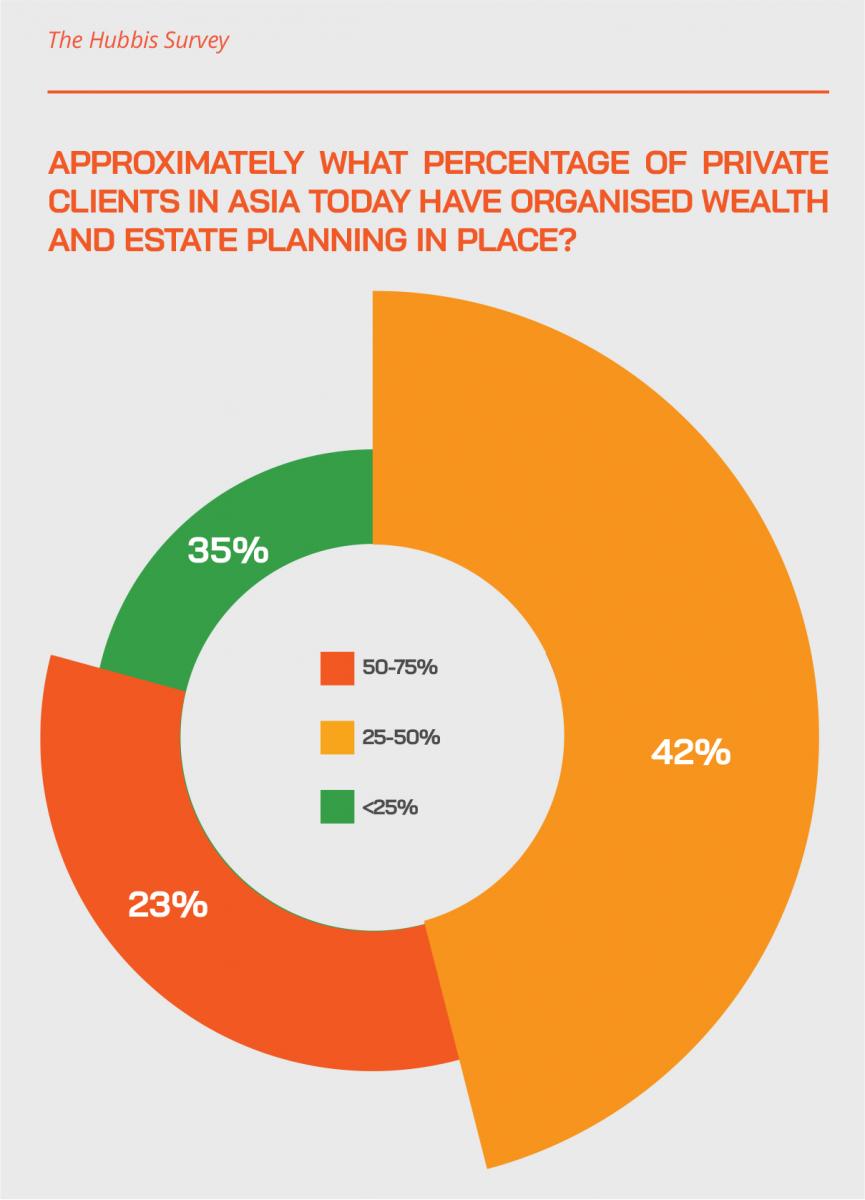

In your experience, are Asia’s HNW and UHNW individuals and families addressing the key issues properly and achieving the right outcomes for their legacy and succession planning and structures?

- As they are often only just discovering the issues, they have a lot to learn still.

- Not yet, although they are slowly waking up to the need to have a robust, future-proof structure in place. An offshore BVI company is no longer sufficient as it was some decades ago.

- They are addressing these issues in a somewhat ad hoc manner. They are not yet holistic in their approach.

- They are beginning to address the key issues properly but a lot of first generation patriarchs may have originally had fairly simplistic goals when thinking about the process. As time has gone on, they will have had to perhaps modify/rethink those rather simplistic plans.

- Inching ahead, but room for a lot of improvement.

- Yes, in Asia, HNW or UHNW clients are normally covered by maybe 3-5 bankers, and most experienced bankers now cover this topic professionally.

- I would say 50/50 and it's due to the culture of Asia's HNW and UHNW individuals and families as some of them have concerns about establishing either a revocable or irrevocable trust.

- Less so in Asia than in other parts of the world (especially Europe) but that can be explained by the fact that the wealth is not as old as in Europe. Nevertheless, the trend is certainly towards a much deeper understanding of these issues by Asian families.

- Progress yes, but these families still need time to get educated, and there is still a long way to go despite some major advances in the past five years.

- Yes, they are increasingly consulting different professionals in the respective areas to set up the structures properly.

- Many of them are still on a learning curve, and slow. Asian families tend to be more conservative and usually will just follow the wishes of the patriarch or matriarch.

- An increasing number of these families are taking this seriously, but it remains our responsibility as advisors to ensure they do and seek appropriate advice and solutions.

- We find more and more families willing and able to address the key issues and achieving the right outcomes with good succession planning and suitable structures.

- It varies tremendously and is often also dictated by the ability of the wealth owners/generators to bring the younger generations to the table.

- They essential element is obtaining professional advice, and some are still not really willing to do that and to pay get proper advice.

- In the past this has been more commodity driven, but many families are now multi-jurisdictional and therefore are being forced to consider the issues properly.

- Actually, in markets like Malaysia, we don't have the experts who know all the answers and what the clients should do exactly.

- These HNW and UHNW families tend to be large in Asia and increasingly want to set up succession planning and structures to continue to achieve the right outcomes.

- If they are willing and open to take professional help then yes but without it they sometimes don't see the bigger picture or can be somewhat naïve in thinking that ‘everything will just work out ok’.

- This needs to be approached cautiously – money easily obtained, especially that which is unearned, can have the habit of corrupting, which lots of people fail to fully appreciate.

- It depends on the families and specific situations, and it sometimes can be difficult to address key issues if there are substantial internal family conflicts.

- Asian clients normally need to take a long time in the communication process in order to get the right structures for their needs in the building of their succession plan.

Delivering advice and structures across multiple jurisdictions

It’s all about working together, according to one panellist, addressing the issue of how estate planning specialists at the banks can work with the various professionals to achieve the best outcomes for clients. “When working with business succession, there are likely to be multiple sets of advisors,” they reported. “Take a simple family with a Patriarch who has two sons. In this case, the patriarch may have his own lawyers, accountants, bankers and trustee, as might each of the children. All of these advisors are likely to need to be involved in the succession planning.”

They said it is therefore vital that the different experts have mutual respect for one another and recognise that just because one advisor has a plan, it may not be the best for all the family members.

Multiple jurisdictions are also inherent in wealthy family businesses, as there are likely to be business units in multiple jurisdictions as well as family members living in all sorts of different locations, all of which have their own rules. “In these situations, as with all estate planning, it is important that tax planning does not drive the family succession, but that the objectives, traditions, behaviour and values of the family drive these decisions,” a panellist advised. “Once these have been determined, the tax planning, asset protection and timing of the business succession can be more effectively addressed.”

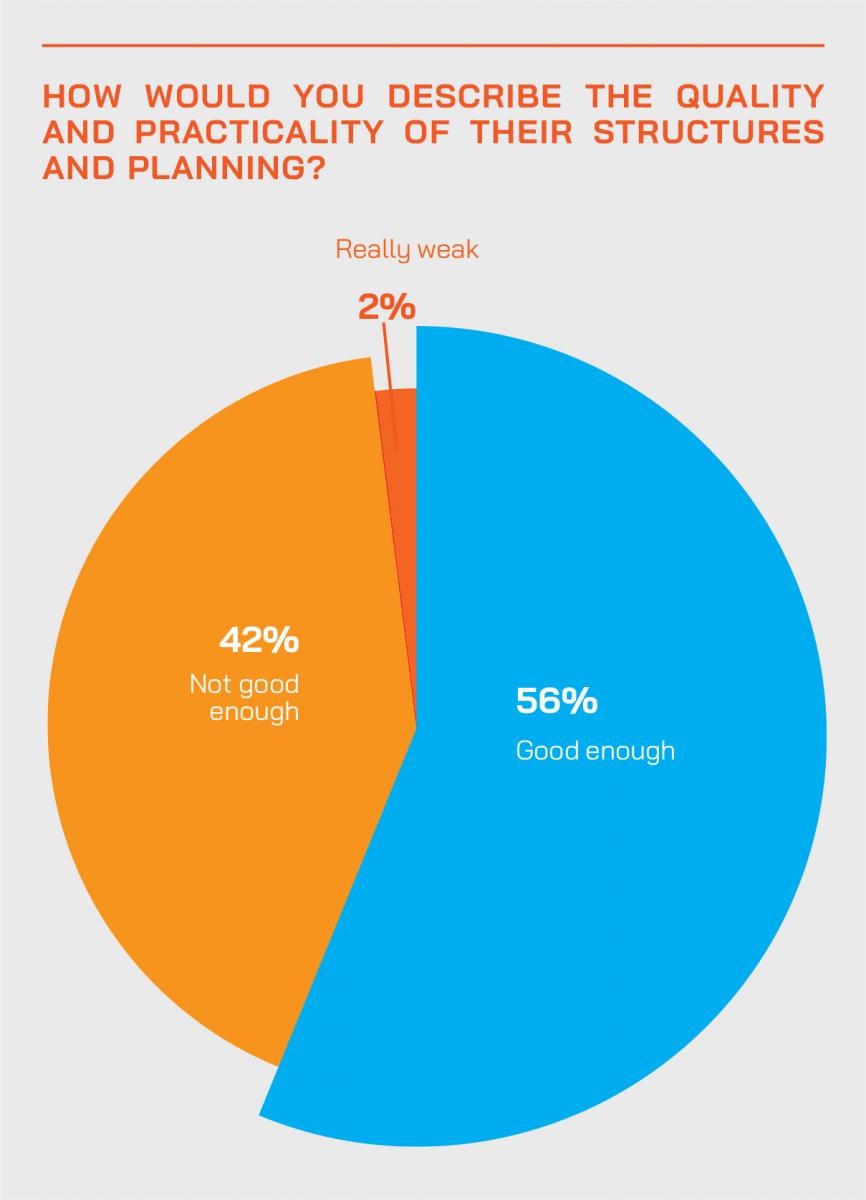

Are the private banks and the independent wealth firms providing robust support for these developments, or are they lagging behind, and why?

- They all play their respective roles, but it's never just one source of information these clients require.

- Could be better, but the real challenge is for Asian clients to become more open minded towards discussions.

- Yes, the private banks and independent wealth firms are nowadays providing robust support.

- We find that only very few banks are actually taking the initiative.

- The independent wealth firms probably lag behind but that does not mean that they cannot have a robust panel of trusted third-party providers that they work with to fill in gaps.

- Not exactly, because of many conflicts of interest.

- Yes, they have poured more resources into trust, estate and succession planning.

- Most of the private wealth departments do not have the expertise to properly advise on this topic, but they can bring along the external experts that clients need in order to be comfortable to share information and build the right solutions.

- We think private banks and Independent Wealth firms are providing robust support as they could see this scope of business is the trend and could provide clients a one stop solution and make the assets ‘stickier’, including for future younger generations of clients.

- They are seen as more proactive and supportive to address to these important clients requirements. However, they still have further room for improvement.

- They need to be constantly upskilling themselves, and they need to work more closely with the regulators and other authorities.

- From our perspective, yes, the private banks and the independent wealth firms are working closely with the professional firms to serve their clients nowadays on these important areas, as a core part of their mission and to protect their futures as well.

- They are lagging behind because they missed the point in developing this solutions and focus solely on the transactional revenues, rather than maintaining client relationships for the longer-term. The short-term mentality needs to give way to take private banking to what it was, which is to work with clients for the longer-term.

- They are more helpful certainly but still have an agenda. A separate succession expert, with relationship with banks, trusts and wealth firms would probably provide better support.

- Certainly, private bankers and wealth managers can and do play a very important role to help develop the families’ succession plans as they play a key role in the financial management and planning, and oftentimes they actually have a bigger picture view and better insights than other individual professional services providers, such as lawyers, trustees and so forth, who approach these matters from their own angles.

Disputes and how to avoid them

On the issue of whether enough is being done to mitigate or avoid family disputes, a panellist explained how trustees historically (and many still today) see the settlor as their ‘client/customer’ and they often forget that the settlor actually hands over the legal ownership of the assets in trust to the trustee and the trustees act in the best interest of all beneficiaries and not only to the wishes of the settlor. One additional aspect to bear in mind is that often trusts have Protectors who play (or should play) an important role as well.

Family feuds at the heart of big companies such as Samsung show the damage that can arise from avoiding difficult conversations, said one guest. Most families say that there will be no family disputes and an informal arrangement is sufficient. A guest said that patriarchs often tend to believe that the next generation ‘know’ what they want and how to put it in place. But sometimes what one person might say, and another person hears are very often two totally different things.

“I see this on a personal level in my own family,” this expert commented, “with my mother, father and brother perhaps having had a conversation and a week later, I discuss it with my brother and perhaps he has a totally different recollection from mine. Communication, reaching agreement and documenting that agreement is therefore key to reducing the risk of family disputes at a later stage. It is important to understand that business succession is a dynamic topic. Unfortunately, it is not just enough to have one meeting and think everything is sorted. It is also important not to ‘force’ a succession. The succession planning needs to go through a series of steps before the plan is even put together to ensure it is a success.”

Another guest returned to the importance of proper communication of wishes. “The trustees always go as per the wishes of the settlor, which is obviously the binding bond and the trust deed, and the more informal guidance in the letters of wishes,” he said. “But I can cite one example where the settlor had a long-established trust for the benefit of his family, but he made certain changes that he never communicated with his family. I suggested several times that he might share the changes with the wife and children, but he did not. He had changed things to exclude US beneficiaries, knowing that one of his daughters was going to move to the US, and then he passed away due to Covid-19 and his daughter, suitably lawyered up, was then coming to us very disappointed. But the settlor’s wishes were hard coded after the changes he made.”

He added that a positive to come out of the pandemic, one that is also in part driven by the intensifying global regulatory pressures, is increasing rationalisation and consolidation of structures. “A major positive for us is fewer structures, fewer trusts and better overall planning and organisation,” he reported.

Expert Opinion - Clifford Ng, Partner (Hong Kong), Zhong Lun Law Firm: “Is enough being done to mitigate or avoid family disputes? Well, as a lawyer, parties will generally find that avoiding disputes occurring in the first place cost much less than resolving them after litigation or after the dispute has surfaced in the relationship. Family disputes often build up over many years and there is not a lot of lawyers or other advisors who come on the scene intermittently can do to help resolve things.

The Final word

A fascinating and highly informative discussion closed with panellists agreeing that these are vital topics for Asia’s private clients to address, and that it was even more essential than ever before for the combined expertise of the wealth management and professional services industries to collaborate to help these clients achieve the best thought out, best designed and best executed structures and solutions.