Wealth Solutions & Wealth Planning

Amendments to Indian Tax Residency Rules: an Overview

Surabhi Marwah of EY

Jun 26, 2020

Surabhi Marwah, Partner, People Advisory Services and Private Client Services Co-Leader at EY, shares her insights on the changes to the Indian tax residency rules.

By Surabhi Marwah, Partner, India, EY

The Indian tax authorities have brought in two major amendments to the Indian tax residency rules for individual taxpayers. These changes are effective from fiscal year 2020-21, and will significantly impact Indian citizens and Persons of Indian Origin (PIOs).

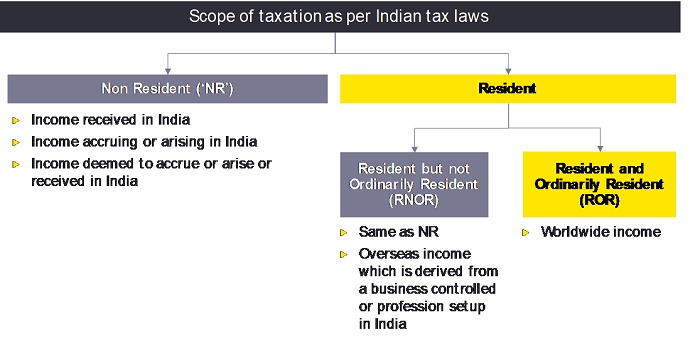

Taxation in India is (or was prior to this amendment) predominantly dependent on the residential status of an individual. The domestic tax law divides individuals into three categories, namely, Resident and Ordinarily Resident (ROR), Resident but not Ordinarily Resident (RNOR) and Non-Resident (NR).

Pictorial representation for scope of taxation for different categories of individuals:

Let us now discuss the rules to determine residency and the amendments related to PIOs and Indian citizens.

An individual is treated as a resident if he/she is:

- Physically present in India for 182 days or more in the relevant fiscal year (182-day rule), or;

- Physically present in India for 60 days or more in the relevant fiscal year and 365 days or more in aggregate in four preceding fiscal years (60-day rule).

If none of the above two conditions are satisfied, the individual is treated as an NR.

A resident individual is treated as RNOR if he/she satisfies any one of the following conditions:

- He/she has been an NR in 9 out of 10 fiscal years preceding the relevant fiscal year.

- His/her physical presence in India is less than or equal to 729 days during 7 fiscal years preceding the relevant fiscal year.

If none of the above two conditions are satisfied, the individual is treated as an ROR.

The rules are a bit different for PIOs and Indian citizens:

- An Indian citizen who leaves India as a member of the crew of an Indian ship, or for taking employment outside India, will qualify as NR if he/she is physically present in India for less than 182 days in the relevant fiscal year (i.e., the 60-day will not apply).

- An Indian citizen or a PIO who is based outside India and comes on a visit to India will qualify as NR if he/she is physically present in India for less than 182 days.

- First amendment (to the above): Effective fiscal year 2020-21, the said limit of 182 days is to be reduced to 120 days for individuals who have India-sourced income exceeding INR1.5 million in the relevant fiscal year. Further, such individuals will qualify as RNOR if they are physically present in India for 120 days or more, but less than 182 days in the relevant fiscal year, and physically present in India for 365 days or more during 4 fiscal years preceding the relevant fiscal year. Below is an illustration explaining the impact due to this amendment under different scenarios:

.jpeg)

*RNOR if qualifies as an NR in 9 out of 10 preceding years or has stayed in India for an aggregate period of 729 days or less in the preceding 7 years; else ROR

- Second amendment: Effective fiscal year 2020-21, a concept of deemed residency has been introduced. An Indian citizen having India sourced income exceeding INR1.5 million during the relevant fiscal year will deemed to be an RNOR in India if he/she is not liable to tax in any other country by reason of domicile or residence or any other criteria of similar nature. As per various publicly available official documents, it was introduced as an anti-abuse provision to discourage High Net Worth Indian Citizens (‘HNI’) seeking to avoid paying taxes in India by becoming non-residents in India and overseas. It is basically to bring Indian Citizen taxpayers who are stateless, to tax in India.

In the ensuing paragraphs, we have discussed some of the pertinent questions which most of impacted individuals may have about the amendments.

- What is to be included while computing the INR1.5 million threshold?

Though clarity is awaited from the authorities, it is currently interpreted to include the below:

-

- Income that accrues or arises in India or is deemed to accrue or arise in India;

- Income that is received in India or is deemed to be received in India;

- Income that accrue or arise outside India but is derived from a business controlled in or a profession set up in India.

Further, any exempt income should not be included while evaluating the INR1.5 million threshold.

- The deemed residency concept sets out the concept of ‘liable to tax’. What is it and why is it important?

In the Indian context, where a country has the right to tax, it is interpreted that the individual is “liable to tax”. It is irrelevant whether such right is exercised or not. The term ‘liable to tax’ is different from “subject to tax” or “exemption from tax’ or “non-payment of tax’ or ‘not being subject to tax’. It can be better explained through the examples below:

-

- Income is taxable in a country, but due to specific exemption provided on fulfilment of certain conditions, the individual does not pay any taxes on that income. In such a case, it can be said that the individual is ‘liable to tax’ even though there is no actual payment. The deemed residency rule will not trigger in such a situation.

- Income is earned in a country where there is no personal tax regime, i.e., zero tax jurisdictions like UAE and other middle east countries. These countries do not levy any income-tax on individuals. One interpretation suggests that if the individual is a resident of a zero-tax jurisdiction, he cannot be treated as stateless and hence cannot be a deemed resident of India, whether or not such jurisdiction levies any personal tax. Representations have been made to the authorities to provide guidelines on this matter. However, till the time we have such guidelines, the more conservative view is that individuals who are from zero-tax jurisdictions are not considered liable to tax and hence will qualify as deemed residents of India under the amended residency rules provided their India sourced income exceeds INR1.5 million. Where the later view is taken by the Indian tax authorities, these individuals can explore breaking their residency under the Double Tax Avoidance Agreement signed between India and the other country (tax treaty). If they are treated as a resident of the other country under the tax treaty, the benefits which were available to them prior to the amendment will typically continue to be available.

· If the foreign income is not taxable for new category of RNORs (deemed residents and individuals crossing 120 days threshold), what is the rationale behind introducing such new category?

Under the domestic tax laws of India and for the purposes of a tax treaty an RNOR individual is treated as a resident for application of various provisions related to exemptions, deductions, tax rates etc., even if such resident individual is not taxable on his worldwide income in India like an ROR. Some practical situations:

o An NR gets a preferential tax treatment on capital gains from unlisted shares over an NOR or ROR under the domestic tax laws of India

o An individual has dividend income from India. He/she qualifies as a RNOR under the domestic tax laws but a resident of other jurisdiction after applying the ‘tie-breaker rule’ of the treaty, he/she will be able to avail beneficial rates provided under the treaty for on such dividend income.

Example: Under the domestic tax laws, in case of residents, dividend income is taxable at slab rates, highest rate being 30%. (plus surcharge and cess) whereas NRs can enjoy concessional rates provided under the treaty (e.g., India – UAE – 10%; India - Hong-Kong – 5%)

Given the amendments, it has become important for PIOs and Indian citizens to plan their tax matters meticulously. PIOs and Indian citizens who come on a visit to India and would like to maintain NR status can either limit their stay below 120 days or plan their India sourced income to remain below INR1.5 million where they can enjoy the enhanced limit of 182 days.

On the other hand, Indian citizens based out of zero tax jurisdictions, in light of the arguments given above, will be better placed if they maintain their residency in the other jurisdiction in order to neutralise the impact of being a deemed resident under the tax treaty.

All views express are personal.