Wealth Solutions & Wealth Planning

How to service Chinese wealth as it goes global

Jun 9, 2017

The last few years have seen explosive growth in understanding among Chinese HNW and UHNW individuals of wealth structuring and transition. Yet wealth managers and professional services firms continue to grapple in navigating what is a tricky regulatory and cultural landscape.

It is with this in mind that Hubbis – in conjunction with Jersey Finance – conducted this research in May 2017.

It involved an online survey of more than 60 wealth management and professional services practitioners across Hong Kong, Singapore and Mainland China.

The aim is to follow up on the detailed research done in October 2016, to understand how the current landscape is impacting wealthy Chinese and their approach to succession planning, wealth transfer and offshore investing.

Key survey takeaways

Key survey takeaways

• Legacy planning is the key consideration for PRC families today - 47%

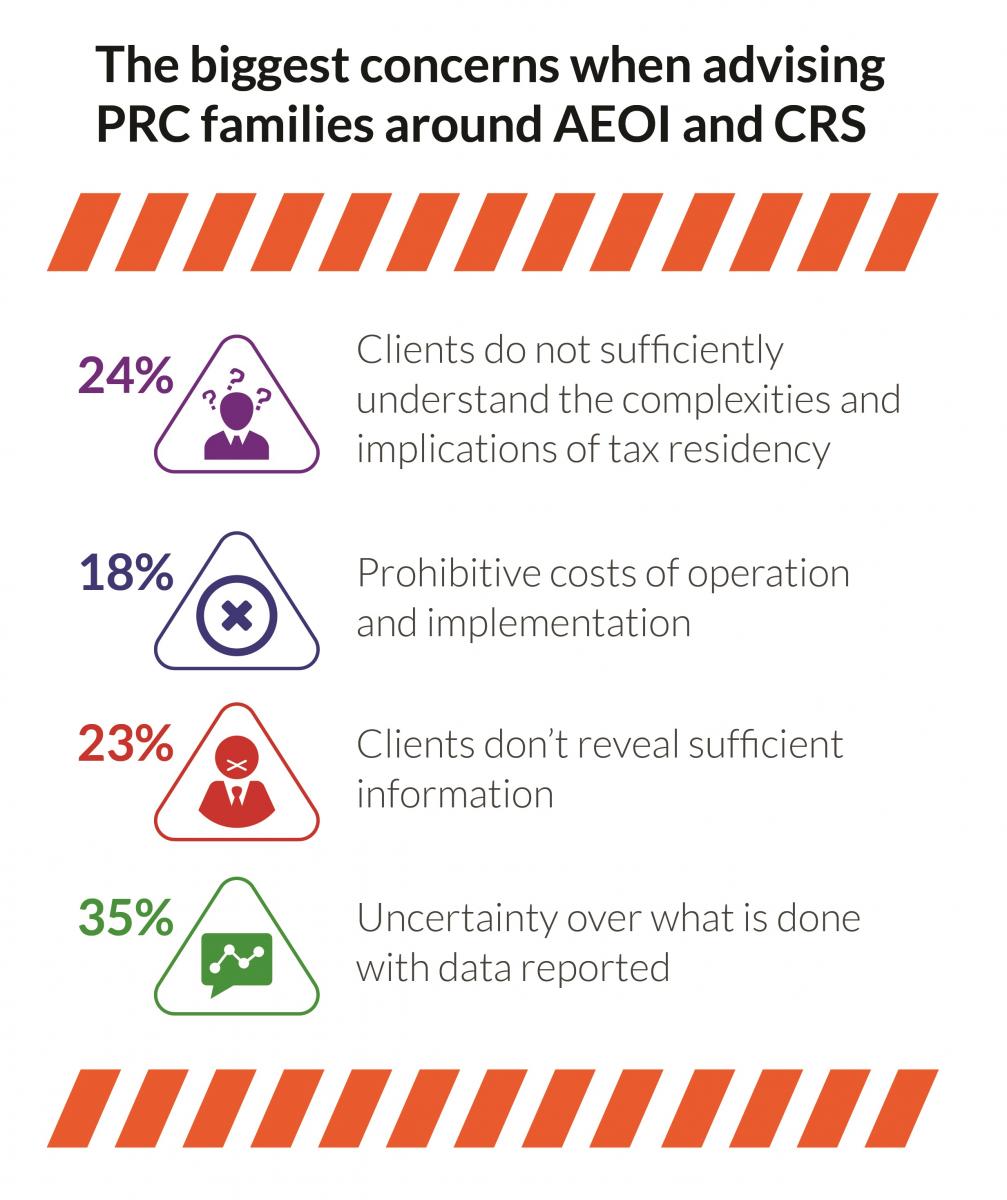

• The biggest concern when advising PRC families around the Automatic Exchange of Information (AEOI) and CRS is that clients don’t reveal sufficient information - 35%

• The top factor holding PRC clients back with wealth transition stems from misconceptions about the issues and solutions - 59%

• The biggest misconception PRC families have with wealth structuring is loss of control - 88%

• The most popular structure among PRC families today is trusts - 47%

• Family disputes are most likely to derail estate / succession planning for PRC clients - 41%

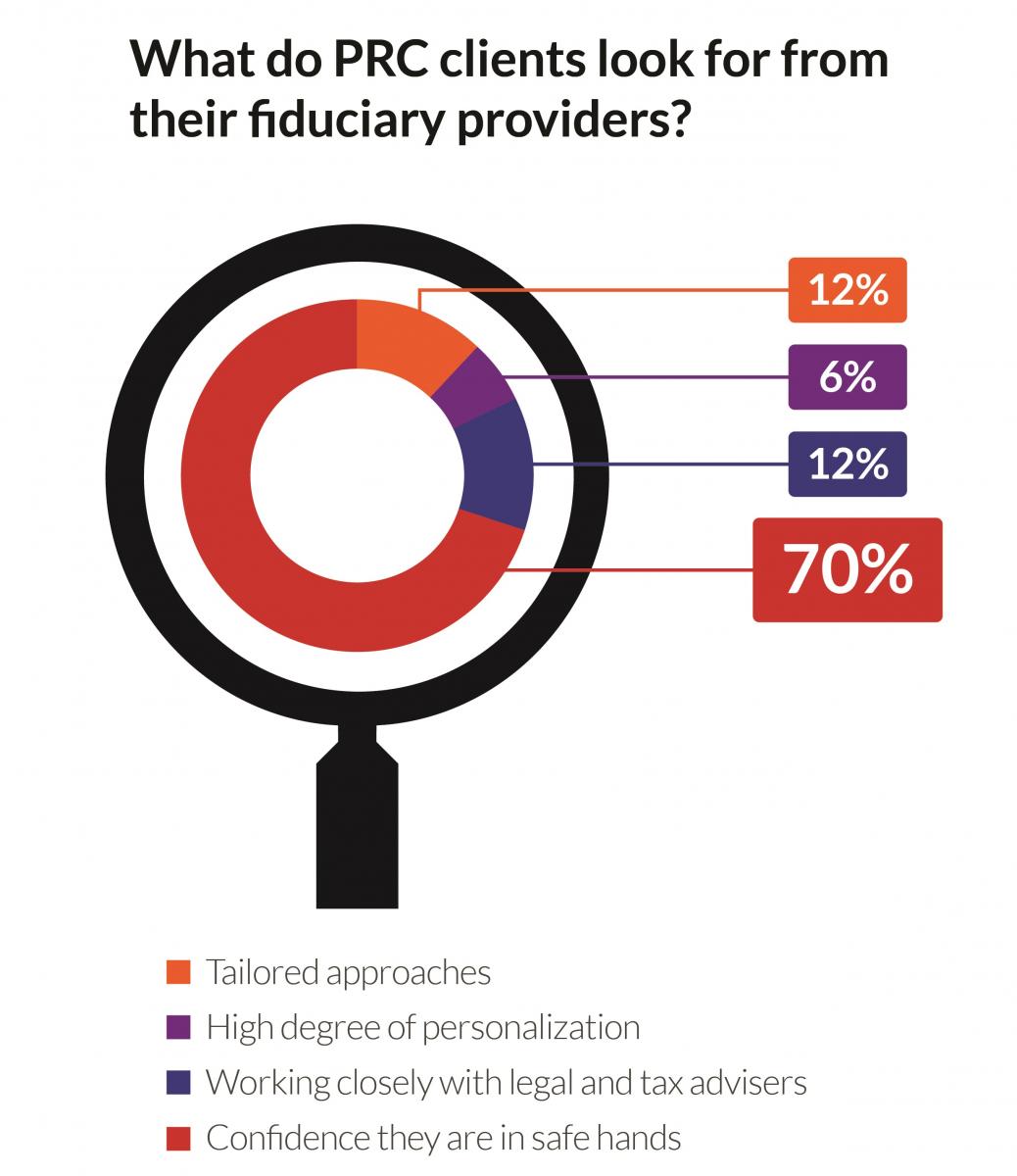

• When choosing their fiduciary providers, PRC clients mainly seek confidence that they are in safe hands - 70%

Servicing Chinese wealth

Broadly, helping Chinese HNW clients to diversify, protect and pass on their wealth is no different in concept than it is for their peers in other countries.

They face similar succession issues as individuals from many other countries. So standard asset protection structures such as companies, trusts and private trust companies are equally relevant.

More specific to China, there is a drive by wealthy individuals and families for globalisation of their wealth as well as their families.

The challenge, however, is the time it takes to get Chinese clients comfortable with the concept of structures such as trusts and the responsibilities involved, as well as what it means to cede control of their assets.

As a result, the starting point is to understand their needs and then help them get familiar with the risks of doing nothing.

There are two key peculiarities with China:

• Firstly, many HNW individuals in the mainland are younger than in other countries, so might not have the same urgency to plan for a generational shift

• Secondly, they can’t invest easily in their own country due to lack of products, so a challenge exists in selecting investment opportunities overseas

As a result, any structuring is offshore, where these clients can use common structures such as trusts and offshore companies.

However, as with all HNW clients, they have to be made to understand that wealth preservation isn’t just about investing assets. It can also be a part of developing a succession plan and getting the next generation involved.

In line with this, in a jurisdiction that has become increasingly ‘clean’, advisers need to be aware of and comply to global standards on regulation.

The increased scrutiny of overseas transfers has also made it more of a struggle for clients to move money from the mainland.

Either way, some key guidelines that experienced market practitioners say they follow include:

• Increase checks to ensure advisers don’t inadvertently help clients to transfer funds out of China in excess of the annual allowance

• Assume even the most confidential structures are available for inspection by tax authorities

• Tax should not drive structuring decisions

• Don’t make the client’s problem your problem

• Focus on wealth that is either already outside of China or is about to be deployed outside of China

• Deal with clients from licenced offices outside of China

What is considered the right advice in China is, therefore, a changing concept.

While tax planning is relatively straightforward at the moment, this is likely to change.

The Common Reporting Standard (CRS) and other reporting, as well as increased restrictions on capital flows, and reforms to immigration programmes and property ownership taxation rules (such as in the UK and Australia), result in a need to adapt.

Further, advisers and clients must be mindful of tax changes coming to Individual Income Tax laws, and possible estate duty in the PRC.

The initial impact of this is simply that it will require existing structures to be reviewed.

Meanwhile, to find and access PRC clients, advisers should aim for the next generation, who tend to be more open and understanding of the need to act. This is partly because they have more of a global influence due to their (often) overseas education.