Can your child bring you into the tax net? Perhaps, perhaps, perhaps.

Fiona Poole of Maurice Turnor Gardner

Aug 30, 2018

It might also be necessary for the parents to get their own affairs in order and ensure that their child’s presence in the UK does not make them inadvertently UK resident.

by:

Fiona Poole, Partner

Sarah Conway, Partner

Colin Senez, Associate

Maurice Turnor Gardner LLP

For some families, a long-standing tradition exists where parents send their children to boarding schools rather than day schools and in many circumstances families living outside the UK will send their children to UK boarding schools in order to offer their children an education best suited to their needs.

Quite obviously, the primary concern when parents embark on sending their children to the UK and to boarding school is without question their children’s welfare, however it might also be necessary for the parents to get their own affairs in order and ensure that their child’s presence in the UK does not make them inadvertently UK resident. If the child is at boarding school and the parents come to visit, then the number of days they can spend in the UK with their child in the UK without acquiring UK residence will depend on a number of factors.

UK tax residence is determined in accordance with a statutory residence test, which is structured in three parts:

- The first part identifies when an individual will be conclusively non-UK tax resident.

- The second part identifies when an individual is conclusively UK tax resident (also known as the “automatic UK” tests).

- The third part is the tie-breaker – and the test on which this article will focus. If an individual does not meet either of the above tests, their residence is assessed in accordance with the “sufficient ties” test which involves a consideration of the time an individual physically spends in the UK with regard to his or her ties or connections to the UK.

Under the sufficient ties test, the statutory principle is that an individual’s residence should reflect not only the time he spends in the UK, but also the other ties he has with the UK. The test identifies a list of connecting factors which, when linked with the amount of time spent in the UK by an individual, will be relevant in determining that individual’s residence status. These “UK ties” are:

- The family tie – the individual has a spouse, partner or minor child who is resident in the UK. A special rule applies to prevent there being circularity: so that if both parents accompany the child, each parent will not represent a “tie” for the other, and, as will be seen below, children at school are treated slightly differently.

- The accommodation tie - the individual has a “place to live” in the UK available for use for a continuous period of at least 91 days, and the individual does in fact make use of it at any time for at least one night during the relevant tax year. An accommodation does not need to be owned by the individual and can include rented accommodation, and in certain circumstances can be a relative or close friend’s house where that individual has a room available to them for a continuous 91 day period. In certain circumstances, the same can also apply to arrangements with hotels where the individual has continual access to a particular room so care needs to be taken when making arrangements to visit the children.

- The work tie – if the individual does 3 or more hours of work in the UK on at least 40 or more days in a tax year (whether continuously or intermittently) then they will develop a work tie. ‘Work’ takes its every day meaning and will include work related travel time. For example, taking a laptop with you and working in the UK when visiting your child will give you a work tie if you meet the time and day count, but crucially any work can contribute to a work tie – such as answering work e-mails on a smartphone. It is not unreasonable to assume that an individual might meet the work tie if glued to their phone during their visits to the UK, and if done a 40 day period. In the event of an enquiry, the UK tax authorities have been known to ask for e-mails sent during an individuals stay in the UK if the question of someone’s work tie arises to establish whether or not they have acquired a work tie.

- The 90 day tie –the individual has spent more than 90 days in the UK in either of the last two tax years.

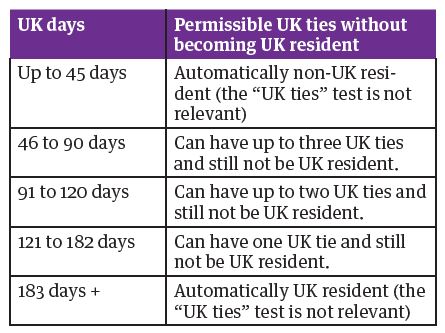

The days that can be spent in the UK are then applied on a sliding scale with the permitted amount of days in the UK without becoming UK resident steadily reducing as the ties an individual has increases:

But, it gets a little more complicated when a child is in full-time education.

If at any time during a tax year an individual has a child under the age of 18 who is resident in the UK, that individual will have a family tie for that tax year. For a child in full-time education, his or her residence status is determined with a slight adjustment to the normal rules – such a child is not UK resident if they spend fewer than 21 days in the UK outside term time.

Time spent in “full-time education” is time spent at school during term-time, including half-term breaks and other breaks when there is no teaching. So any time spent during such breaks does not count towards the 21 days, however normal holidays (e.g. Christmas, Easter and summer) do not qualify as part of term-time so if the child spends more than 21 days in a tax year with a friend or guardian (or even their parent) in the UK, the time-limit may be breached and the child might be treated as UK tax resident.

For the parent of a child in full-time education, the family, work and accommodation ties could be an issue that need to be considered.

Satisfying the family tie test will not, on its own, make someone conclusively UK resident and it is a factor that, in combination with other ties and the amount of time an individual spends in the UK, will contribute towards determining if they are resident in the UK in any one tax year.

As ever, you should not let the tax tail wag the dog – especially where children and their education are concerned, but it never hurts to be in the know and plan accordingly. Inadvertent UK tax residence can be very complicated, but that’s another story for a different article.

Partner at Maurice Turnor Gardner

More from Fiona Poole, Maurice Turnor Gardner

Latest Articles